Scotland's fiscal outlook: medium-term financial strategy

This is the seventh Medium-Term Financial Strategy published by the Scottish Government. It provides the economic and fiscal context for the Scottish Budget and sets the medium-term strategy for sustainable public finances.

Chapter 3: Scotland’s Spending Outlook

This chapter will explore the drivers of growth in public spending in Scotland from the starting point of the 2025-26 Scottish Budget. This approach assumes, for the purpose of illustrating the drivers of public spending and pressures on the Scottish Budget, that the Scottish Government’s current policies and services continue.

3.1 Summary of resource spending position and fiscal gap

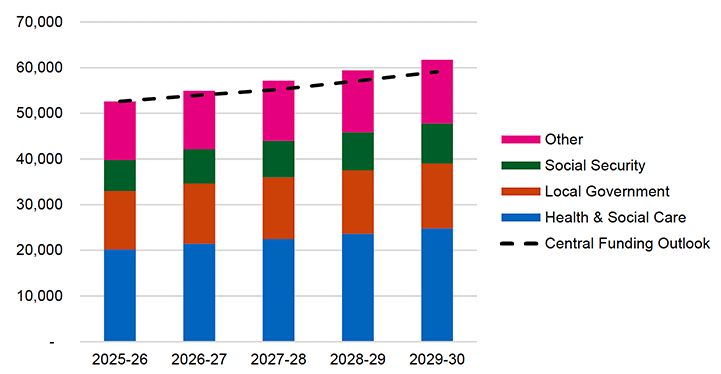

The 2025-26 Scottish Budget was set at a total value of £58.6 billion for resource and capital spending combined.[31] Resource spending comprises nearly 90 per cent of this, with spending on Health and Social Care, Local Government and the public sector paybill being the largest components of spending, as well as some of the main drivers of the expected growth in future spending.

We take the 2025-26 Scottish Budget as the baseline position for resource spending and apply specific growth assumptions to each of the different areas of spend, as set out in Section 3.3 Resource Spending Outlook. When combined, resource spending increases from £52.6 billion[32] in 2025-26 to £61.7 billion in 2029-30.

Forecast growth in spending is 4.1 per cent per year in nominal terms on average over our medium-term horizon. This is between 1.7 per cent and 2.0 per cent higher than forecast inflation each year, and, more significantly for the public finance outlook, higher than forecast funding growth, which averages 2.9 per cent per year in nominal terms under the central funding scenario for the period.

Source: Scottish Government

The Scottish Government has made a conscious decision to invest in the people of Scotland through policy choices such as concessionary travel, free prescriptions and free university tuition. We have chosen to implement a person-centred social security system to invest in improved outcomes for the people of Scotland, provide vital assistance to enable older people to heat their homes and to help disabled people live independent lives. We have also invested to drive forward progress in eradicating child poverty, including through our Scottish Child Payment, devolved employability services and the supply of affordable homes.

We do, however, recognise the additional costs of this investment, as well as the additional cost of Scotland’s proportionately larger public sector workforce and comparatively higher public sector pay, as drivers of growth in the public spending over the medium-term horizon. This divergence in the growth in spending relative to the growth in funding, set out in Chapter 2, increases the challenge we face each year, from a balanced budget in 2025-26, to a gap of £2.6 billion in 2029-30, which is why we are setting out the actions in our sustainability delivery plan to mitigate this.

| (Nominal figures in £million) | 2025-26 | 2026-27 | 2027-28 | 2028-29 | 2029-30 |

|---|---|---|---|---|---|

| Resource spending | 52,623 | 54,938 | 57,132 | 59,453 | 61,723 |

| Resource funding (central scenario) | 52,623 | 53,975 | 55,235 | 57,100 | 59,099 |

| Resource Fiscal Gap | - | (963) | (1,897) | (2,353) | (2,624) |

The rest of this chapter examines the key drivers of the forecast growth in spending.

3.2 Resource spending outlook

Underpinning the pre-measures spending outlook presented in this chapter is the OBR forecast of inflation, consistent with the UK Spring Statement. Growth in public spending is usually measured against the GDP deflators published quarterly[33] by HM Treasury and we have assumed that, in general, public spending is constant in real terms, meaning it grows in line with the GDP deflators.

| (Figures in £million) | 2025-26 | 2026-27 | 2027-28 | 2028-29 | 2029-30 |

|---|---|---|---|---|---|

| Year-on-year growth | 2.65% | 1.66% | 2.04% | 1.95% | 1.88% |

Source: Office for Budget Responsibility Spring Forecast, March 2025

There are elements of the Scottish Budget where GDP deflators may not fully

capture the inflationary pressures experienced by the Scottish public sector, and where we expect greater pressure on public spending. These are set out below.

