Building a New Scotland: A stronger economy with independence

This paper sets out the Scottish Government’s proposals for the economy of an independent Scotland. It explains what these proposals would mean for you, for businesses, and for Scotland as a whole. It is the third in the 'Building a New Scotland' series, focusing on independence.

Scotland’s economic potential

Key points

The Scottish economy has many strengths, and great potential, but is currently part of a UK economic model that is less productive, with lower national income per head and greater inequality than independent countries comparable to Scotland.

This relatively poor UK economic performance was evident even before Brexit.

Outside the EU, Scotland is now outside a European Single Market that by population is seven times the size of the UK. This is likely to lead to further negative economic outcomes.

In the UK, economic activity is disproportionately concentrated in London and the South East of England. The extent of this geographical inequality is unusually high.

UK wages, adjusted for inflation, are now at around the same level as they were 15 years ago, before the financial crisis. This low wage growth is particularly concerning in the middle of a cost of living crisis.

In an independent Scotland, control of key economic powers would transfer from Westminster to the Scottish Parliament.

The Scottish Government believes that taking decisions in Scotland, combined with our economic strengths, will lead to better outcomes for the people who live here.

We have significant offshore renewables resources and are ranked first amongst the UK’s nations and regions for green growth potential and opportunity.

Our food and drink sector is a success. It supported 122,000 jobs in Scotland in 2019, and added £5.8 billion to the economy that year. Scottish salmon is the UK’s largest food export, with an export value of over £600 million in 2019. Scotch whisky is the UK’s biggest drink export, accounting for a fifth of all UK food and drink exports.

We are a highly educated and skilled country, with a higher share of our population with a university or college education than anywhere else in the UK or EU. We have world-class universities – with three in the top 200 of the Times Higher Education World University Rankings 2023. And Scotland continues to be seen as a desirable place to study and work for international students and researchers.

We have key specialisms in digital technology, including artificial intelligence and cyber security. Edinburgh is now aiming to be the Data Capital of Europe and Dundee is a leader in the gaming industry. In 2019, the tech sector employed 73,700 people.

Given these strengths Scotland is well-placed to match the success of comparable independent countries instead of being part of a relatively poorly performing UK economic model set for further relative decline as a result of Brexit.

The Brexit-based UK economic model

The debate about our economy often focusses on the current fiscal position of Scotland within the UK.

But the point of independence is to change things. Indeed Scotland’s fiscal position is a consequence of an unbalanced UK economic model in which economic activity is disproportionately concentrated in London and the South East of England.[12]

The full powers of an independent country would give Scotland the opportunity to develop a new economic model, one that is tailored to our circumstances, opportunities and strengths.

The alternative is to be a regional part of a Brexit-based UK economy. That means:

- being tied to the UK’s stagnating economy. The UK’s economic and social model does not generate broadly based prosperity: it creates concentrated wealth.[13] Compared with neighbours in north-western Europe, the UK has high income inequality, high rates of poverty and low productivity

- being outside the EU and a market that by population is seven times the size of the UK. The Office for Budget Responsibility (OBR) estimates that Brexit will reduce long-run productivity by 4% compared with remaining in the EU.[14] This equates to a loss of around £100 billion in lost output and £40 billion in public revenues.[15] Scotland’s share, calculated by head of population, would be around £3.2 billion less each year

- population decline. Scotland’s population at the time of the Union between Scotland and England is estimated to have been a fifth of that of England and Wales.[16] Today the figure is less than a tenth, or 8.1% of the overall UK population. It is projected that by 2045, if we do nothing, this will fall to 7.6%.[17] A falling working age population will result in a smaller proportion of people generating tax revenue to pay for public services, and the UK’s current restrictive migration policies will only exacerbate these trends[18]

- · low and unequal incomes. Wages, adjusted for inflation, are now at around the same level as they were 15 years ago, before the financial crisis, with household incomes in the UK falling behind those in many other European countries.[19] If pay had continued to grow at pre-crisis rates, workers would be earning an average of £9,200 more each year. Eight million young people in the UK have never worked in an economy with rising average wages, and 25 million have never lived in a country where the top 10 per cent have had incomes less than five times that of the bottom 10 per cent.[20]

The Scottish Government’s view is that this reveals a UK economy that is not well placed to meet the challenges of the 21st century.[21]

A recent report by the Resolution Foundation set out clearly the extent of the UK’s relative economic decline:

- in 2007, just before the financial crisis, GDP per capita in the UK was just 6% lower than in Germany, but by 2019 this gap had increased to 11%

- labour productivity grew by just 0.4% a year in the UK in the years following the financial crisis, half the rate of the 25 richest Organisation for Economic Co-operation and Development (OECD) countries (0.9%)

- real wages grew by an average of 33% a decade from 1970 to 2007 but growth fell to below zero in the 2010s

- having surged during the 1980s and remained consistently high ever since, income inequality in the UK was higher than any other large European country in 2018

- low-income households in the UK are now 22% poorer than their counterparts in France and 21% poorer than low-income households in Germany.

