Scottish Sea Fisheries Statistics 2020

National Statistics publication that provides data on the tonnage and value of all landings of sea fish and shellfish by Scottish vessels, all landings into Scotland, the rest of the UK and abroad, and the size and structure of the Scottish fishing fleet and employment on Scottish vessels.

Part of

3. Landings

3.1. Landings by Scottish vessels by species type

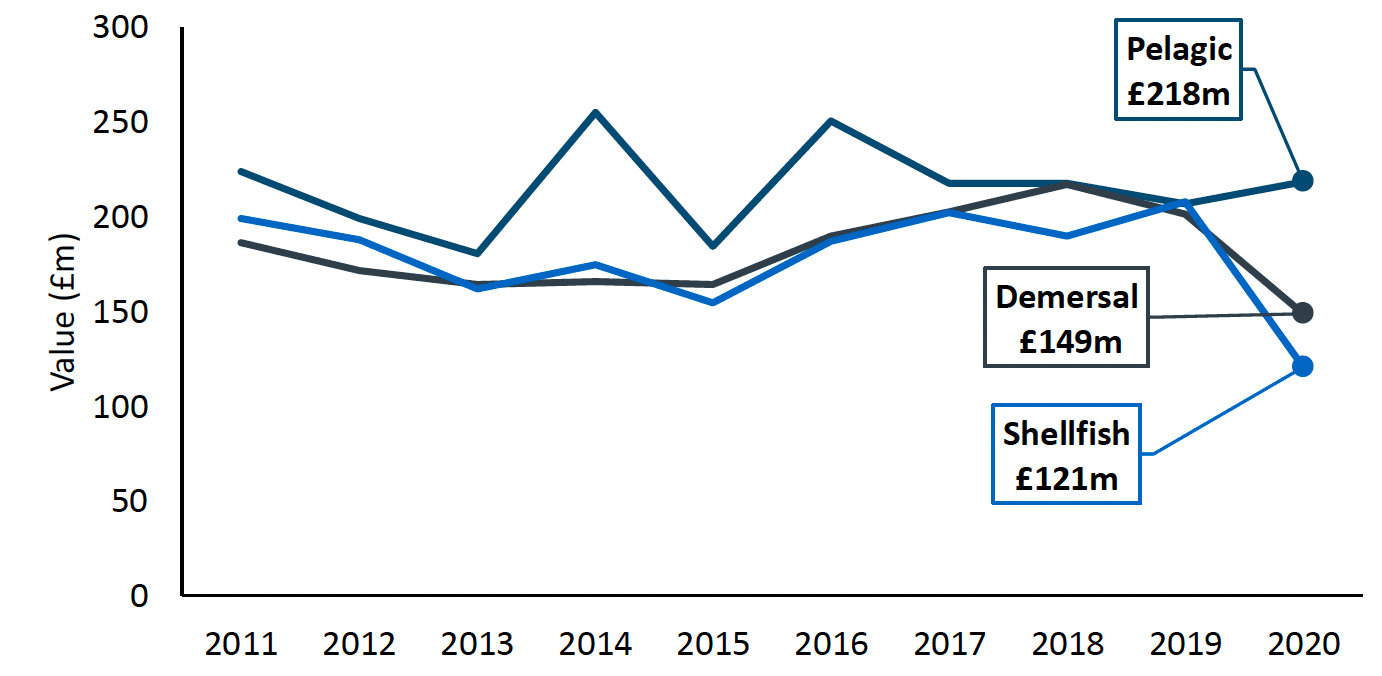

The 21 per cent decrease in the real terms value of landings by Scottish vessels to £488 million, between 2019 and 2020, was driven by a decrease in the value of shellfish and demersal species. The real terms value of shellfish landings decreased by 42 per cent and demersal landings decreased by 26 per cent compared to 2019, whereas pelagic landings increased by six per cent.

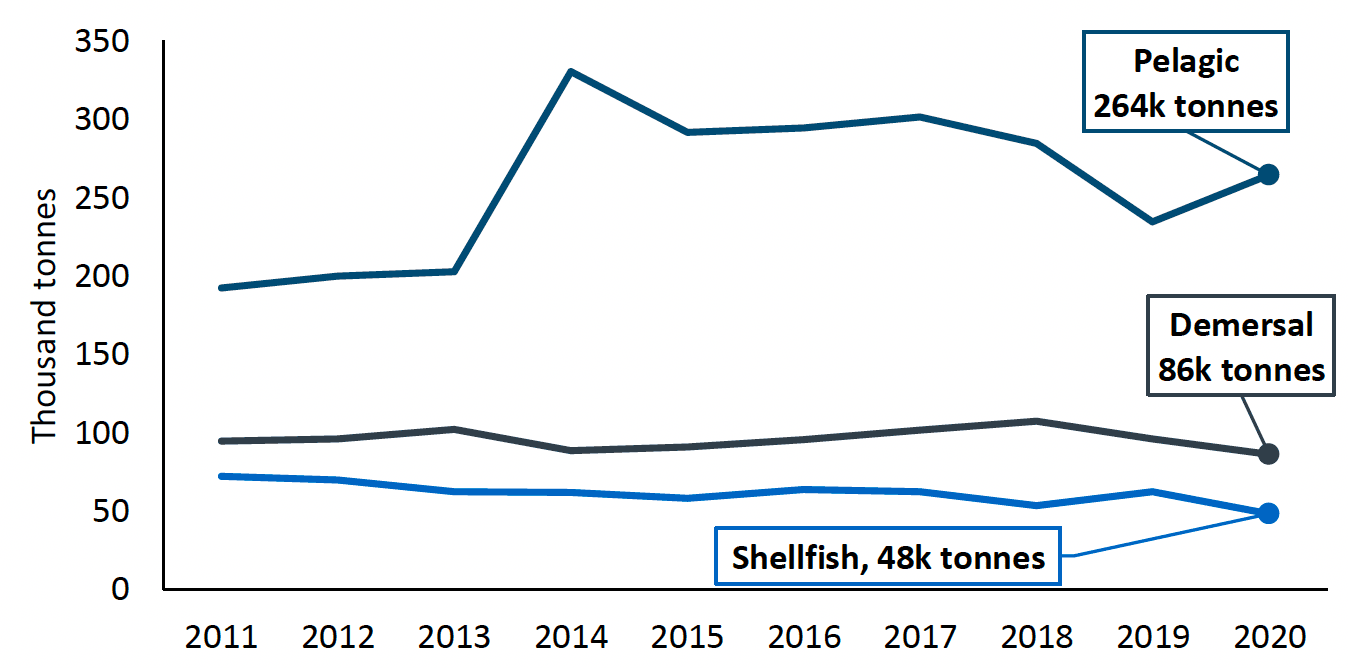

The two per cent increase in tonnage landed by Scottish vessels is attributed to an increase in landings of pelagic fish. Shellfish landings fell 23 per cent by tonnage and demersal landings fell 10 per cent. Pelagic landings increased by 13 per cent.

