Scotland's Marine Atlas: Information for The National Marine Plan

Scotland's Marine Atlas is an assessment of the condition of Scotland's seas, based on scientific evidence from data and analysis and supported by expert judgement.

AQUACULTURE

What, why and where?

Aquaculture produces Scotland's most valuable food export. It involves the farming or culturing of fish, molluscs, crustaceans or algae. The industry in Scotland is dominated by farming of Atlantic salmon but also has significant rainbow trout and mussel production. It is also important because of its capacity to produce food rich in omega-3 oils that help to promote health. Although much of the production is exported, aquaculture also makes an important contribution to food security.

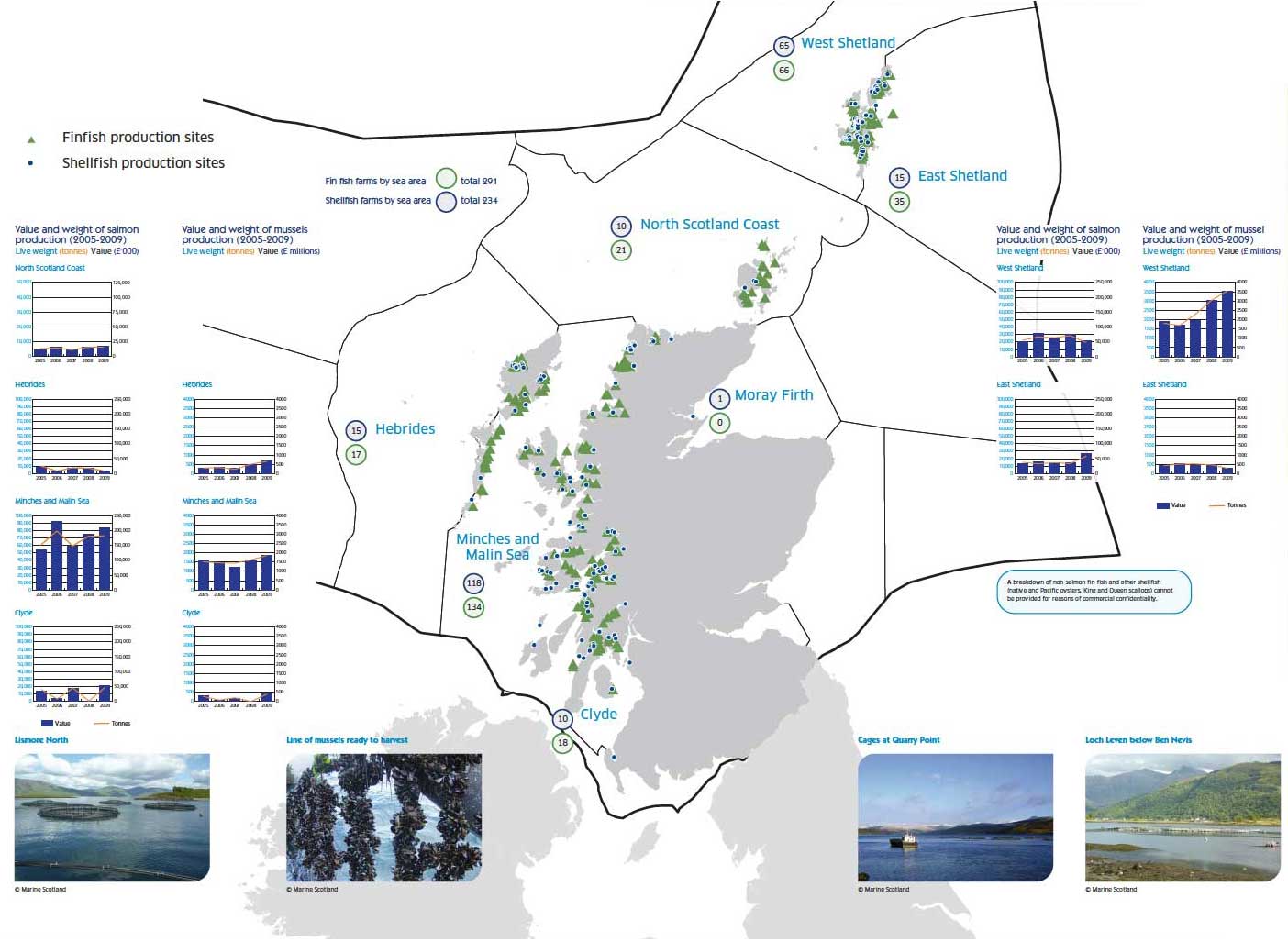

Scotland is one of the three largest producers of farmed Atlantic salmon in the world along with Norway and Chile, and the largest in the EU. 144,000 tonnes were produced in 2009. Rainbow trout (2,620t), brown trout (157t), halibut (69t) and some Arctic charr are also produced. Cod production in 2009 was negligible compared with 2008 when 1,821t was produced. This change was because of the closure of the major production company.

Shellfish production was dominated by blue mussels in 2009 (7,180t). This was an increase of about 36% since 2006. Pacific oysters (2,911,000 shells) and Native oysters (490,000 shells), King (35,000 shells) and Queen (168,000 shells) scallops have also been cultured. All statistics are from the Scottish Fish Farms and Shellfish Farms, Annual Production Surveys 2009 (1)(2).

Aquaculture has been the fastest-growing food production sector in the world, with an average worldwide growth rate of 6-8% per year since the millennium. Global aquaculture has increased by a third since 2000, and currently provides around half of the world's seafood for human consumption (3).

Atlantic salmon production and turnover (2005-2009)

Source: Marine Scotland (1)

Other fin-fish species production and turnover (2005-2009)

Source: Marine Scotland (1)

Mussel and other shellfish - production and turnover (2005-2009)

Source: Marine Scotland (1)

Other shellfish, by species, production and turnover (2005-2009)

Source: Marine Scotland (2)

Contribution to the economy