The detrimental economic impact of Brexit on Scotland (see Box 2) and the UK as a whole is now evident:

“The UK is lagging behind the rest of the G7 in terms of trade recovery after the pandemic; business investment…trails other industrialised countries despite lavish Treasury tax breaks to drive it up.”[22]

The OECD predicts that the UK will be the slowest growing G20 nation over the next year, apart from sanctioned Russia.[23]

Catherine Mann of the Bank of England’s Monetary Policy Committee recently assessed the impacts of Brexit:

“the more sluggish recovery in UK trade relative to G7 peers, which is associated with Brexit, portends downside risk to productivity growth, and therefore a lower long-term real rate. Erosion in competition, fewer varieties, and less new technology imported into the domestic UK market, and the loss of economies of scale and market knowledge associated with export expansion translate into lower firm-level and aggregate productivity growth”.[24]

The Resolution Foundation has found that the UK economy is less open and less competitive as a result of Brexit:

“following the implementation of the EU-UK Trade and Cooperation Agreement (TCA), the UK has suffered a broad-based fall in both openness and competitiveness in 2021. Between 2019 and 2021, UK trade openness fell by 8 percentage points, significantly more than in countries with similar trade profiles, such as France which experienced a 2-percentage-point decline”[25]

It concluded that this will have a detrimental impact on the UK’s productivity and on people’s wages:

“A less-open UK will mean a poorer and less productive one by the end of the decade, with real wages expected to fall by 1.8 per cent, a loss of £470 per worker a year, and labour productivity by 1.3 per cent, as a result of the long-run changes to trade under the TCA”.[26]

Box 2: How has Brexit affected Scotland’s economy?

Brexit has created new trade frictions and costs for businesses in Scotland.

Scotland’s trade in goods with the EU was particularly affected at the start of 2021 when new checks and requirements were introduced under the agreed UK-EU trade deal.

Scottish Government analysis shows that the value of Scotland’s total trade in goods with the EU (imports plus exports) was 12% lower in 2021 than it otherwise would have been under continued EU membership.[27] Much of this decline is driven by a reduction in EU imports.[28]

Imports of food and live animals (dairy products, vegetable and fruit) were 21% lower.

Imports of manufactured materials (textiles, fabrics and rubber) were 23% lower.[29]

Imports of miscellaneous manufactured articles (apparel and clothing accessories) were 33% lower.

Latest survey data show that many Scottish businesses are facing additional costs due to Brexit. Around 27% were facing higher transportation costs, 16% were reporting additional costs due to changing supply chains and a further 15% due to red tape.[30]

In addition to the direct effect of increased trade costs, Brexit has contributed to a shortage of labour in the UK economy. This has had an additional inflationary headwind compared to other major advanced economies due to lack of available skills. Many EU nationals have left Scotland (and the rest of the UK) since the UK left the EU, during a period that has coincided with the pandemic and the introduction of the new UK immigration system. In Scotland, sectors such as accommodation & food, administration & support services as well as some areas of food manufacturing have seen large decreases in the number of EU workers, which has contributed to recruitment challenges.[31]

Trade impacts are based on one year’s data. But Brexit is a long-term shock.

More broadly, the data suggest that the UK as a whole has become less open. Trade as a share of UK GDP has fallen 12% since 2019: two-and-a-half times more than in any other G7 country.[32]

In other words, because of Brexit, UK trade has recovered from the shock of the pandemic much more slowly than other G7 countries.

Only independence would give Scotland the power to reverse Brexit and its associated negative impacts.

