Scottish National Adaptation Plan: annual report 2025 to 2026

The annual progress report setting out the delivery record over the past 12 months of the Scottish National Adaptation Plan relating to climate change.

Economy, Business and Industry (B)

SNAP3 Outcome: Economies and industries are adapting and realising opportunities in Scotland’s Just Transition.

Climate change poses profound risks to our economy. This chapter sets out four objectives that collectively focus on how Scotland can build resilience to the economic impacts of a changing climate and maximise the innovation opportunities for businesses, people, and communities.

Objectives

B1 – Business understanding of climate risk

Businesses understand the risks posed by climate change and are supported to embed climate risks into governance, investment, and operations, and are collaborating on effective adaptation action

Climate change is increasingly affecting businesses across Scotland, through damage to premises and assets, risks to employee and customer health and safety, and disruption to supply chains.

The Scottish Government’s Adaptation Scotland Programme, working with business support services including Scotland’s Enterprise Agencies, is strengthening advice and guidance on practical actions companies can take to identify, manage and respond to climate risks, while also exploring new economic opportunities.

To support businesses across Scotland, during the reporting period:

- Vulnerable sectors and supply‑chain resilience were supported through the publication of three Adaptation Scotland Industry Insight guides for Environmental Horticulture, Wholesale Food & Drink and Scotch Whisky. Published in August 2025, the guides have been accessed over 2,000 times, helping businesses in these exposed sectors adapt operations and identify new opportunities.

- Adaptation capability across Scotland’s enterprise system was strengthened, with 103 client‑facing advisors across Highlands and Islands Enterprise (25), Scottish Enterprise (17) and South of Scotland Enterprise (61) completing Adaptation Scotland’s Climate Resilience Training between January 2025 and March 2026. This training has enabled advisors to embed adaptation in existing advice, so businesses are supported to better identify and manage climate risks.

- Demand for early adaptation support was reflected by growing uptake of Adaptation Scotland’s practical tools in 2025-26, including over 2,300 accesses of the SME Climate Resilience Checklist and 2,289 unique views of business adaptation webpages. Since its launch in 2025, 161 companies have also completed Scottish Enterprise’s refreshed Net Zero Accelerator, supporting the development of climate plans that address both mitigation and adaptation. Together these illustrate growing business recognition of climate risks to competitiveness.

- Adaptation continues to be mainstreamed into funding and business support, with Scottish Enterprise linking grant funding to net zero planning, specifically through completion of the Net Zero Accelerator tool.

B2 – Support for farming, forestry, fishing and aquaculture sectors

Farming, forestry, fishing, and aquaculture businesses are supported to adapt production and operations in a way that benefits livelihoods, resilience, and the economy in a changing climate.

Agriculture

Land management in Scotland will change as we tackle the twin climate and biodiversity crises which will present both challenges and opportunities for farmers and crofters, building on their traditional leadership role in land management and stewardship.

We have continued to deliver the Agricultural Reform Programme, to deliver our Vision for Agriculture for Scotland to become a global leader in sustainable and regenerative farming.

To support the agriculture sector, during the reporting period:

- The Agri‑Environment Climate Scheme (AECS) continued to support climate‑resilient land management, with over £338 million committed to more than 3,400 farm and croft businesses, including measures to maintain and enhance soils in FY 2025/26. AECS will run until at least 2030 to continue to deliver significant benefits for farmers, crofters and our environment.

- Enhanced Greening requirements expanded the area of land managed for environmental benefit, with new options such as agroforestry supporting adaptation outcomes including improved soil stability and water management.

- The Whole Farm Plan was introduced for basic payment recipients, requiring businesses to undertake proportionate assessments of soil, carbon, biodiversity and animal health. This is supporting improved decision‑making and farm‑level climate resilience, with full coverage required by 2028.

- New requirements for managing areas of peatland and wetland on farm, have been added to Good Agricultural and Environmental Conditions (GAEC6) to allow for the maintenance of soil organic matter.

- The Code of Practice on Sustainable and Regenerative Agriculture was published, providing practical guidance for farmer on climate and nature‑positive approaches, with a strong emphasis on soil health as a foundation for climate resilience.

- The Rural Support Plan (2026–2030) set out Climate Change Mitigation and Adaptation as a core strategic outcome, providing policy certainty and aligning future support with delivery of climate resilience.

The First Minister announced that £14.25 million will be allocated to delivering the Future Farming Investment Scheme (FFIS) for the financial year 2026/27.

Forestry

Forestry in Scotland is worth £1.1 billion per year to the Scottish economy and supports more than 34,000 jobs. Alongside their important economic value, forests have a crucial role to play in mitigating against climate change, tackling nature loss and in supporting the well-being of the people of Scotland.