| Species | Tonnage 2020 | Change from 2019 | Value (£000) 2020 | Change from 2019 |

|---|---|---|---|---|

| Haddock | 23,443 | -13% | 32,550 | -25% |

| Monkfish | 11,507 | 8% | 30,156 | -17% |

| Cod | 8,415 | -42% | 24,087 | -44% |

| Other demersal | 42,712 | -2% | 61,946 | -21% |

| Total demersal | 86,077 | -10% | 148,739 | -26% |

| Mackerel | 170,744 | 34% | 180,893 | 8% |

| Herring | 48,759 | -1% | 27,157 | -1% |

| Other pelagic | 44,898 | -22% | 10,334 | -12% |

| Total pelagic | 264,401 | 13% | 218,384 | 6% |

| Nephrops | 15,946 | -34% | 46,810 | -49% |

| Scallops | 14,579 | -3% | 27,168 | -28% |

| Other shellfish | 17,606 | -24% | 46,607 | -41% |

| Total shellfish | 48,131 | -23% | 120,585 | -42% |

| Total | 398,608 | 2% | 487,708 | -21% |

In 2020, pelagic species represented 66 per cent by tonnage (264 thousand tonnes) and 45 per cent of value (£218 million). Demersal species represented 22 per cent of the tonnage of all landings (86 thousand tonnes) and 30 per cent of the value (£149 million). Shellfish landings accounted for 12 per cent of tonnage (48 thousand tonnes) and one quarter of value (£121 million). This highlights the general difference in prices: shellfish and demersal species generally tend to attract higher prices per tonne than pelagic species.

3.1.1. Pelagic species

Mackerel remained the most valuable species with £181 million, accounting for 37 per cent of the total value of Scottish landings. In 2020, the real value of mackerel landings increased by eight per cent and tonnage increased by 34 per cent in line with an increase in available quota. The real terms value and tonnage of herring both decreased by one per cent since 2019.

Over the ten years 2011-2020, the tonnage of pelagic landings has increased by 37 per cent with real terms value decreasing by two per cent.

3.1.2. Demersal species

Scotland has a mixed demersal fishery which includes more than a dozen species with landings that are worth £1 million or more annually (Table 5). Most demersal species decreased in real terms value compared to 2019 with a modest increase in the value of megrim. The real terms value of megrim increased 14 per cent. The top three demersal species by value are haddock, monkfish (anglerfish) and cod. Haddock remained the most valuable demersal species and represented seven per cent of the total value of Scottish vessels' landings and 22 per cent of the value of demersal landings in 2020. Monkfish accounted for six per cent of the value of Scottish vessels' landings and 20 per cent of demersal landings in 2020. Cod accounted for five per cent of the total value of Scottish vessels' landings and 16 per cent of the value of demersal landings in 2020.

Haddock landings fell in real terms value by 25 per cent but remained the most valuable demersal species at £33 million. The real terms value of monkfish was down 17 per cent to just over £30 million and cod fell 44 per cent to £24 million.

Compared to 2011, demersal landings fell nine per cent with real terms value decreasing by 20 per cent. This is not a long-term decrease and is likely just a reflection of the decrease in 2020 due to the impact of Covid-19.

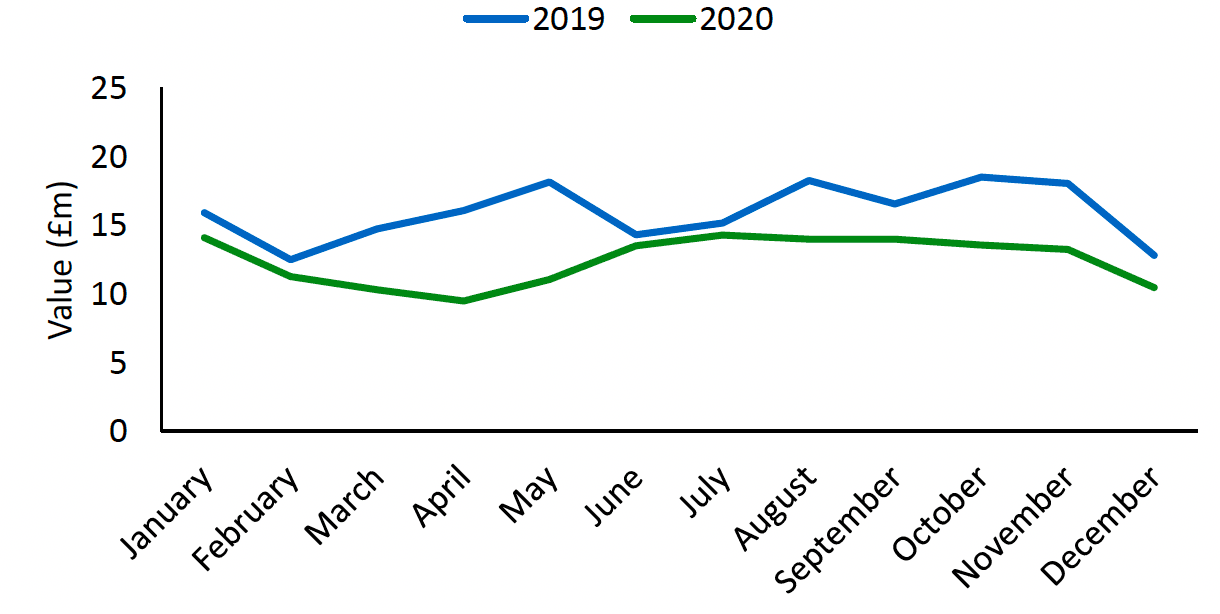

The value of demersal landings in 2020 saw a large decrease (26 per cent decrease in real terms) compared to 2019 (Table a), particularly from March to May (where the decrease ranged from 34 per cent to 44 per cent), which coincides with the first UK coronavirus lockdown (Table b). The lockdowns and restrictions imposed as a result of the Covid-19 pandemic impacted many fishing vessels ability to land and sell fish during these months. Similar, but smaller decreases in value can be seen during the months October to December when further restrictions and a second lockdown were introduced (Table b, Chart 4).

| 2019 | 2020 | ||||

|---|---|---|---|---|---|

| Month | Tonnes landed (000's) | Value (£m) | Value (real terms) (£m) | Tonnes landed (000's) | Value (£m) |

| January | 8 | 16 | 17 | 7 | 14 |

| February | 7 | 12 | 13 | 6 | 11 |

| March | 7 | 15 | 16 | 6 | 10 |

| April | 9 | 16 | 17 | 6 | 9 |

| May | 10 | 18 | 19 | 9 | 11 |

| June | 8 | 14 | 15 | 9 | 13 |

| July | 8 | 15 | 16 | 8 | 14 |

| August | 8 | 18 | 19 | 7 | 14 |

| September | 8 | 17 | 17 | 7 | 14 |

| October | 8 | 18 | 20 | 7 | 14 |

| November | 9 | 18 | 19 | 7 | 13 |

| December | 6 | 13 | 14 | 6 | 10 |

As well as the restrictions imposed as a result of the Covid-19 pandemic, there was also a disruption to market demand and prices for some species due to the closure of the restaurant and hospitality sector in the UK and abroad during these months. Fishing businesses were provided with financial support from the government as a result of the hardship they experienced during the Covid-19 pandemic.