The UK Internal Market Act 2020 (the IMA) has reduced the ability of Scotland to make decisions that suit its circumstances. It deepens UK-wide uniformity, centralises economic control in the hands of the Westminster Government, and limits the Scottish Parliament’s ability to address public health issues, such as food content standards or alcohol-related harm.[33]

Scotland will see devolved powers further undermined if the Westminster Government decides to accept reduced standards to secure a free trade agreement with other countries. The USA, for example, has been clear that agriculture, food standards and drug prices will be on the table in any future trade deal with the UK.[34]

As things stand, the Scottish Parliament does not have the power to resist Westminster imposing lower standards in Scotland, even in devolved areas. This poses significant risks to the economy.[35] The food and drink sector is more important economically to Scotland than it is to the UK as a whole. The industry’s success is based on the quality guarantee that comes with Scottish provenance and any change in regulatory approach that compromised standards would have a severe impact.

It is worth comparing the prospects for Scotland’s economic future with the example of Ireland. EU membership allowed Ireland to escape over-reliance on a sluggish UK economy.[36]

While a range of factors contributed to its rapid development post EU accession, Ireland’s national income increased rapidly as it diversified trade away from the UK and towards the EU and the rest of the world, as shown in Table 1.[37]

| 1973 | 1979 | 2000 | 2019 | 2020 | |

|---|---|---|---|---|---|

| Population of Ireland (millions) | 3.09 | 3.37 | 3.81 | 4.93 | 4.99 |

| GDP[38] per head Ireland (USD, constant prices, 2015 PPPs) | 15,019 | 18,299 | 46,873 | 83,874 | 88,111 |

| GDP per head UK (USD, constant prices, 2015 PPPs) | 21,155 | 23,163 | 37,081 | 45,157 | 40,741 |

| Net National Income per head Ireland (USD, constant prices, 2015 PPPs) | NA | NA | 34,083 | 44,029 | 41,881 |

| Net National Income per head UK (USD, constant prices, 2015 PPPs) | NA | NA | 31,189 | 38,126 | 33,777 |

| UK share of Ireland’s goods exports (%) | 55 | 46 | 22 | 10 | 9 |

| UK share of Ireland’s goods imports (%) | 51 | 50 | 31 | 23 | 23 |

| EU share of Ireland’s goods exports (%) | 24 | 35 | 40 | 35 | 38 |

| EU share of Ireland’s goods imports (%) | 26 | 26 | 22 | 33 | 31 |

Sources: World Bank Population, total, OECD Gross domestic product (GDP), OECD Net national income per head, De Bromhead, A. Adams, R. and Casey, C. (2021) Ireland’s economy since independence: what lessons from the past 100 years? Economics Observatory

For Scotland, the danger of not acting quickly is that, outside the EU, exports to Europe will fall, and UK regulations will increasingly diverge from those of the EU. As part of the UK, Scotland would be increasingly locked into a UK economic model that delivers low growth.

Box 3: New economic thinking

Economic thinking has shifted profoundly in recent years. Organisations like the OECD and IMF, which had prioritised market-driven approaches to economic development, are now significantly more interested in researching and promoting policies to reduce inequality and boost workers’ bargaining power.

The slow, uneven recovery that followed the global financial crisis in 2008 led to a reassessment of many of the orthodoxies and assumptions of recent decades.

The rise of political populism and experience of the pandemic has intensified concerns about an approach to economic policy-making that ultimately produced slower productivity growth[39] and higher inequality[40] compared with preceding decades.

The shift in attitude is reflected in international economic institutions’ approach to inequality, for example, the OECD and European Union’s interest in minimum wage setting and extending collective bargaining coverage, and renewed interest in industrial policy.[41]

The range of policies supported by these institutions has widened significantly. For example, the OECD’s 2018 Job Strategy promoted the benefits of policies to increase collective bargaining coverage,[42] a significant change from its previous strategies.

The 21st century economy will require structural shifts of a scale that only government can shape. National co-ordination and substantial investments in infrastructure, for instance energy networks and public transport, are necessary to support the fastest possible just transition to net zero.

This new economic thinking informs both the Scottish Government’s commitment to a Wellbeing Economy and the proposals in this publication.