To support the productivity and increase the resilience of the forest resource and industry, Scottish Forestry, during the reporting period:

- In total, Scotland created 8,470 hectares of new forest or woodland, representing 54% of all UK new woodland creation. 5,300 hectares of native woodlands were created, surpassing the Scottish Government’s commitment of 4,000 hectares set out in the Programme for Government (PfG). This makes Scotland a leader in the UK in woodland creation. However, challenges around woodland removal for electivity infrastructure project equating to 2,800m have meant Scotland has did not meet it’s 10,000 hectares under the PfG and 18,000 hectares under the Climate Change Plan for 2024/25.

- Since 2025, forest plans have continued to play a central role in managing long‑term change in Scotland’s forest resource. All relevant forestry activity is underpinned by the UK Forestry Standard (UKFS), which sets the technical requirements for sustainable forest management and is a prerequisite for Forestry Grant Scheme (FGS) approvals, Felling Permissions, and Forestry Environmental Impact Assessment determinations. Data collection processes are now in place, with a full annual dataset for the period 1 April 2025 to 31 March 2026 due to be collated by October 2026, ensuring future reporting is based on complete and high‑quality information.

Fishing and aquaculture

It is essential that our aquaculture and fisheries sectors are supported to adapt to the impacts of climate change including ocean acidification, which affect the distribution and abundance of marine species.

With regards to fisheries and the aquaculture sector, during the reporting period:

- Fisheries Management Plans (FMPs) are being developed with a clear objective to adapt management approaches to changing climatic conditions and will be reviewed as climate science and management tools evolve. This aims to help build capacity to manage risks to fish stock distribution, abundance and ecosystem stability.

- Work is underway to reduce unwanted catch and bycatch through tailored, fleet‑specific, measures developed collaboratively with stakeholders to help manage risks to stock resilience and sensitive marine species.

- Vessel tracking (i‑VMS) and limited remote electronic monitoring on vessels under 12m are being progressed through the Inshore Fisheries Management Improvement Programme, with implementation targeted for 2026. This aims to help reduce the risks from insufficient spatial data under changing conditions.

- To support long‑term adaptive capacity and innovation, the Sustainable Aquaculture Innovation Cluster (SAIC) has been established to enable the coordination and funding of aquaculture research and innovation through to 2031.

- A wide range of research and innovation is underway to better understand and address health risks that warming waters pose to salmon and other farmed species

B3 – Innovation opportunities

Scotland is a hub for innovative adaptation solutions and opportunities.

To innovate and support innovative approaches to investment in Scotland’s natural capital, during the reporting period:

- The Facility for Investment Ready Nature in Scotland (FIRNS) fund has recently been extended into financial year 2026/27. This round of competitive continuation funding is available for existing grantees to enable projects to strengthen their investment readiness. During 2025 an external evaluator was commissioned to generate robust quantitative data to analyse the fund’s impact. A report will be published by FY Q1 2026/2027.

- The development of a Nature Investment Exchange (formerly Prospectus) to help generate new projects and partnerships that meet policy priorities that tackle the climate and biodiversity emergencies. The project had a soft launch in March 2026, with a database of 22 high‑integrity natural capital projects seeking private investment, with additional projects to be added over time.

- Following extensive research and analysis of blended finance methods being used in the UK and internationally, the 'peatland pilot' was launched alongside the Peatland ACTION 2025 funding round attracting four applications for Carbon Contracts. Final outcomes from panel decisions are still awaited. An evaluation is underway to inform how to develop the scheme for 2026.

- The Scottish Government-NatureScot project to develop an Ecosystem Restoration Code (ERC) for Scotland, in response to CivTech challenge 8.6, concluded in March 2026 with the production of a Competent Model for a new high-integrity mechanism for private investment in nature and biodiversity restoration. The Competent Model sets out: (a) the individual requirements and criteria that ERC projects will need to meet; and (b) the means by which these are validated to evidence compliance.

A strong evidence base is at the heart of innovative adaptation. During the reporting period:

- The Scottish Government with Enterpise Agencies Partners, undertook research, via ClimateXChange, to understand the economic opportunities posed by adaptation – the goods, services and technologies required to adapt. The work focussed on opportunities within the built environment, financial services and food and drink industry; looking to establish if these were near term or future opportunities and where Scotland had existing strengths.