3.1.3. Shellfish species

Nephrops are the most valuable shellfish stock and the only shellfish species currently subject to quota. The Scottish fleet fish for Nephrops by creeling and by trawling. Creeled Nephrops are often caught and exported live. Creeled Nephrops represent a smaller tonnage of landings, but attract a price per tonne more than three times that of trawled Nephrops. The average price per tonne of creeled Nephrops was £10,059 per tonne while for trawled Nephrops the average price was £2,317 per tonne. In 2020, 1,271 tonnes of creeled Nephrops were landed by the Scottish fleet with a value of £13 million[3]. Fifteen thousand tonnes of trawled Nephrops were landed worth £34 million[4]. These data are presented in Table 27c.

Scallops contribute six per cent to the overall value landed by Scottish vessels and were worth £27 million in 2020. Edible crabs, velvet swim crabs and lobsters make up a small proportion of overall value landed by Scottish vessels (seven per cent combined) but are important for Scotland's large creel-fishing fleet, particularly those limited to inshore waters.

Tonnage of edible crabs decreased from 2019, by 26 per cent to eight thousand tonnes and the value in real terms decreased by 45 per cent to £15 million. Tonnage of lobsters decreased by 12 per cent from 2019, to 1,082 tonnes and the value in real terms decreased by a quarter (25 per cent) to £14 million.

Over the period 2011 to 2020, shellfish landings have fallen by 33 per cent while real terms value has fallen by 39 per cent. This decrease is mainly a result of the fall in landings and value in 2020 due to the impact of Covid-19. Overall the shellfish sector in 2020 saw large decreases in tonnage (23 per cent) and value (42 per cent in real terms) compared to 2019 (Table a).

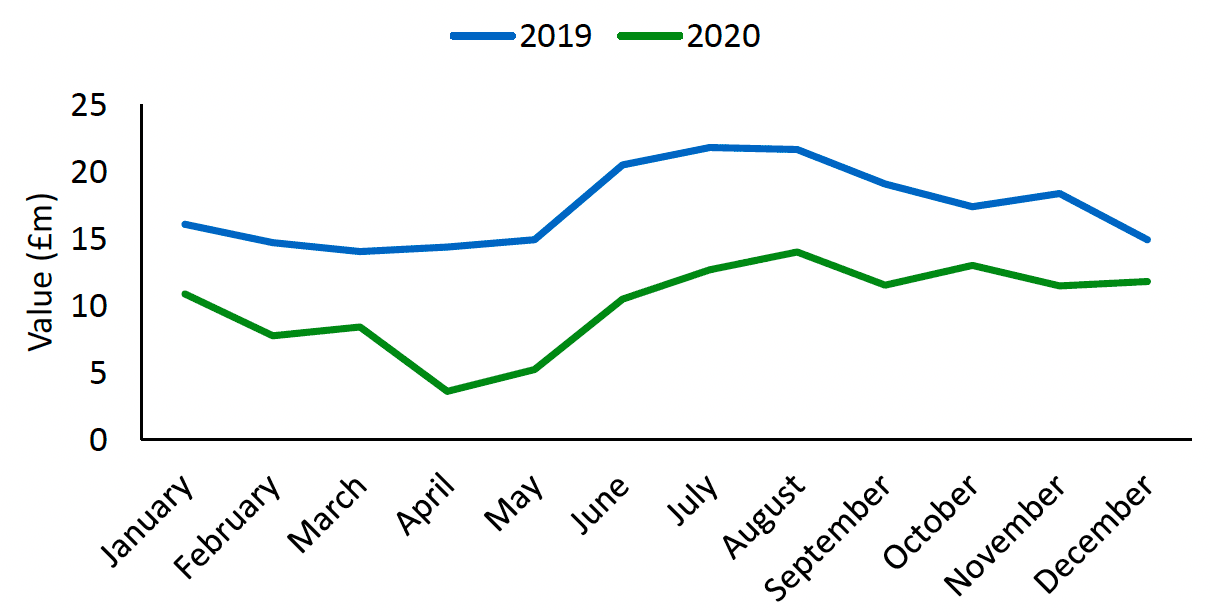

Coronavirus and the lockdowns associated with it had a large impact on the shellfish sector, particularly during lockdown months April 2020 and May 2020.

In April 2020, shellfish landings and value were down by 60 per cent and 75 per cent (in real terms) respectively compared to April 2019 (Table c, Chart 5).

While April and May were particularly poor months for the shellfish sector, both landings and value decreased in every month in 2020 compared to 2019, showing the impact that Covid-19 had on this sector.

| 2019 | 2020 | ||||

|---|---|---|---|---|---|

| Month | Tonnes landed (000's) | Value (£m) | Value (real terms) (£m) | Tonnes landed (000's) | Value (£m) |

| January | 4 | 15 | 16 | 4 | 11 |

| February | 4 | 14 | 15 | 3 | 8 |

| March | 4 | 13 | 14 | 3 | 8 |

| April | 4 | 14 | 14 | 2 | 4 |

| May | 4 | 14 | 15 | 2 | 5 |

| June | 6 | 19 | 21 | 5 | 10 |

| July | 7 | 21 | 22 | 5 | 13 |

| August | 6 | 20 | 22 | 5 | 14 |

| September | 6 | 18 | 19 | 5 | 12 |

| October | 6 | 16 | 17 | 6 | 13 |

| November | 6 | 17 | 18 | 5 | 11 |

| December | 4 | 14 | 15 | 4 | 12 |

Hospitality closures due to Covid-19 resulting in a loss of trade and markets particularly affected the shellfish sector. Both foreign and domestic foodservice markets collapsed as a result of hospitality closures and both import and export markets were further constrained by reduced transport and logistic timetables. Fishing businesses were provided with financial support from the government as a result of the hardship they experienced during the Covid-19 pandemic.