Scotland’s economy

Structure of Scotland’s economy

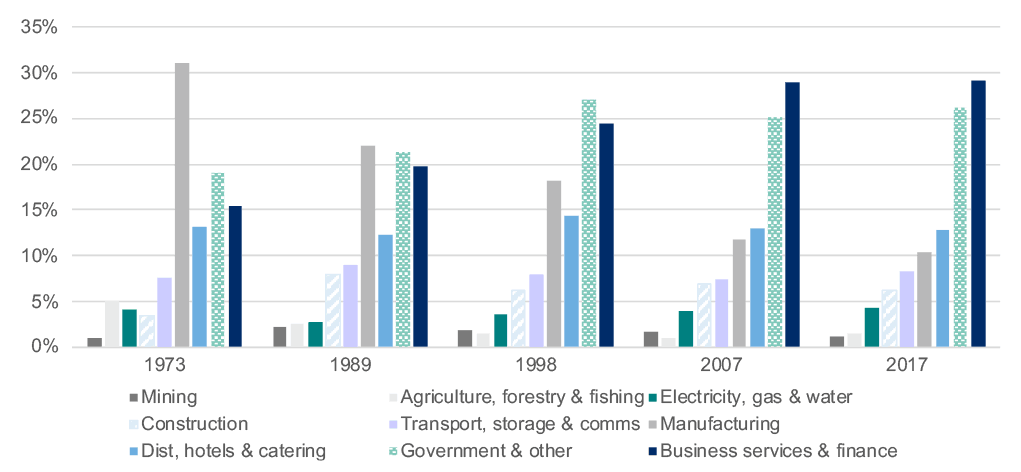

The structure of the Scottish economy has evolved significantly over recent decades in response to a range of factors including technological change, policy choices at UK level, and increased openness and competition within the global economy.

These trends have contributed to a major shift in Scotland from manufacturing to service-based activities, as shown in Figure 1.

Source: Scottish Government (2021) Supply, Use and Input-Output Tables: 1998-2018 (Note: these data are not fully consistent over time because of changes in accounting systems and industrial classifications)

Performance of Scotland’s economy

Since the establishment of the Scottish Parliament in 1999, the Scottish economy has performed well relative to the UK as a whole; although the UK has performed poorly, relative to independent European countries comparable to Scotland.[43]

Successive Scottish Governments have pursued policies on economic development and productivity. Historic gaps in productivity and wages between Scotland and other parts of the UK have narrowed.

However, key economic powers are reserved to Westminster (see Box 4), and across the ten comparable independent European countries whose performance we looked at in the first Building a New Scotland publication, GDP per capita in 2021 was on average £14,000 per person higher than in Scotland (£11,000 excluding Ireland).[44]

Box 4: Reserved economic powers

- foreign affairs and international trade

- fiscal, economic and monetary system, including most aspects of taxation

- most social security benefits

- tax credits and child benefit

- the minimum wage

- financial regulation

- immigration

- key aspects of energy policy, including North Sea revenues, generation and supply of electricity, and offshore oil and gas

- trade and industry, including company law, competition, and consumer protection

- cyber security

- many aspects of transport

- employment legislation, and industrial relations law

- broadcasting and media regulation

- telecommunications regulation.

Across a range of indicators Scotland has generally outperformed nations and regions outside London and South East England, and the gaps in performance between Scotland and the UK as a whole have narrowed significantly across some measures, as set out below.

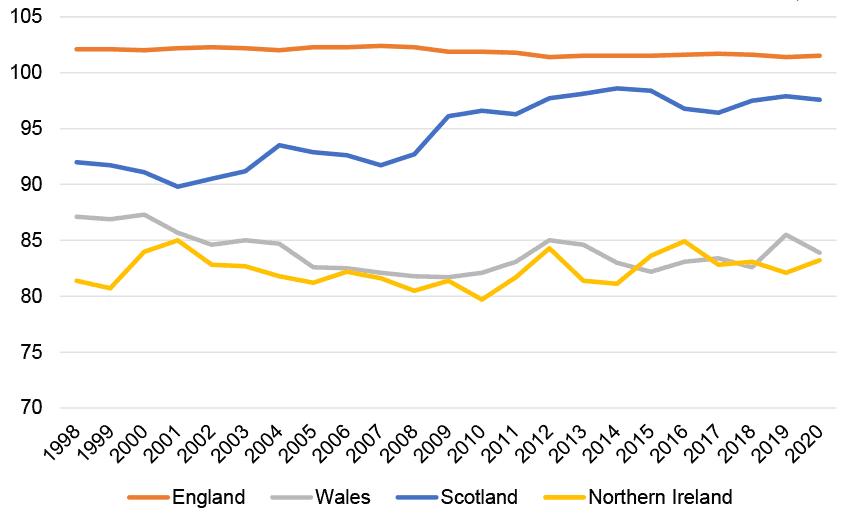

In 1999, when the Scottish Parliament was established, Scotland’s productivity levels were 8% lower than the UK average. The most recent available data show that the gap is now only around 2%, with only London and the South East performing better than Scotland on this measure.[45] Figure 2 shows Scotland’s productivity levels, as well as those of the other UK nations, since 1998.