- In shaping the next RESAS Strategic Research Programme (2027–2032), the Scottish Government has explicitly embedded adaptation research as a core priority, at the heart of the research agenda. Published in March 2026, the strategy sets out a bold mission to deliver climate‑positive and climate‑resilient landscapes, underpinned by a dedicated challenge area focused on adapting to climate change. This positions adaptation not as a peripheral consideration, but as a foundational pillar guiding future research, investment, and impact.

B4 – Economic development and supply chains

Economic development is informed by climate risks and opportunities including identifying and managing supply chain vulnerabilities for vital food and goods

It is essential that budget processes and the wider financial system take climate risks into account to ensure that spending avoids locking in risk and instead strengthens preparedness. During the reporting period:

- Budgeting and decision‑making: For the second year, the Scottish Government published a Climate Taxonomy as part of the 2026–27 Scottish Budget, using budget tagging to identify cross‑portfolio expenditure as having positive or negative impacts on adaptation and mitigation. This work is supporting improved medium‑ to long‑term financial planning by increasing transparency over cross‑government spending, including how expenditure can be used to climate‑proof wider investment beyond activities with a primary adaptation purpose.

- Economic analysis to inform medium‑ to-long‑term financial planning: Research scoping Scotland’s investment needs to 2040 across five critical sectors (agriculture, natural environment, transport, community resilience, and the built environment) was published to support improved understanding of medium‑ to long‑term adaptation financing requirements. This work followed an industry, academic, and policy workshop on addressing Scotland’s adaptation finance gap held in spring 2025, where quantifying investment need was identified as a priority action. The research outlines the respective roles of the public and private sectors in meeting these needs and was published via ClimateXChange in May 2026.

- Scottish National Investment Bank (SNIB): Prior to making an investment, the Scottish National Investment Bank conducts a Climate Risk Assessment (CRA) for all prospective investees. The CRA is a structured evaluation designed to identify and assess material climate‑related risks and opportunities, and forms part of the Bank’s due diligence and investment approval processes.

- Climate‑proofing at SNIB: In April 2025, the Bank introduced a Post‑Investment Action Plan requirement, including completion of a short Climate Adaptation Checklist by new investees. This tool supports investees to consider the management of physical climate risks relevant to their business and is based on Adaptation Scotland’s SME Climate Resilience Checklist. Since 2023, the Bank has voluntarily aligned with the Taskforce on Climate‑related Financial Disclosures (TCFD) through publication of an annual report. Aggregated portfolio climate‑risk exposure is captured in the Bank’s 2025 TCFD report, with core elements embedded in the Bank’s Annual Accounts to ensure integration into financial reporting. In Q1 2026, the Bank published Pathway to Resilience: The Bank’s Approach to Adaptation, setting out its framework for managing climate risk and enhancing climate resilience across its activities.

- Financial services engagement: Engagement with the financial services sector has continued, including an introductory roundtable with insurance providers focused on their approaches to managing physical climate risks in decision‑making, and on longer‑term opportunities to support household behavioural change that contributes to climate adaptation.

Climate change is among factors which can cause disruption, including price spikes, to our supply chains for critical foods and good. Adaptation will also mean there will be increased demand on supply chains for certain good, technologies and services which can help us prepare for climate supply.

To support the safe supply of critical goods and foods, during the reporting period:

- International Food Security Collaboration: International collaboration continues to be an important objective in food security, with the Scottish Government having successfully delivered Scotland’s Global Food Security Conference 2025 in partnership with SEFARI Gateway. The three-day event brought together 130 participants from across international organisations, the diplomatic community, academic, and the private sector on the theme 'Global food security: climate change, collaboration, and comparative advantage. We continue to engage with the other UK nations on issues relating to Critical National Infrastructure (CNI), with ongoing work to consider how we can strengthen UK wide collaboration on emergency planning and resilience.

- Trade Agreements: In 2025, we urged the UK Government to ensure that adaptation, mitigation, and resilience are fully considered in Free Trade Agreement negotiations, including Switzerland, Republic of Korea, Turkey, the Gulf Cooperation Council, and India. We have also set out our position that UK Tariff structures should aim to support and further facilitate trade in environmental goods and incentivise green industries to help progress towards a global green economy. See the latest Annual Report of Scotland’s Vision for Trade, published in January 2026, which sets out progress we made towards our trade objectives in line with our values.

- WTO Environmental Goods and Services: In parallel, we have engaged with the UK Government regarding their participation in the World Trade Organization environmental fora, including at the Committee for Trade and Environment and in Trade, Environment, and Sustainability Structured Discussions, where they addressed issues including environmental goods and services, which support trade in climate critical goods and services, as well as wider climate adaptation priorities.

- Critical Minerals: We also welcomed the publication of the UK Government’s Critical Mineral Strategy in November 2025 and have engaged with the UK Government on critical minerals, where relevant, as part of trade agreements and arrangements.