3.2.1 Pay

The Scottish Government is committed to delivering high-quality services across Scotland, and values investment in our public sector workforce. Spending on workforce pay across the devolved public sector in Scotland (including Local Government) is estimated to account for 55 per cent of the entire Scottish resource budget in 2025-26.[34]

The 2025‑26 Public Sector Pay Policy (PSPP), published in December 2024, set pay metrics that are fair, sustainable and realistic within a multi‑year pay envelope of 9 per cent over 2025‑26, 2026‑27 and 2027‑28. This was informed by an expected CPI inflation forecast of 6.9 per cent across the same period at the time of publication. There is flexibility for employers to configure three‑year proposals within the 9 per cent pay envelope, provided they have a fiscally sustainable approach.

In the absence of any policy measures on workforce, the total public sector paybill (including Local Government) is estimated to reach approximately £29 billion in 2025-26. The expected trajectory of this pre-policy paybill is set out in Table 3.03. Public sector pay is assumed to grow by 3 per cent in 2025-26, and 2.9 per cent per year in 2026-27 and 2027-28, to remain within the overall 9 per cent multi-year envelope, except for workforces where pay deals have already been agreed.[35] Thereafter, pay is assumed to grow in line with CPI inflation of 2.0 per cent while workforce growth is assumed to be flat over the five-year period.

| (Figures in £million) | 2024-25 | 2025-26 | 2026-27 | 2027-28 | 2028-29 | 2029-30 |

|---|---|---|---|---|---|---|

| Pre-policy baseline | 27,449 | 28,952 | 29,887 | 30,754 | 31,396 | 32,036 |

Source: Scottish Government

To quantify the scale of the fiscal risk associated with pay deals settling above the pay metric, an alternative scenario shows pay growth at 4 per cent per annum for the first three years, returning to 2 per cent pay growth from 2028-29 onwards.

This scenario, set out in Table 3.04, excludes Health workforces, as the MTFS resource spending trajectory uses a separate spending growth assumption for total Health and Social spending (see Section 3.2.3 below).

| (Figures in £million) | 2024-25 | 2025-26 | 2026-27 | 2027-28 | 2028-29 | 2029-30 |

|---|---|---|---|---|---|---|

| 4% pay growth per year | - | 132 | 314 | 524 | 554 | 566 |

Source: Scottish Government

Note: Where emerging pay deals have been agreed as of 13 June 2025, no adjustment to the illustrative scenarios has been applied as these are already included in the pre-policy baseline.

Multi-year pay deals provide certainty for the public sector workforce and an opportunity for the Scottish Government, employers and Trade Unions to plan for and transform our public services to improve outcomes for the people of Scotland. As of 13 June 2025, not all workforces within the devolved public sector have agreed pay deals for 2025 to 2026 or beyond. Where pay deals have been agreed, costs are estimated to be around £122 million higher, compared to the costs expected under the Public Sector Pay Policy published in December 2024.

Box 3.01: Inflation protection clauses in public sector pay deals

There are currently three pay awards, as of 13 June 2025, that include inflation protection clauses. Both NHS Agenda for Change (AfC) and Scottish Prison Service (SPS) have agreed a two year pay award with 4.25 per cent in 2025-26 followed by 3.75 per cent in 2026-27. It includes an Inflation Guarantee which states that the pay deal will be 1 percentage point higher than annual average CPI inflation. For 2025-26, the Inflation Guarantee will be triggered if average inflation over 2025 exceeds 3.25 per cent.

The OBR’s March 2025 CPI inflation forecast is 3.2 per cent for 2025-26, dropping below the Bank of England’s 2 per cent inflation target from 2026-27.[36] The Bank of England also forecast inflation at 3.25 per cent in 2025-26 but with a slower return to the target.[37] As a general measure, and everything else being equal, every 0.1 percentage point increase in the pay award would cost an extra £9 million for AfC and £0.3 million for SPS in 2025-26.

ScotRail and Caledonian Sleeper have accepted a two-year pay award with 3.6 per cent in first year followed by 3 per cent in second year. This includes Retail Price Index (RPI) inflation protection for year two where the pay deal will be either 3 per cent or January 2026 RPI, whichever is higher. As a general measure, and everything else being equal, every 0.1 percentage point increase in the pay award for Scotrail, over and above the current pay offer, would cost an extra £0.4 million in 2026-27.

