Scottish Housing Market Review Q2 2026

Quarterly bulletin collating a range of previously published statistics on the latest trends in the Scottish housing market.

Part of

3. Residential Land and Buildings Transaction Tax

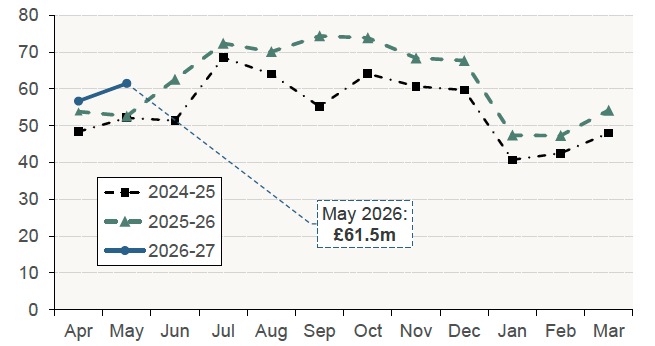

Provisional estimates indicate that revenue from Residential LBTT (excluding the Additional Dwelling Supplement) in financial year 2025/26 was £744.8 million, an annual increase of £89.5 million (13.7%). Growth in both the average purchase price of a property and the number of transactions has contributed to this growth, which was similar to the revenue growth recorded in the previous financial year (13.1%).

More recently, provisional estimates indicate a slight softening in the growth rate, with revenues across April and May 2026 up by an annual 11.1%.

Chart 3.1 Residential LBTT revenue (excluding ADS), £ millions (Monthly data, to May 2026)

Source: Revenue Scotland

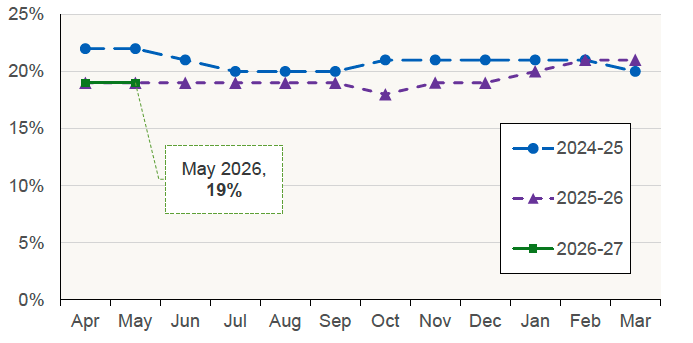

Chart 3.2 plots the percentage of total residential returns received where ADS was declared due. ADS is a flat rate tax (payable in addition to LBTT) on the purchase price of an additional residential property (e.g. a second home). It was first introduced in 2016, with the tax rate initially set at 3%, before being increased to 4% in January 2019, 6% in December 2022 and 8% in December 2024. There was a significant decline in the share from February 2024 (25%) to April 2025 (19%). After some fluctuation in the remainder of 2025-26, the share has remained around 19% in the first two months of 2026-27.

Chart 3.2 Percentage of residential returns received where ADS was declared due (Monthly data, to May 2026)

Source: Revenue Scotland

Contact

Email: Bruce.Teubes@gov.scot