- Food safety: Food Standards Scotland (FSS) continues to ensure sustainability is embedded into its decision food businesses and consumers in Scotland. In 2025 this included:

- Launching the new FSS website, which provides improved accessibility of food safety advice for consumers including guidance on safe food handling during flooding events, during warmer weather and instances of power cut.

- On-going development of horizon scanning capability to support the identification of food safety risks internationally, including those which have been attributed to changes in climate (e.g. flooding and crop failures)

- Publication of data in the joint FSS/Food Standards Agency Our Food report and DEFRA's UK Food Security Report which supports government in reviewing the safety and standards of the UK food chain, and the impacts of stresses including the risks from climate change.

- Continued to collaborate with scientists through the SG Strategic Research programme on research which improves our understanding of the potential impacts of climate change on food safety risks, and supports the development of interventions for mitigating these risks. A key example is the research being led by Rowett Research Institute on the risks of mycotoxins in Scottish cereal crops.

To support alignment of economic development with adaptation, during the reporting period:

- Community Wealth Building: The Community Wealth Building (Scotland) Bill was unanimously passed by the Scottish Parliament in February 2026. The Bill includes provisions to support local climate resilience and the mitigation of the effects of climate change.

- Public procurement: In 2025-2026, following a review of climate adaptation and procurement practice, we updated the Climate Change Adaptation Guidance on the Sustainable Procurement Tools. On the Sustainable Procurement Tools, we refreshed and relaunched three of the eLearning modules (Introduction to Sustainable Procurement, Climate Literacy and Circular Procurement and Supply) and expanded the suite of case studies from across the Scottish public sector. In the most recent Scottish Ministers’ Annual Report on Procurement Activity in Scotland (2023-24), 86% of reporting bodies provided evidence of how they were addressing climate change through public procurement activity.

- Embedding climate risk in enterprise support: All three Enterprise Agencies undertook climate risk assessments to inform their corporate risk registers and to build practical capability in undertaking CCRA‑style assessments. This first‑hand experience is supporting business advisers to engage more effectively with businesses on climate resilience and adaptation.

- Integrating adaptation into investment decisions and regional resilience: At Scottish Enterprise, climate adaptation continues to be embedded within project appraisal processes, with all major infrastructure projects progressing through the Project Lifecycle approach. This includes use of the Net Zero Improvement Tool to identify climate risks, opportunities, and appropriate mitigation or adaptation measures. Regional business resilience in climate‑exposed areas was also strengthened through the publication of the first Highland Climate Change Risk and Opportunity Assessment, which provides practical case studies showing how climate change is already influencing business operations, costs, and investment decisions.

‘Economy, Business and Industry’ Indicators

| Indicator | Ambition | Actual trend | Observations |

|---|---|---|---|

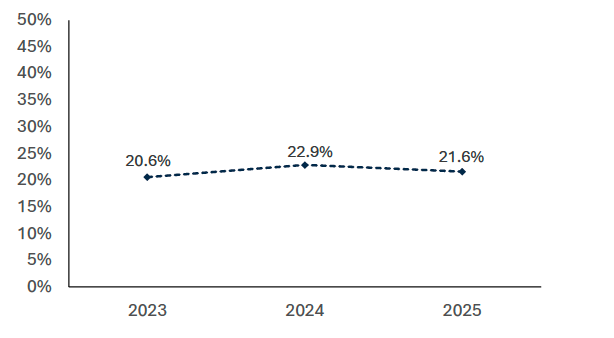

| B1.1 – Businesses monitoring climate related risks | Increasing / improving trend | Maintaining trend | In 2025, 21.6% of businesses reported that they had assessed climate change related risks, broadly in line with 22.9% reporting this in 2024. |

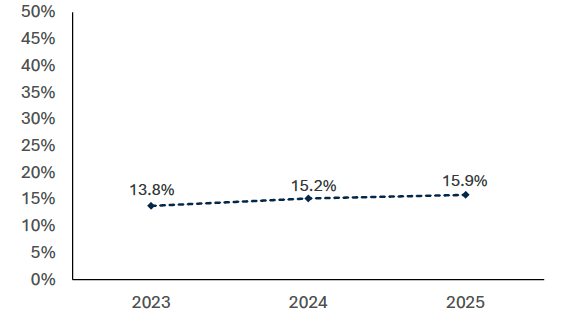

| B1.2 – Businesses taking action to adapt to the effects of climate change | Increasing / improving trend | Maintaining trend | In 2025, 15.9% of businesses reported that they had taken action to adapt to climate change, in line with 15.2% in 2024. |