Inflation outlook and risks

If CPI inflation continues in line with current forecasts[38], there would be no additional costs associated with the inflation guarantee for AfC and SPS. However, inflation protection clauses carry some financial risk. The outlook for inflation remains highly uncertain, with both upside and downside risks driven by factors such as global energy prices, domestic wage pressures, the broader economic environment and ongoing global trade tensions.

3.2.2 Workforce

The devolved public sector full-time equivalent workforce (FTE) stood at 469,100 FTE in March 2025, and 550,000 by headcount. While it has grown by around 1.8 per cent per annum, on average, over the last five years, there has been a marked slowdown over the past year (March 2024 to March 2025) where the total workforce number was broadly flat on an FTE basis.

Scotland’s public sector is proportionately larger and better paid when compared to the rest of the UK. The larger size of the workforce is both in terms of the share of the economy and share of total employment. As the Scottish Government’s budget is primarily dictated by the levels of spending in the rest of the UK and with proportionately more public sector workers in Scotland, as well as higher pay for public sector workers in Scotland on average, this places a structural pressure on our budgets.

As set out above in Table 3.03, the pre-policy baseline assumes that growth in the devolved public sector workforce has now plateaued and will continue to be broadly flat. As a general measure, and everything else being equal, a 1 per cent reduction in the workforce results in around £160 million of savings in the first year and recurring savings of around £300 million in subsequent years once fully achieved.

To quantify the potential costs or savings from faster, or slower workforce growth, two alternative scenarios are illustrated in Table 3.05. It shows the fiscal impact of the workforce declining or increasing by 1 per cent per year respectively over the next five years while pay award assumptions are unchanged from the pre-policy baseline.

| (Figures in £million) | 2024-25 | 2025-26 | 2026-27 | 2027-28 | 2028-29 | 2029-30 |

|---|---|---|---|---|---|---|

| Workforce reduces by 1% per annum | - | (157) | (459) | (775) | (1,098) | (1,429) |

| Workforce grows by 1% per annum | - | +157 | +463 | +788 | +1,127 | +1,481 |

Source: Scottish Government

We recognise the importance of being transparent around the data sources used to make decisions on the public sector workforce. Annex D contains a Pay and Workforce factsheet that sets out the main sources of data that are used, providing breakdowns by broad workforces.

3.2.3 Health and Social Care

Scotland is facing various population health challenges – our population is ageing, demand for health and social care services is rising and health inequalities are widening. In addition, the impacts of inflation, rising energy costs and Brexit mean that the finite funding is worth less in real terms but is expected to deliver more. NHS Boards have set ambitious recurring savings plans while seeking to manage ongoing operational and demand pressures. We have spending challenges in new medicines, procurement and in workforce pay.

In the 2023 MTFS, we forecast that Health and Social Care (HSC) spending would grow by 4 per cent in nominal terms each year. In reality, HSC spending has grown at a faster rate than this, averaging 5.6 per cent nominal growth over the last four years.[39] In their latest Fiscal Sustainability Report, the SFC projected an average of 3.3 per cent real growth in Health resource spending (between 5.0 per cent and 5.4 per cent nominal) for the first ten years of their period, from 2030 onwards.[40]

Consequently, we have updated our HSC spending forecast to reflect the observed growth in HSC spending in recent years and anticipated future costs. We forecast 3.3 per cent real-term average growth per annum. This represents higher growth in spending than the anticipated associated funding that the Scottish Government will receive from the UK Government. This is, however, before required savings and efficiencies, as set out in Chapter 4 and the Fiscal Sustainability Delivery Plan, are taken into account.