Source: Regional labour productivity, UK Office for National Statistics (ons.gov.uk)

Average earnings have also grown at a faster rate in Scotland than in the UK as a whole, to the point where they are now in line with the UK average.[46]

Labour market indicators have also performed well, with employment (and particularly women’s employment) improving considerably since 1999, and unemployment is currently at historically low levels. However, the data also point to limited growth in real pay in the decade following the financial crisis and, more recently, a rise in economic inactivity with the latest data showing Scotland’s inactivity rate 0.7 percentage points above the UK average in May-July 2022.[47]

Further information on Scotland’s economic performance is presented in the Scottish Government’s evidence paper for the National Strategy for Economic Transformation.[48] Scotland’s improving economic performance indicates that it is well positioned to learn from the experience of those nations that have used the full powers of independence to achieve significantly better outcomes, including higher national income per head and lower income inequality.[49]

Scotland’s strengths

Successful independent countries comparable to Scotland are common in Europe. Indeed, they are among the wealthiest, fairest and happiest societies on earth.[50]

Scotland enjoys extraordinary natural heritage, a highly educated workforce, and has a range of industries, some of which are already successful in global markets and have significant potential to develop further.

Scotland’s strengths and potential are closely aligned with current EU priorities,[51] in particular:

- the European Green Deal, aiming to make Europe the first climate-neutral continent by 2050

- transitioning to a circular economy

- education and skills fit for the digital era

- upholding fundamental human rights and promoting equality, tolerance and social fairness; and

- an economy that works for people.

Natural resources

Scotland has significant offshore renewables resources and recently launched the world’s largest floating offshore wind leasing round through ScotWind, which provides seabed rights for potential development of almost 28 GigaWatts (GW) of offshore wind energy, putting Scotland at the forefront of the global development of the sector. Scottish natural capital assets also account, for example, for the majority of the UK’s fishing (88%), renewable energy (58%) and timber (61%).[52]

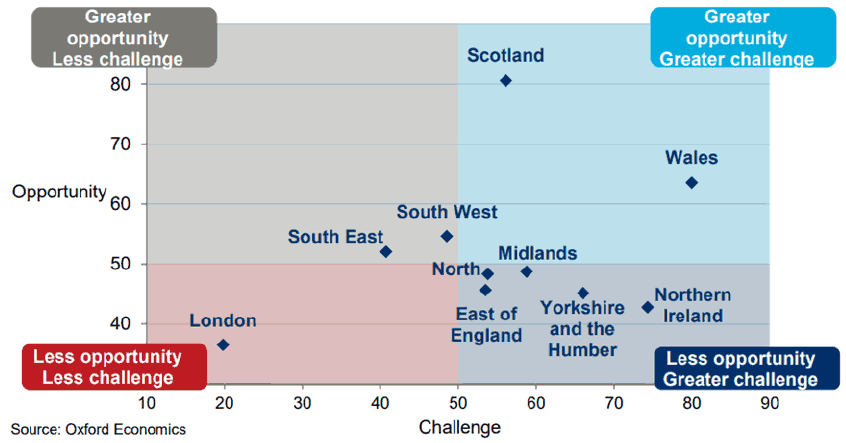

Figure 3, below, shows the Green Growth Index by Oxford Economics, commissioned by the Lloyds Banking Group,[53] which places Scotland first in the UK for green economy opportunities. This reflects Scotland’s existing green industrial base with a growing number of green jobs and innovation activity, take-up of relevant skills and training, and development and use of renewable energy infrastructure. The report ranks the level of green growth challenge for each part of the UK based on an assessment of the relative need to reduce emissions rates and economic reliance on carbon-intensive industry.