| B2.1 – Proportion of agricultural land under management under AgriEnvironment Climate Scheme | Increasing / improving trend | Too early to say | In 2025, 832,894 hectares of agricultural land were managed under the Agri-Environment Climate Scheme (AECS) contracts for the options included in the indicator (all options measured in hectares through the scheme, including the organic conversion and maintenance options). This represents a similar proportion of the total agricultural land covered under contracts since 2024 (16.6% in 2025 compared to 16.5% in 2024). |

| B2.2 – Proportion of Forest Plans revised under the new edition of the UKFS | Ensure all future approved plans and amendments comply with the new edition of UKFS after the ‘go-live’ date in October 2024 | Too early to say | Scottish Forestry approvals have required compliance with the updated standard from 1st October 2024. A transition period has been adopted between 1st October 2024 and the 1st March 2025 to allow for plans under contract from before the 1st October 2024 to be completed. Recording of data for this indicator began on 1st April 2025, the full year's data (01/04/2025 - 31/03/2026) will not be collated until October 2026. |

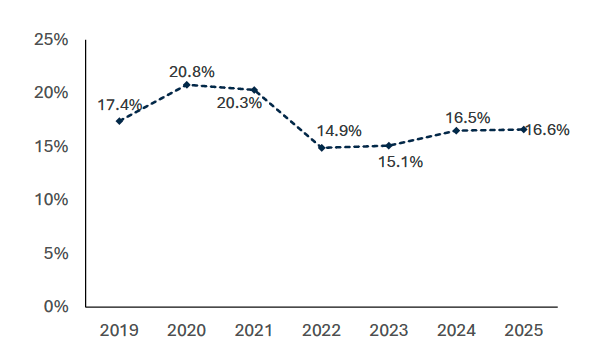

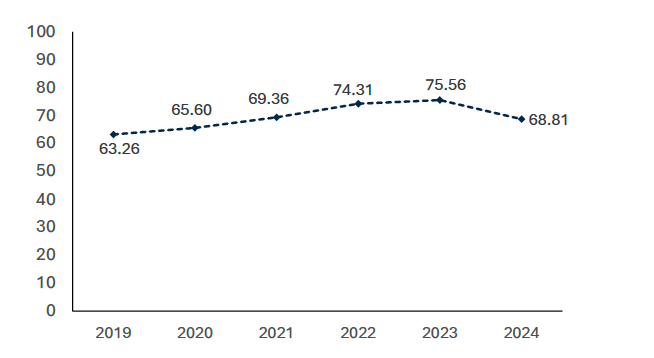

| B2.3 – Commercial fish stocks fished at sustainable levels | Increasing / improving trend or Maintaining trend | Too early to say | The index of sustainable fishing in Scotland stood at 68.81% in 2024, which represents a small decrease from the 2023 value (75.56%) but a significant increase from the time series minimum (40.89% in 1999). Trend data will be reported on once 2025 figures are available. |

| B2.4 – Tonnage and value of fish stocks landed | Increasing / improving trend or Maintaining trend | Increasing / improving trend | In 2024, 532,094 tonnes of fish was landed by Scottish vessels, the greatest tonnage of the last ten years. The value of these landings in 2024 was £734 million. This is the highest value (adjusted to 2024 prices) of the last ten years. |

| B2.5 – Operating profits for fishing fleets | Increasing / improving trend or Maintaining trend | Increasing / improving trend | Average real operating profits per vessel continued to increase in Scotland in 2024, rising to £165,000, following a relatively stable period between 2019 and 2022, when average profits fluctuated between £109,000 and £123,000 (in 2024 prices). Growth began to pick up in 2023 and accelerated further in 2024, which recorded the highest level of average operating profit, in real terms, across the 2019-2024 period. |

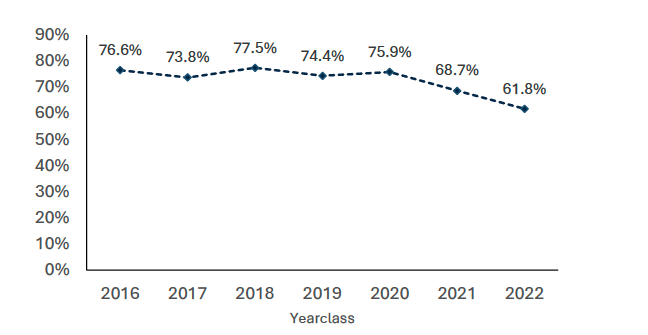

| B2.6 – Survival to harvest of salmon smolts put to sea[41] | Maintaining trend | Too early to say | 61.8% of the 2022 yearclass of salmon within seawater production survived to harvest, down from 68.7% of the 2021 yearclass. Due to the underlying methodology, the 2022 yearclass is the last one for which the indicator can be calculated. |