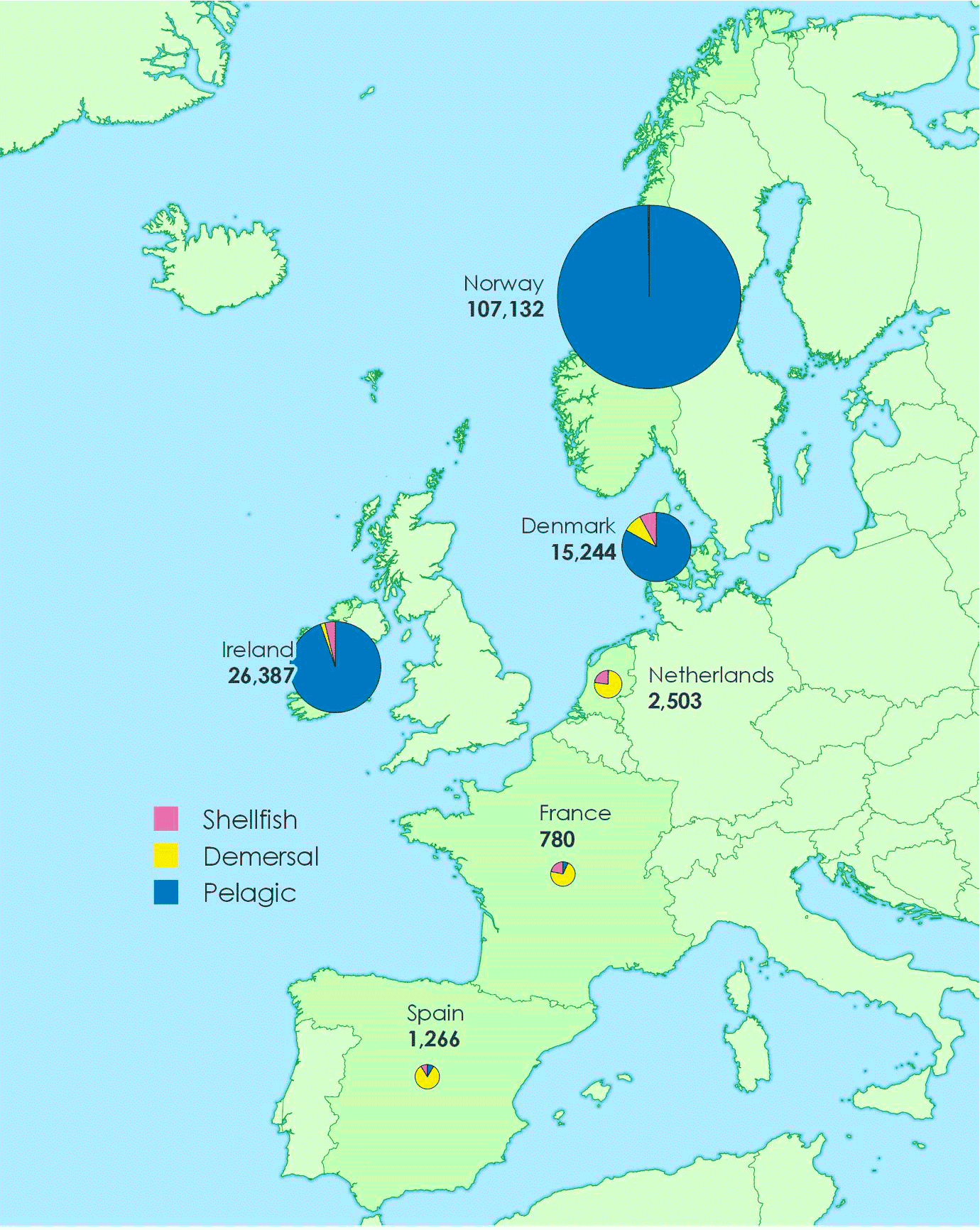

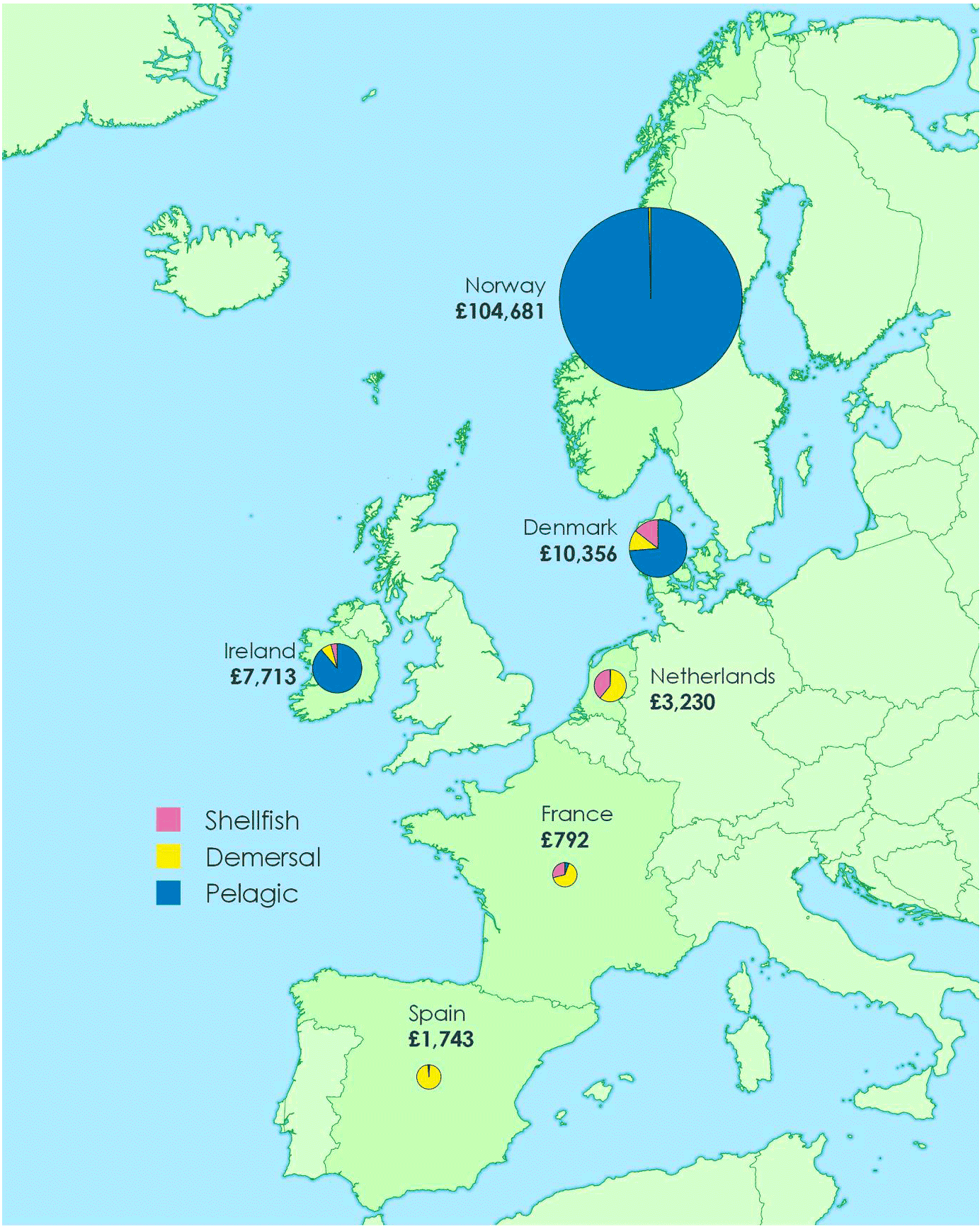

3.2. Landings abroad by Scottish vessels

In 2020, Scottish vessels landed 153 thousand tonnes of sea fish and shellfish worth £129 million abroad. The tonnage landed abroad increased by three per cent and the real terms value of landings abroad decreased by two per cent compared to 2019 (Table 4). Landings abroad accounted for 38.5 per cent of all landings by Scottish vessels by tonnage and 26.4 per cent by value. Of this, 94 per cent of the tonnage landed abroad was pelagic, four per cent was demersal and two per cent was shellfish.

The main species landed abroad was mackerel, representing 77 per cent of the total value of fish landed abroad in 2020. Since 2019, mackerel landings abroad have increased in tonnage by 30 per cent and increased in real terms value by six per cent. There were 93 thousand tonnes of mackerel worth £99 million landed abroad, which is 54 per cent of the total tonnage and 55 per cent of the value of mackerel landed by Scottish vessels. The price for mackerel landed into the UK was an average of £1,046 per tonne and mackerel landed abroad was an average of £1,071 per tonne in 2020.

Norway is by far the largest destination for Scottish vessels' landings abroad, accounting for 70 per cent by tonnage and 81 per cent by value of all Scottish vessels' landings abroad. Landings into Norway increased 42 per cent by tonnage compared to 2019 and the real terms value of these landings have increased by 24 per cent (Table 25). The increase in tonnage of mackerel landings into Norway is consistent with the increase in overall tonnage of landings of mackerel by Scottish vessels. Nearly all Scottish landings into Norway were of pelagic species.

In 2020, 87 per cent of the value of landings into Norway was for mackerel, amounting to 83 thousand tonnes with a value of £91 million.

Key countries for demersal landings were the Netherlands, Denmark and Spain. Scottish vessels landed 5,600 tonnes of demersal species abroad with a value of just over £6.4 million.

There was 3,112 tonnes of shellfish landed abroad by Scottish vessels in 2020, an increase of 13 per cent on 2019. These were mainly into Denmark, Ireland and the Netherlands.