Source: Oxford Economics (2021) Lloyds Banking Group UK Green Growth Index

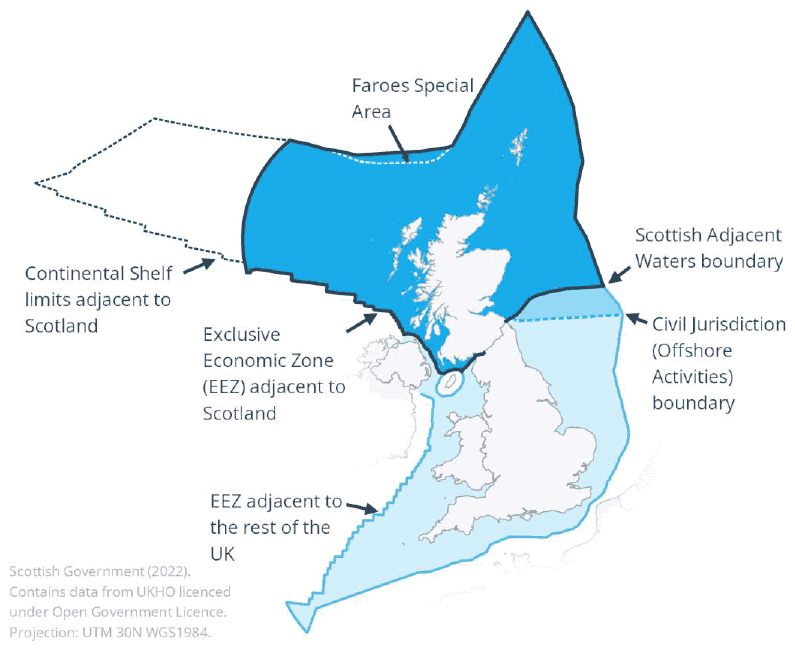

Figure 4 shows Scotland’s share of the UK’s current ‘Exclusive Economic Zone’. Exclusive Economic Zones (EEZs) are areas of the sea over which coastal countries have exclusive sovereign rights and duties in relation to natural resources, such as fish and energy resources.[55] Scotland’s 63% share of the UK’s current EEZ is an estimated 462,315 square kilometres and is nearly six times larger than the land area of Scotland, with 18,743 kilometres of coastline.[56]

Including its entire continental shelf (areas of seabed that can extend beyond the EEZ, where countries continue to have exclusive sovereign rights over natural resources such as oil, but not fish for example),[57] Scotland’s seas are an estimated 617,643 square kilometres (an area around two and a half times the land area of the UK).[58]

As an independent member state of the EU, our EEZ would be the fourth largest of EU member states’ core waters;[59] larger, for example, than those of Ireland, France or Portugal.[60] These waters are not only significant geographically, but are also among the richest in the world in terms of fisheries, marine biodiversity, and offshore renewable energy potential.[61]

Source: Continental Shelf (CS) (Designation of Areas) Order 2013 | Marine Scotland Information © Marine Scotland. Limits and boundaries are explained at Limits and Boundaries | Marine Scotland Information[62]

A rich and diversified economy

Scotland has a rich and diversified economy, with key strengths in areas ripe for growth in the future:[63]

- the energy sector, including renewables, accounted for £20bn gross value added (GVA)[64] in 2019 and 69,000 jobs in 2019. GVA per head was estimated to be over £275,000 in the energy growth sector in 2019[65]

- the food and drink sector accounted for 122,000 jobs in Scotland in 2019, with a GVA of £5.8 billion (2019)[66]

- Scottish salmon is the UK’s largest food export, with an export value of over £600 million in 2019.[67] Scottish fishing and aquaculture (fish and shellfish farming) had a turnover of over £1.1 billion in 2019[68]

- in 2019, Scotch whisky alone accounted for 21% of all UK food and drink exports,[69] and was the UK’s biggest drink export, with turnover of £4.1bn in 2019[70]

- we are home to dynamic creative industries digital skills and technologies including architecture, advertising, performing arts and writing and publishing, and we have growing strengths in . Creative industries (including digital) employed 90,000 people in 2019, with a GVA of £4.2bn in 2019[71]

- we are a world leader in tourism, drawing on Scotland’s long-standing cultural assets and reputation. Tourism employed 229,000 people in 2019, with a GVA of £4.5bn in 2019[72]

- in 2019 financial and business services employed 235,000 people.[73] Scotland has leading positions in responsible and ethical finance. Research published by the ethical finance hub finds that Scotland’s share of the UK’s responsible investing market outweighs its share of the conventional market[74]