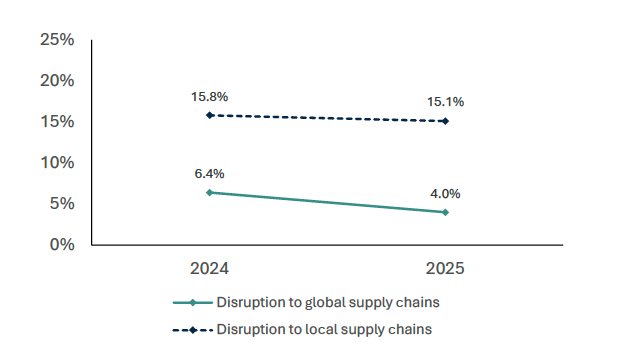

| B4.1 – Reported disruption to supply chains as a result of severe weather event | Decreasing / worsening trend | Maintaining trend | In 2025, 15.1% of businesses impacted by severe weather reported disruption to local supply chains as a result, in line with 15.8% reporting this in 2024. In 2025, 4.0% of businesses impacted by severe weather reported disruption to global supply chains as a result, broadly in line with 6.4% in 2024. |

B1.1 – Businesses monitoring climate related risks

Description: This indicator shows the percentage of businesses in Scotland who are reporting assessing climate change related risks[42]

Data source: Business Insights and Conditions Survey

Ambition: Increasing over time

Actual trend: Maintaining

In 2025, 21.6% of businesses reported that they had assessed climate change related risks, broadly in line with 22.9% reporting this in 2024. Business action in relation to monitoring climate risks can make them more prepared for and able to respond to climate change impacts, such as severe weather events.

In 2025, the most common climate related risk assessed by businesses was risks to supply chain disruption (15.2% of businesses). Fewer had considered risks from increased flooding (7.0%) and temperature increases (6.2%), with 3.3% reporting that they had considered risks from water scarcity.

B1.2 – Businesses taking action to adapt to the effects of climate change

Description: This indicator shows the percentage of businesses in Scotland reporting taking action to adapt to effects of climate change[43]

Data source: Business Insights and Conditions Survey

Ambition: Increasing over time

Actual trend: Maintaining

In 2025, 15.9% of businesses reported that they had taken action to adapt to climate change, in line with 15.2% in 2024.

Business action in relation to adaptation can make them more resilient and prepared for climate hazards, thereby reducing vulnerability.

One in ten (9.9%) of businesses in 2025 reported that they had taken action around supply chain disruption and distribution. Fewer reported action around the risk of temperature increases (5.2%) and increased flooding (4.5%), with 2.2% reporting they had taken action around water scarcity risks.

B2.1 – Proportion of agricultural land under management under AgriEnvironment Climate Scheme

Description: This indicator shows the proportion of agricultural land under management contracts which include adaptation related measures[44]

Data source: Scottish Government

Ambition: Increasing over time

Actual trend: Too early to say

In 2025, 832,894 hectares of agricultural land were managed under the Agri-Environment Climate Scheme (AECS) contracts for the options included in the indicator (all options measured in hectares through the scheme, including the organic conversion and maintenance options). This represents a similar proportion of the total agricultural land covered under contracts since 2024 (16.6% in 2025 compared to 16.5% in 2024).

This was a decrease in total hectares covered from the previous year when 849,094 hectares were covered. The reason for the decrease is that the management area of contracts coming to an end in 2024 was greater than the management area from the new contracts starting in 2025.

The Agri-Environment Climate Scheme is the Scottish Government’s key mechanism providing support for land managers to undertake actions which protect and enhance Scotland’s magnificent natural heritage, improve water quality, manage flood risk, preserve historic sites and mitigate and adapt to climate change. This indicator does not capture actions which take place outside of the scheme, and so may not provide a full picture of agricultural resilience in Scotland.

B2.2 – Proportion of Forest Plans revised under the new edition of the UKFS

Description: This indicator measures the proportion of Forest Plans (private and public sector) revised under the new edition of the UKFS as a percentage of area under forest plans

Data source: Scottish Forestry

Ambition: Ensure all future approved plans and amendments comply with the new edition of UKFS after the ‘go-live’ date in October 2024

Actual trend: Trend data not yet available - first full reporting period will be presented in SNAP3 2027 progress report

Forest plans are one of the principal tools used to manage long-term change in the forest resource. The UK Forestry Standard (UKFS), the UK technical standard for sustainable forest management underpins all Forestry Grant Scheme (FGS) and Felling Permission approvals, and all Forestry Environmental Impact Assessment determinations.