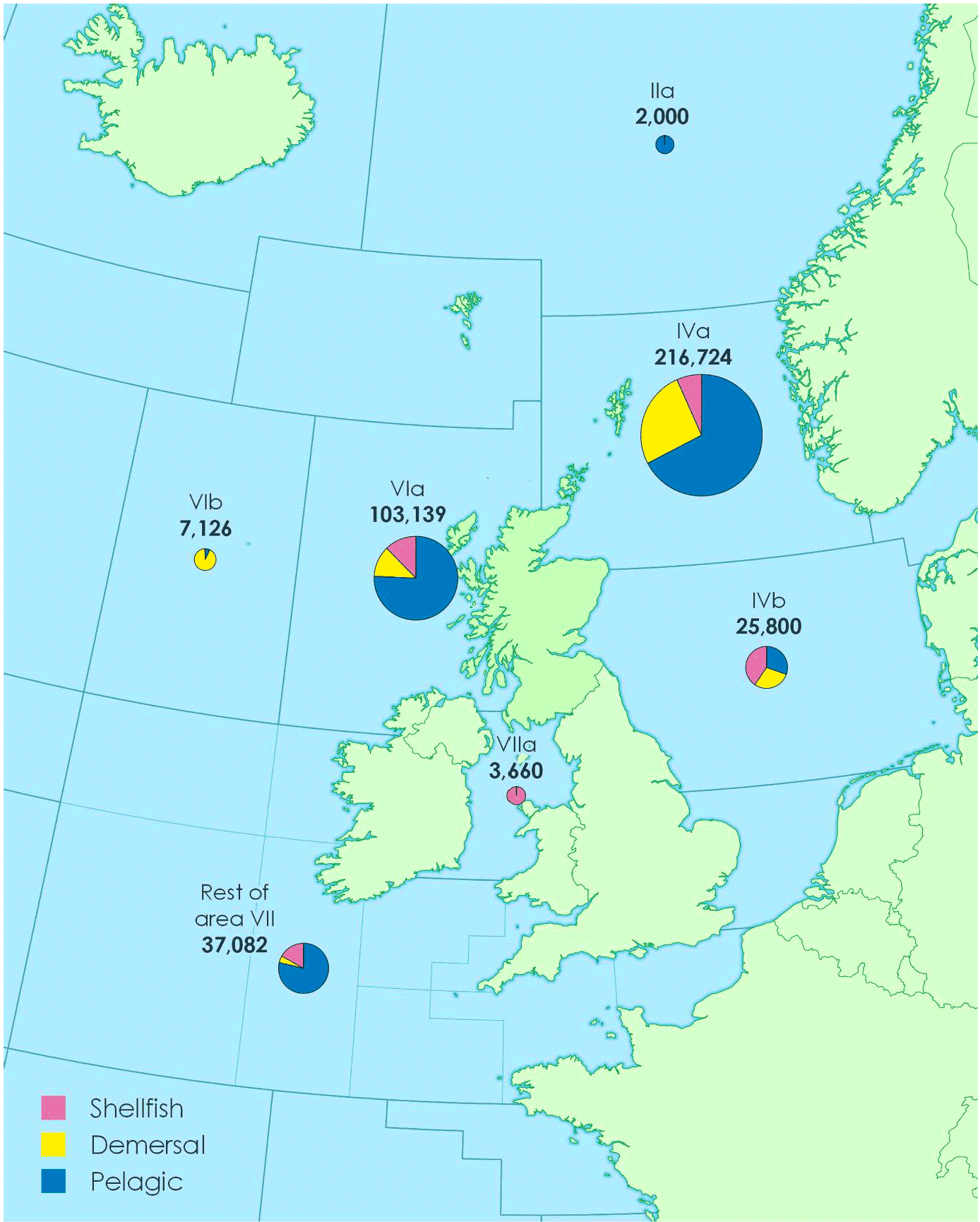

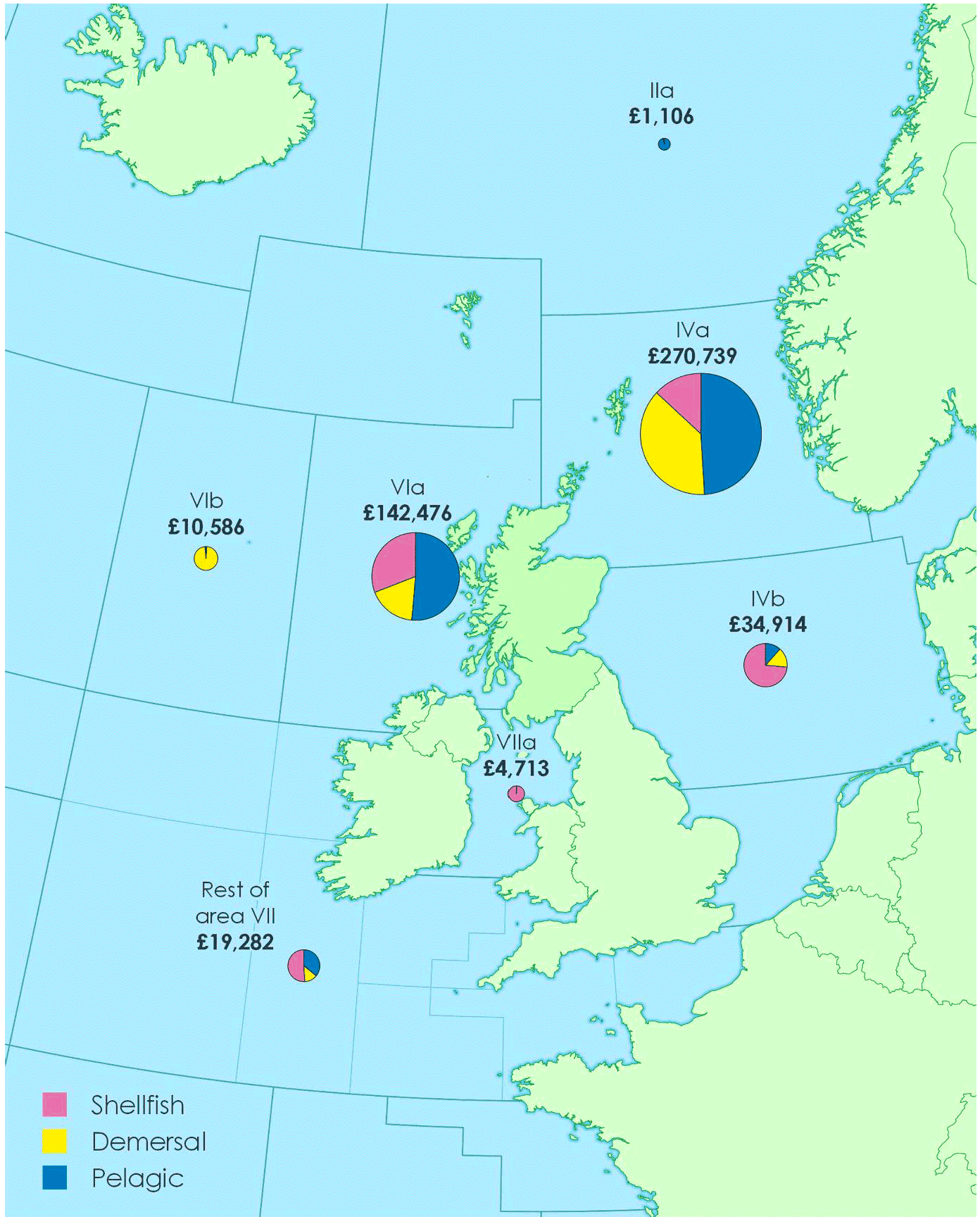

3.3. Landings by area of capture

Scottish vessels are most active in two main ICES Rectangles [5]: the Northern North Sea (ICES Area IVa) and the West Coast of Scotland (ICES Area VIa). Two-hundred and seventeen thousand tonnes of sea fish and shellfish with a value of £271 million were landed from the Northern North Sea, representing 54 per cent of the tonnage and 56 per cent of the value of all landings by Scottish vessels (Table 28). Just over one quarter (26 per cent) of landings by Scottish vessels, by tonnage were caught in the West Coast of Scotland (VIa), providing 29 per cent of the total value of all Scottish landings. Area VII (excluding the Irish Sea) accounted for nine per cent of the tonnage of all landings and four per cent of value.

By species type, 65 per cent of the tonnage of all demersal landings by Scottish vessels was caught in the Northern North Sea (IVa), and 14 per cent in the West Coast of Scotland (VIa). For pelagic landings, 55 per cent by tonnage were caught in the Northern North Sea (IVa) and 30 per cent were caught in the West Coast of Scotland (VIa).

Consistent with 2019, a higher tonnage of shellfish species was caught in the Northern North Sea than in the West Coast of Scotland (Area VIa). The Central North Sea (ICES Area IVb) and area VII (excluding the Irish Sea)) are also areas of considerable activity for shellfish fisheries. By tonnage, shellfish catches from the Northern North Sea (IVa) accounted for 30 per cent of all shellfish landings and 27 per cent of shellfish landings were caught in the West Coast of Scotland. Twenty two per cent of shellfish catches were from the Central North Sea (IVb), 13 per cent in area VII (excluding the Irish Sea) and eight per cent were from the Irish Sea (VIIa). Almost all landings from the Irish Sea were of shellfish species.

Further data on fishing activity in the seas around the UK by Scottish vessels, other UK vessels and foreign vessels that land into the UK are available by ICES rectangle on the Scottish Sea Fisheries Statistics website (see Annex 3). These data show the tonnage and value of landings by species and fishing effort by ICES rectangle. Maps on fishing activity in Scottish waters by Scottish vessels, other UK vessels, and foreign vessels that land into the UK are available on the National Marine Plan Interactive (NMPi) webpage.