- our specialisms in digital technology, including artificial intelligence and cyber security, build on Edinburgh’s international prominence in data and AI and its aim to be the Data Capital of Europe,[75] as well as Dundee’s leadership in gaming, with internationally renowned gaming companies and Abertay University ranked best in Europe for gaming education and 7th best in the world for post-graduate gaming design.[76] The economic potential of Scotland’s digital technologies sector is high and the sector employed 74,000 people and contributed £5.3 billion (GVA) to Scotland’s economy in 2021.[77] The tech sector in Scotland is forecast to be the second fastest growing sector in Scotland to 2029 in terms of GVA (26%) – growing 1.5 times faster than the economy overall (18%)[78]

- we have one of the biggest life sciences clusters in Europe[79] with world leading expertise in drug discovery and precision medicine, medical technologies and pharmaceutical services, digital health and care, animal health and agri-tech. The life sciences sector employed 20,000 in 2019 in 565 diverse organisations, with a GVA of £1.6bn in 2019. Scottish life sciences jobs are highly productive. In 2019, GVA per head was over £ 88,000 in the life sciences sector[80]

- the past decade has seen significant growth in the professional, scientific and technical activities sector, so much so that it is now the largest sector in Scotland in terms of number of businesses (47,240 businesses, 13.7% of Scottish total). 2010-2021 also saw considerable business growth in services, information and communication, education, and arts entertainment and recreation industry sectors[81]

- we have a growing space sector. Almost one fifth of all UK jobs in the space sector are based in Scotland. We are well positioned geographically for the types of orbit best suited to small satellites used for earth observation and we are building on our manufacturing expertise in this area, currently producing more small satellites than any other country in Europe.[82]

Education and skills

With three universities in the overall world top 200, and nine in the top 200 based on international outlook,[83] Scottish universities and colleges are a national success story.

Many of our higher education institutions lead the way in vital areas of research with truly global impacts, and Scotland continues to be seen as a desirable location to study and work for talented undergraduates and researchers.[84]

As a respected partner in European research and innovation programmes, Scotland has expertise and best practice to share, including in areas like artificial intelligence (AI), renewable energy technology, ageing populations and anti-microbial resistance. These are areas that are best tackled collaboratively, across nations.

With our globally-renowned research and innovation, an independent Scotland would be well placed to help the EU achieve its ambition of being a global leader in AI. As outlined in our AI strategy, we share the EU’s commitment to adopting AI using a values-based approach.[85]

Scotland has large clusters of scientists working in life sciences, including Europe’s largest concentration of animal health and aquaculture researchers.[86] As a member state, an independent Scotland would contribute positively in areas of expertise such as energy, the environment and fisheries. We have the third largest salmon aquaculture industry worldwide and are a major exporter of nutritious seafood, with the potential to make a direct contribution to enhancing European food security.

Scotland’s tech sector has particular strengths in software development, data science, biotechnology, sensors, and connectivity. Scotland’s ambition is to become Europe’s leading space nation,[87] with Glasgow already building more small satellites than any other place in Europe. Scotland is therefore well positioned to contribute to the innovation and growth which will be critical to the EU’s long-term prosperity and sustainable growth. With Scotland becoming one of the major hubs for data and technology start-ups,[88] we also have much to contribute to the digital economy, including the computer games sector.

A key example is the £11.5 million InGAME R&D Centre based in the heart of the Dundee video games cluster, led by Abertay University, in partnership with the University of Dundee, the University of St Andrews and local and international industry.[89] InGAME aims to deliver innovative research and offer R&D support and services to games companies. As well as Dundee and Angus College leading the way in e-sports education, using their expertise to deliver a progression pathway that will support the future development of this industry and maximise the educational benefit.[90]

Universities Scotland estimates the GVA of the Scottish Higher Education sector in 2019 was £8 billion.[91]

