Government expenditure & revenue Scotland 2024-25

Government Expenditure and Revenue Scotland (GERS) is an Accredited Official Statistics publication. It estimates the revenue raised in Scotland and the cost of public services provided for Scotland.

Part of

Preface

This report is the thirty-second in the series of official published estimates of expenditure and revenue balances of the public sector in Scotland.

GERS is classified as Accredited Official Statistics and is produced in accordance with the principles of the Code of Practice for Statistics. More information about Accredited Official Statistics, including the latest assessment report on GERS (number 274), is available on the UK Statistics Authority website.[3]

Feedback from users of the publication is welcome. Comments can be emailed to:

Recent Statistical Decisions and Changes

A number of statistical changes are relevant to this year’s publication.

Crown Estate Revenues

The Crown Estates in both Scotland and the UK have undertaken auctions of option rights to develop offshore wind projects. In Scotland these are known as ScotWind and in the rest of the UK the Offshore Wind Leasing Round 4. These options last for up to 10 years. Due to the different timing of the auctions in Scotland and the rest of the UK, and to different contractual arrangements, the revenues will have a slightly different profile in Scotland and the UK. The UK Crown Estate recognised around £1.1 billion of revenue from option fees in its 2024-25 Annual Report. Crown Estate Scotland accounts show that ScotWind contributed £76 million to the Scottish Consolidated Fund in 2023-24 and is expected to have contributed a similar amount in 2024-25.

These numbers are not yet reflected in the UK Public Sector Finances. They will be reflected in the future editions of GERS as updates are made to the UK figures.

Methodological changes in this edition of GERS

There are no major methodological changes in this edition of GERS. However, the data source used for some apportionments, the Office for National Statistics (ONS) Country and Regional Public Sector Finances publication, was not published in 2025. Further details are provided in the revenue methodology document.

What Questions Does GERS Address?

GERS addresses three questions about Scotland’s public sector accounts for a given year:

1. What revenues were raised in Scotland?

2. How much was spent on public services for Scotland?

3. To what extent did revenues cover the costs of these public services?

How does GERS relate to devolved public sector finances?

GERS does not directly relate to the finances of the Scottish Government or the wider devolved public sector. The fiscal balances in GERS compare total public sector spending to total public sector revenue. They do not correspond to a deficit of any particular part of the public sector. Separate reports are available on Scottish Government and Scottish Local Government finances.

In 2024-25, the devolved public sector borrowed £2.5 billion. This consisted of:

- £139 million of borrowing by the Scottish Government,[4] which was all capital borrowing with no resource borrowing.

- £2,359 million of Local Government borrowing,[5] which is used only to finance capital expenditure.

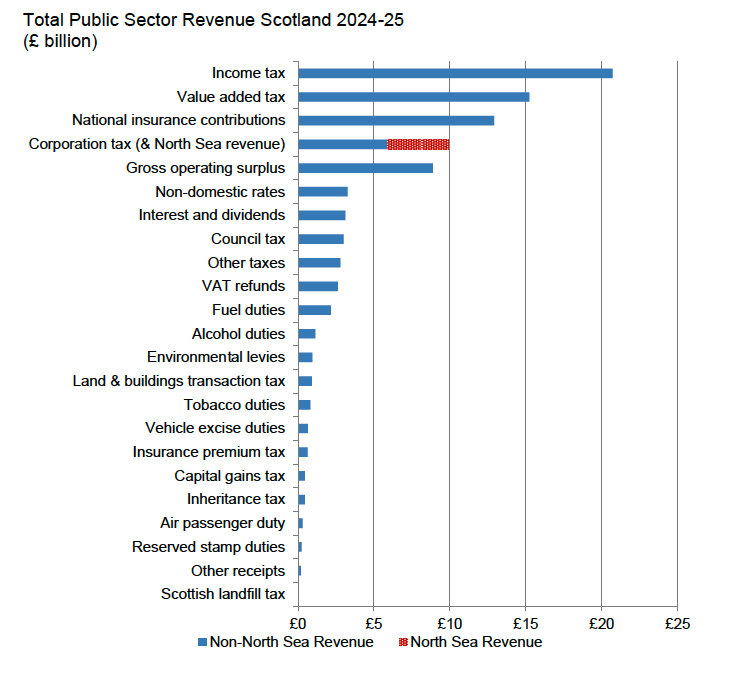

Revenue

Public sector revenue is estimated where a financial burden is imposed on residents and enterprises in Scotland.