3.4. All landings into Scotland

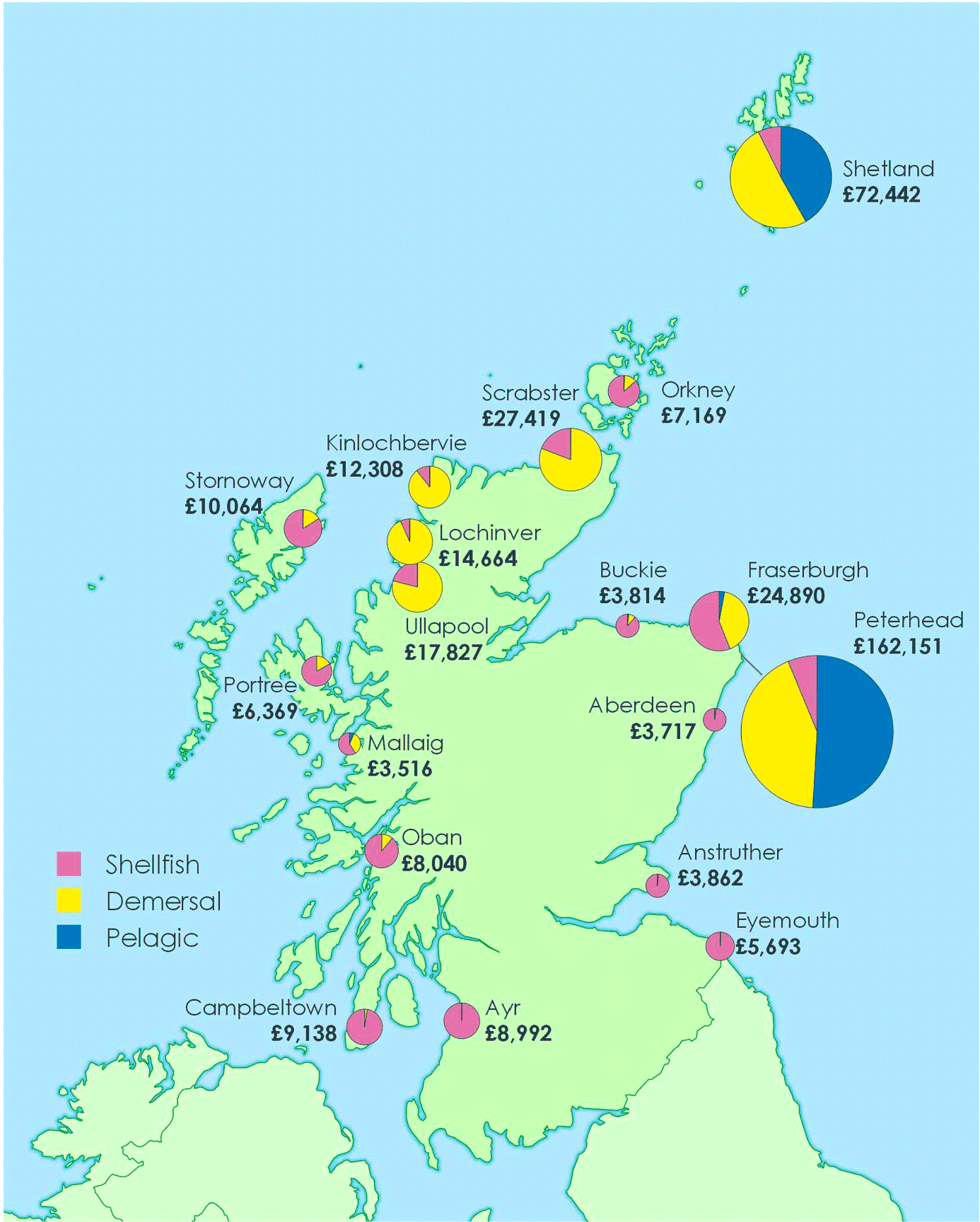

In 2020, 287 thousand tonnes of sea fish and shellfish with a value of £402 million were landed into Scotland. This represents a four per cent decrease in tonnage and a 27 per cent decrease in real terms value from 2019. Landings of pelagic species accounted for 47 per cent, demersal species 40 per cent and shellfish species 13 per cent of the total tonnage landed into Scotland. By value, almost half (46 per cent) of landings into Scotland were demersal species, 28 per cent were pelagic and 26 per cent were shellfish species. The differences in shares by tonnage and value reflect the differences in average prices per tonne (for landings by Scottish vessels) across the species types: shellfish sell at relatively higher average prices per tonne, whilst pelagic species receive the lowest average prices per tonne (Table 23).