The UKFS was reviewed and revised with stakeholders in 2023 to ensure, amongst other things, that compliance with the standard increases the resilience of the forest resource.

Scottish Forestry approvals have required compliance with the updated standard from 1st October 2024. A transition period has been adopted between 1st October 2024 and the 1st March 2025 to allow for plans under contract from before the 1st October 2024 to be completed. Recording of data for this indicator began on 1st April 2025, the full year's data (01/04/2025 - 31/03/2026) will not be collated until October 2026, therefore a nil return has been submitted for this period and future reporting will have a lag in order to present a full year's data.

B2.3 – Commercial fish stocks fished at sustainable levels

Description: This index measures our confidence that Scottish fish stocks are being fished sustainably

Ambition: Increasing or maintaining over time

Actual trend: Too early to say (Increasing over time with a small decline in the most recent year)

The index of sustainable fishing in Scotland stood at 68.81% in 2024, which represents a small decrease from the 2023 value (75.56%) but a significant increase from the time series minimum (40.89% in 1999). Further years of data will be required to report confidently on a trend for this indicator due to year to year fluctuations.

This indicator is relevant to resilience of Scotland’s fishing industry. When combined with indicators 2.4 and 2.5, it represents a measure of whether fishing vessels are able to continue to find a market for their fish, to fish sustainably, and to stay in profit. The indicator highlights that fish stock sustainability in Scotland has increased through time.

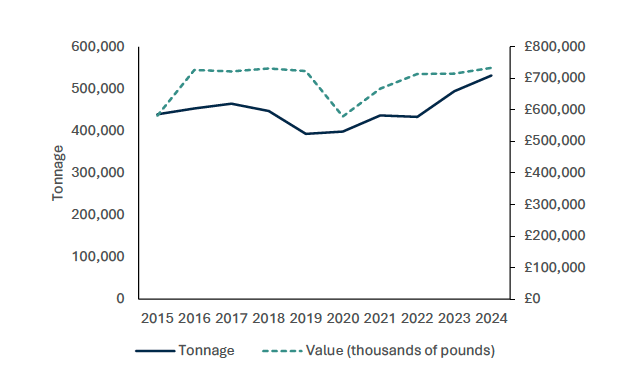

B2.4 – Tonnage and value of fish stocks landed

Description: This indicator shows the tonnage and real value of fish stocks (in £) landed by Scottish vessels

Ambition: Increasing or maintaining over time

Actual trend: Increasing

In 2024, 532,094 tonnes of fish was landed by Scottish vessels, the greatest tonnage of the last ten years. The value of these landings in 2024 was £734 million. This is the highest value (adjusted to 2024 prices) of the last ten years.

The tonnage and value of fish landed is made up of a variety of different species with different trends over time. The value shown here is the real value has been adjusted by inflation. Many key commercial fish species are controlled by quotas, which limits the volume of commercial catch in any year to help preserve fish stocks. This will impact on the tonnage and value caught per species and the overall tonnage and value. The average price per tonne varies considerably by species. In 2024, the average price per tonne of Lobster was £14,886. Whereas, the average price per tonne of Blue whiting was just £251. Typically, pelagic species, like Mackerel, Herring and Blue whiting are caught in large volumes and have a lower price per tonne. Shellfish species are typically caught in smaller volumes and have a higher price per tonne. Hospitality closures due to Covid-19, in 2020 and to a lesser extent in 2021, resulted in a loss of trade and markets particularly affected the shellfish sector.

When combined with indicators 2.3 and 2.5 it provides a measure relevant to resilience of Scotland’s fishing industry. It represents a measure of whether fishing vessels are able to continue to find a market for their fish, are able to fish sustainably, and able to stay in profit.

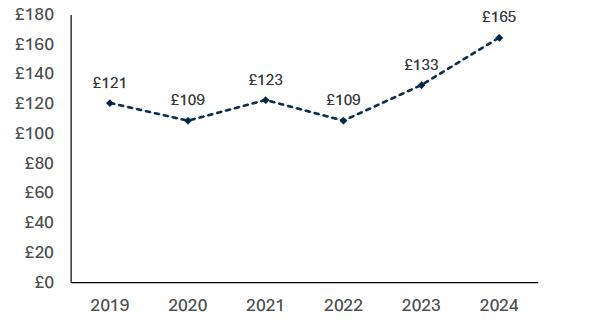

B2.5 – Operating profits for fishing fleets

Description: This indicator shows the real annual operating profit (£) for Scottish fishing vessels fleets