Box 3.02: Health & Social Care scenario analysis

We assume that Health and Social Care spending increases on average by 3.3 per cent real growth a year without intervening measures. As HSC constitutes almost 40 per cent of the Scottish Budget, our resource spending forecast is very sensitive to this assumption. If HSC spending was to grow by 1 per cent more or less than we assumed, it would have the following impact on the Scottish Government’s resource spending trajectory and fiscal position:

| (Figures in £million) | 2025-26 | 2026-27 | 2027-28 | 2028-29 | 2029-30 |

|---|---|---|---|---|---|

| Central resource forecast | 52,623 | 54,938 | 57,132 | 59,453 | 61,723 |

| HSC growth +1% | - | 225 | 477 | 757 | 1,065 |

| HSC growth -1% | - | (225) | (473) | (742) | (1,035) |

There are a range of factors that affect Health and Social Care spending in Scotland. Some of these, such as pay and demographics, have specific and more pronounced impacts on spending in Scotland than in the rest of the UK, due to a larger and better paid workforce in Scotland, and an older and sicker population. However, other factors such as increasing costs of prescriptions and medical supplies have similar impacts on Health and Social Care spending in the rest of the UK. Where this is the case, we would anticipate equivalent spending pressures in the UK which would result in funding for the Scottish Government of a proportionate amount.

3.2.4 Social Security

Social Security is an investment in the people of Scotland. The Scottish Government is building a modern Social Security system with dignity, fairness and respect at its heart, where people receive the support to which they are entitled. This investment is key to our national mission to eradicate child poverty and our commitment to help low-income families, support older people and unpaid carers, and enable disabled people to live full and independent lives.

The SFC’s June 2025 forecasts show overall expenditure on Social Security Assistance increasing from £6.8 billion in 2025-26 to £8.8 billion by 2029-30. This is mainly due to factors common across the UK such as the projected increasing demand for disability payments, increased cost of living, and rises in payment rates due to uprating. The increase in expenditure is also due to the success in benefit take-up, as well as new benefits only available in Scotland, such as the Scottish Child Payment and Two-Child Limit Payment from March 2026.

In addition to their headline social security forecast, the SFC have produced an illustrative costing of the recent change to the Pension Age Winter Heating Payment from Winter 2025-26. This costing, incorporated into our resource spending forecast, reflects the Scottish Government’s decision to mirror the UK Government’s extension to Winter Fuel Payment eligibility in Scotland.[41] The SFC estimate that these changes will add £53 million in 2025-26, increasing to £65 million per year by 2029-30, to their forecasts (increasing with inflationary uprating).

As part of the Social Security (Amendment) (Scotland) Act 2025, all Social Security Assistance delivered under the 2018 Act will be uprated in line with inflation. To maintain their value as prices rise in the economy, the Scottish Government uprated all Scottish Social Security payments by 1.7 per cent in April 2025, in line with the 12 months to September 2024 Consumer Price Index – a leading measure of inflation.

Disability benefits account for the majority of devolved Social Security Assistance (81 per cent in 2025-26). Eligibility for these benefits has historically been less sensitive to macroeconomic changes than for income replacement benefits, such as Universal Credit,[42] with demand for disability benefits tending to fluctuate more directly with changes in the “health of the nation”. However, in their December 2023 forecast the SFC highlighted that the higher demand for disability benefits observed across the UK was driven by factors such as the role of the cost of living crisis and the number of people with long-term health conditions. The same factors apply to the demand for Scottish disability benefits.

Table 3.07 presents the SFC’s forecast of the total additional investment in Social Security Assistance, which is funded from the Scottish Budget. The SFC include spending on Discretionary Housing Payments and Employability Services within their Social Security forecast, however, these are not part of the Social Security Assistance budget, so are not shown in our headline Social Security spending figures.[43]

| (Figures in £million) | 2025-26 | 2026-27 | 2027-28 | 2028-29 | 2029-30 |

|---|---|---|---|---|---|

| SFC June 2025 forecast of Social Security Assistance expenditure | 6,772 | 7,544 | 7,976 | 8,379 | 8,825 |

| Expenditure on social security payments with funding from BGAs | 6,132 | 6,730 | 7,129 | 7,505 | 7,928 |

| BGAs* | 5,725 | 6,191 | 6,440 | 6,680 | 7,001 |

| A: Difference (forecast benefits expenditure funded by BGAs minus BGAs) | 407 | 538 | 689 | 825 | 926 |

| B: Payments Unique to Scotland | 567 | 738 | 770 | 795 | 817 |

| C: Other Social Security payments** | 73 | 76 | 78 | 79 | 80 |

| Total additional investment (A+B+C) | 1,048 | 1,353 | 1,537 | 1,700 | 1,823 |

*Based on the UK Government Spring Statement, March 2025, and includes anticipated BGA funding of £120 million per annum from the UK Government’s Winter Fuel Payment policy change.

** These are payments that have replaced a corresponding UK Government payment and do not have a Social Security BGA, such as the Scottish Welfare Fund and Funeral Support Payment.