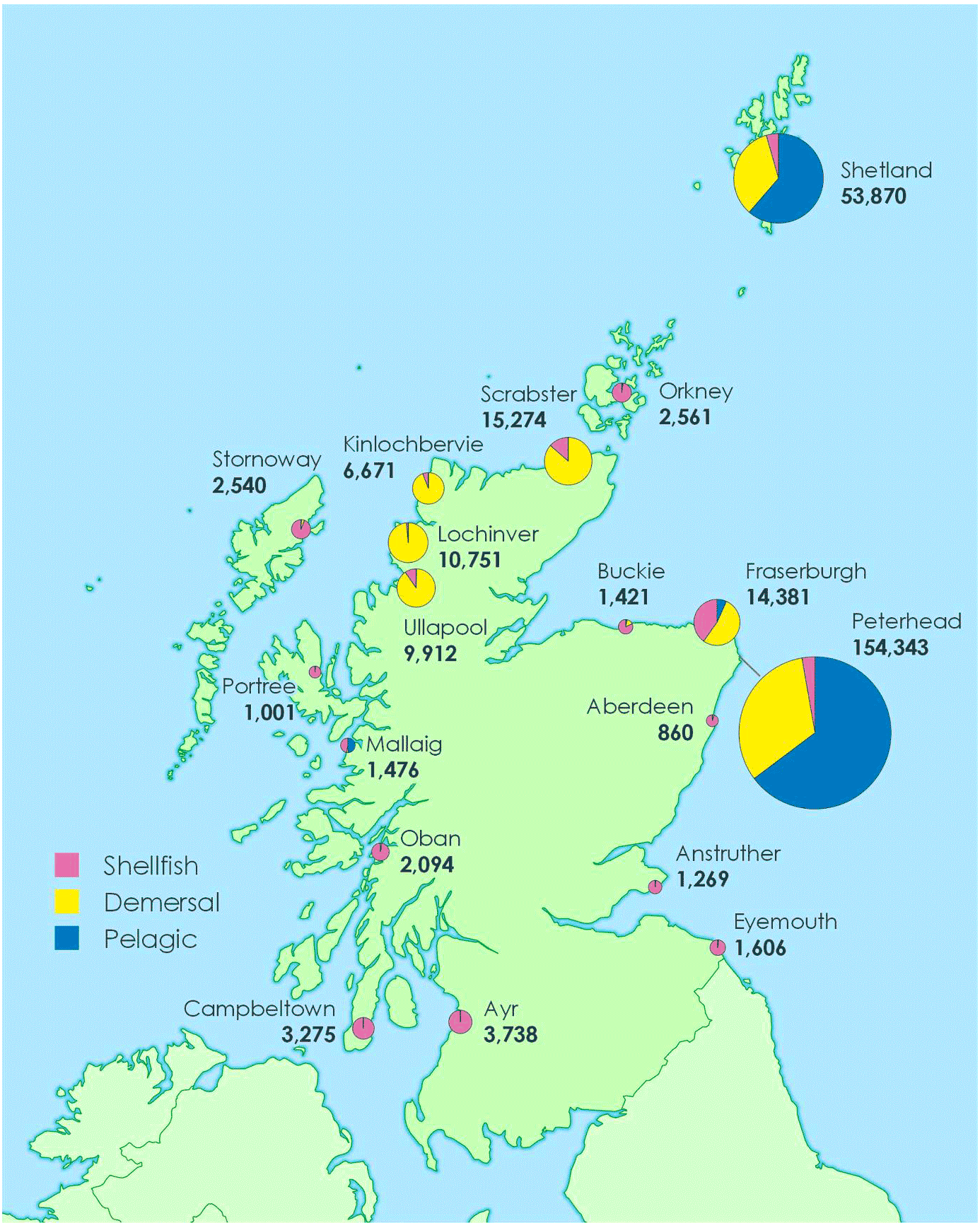

Figures 6 and 7 show landings by all vessels by species type into the eighteen Scottish port districts (also in Table 29). Landings into the south-west coast (districts Ayr, Campbeltown and Oban) and south-east coast (districts Anstruther and Eyemouth) were dominated by shellfish, while landings into the north-west coast (particularly districts Kinlochbervie, Lochinver and Ullapool) were mostly demersal and the north-east coast (particularly districts, Peterhead and Shetland) had most of the pelagic landings. The top three districts in Scotland by total tonnage landed were Peterhead (east coast), Shetland (northern island) and Scrabster (north-east coast). Peterhead is the single largest fishing port in the UK by tonnage and value of landings.

Combined, the top three districts for tonnage in 2020, accounted for 78 per cent of total weight landed and 65 per cent of value of all landings into Scotland. Peterhead had 154 thousand tonnes landed in 2020, with a value of £162 million. This represents a seven per cent increase in tonnage and a 16 per cent decrease in real terms value from 2019. By tonnage, over three-fifths (65 per cent) of the landings into Peterhead comprised pelagic species and these accounted for just over half (51 per cent) of the landings value into the district. Thirty-two per cent of the tonnage landed into Peterhead was demersal species that accounted for 43 per cent of the value.

Landings into Shetland totalled 54 thousand tonnes (up four per cent from 2019) and were valued at £72 million (down 17 per cent in real terms). As with Peterhead, the majority of landings into Shetland by tonnage were of pelagic species, which represented 61 per cent of the total tonnage landed and 42 per cent of the total value of landings. Demersal species accounted for 34 per cent of the tonnage and just over half (51 per cent) of the value landed into Shetland.

Landings into Scrabster totalled 15 thousand tonnes (down 16 per cent from 2019) worth £27 million (down 33 per cent in real terms). The largest landings were of demersal species, which represented 86 per cent of the tonnage landed and 81 per cent of the total value of landings. Shellfish species accounted for the remaining 14 per cent of tonnage and 19 per cent of the value landed into Scrabster, with pelagic species making up less than 0.5 per cent of the tonnage and value.

The largest percentage fall in tonnage landed compared to 2019 was into Mallaig (48 per cent fall) with lower landings into the district of demersal species, sprats, Nephrops, Scallops and other shellfish species being the main factors. The largest percentage rise in tonnage was into Peterhead (up seven per cent) due to increased landings of mackerel following an increase in available quota.

3.5. Total Allowable Catches quota and uptake

Total Allowable Catches (TAC) are limits set at annual international negotiations for individual fish stocks and represent the maximum of each fish stock that can be caught. For 2020, and while the UK was still a member of the European Union (EU) the majority of stocks were managed and fished only by EU member states. Member states access to the management and fishing of stocks is based on a number of factors including historic track record. The TACs for these stocks were set by the European Commission through internal negotiations between EU member states with an interest and based on independent scientific advice from ICES. The remaining stocks are managed and shared with other Coastal States: Norway, Iceland, the Faroe Islands, Greenland and Russia, with TACs for these set at separate negotiations. The EU TAC is shared among EU member states based on a number of factors, including each member state's past catch record. The amounts corresponding to this share, known as quotas, are shown at the UK and at the Scottish Producers Organisations' (POs) level in Table 33a. Uptake of key commercial quota stocks by all Scottish vessels by tonnage and value landed are presented in Table 34.

In general, Scottish POs had high quota uptake in 2020, for key demersal and pelagic species. Uptake of mackerel and herring stocks in both the West of Scotland and the North Sea were all above 99 per cent with herring in the North Sea and mackerel in the West of Scotland exceeding quota[6]. West of Scotland cod has a nil quota and is managed as a bycatch.

For demersal stocks, uptake in the North Sea was generally high with cod quota uptake at 99.6 per cent and haddock at 80 per cent. The Scottish quota reduction for cod of more than 50%, between 2019 and 2020, led to an increased pace of quota uptake, reflecting the importance of this species to the domestic fleet. Uptake of plaice, megrim and sole was lower (34 – 61 per cent). In the West Coast, demersal uptake was slightly more varied for each species than the North Sea. Haddock uptake was fairly low compared to 2019 at 70 per cent in area Vb, VIa and just 52 per cent in area VIb, XII, XIV. Monkfish uptake reached 95 per cent in the West Coast but was lower in the North Sea IIa(EU) and IV(EU)) at 71 per cent.

Pelagic species have consistently high quota uptake for both the West Coast and North Sea. Mackerel quota uptake was 102 per cent in the West Coast and 99 per cent in the North Sea. This is five percentage points down on 2019, for the West Coast and eight percentage points down for the North Sea. However, there was a significant increase in available quota for West Coast mackerel in 2020, compared to 2019, so this lower uptake does not mean a lower tonnage landed.

For herring, West Coast uptake was at 99.6 per cent and North Sea uptake was 103 per cent.

The only shellfish species subject to quota is Nephrops. In 2020, Scottish PO quota uptake for North Sea Nephrops was 61 per cent and for West Coast Nephrops it was 43.5 per cent. This is 36 percentage points down compared to 2019, for the North Sea and 17 percentage points down for the West Coast.

Contact

Email: fisheriesstatistics@gov.scot