In general, the way in which revenue is collected means that separate figures for each country and region of the UK are not available for most revenues, although following increased devolution in recent years, more Scottish data have become available. As a result, Scottish public sector revenue is estimated by considering each revenue stream separately. Where Scottish data are unavailable, GERS estimates revenue using a set of apportionment methodologies, refined over a number of years following consultation with and feedback from users. The methodology note on the GERS website provides a detailed discussion of the methodologies and datasets used.[6]

Expenditure

Public sector expenditure is estimated on the basis of spending incurred to provide services for residents of Scotland. That is, a particular public sector expenditure is apportioned to a region if the outcome of the expenditure is thought to provide a public service which benefits residents of that region.

This is a different measure from total public expenditure in Scotland. For most expenditure, spending for or in Scotland will be similar. For example, the vast majority of health expenditure by NHS Scotland occurs in Scotland and is for patients resident in Scotland. Therefore, the in and for approaches should yield virtually identical assessments of expenditure. However, for expenditure where the service provided is more collective in nature, such as defence, an assessment of ‘who the service is for’ depends upon the nature of the specific type of expenditure being assessed. Where there are differences between the for and in approaches, GERS estimates Scottish expenditure using a set of apportionment methodologies, refined over a number of years following consultation with and feedback from users.

The for approach considers the location of the recipients of services or transfers that public sector expenditure finances, irrespective of where the expenditure takes place. For example, with respect to defence expenditure, as the service provided is a national ‘public good’, the for methodology operates on the premise that the entire UK population benefits from the provision of a national defence service. Accordingly, under the for methodology, national defence expenditure is apportioned across the UK on a population basis.

The Data Sources

The source of the revenue data in GERS is ONS’s Public Sector Finances, which provides disaggregated figures relating to UK public sector revenue.[7]

The data sources used to estimate Scottish public sector expenditure in GERS are Scottish Government accounting data, and HM Treasury’s Public Expenditure Statistical Analyses[8] and the supporting Country and Regional Analysis (CRA).[9]

GERS also uses the estimates of Scottish Gross Domestic Product (GDP) in current market prices published in the Quarterly National Accounts Scotland (QNAS).[10]

Additional Information on the GERS Website

The GERS website contains a number of additional analyses of Scotland’s public sector finances. In addition to containing copies of the GERS report from 1990-91 onwards, the website also contains the tables underpinning this edition of GERS in Excel format and statistics providing a consistent time series of Scotland’s public sector finances from 1998-99 to 2024-25. The GERS website can be accessed via:

Economy statistics - gov.scot (www.gov.scot)

Comparisons to other countries and regions of the UK

GERS does not provide comparisons of Scottish revenue and expenditure with other parts of the UK, as data are not yet available for the latest years for each country and region of the UK. Users who are interested in these comparisons are advised to use the Country and Regional Public Sector Finances publication published by the ONS, available at the link below. A comparison between the ONS and GERS revenue figures for Scotland, for years up to 2022-23, is provided in Table 1.5.

Country and regional public sector finances, UK - Office for National Statistics (ons.gov.uk)

International comparisons

The Scotland figures in the main tables in GERS are produced to be comparable to the UK figures presented in the ONS Public Sector Finances and the OBR Economic and Fiscal Outlook. These report for the public sector as a whole on a financial year basis. In contrast, organizations such as the OECD and the International Monetary Fund report countries’ finances on a calendar year basis and for the government sector only. Figures for Scotland on this basis are available in Table A.4.

Contact

Email: economic.statistics@gov.scot