The additional investment in social security compared to England and Wales represents just over 3 per cent of the Scottish Government’s resource budget by 2029-30. This investment results from conscious policy choices made by Ministers and the Scottish Parliament, including a different approach to fast-tracking support for people with terminal illness and providing short-term assistance, a client-centred approach, and encouraging take-up of benefits.

Payments that are unique to Scotland, for which there are no UK equivalents, are forecast to total £817 million by 2029-30. Almost two-thirds of this delivers a Scottish Child Payment to low-income families with children, which modelling estimates will keep 40,000 children out of relative poverty in 2025-26. This is a significant public policy intervention, which is key to helping us substantially reduce levels of child poverty in Scotland and drive progress toward the 2030 targets.

As announced in the 2025-26 Scottish Budget, payments will also be made from March 2026 onwards to mitigate the impact of the UK Government’s two-child limit policy through the Two Child Limit Payment, at an estimated cost of £11 million in 2025-26 and rising to £194 million by 2029-30. However, recent media reporting suggests that the UK Government may make changes to the two-child limit policy in the Autumn Budget. Any resultant UK Government policy change may change the level of spending required through the Two Child Limit Payment.

Box 3.03: Social Security scenario analysis

We use the SFC’s forecasts for Social Security spending in the Scottish Budget and MTFS. These are, however, only forecasts and the Scottish Government must fund actual demand for these payments.

The SFC publish a Forecast Evaluation Report (FER) each Autumn, in which they evaluate how accurate their forecasts from previous years were compared to outturn. Table 3.08 shows the impact on forecast Social Security Assistance spending if we apply the SFC’s most recent forecast error.[44]

| 2025-26 | 2026-27 | 2027-28 | 2028-29 | 2029-30 | |

|---|---|---|---|---|---|

| SFC June 2025 forecast of Social Security Assistance | 6,772 | 7,544 | 7,976 | 8,379 | 8,825 |

| SFC forecast error, 1% cumulative error (FER 2024)[45] | - | +75 | +155 | +239 | +327 |

This forecast error is positive, meaning that the SFC underestimated spending on Social Security Assistance, largely due to higher than forecast demand for disability payments partly linked to UK-wide trends.[46] This analysis does not reflect the financial risk of policy changes and future forecast errors could be negative rather than positive.

3.2.5 Local Government

The Local Government scenario in the MTFS reflects forecast expenditure in relation to the funding made available to Local Government by the Scottish Government through the combination of the General Revenue Grant, including Specific Revenue Grants, and forecasts of income raised locally by Non-Domestic Rates. This reflects approximately 85 per cent of actual expenditure by Local Government, which is otherwise funded by service fees, charges and council tax.

The scenario assumes that Local Government is subject to similar spending pressures as the rest of the public sector. Our underlying forecast assumptions therefore reflect that the same demographic pressures experienced by health and social care apply to social care services delivered by Local Government. As a result, the illustrative modelling applies above inflation growth to social care non-pay spending, Public Sector Pay Policy to social care pay and real-terms growth to remaining Local Government spending.

3.2.6 Other above-inflation spending

As well as the main areas of above-inflation spending detailed earlier, we include some targeted above-inflation growth in specific spending commitments in the MTFS forecast. These include the 2025 Programme for Government commitment on peak rail fares, the Scottish Government’s concessionary travel policies, the costs of hosting Euro 2028 and the Scottish Parliament Elections in 2026. Including targeted growth on commitments such as these ensures that we are more fully capturing expected medium-term spending on specific commitments.

3.3 Capital spending outlook

Over the past couple of years our capital budget has faced significant challenges. The average cost of construction materials has increased by over 27 per cent when compared to pre-Covid levels. This was coupled with a 4.3 per cent real-term reduction in our UK capital Block Grant over the period 2022-23 to 2024-25. This reduction in our spending power has meant that we have had to change the delivery timescales for some of the projects and programmes within the 2021 Infrastructure Investment Plan (IIP) pipeline and has led to an increase in backlog maintenance that needs to be addressed in the upcoming years.

