Scottish Housing Market Review Q2 2026

Quarterly bulletin collating a range of previously published statistics on the latest trends in the Scottish housing market.

Part of

8. Mortgage Arrears and Possessions

8.1. Arrears

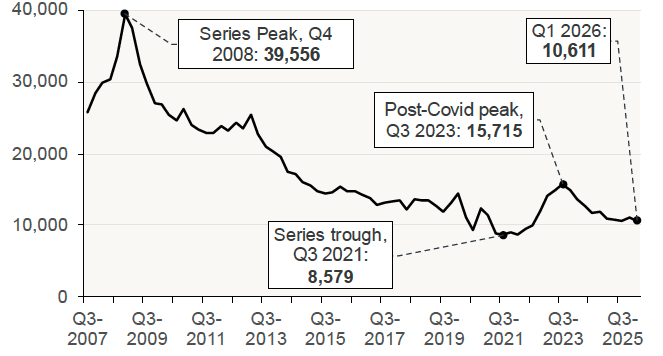

The number of regulated mortgage accounts entering arrears in the UK nearly doubled (up 83%) over the period from Q3 2021 to Q3 2023 as inflation and interest rates spiked. The number of mortgages entering arrears then fell by nearly a third (32%) between Q3 2023 and Q3 2025 following an easing in inflation and interest-rate trends, and since then has levelled off.

Chart 8.1 Number of regulated mortgage loan accounts entering arrears: UK (Quarterly data, to Q1 2026)

Source: FCA. Includes both securitised and unsecuritised loans.

The decrease in mortgages entering arrears since Q3 2023 has fed through to the total stock of regulated UK mortgage accounts in arrears, which has fallen by 10% from a post-pandemic peak of 148,943 in Q2 2024 to 129,887 in Q1 2026. [Source: FCA]

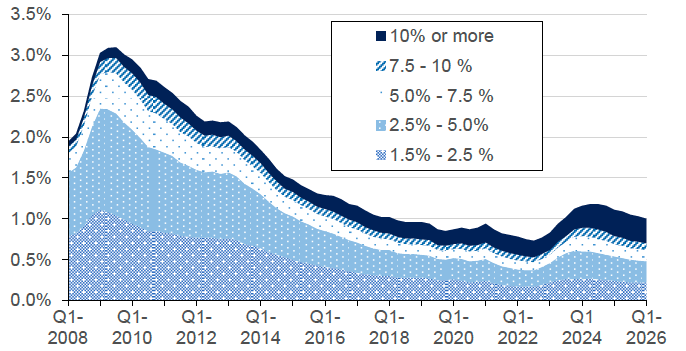

Similarly, Chart 8.2, which breaks down arrears by degree of severity, shows that the share of lenders' outstanding regulated mortgage balances in arrears of more than 1.5% of the outstanding loan balance has edged down from a recent peak of 1.2% to stand at 1.0% in Q1 2026. However, this remains above the post-pandemic low of 0.7% in Q3 2022.

Chart 8.2 Regulated mortgage balances in arrears by severity: UK (Quarterly data, to Q1 2026)

Source: FCA. Includes both securitised and unsecuritised loans; share is calculated as balances on cases which are in arrears expressed as a % of total loan balances.

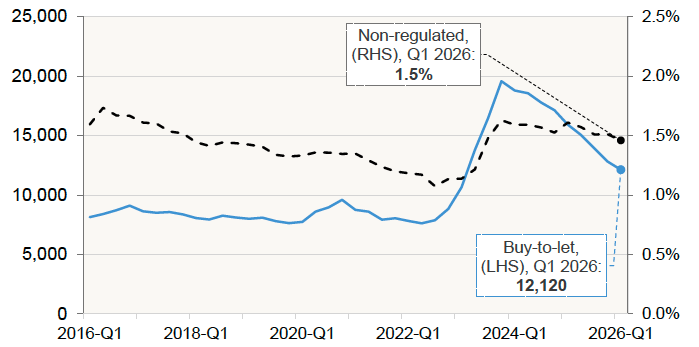

UK Finance data shows that there were 12,120 buy-to-let (BTL) mortgages in arrears of 1.5% or more of the outstanding balance across the UK at the end of Q1 2026, down by 5.4% from the previous quarter. This is the ninth consecutive quarter-on-quarter fall, with the number of BTL mortgages in arrears falling by 38% since its recent peak of 19,570 in Q4 2023. BTL mortgages in arrears as share of total BTL mortgages has fallen from 0.99% to 0.63% over this period.

FCA data for non-regulated lending (which includes BTL lending but also some other types of lending and is collected on a somewhat different basis[5]) shows that at the end of Q3 2025 mortgages which were 1.5% or more in arrears represented 1.5% of the total non-regulated residential loans, unchanged from the previous quarter.

Chart 8.3 Number of Buy to Let mortgages, and share of non-regulated mortgages, in arrears of 1.5% or more of loan balance, UK (Quarterly data, to Q1 2026)

Source: Buy to Let – UK Finance; Non-regulated loans – FCA. FCA data includes both securitised and unsecuritised loans; the share of loans in arrears is the number of loans in arrears as a percentage of all non-regulated loans.

8.2. Possessions

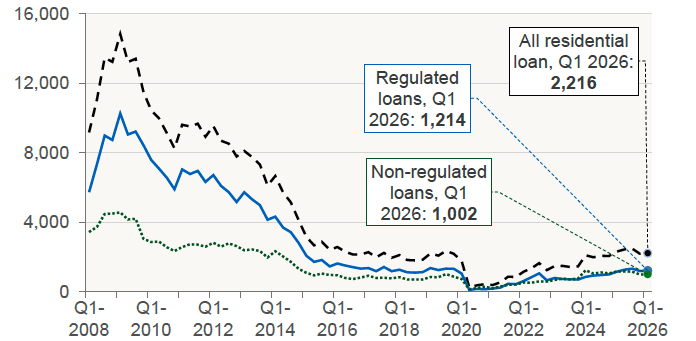

For regulated mortgages in the UK, the downward trend in the number of mortgages entering arrears and the stock of mortgages in arrears has not yet translated into falling possessions, with the 1,214 new possessions in Q1 2026 representing an annual increase of 5.4%. However, the rate of growth of possessions has eased, down from an annual growth rate of 43% in Q4 2024, and the level of possessions remains below its pre-Covid levels (a quarterly average of 1,318 in 2019). [Source: FCA]

Meanwhile, there were 1,002 non-regulated mortgage possessions in the UK in Q1 2026. This represents a 1.0% increase compared to the previous quarter, but a decrease of 13.8% compared to the corresponding quarter in 2025. The number of non-regulated mortgage possessions remains above its pre-Covid levels (a quarterly average of 889 in 2019). [Source: FCA]

With respect to BTL mortgages (a component of non-regulated mortgages), UK Finance data show that there were 810 BTL mortgages in the UK taken into possession in Q1 2026, a 5.2% increase from the previous quarter, but unchanged on the year. New possessions were also above pre-Covid levels (the 2019 quarterly average was 668).

Chart 8.4 New possessions by type of mortgage: UK (Data as at end of quarter, to Q1 2026)

Source: FCA

Contact

Email: Bruce.Teubes@gov.scot