Aquaculture is a growing and increasingly important industry, helping to underpin sustainable economic growth in rural and coastal communities in the Highlands & Islands. It has a production value (turnover) worth around £427M per year to the Scottish economy, at farm gate prices in 2009. This was composed of about £412M Atlantic salmon, £6M rainbow and brown trout and £0.5M halibut, with £7M mussels, £1.4M other shellfish. Farmed salmon exports are valued at £285M annually. Exports from fish and aquaculture are Scotland's largest food export.

Key export markets for Scottish salmon include major European countries such as France, Belgium, Netherlands and Luxembourg. The USA became the number one export market for Scottish farmed salmon in 2009.

The provision of jobs in remote and rural areas is a key benefit. Salmon production supports about 874 full-time and 963 part-time jobs. Trout and other finfish production and processing support about 134 full-time and 183 part-time jobs with shellfish supporting about 169 full-time and 345 part-time jobs. (1)(2)

A survey of the Scottish Salmon Producers' Organisation members indicates that employees stayed an average of eight years against a UK average for length of service of 5.6 years. 13% of staff were migrant workers.

Production growth in value terms has averaged 4.6% per annum over the period 2000-2009. The salmon sector in particular is now expanding again after several years of contraction, partly in response to the production gap left by the recent collapse in Chilean salmon production, and partly in response to the opening up of new, and strong growth in existing, markets.

Pressures and impacts on Scotland's socio-economics

Positive

- Salmon provides significant food exports

- Employment in remote and rural communities

- Knowledge transfer from university to industry

- Providing healthy food and food security

Negative

- Potentially restricting sea bed use by other users

- Infrastructure may have a visual impact on coastal locations

Locations and production figures of finfish and shellfish sites (2005-2009)

Pressures and impacts on the environment

Pressure theme: Climate change and physical pressures

Pressure: Local water flow rate and wave exposure changes

Impact: Site infrastructure (e.g. pens and floats) has the potential to alter tidal currents and wave conditions.

Pressure theme: Pollution and other chemical pressures

Pressure: Synthetic compound contamination

Impact: The dispersion of chemicals (from treatments, spills, food and faecal matter) has the potential to be toxic to benthic species.

Pressure: Non-synthetic compound contamination

Impact: Antifoulant paints and fish feed have resulted in elevated concentrations of copper and zinc in sediments. Discharges of chemicals can be toxic to benthic species.