Despite the significant real-term cuts and the economic challenges, we have delivered many of the projects set out in the 2021 IIP pipeline including:

- Levenmouth Rail Project

- Reston and East Linton Rail Stations

- Barrhead Rail Enhancement

- A92/A96 Haudagain Junction Improvement, Aberdeen

- Inverness Airport Station

- Elective Orthopaedic Centre, Fife

- National Treatment Centre, Inverness

- North East Health and Social Care Hub, Glasgow

- Golden Jubilee Surgical Centre, Clydebank

- Oncology Enabling Projects, Edinburgh Cancer Centre

- National Facility for Women Offenders, Stirling

For the 2025-26 Scottish Budget, we received an increase to our Block Grant from the UK Government, however this only restored funding to 2023-24 levels in real terms and was insufficient to meet all our infrastructure investment needs. To boost this, the Scottish Government maximised capital borrowing and drew down over £300 million of ScotWind revenues to invest in activities that deliver on our net zero ambitions and have a long-lasting benefit for the people of Scotland.

This increase in funding means that we have met our National Infrastructure Mission (NIM) target to increase the budget for infrastructure investment to £6.86 billion in 2025-26. We will set out our long-term vision in the next Infrastructure Investment Plan which will include a refreshed target.

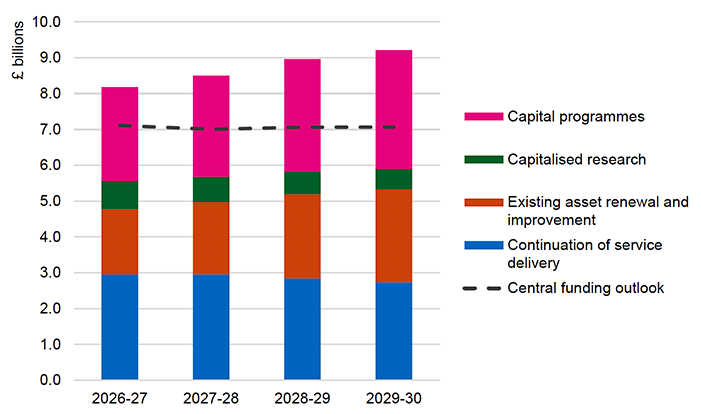

Looking ahead, the UKSR shows that our capital Block Grant is expected to remain broadly flat around £6.65 billion between 2026-27 and 2029-30 which will equate to a decrease by 1.1 per cent in real terms between 2025-26 and 2029-30. However, when accounting for the Scottish Government’s capital borrowing policy and the one-off nature of ScotWind revenues, our overall CDEL budget is forecast to fall by 9.3 per cent over the same period.

This further real-terms reduction is compounded by the real-term cuts in previous years and sustained high levels of inflation which reduced our spending power. As such our capital spending is forecast to exceed our available budget by £1.1 billion in 2026-27, rising to £2.1 billion in 2029-30 without further action. There are risks associated with these forecasts, for example, the significant public and private sector investment required to achieve a just transition to net zero.

Scottish Ministers plan to consult on a draft version of the next Climate Change Plan in Autumn 2025, once carbon budgets have been set in regulations by Parliament. Scottish Ministers welcome the UK Climate Change Committee’s (CCC) advice on how to stay within these limits, however, as they make clear, it is always for Scotland to decide whether those policies are right for Scotland. We recognise that the public and private sectors must work together to achieve our climate and biodiversity ambitions. The purpose of the next Climate Change Plan is to outline policies and proposals to deliver carbon budgets up to 2040. Information will be provided on the costs and benefits of the policies and this will be taken into account by Ministers in the Scottish Spending Review. Further detail is set out in the Spending Risks section.

Source: Scottish Government

| (Figures in £million) | 2025-26 | 2026-27 | 2027-28 | 2028-29 | 2029-30 |

|---|---|---|---|---|---|

| Central capital funding | 7,230 | 7,109 | 7,004 | 7,059 | 7,067 |

| Central capital spending | 7,230 | 8,180 | 8,501 | 8,962 | 9,213 |

| Capital Fiscal Gap | - | (1,070) | (1,497) | (1,903) | (2,146) |

Scotland invests its capital budget in several key areas. First, capital investment is required to maintain the existing public sector asset base to ensure the continued delivery of high-quality public services. For example, maintaining our road, rail and ferry networks and maintaining the asset base of our emergency services. Over the four years, current modelling assumes a slight reduction in this spending area, reflecting a reduction in International Financial Reporting Standard 16 (IFRS16) requirements and a change in maintenance requirements across the period as older assets are replaced.[47]

Second, some assets require improvement or replacement to ensure they remain fit for purpose, for example HMP Glasgow is replacing HMP Barlinnie. This increase over the period reflects the Scottish Government’s ambitions to remove the backlog of maintenance facing the public sector estate, replace our ageing assets, for example Monklands Hospital, and deliver several major improvement projects, such as dualling the A9.