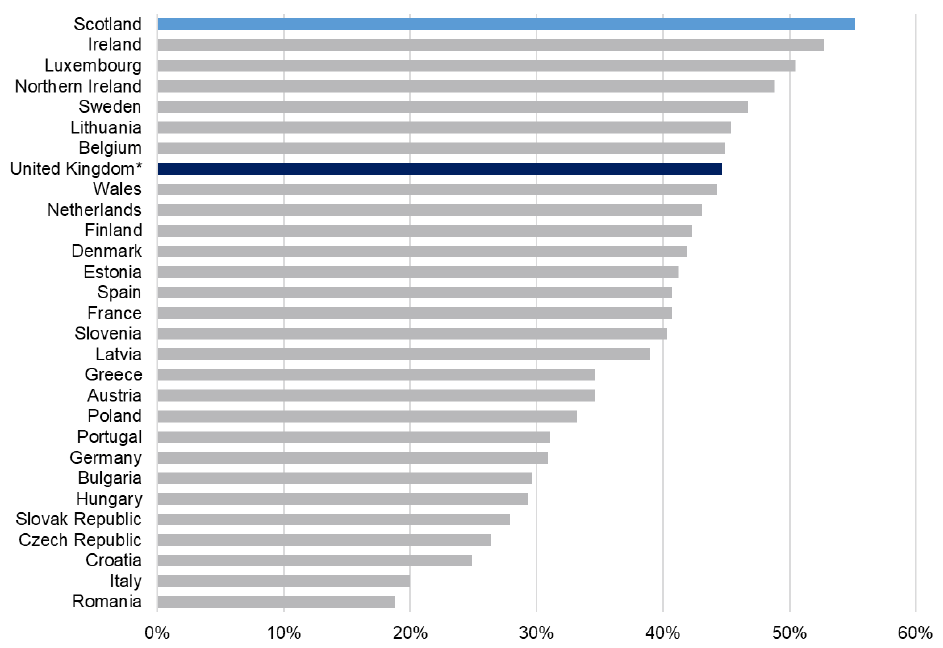

The most recent available data show that Scotland has a higher share of the population aged 25 to 64 years with a tertiary education than the UK or any country in the EU (see Figure 5).[92] This demonstrates that Scotland performs strongly when it comes to investing in skills as measured by tertiary education qualifications.

* UK data are from same OECD source, but was only available up to 2019 at the time these data were accessed Source: OECD Regional Education Statistics (accessed 31/08/22)

Brexit has disadvantaged Scotland in a number of ways relating to education and skills.

For example, the Westminster Government has decided not to participate in Erasmus, depriving thousands of Scottish students the opportunity to study in the EU and worldwide. Erasmus is the European Union's programme for education, training, youth, and sport which, before Brexit, enabled 2,200 Scottish students every year to study or work abroad.[93]

The decision has also seen a reduction in the number of EU students who came to Scotland to study under the scheme. Proportionally more people from the rest of Europe visited Scotland in return under Erasmus and so the reduction in numbers has had an impact on our economy, culture and environment as well as the diversity on campuses.

Brexit has resulted in a reduced number of students from Europe opting to study in Scotland, with the latest applicant statistics showing a 26% decrease in EU applicants applying to Scottish universities between 2021 and 2022.[94]

Another example is Horizon 2020, the EU programme of funding for research, technological development and innovation. Current uncertainty over the UK’s future involvement in this programme is a huge concern to Scotland’s research and innovation community.

Scotland received funding of €874 million from the Horizon 2020 programme over the period of 2014-2020.[95] Scottish organisations were expected to win considerably more funding under the replacement Horizon Europe (2021-2027) scheme.

On re-joining the EU, Scotland would again be able to welcome students from EU countries to our colleges and universities, with EU students, once again, able to enjoy the same access to higher education as Scottish students. It would enable Scottish students to participate in schemes like Erasmus, equipping our young people with the language skills and international outlook required to meet the economic challenges and opportunities we face.

Being part of Horizon Europe would provide access to EU funding: in 2020/21 Scottish higher education institutions received around 7% of their total research income, including funding body grants, from EU government bodies.[96]

It would also provide access to data, equipment, research infrastructure, networks and talent. It would give Scotland a seat at the table when decisions are being made on the future research priorities for the EU, providing the opportunity to shape those in line with expertise in Scotland’s universities and the needs of the Scottish economy and society.

With all the levers at our disposal as an independent country, including a new approach to migration as discussed later in this publication, the higher and further education sectors could play an even greater role in growing the economy.

Conclusions

Scotland has great strengths.

We have a highly educated population and natural resources that would be the envy of most countries.

We lead in the innovative technologies that will both form and support the industries of the future.

We have the strengths to become a successful independent country, matching the performance of comparable countries in Europe.

But we are currently part of an under-performing UK economic model, already suffering the impact of Brexit which will have long-term deep and damaging costs.

Later in this publication, we will set out how the full powers of independence can be used to help realise Scotland’s full potential.

But we first turn to the plan for how Scotland can move from being tied to a poorly performing Brexit-based UK model to an independent country with the powers needed to match the success of comparable independent countries.