Pressure: De-oxygenation (in the sediment and water column)

Impact: Breakdown of organic matter, e.g. uneaten food, can create a Chemical and Biochemical Oxygen Demand ( COD and BOD), which can lower oxygen levels and affect local biodiversity.

Pressure: Organic enrichment

Impact: Deposition of particulate waste (faecal material and uneaten food) beneath cages may result in de-oxygenation of sediments. Shellfish species can also produce waste e.g. 'mussel mud' (faeces).

Pressure: Input of nitrogen and phosphorus

Impact: Excretory products and decaying food release ammonia and salts of nitrate and phosphate. This can contribute to eutrophication and possibly to Harmful Algae Blooms.

Pressure theme: Other physical pressures

Pressure: Litter

Impact: Litter, such as broken nets, plastic pipes and metals, impact on marine species through ingestion, entanglement and smothering.

Pressure theme: Habitat changes

Pressure: Habitat structure changes

Impact: Some underwater infrastructure can abrade the seabed; harvesting of shellfish (if dredged) can cause damage; use of materials to encourage settlement of oysters can cause damage.

Pressure theme: Biological pressures

Pressure: Sustainability of fish feed

Impact: Feeding using wild-caught fish from a lower trophic level may deplete wild stocks. UK industry accounts for 4% of total world-wide fish-oil consumption.

Pressure: Introduction or spread of non-indigenous species and interaction with wild species.

Impact: Escapees interbreeding with wild populations resulting in losses of genetic variability, including loss of naturally selected adaptations.

Some mariculture species can cause habitat modification and trophic competition with indigenous species.

Cages provide potential substrate for non-native species such as caprellid shrimps and colonial sea-squirts (e.g. Didemnum).

Pressure: Reduction in plankton levels

Impact: Overstocking of shellfish could lead to reduction in the standing stock of phytoplankton.

Pressure: Increased numbers of sea lice

Impact: Infection of wild salmonids by sea lice from farmed fish.

Pressure: Introduction of microbial pathogens (disease)

Impact: Parasites and diseases are part of the natural biology and functioning of ecosystems. Disease can move in both directions between farmed and wild fish.

Pressure: Settlement of cultivated species outside sites

Impact: Shellfish larvae can overspill into the surrounding environment, creating new habitat and biomass for others e.g. waterbirds.

Pressure: Management of other species that impact on aquaculture

Impact: For example, taking or killing of seals to protect salmon stocks and prevent damage of aquaculture cages.

Source: Based on CP2 PSEG Feeder Report Table 3.8 (4) and UK Marine Policy Statement (5)

Mussel farm

© Marine Scotland

Unimpacted seabed in the vicinity of a well managed fish farm: brittle stars, common sea urchin, kelp and shell debris present

© Marine Scotland

Forward Look

The immediate prospects for Scottish aquaculture are good. The salmon industry is thriving due to the worldwide effect on demand of the collapse in Chilean production and the opening up of new markets. A recent Institute of Aquaculture report (6) suggests that the prospects for mussel farming are good, in some part due to a decline in Dutch mussel production. Scotland is well positioned to contribute to continued growth in the EU, in line with the EU Aquaculture Strategy.

The global demand for seafood, driven by such factors as the need for protein for an expanding population and the need to replace land-based sources suffering from climate change, is likely to increase demand for Scottish production. The salmon industry has identified a significant opportunity for growth in the next five years. In the 2009 European Fisheries Fund awards, grants to the mussel sector were made which could alone lead to a further increase of more than 2,000 tonnes of production.

The stated desire of one company to move to off-shore or exposed salmon farms may remove the main spatial constraint on the industry, and could herald the next stage of aquaculture development. Potential sites could be over twice as large as existing sites and each would therefore represent a significant increase in the value of the Scottish industry.

Given the interest in macro-algae as a basis for biofuel production and other non-food uses over the last five years, and the established Scottish history of macro-algal harvesting, research is underway to assess international progress in this field to inform possible development of this sector.

The proportion of fish meal and fish oil from capture fisheries in farmed fish diets is starting to decline as alternative ingredients are substituted. Most, but not all, of this comes from capture fisheries from stocks primarily from the NE Atlantic and SW Pacific which are considered to be fished at sustainable levels, although there are uncertainties over the sustainability of some. Scottish aquaculture uses about 4% of this global resource.