Capitalised research supports Research & Development across a number of sectors, including funding for higher education grants to support world leading research in Scottish universities.

Finally, Scotland has several major programmes of capital investment, including in Affordable Housing, Heat in Buildings and supporting Local Government through their General Capital Grant. The increasing spending outlook over the period reflects the Scottish Government’s ambitions across a number of policy areas.

Alongside our capital Block Grant, Scotland receives a Financial Transactions allocation from the UK Government, which we invest in various schemes, including supporting the Scottish National Investment Bank. Between 2022-23 and 2025-26, our FTs allocation has decreased significantly to just £167 million. The UKSR has given us clarity over future years FTs allocations and an increase up to 2029-30. However, this is not enough to compensate for the lack of growth in the block CDEL grant.

Following the UK Government publishing their Spending Review, we have clarity over our future capital and FTs funding envelopes for the next four years and we will undertake a review of all capital spending to reprioritise our programme of work. The Cabinet Secretary of Finance and Local Government intends to publish an infrastructure investment pipeline in December 2025, alongside the 2026-27 Scottish Budget and the Scottish Spending Review. This will provide clarity over the projects and programmes which will be prioritised over the medium term and where commitments will be paused, delayed or rescoped.

Given the fiscal challenges, and particularly the capital funding settlement from the UK Government, we are currently exploring the use of revenue finance models to bring additionality to our capital funding envelope to deliver the infrastructure needed across the country. We will ensure any investment remains affordable for both the resource and capital budgets and that they represent good value for money. We will set out more options at the Scottish Spending Review about projects that could be funded through revenue financed investment.

In our constrained fiscal environment, it is also important that the private sector plays a role in supporting infrastructure investment, particularly in areas such as housing (through the Housing Investment Taskforce for example) and offshore wind. We continue to work with private investors to support investment into Scotland’s infrastructure as we look to deliver effective public services from assets that are fit for purpose.

The Scottish Government remains committed to infrastructure investment as a key lever in securing economic growth, tackling the climate crisis, and delivering high-quality public infrastructure across Scotland. As such, we are doing all we can to maximise the impact of our capital investment towards spend that delivers on the outcomes of this government.

3.4 Spending risks

In addition to the main drivers of spend discussed above, there are a number of potential spending risks that the Scottish Government has to consider when analysing medium-term spending plans and the fiscal sustainability of these. On resource spending, pressures resulting from demand-led spending and demographic changes are the main sources of uncertainty. For the first time we are also presenting information on the Scottish Government’s contingent liabilities and present a fuller picture of the spending risks over the medium term.

As set out in the capital spending section, the real-terms reduction to our capital funding in previous years, coupled with high inflation, has resulted in delays to several infrastructure projects and an increase in backlog maintenance. These pressures are exacerbated by new or more complex commitments, alongside the significant investment required to adapt to the changing climate and achieve our emissions reduction targets.

3.4.1 Demand-led spending

Demand-led expenditure appears across the public sector and will always carry a degree of forecast risk. Budgets reflect expected levels of demand. Actual expenditure depends on the eligible population choosing to use the service and is affected by behavioural and economic factors. Areas where we experience volatility include for example social security benefits, concessionary travel and legal aid.

This has become a more significant feature of the Scottish Budget since the devolution of Social Security, which is now the third largest area of public spending in Scotland, after Health and Local Government. Under the Fiscal Framework, all demand-led policies must be managed within the resource budget available and the limited fiscal levers available to the Scottish Government.

For example, expenditure on Social Security benefits is determined by the number of eligible people who apply for support, all of whom must be paid at the rate set in legislation. This is undertaken in accordance with the principle that social security is an investment in the people of Scotland, set out in the 2018 Social Security Act.

Budget allocations are based on independent forecasts, but the Scottish Government must meet social security expenditure as it arises, even if it differs from forecasts used to set the initial medium-term spending plans or the Budget. This can result in the Scottish Government spending more or less than expected at the time the budget is set.

There is uncertainty in the related BGAs, which relate to Social Security policy as it exists in the rest of the UK. Changes in either UK Government policy relating to devolved benefits, or the OBR's forecasts of benefit demand in the rest of the UK, can affect the funding that the Scottish Government is expected to receive in either direction, and the impact of social security spending on wider spending priorities.