Data source: Seafish, Economies of the Fishing Fleet data (nominal operating profit per vessel), Economics of the UK Fishing Fleet — Seafish (nominal operating profit per fishing fleet segment), and HMT’s GDP deflators at market prices as at time of reporting (deflators)

Ambition: Increasing or maintaining over time

Actual trend: Increasing over time

Average real operating profits per vessel continued to increase in Scotland in 2024, rising to £165,000, following a relatively stable period between 2019 and 2022, when average profits fluctuated between £109,000 and £123,000 (in 2024 prices). Growth began to pick up in 2023 and accelerated further in 2024, which recorded the highest level of average operating profit, in real terms, across the 2019-2024 period.

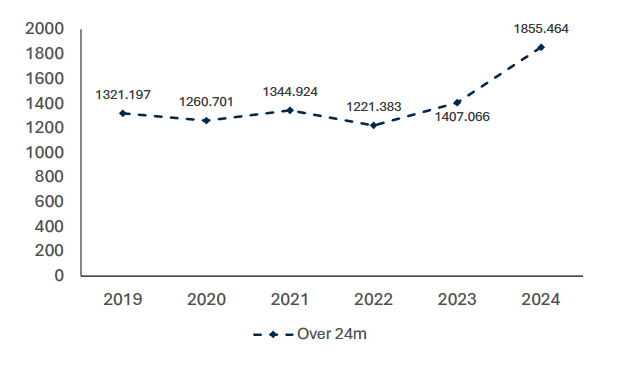

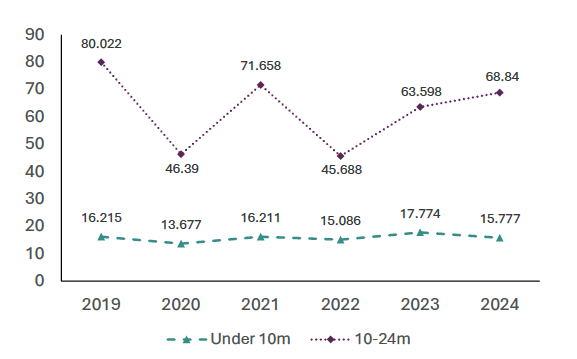

Growth was driven by larger vessels over 24 metres, which recorded the highest operating profits, averaging £1,855,000 in 2024. This represents an increase of 40% in real terms since 2019. For vessels under 10 metres, average operating profits were £16,000 in 2024, remaining broadly consistent with the trend since 2019. Vessels between 10 and 24 metres in length recorded average operating profits of £69,000 in 2024, an increase in real terms compared to 2022 and 2023, but a decline in real terms compared to 2019.

This indicator is relevant to the resilience of Scotland’s fishing industry. When combined with indicators 2.3 and 2.4, it represents a measure of whether fishing vessels are able to continue to find a market for their fish, fish sustainably, and stay in profit.

B2.6 – Survival to harvest of salmon smolts put to sea[48]

Description: This indicator shows the percentage of the number of salmon smolts put to sea within a yearclass and their survival to harvest across seawater production in aquaculture

Data source: Scottish Fish Farm Production Survey

Ambition: No decreasing trend in % survival over time

Actual trend: Too early to say

61.8% of the 2022 yearclass of salmon smolts put to sea survived to harvest, down from 68.7% of the 2021 yearclass. Due to the underlying methodology, the 2022 yearclass is the last one for which the indicator can be calculated.

This indicator may be indicative of aspects of resilience of Scotland’s aquaculture industry. The calculation of survival to harvest includes all types of losses. This includes factors such as predation, mortality, and escapes. Impacts of climate change may also be one of these.

This indicator can be used to understand trends in total losses over longer time periods. No decreasing trend in percentage survival may indicate that the aquaculture sector is adapting to the additional pressures of climate change, although this needs to be assessed within the broader context of losses and the complexities of fish health.

B4.1 – Reported disruption to supply chains as a result of severe weather event

Description: This indicator shows the percentage of businesses in Scotland reporting disruption to supply chains as a result of a severe weather event

Data source: Business Insights and Conditions Survey

Ambition: Decreasing over time

Actual trend: Maintaining

In 2025, 15.1% of businesses impacted by severe weather reported disruption to local supply chains as a result, in line with 15.8% reporting this in 2024. In 2025, 4.0% of businesses impacted by severe weather reported disruption to global supply chains as a result, broadly in line with 6.4% in 2024.

Businesses which are more resilient to climate change should be less vulnerable to supply chain disruption as a result of severe weather events.