As set out in Chapter 2, existing borrowing and reserve powers can help manage in-year forecasting risk for social security and tax, however, these powers are limited and as demonstrated in the position for 2027-28, the scale of adverse movements can exceed the applicable annual limits for any one year.

3.4.2 Climate change and biodiversity

Delivering a just transition to net zero, and restoring and regenerating biodiversity will require sustained action from all sectors of society, and significant revenue spending and capital investment from governments.

Given the scale of these costs and the investment barriers faced, it is clear that public sector spending alone will not be sufficient. The public and private sectors must work together to achieve our climate and biodiversity ambitions. New and innovative investment models are needed to enable public and private finance to combine (blended finance) to achieve long-term value for our communities and environment. These models are already being developed in a number of areas, for example to support private investment in natural capital for peatland restoration and woodland creation.

Climate change places greater pressure on our public spending in three ways: mitigation costs to reduce greenhouse gas emissions and limit further global warming; adaptation costs to reduce climate impacts; and the cost of damages from severe weather events.[48]

One key risk is that funding for the Scottish Government will largely depend on UK Government policy decisions, including whether the response to climate change in some areas involves greater use of spending or non-spending levers, and how the costs of the net zero transition are ultimately split between the private and public sectors.

Additionally, the fiscal risk is not distributed evenly across the UK. In their report on Climate Change (March 2024)[49], the SFC concluded the expected level of per capita public investment required for net zero is higher in Scotland than the rest of the UK, largely as a result of the disproportionate investment required in woodland creation and peatland restoration.

The costs of mitigation are significant. The Climate Change Committee published advice on Scotland’s Carbon Budgets in May 2025[50]. The cost profile of the Balanced Pathway over the period 2025 to 2045, shows an average net cost of £1.4 billion per year, which comprises an average investment cost of £3 billion per year and an average operating cost saving of £1.6 billion per year. The CCC advise that delaying this investment in decarbonisation will delay the benefits, including operating cost savings, improved resilience, and energy security.

As with mitigation, early investment in adaptation can bring greater benefits. Evidence suggests that investing in preventative adaptation can generate savings in the long term, when compared to the costs of recovering from climate damages, with a cost-benefit ratio in the region of £2-10. The Scottish National Adaptation Plan[51] outlines actions to build resilience to climate impacts over the period to 2029.

3.4.3 Demographic change

Scotland’s population is ageing. The recent SFC Fiscal Sustainability Report[52] projects the median age of the Scottish population to increase from 43 in 2029-30 to 49 by 2074-75, with a growing share of the population expected to be over the age of 65. The ageing of the Scottish population is also forecast to happen earlier than the rest of the UK which creates funding and spending risks which will need to be managed.

The Scottish share of the UK population aged 75 and over peaks in the 2030s, and Scotland’s share of people aged 85 and over rises from 7.6 per cent in 2029-30 to 8.3 per cent in 2049-50. The SFC notes that this poses a relative risk to the sustainability of the public finances as health-related expenditure rises, but faster than the related additional funding we may receive from similar increases in age-related health spend in the rest of the UK via the Block Grant.

Over the longer term, the SFC project this trend may reverse, and the Scottish population over the age of 65 as a share of the UK population will actually decrease – meaning we may receive relatively more funding from age-related healthcare spend in the rest of the UK than we have to spend in Scotland – acting as an upside risk to the sustainability of the public finances.

The recent SFC report focuses on population health and the impact on health spending and the future gap between funding and spending. It sets out scenarios based on improved overall population health and worsened health, noting that improved health would have a positive effect on the public finances. The Scottish Government’s recently published Population Health Framework sets out the Government’s plan to improve the overall health of the Scottish population. This sits alongside the longer-term plans for the future of the NHS which are discussed in more detail in Chapter 4.

3.4.4 Contingent liabilities

The Scottish Government’s potential exposure to contingent liabilities has increased over recent years and will continue to do so in the coming years. This is mainly driven by an increase in the exposure to decommissioning projects. This is where the Scottish Government acts as funder of last resort in the event that offshore wind developers are unable to meet their decommissioning obligations at the end of a site’s operational period and all other mitigations such as security packages have been exhausted.

Contingent liabilities are financial obligations that the government may face if certain future events were to happen. The Scottish Government’s contingent liabilities can be split into two categories – those that arise unavoidably out of the ordinary functions of government, for example, commitments to fund pension deficits, or legal claims; and those arising from discretionary policy decisions, such as decommissioning with the policy aim of stimulating the development of the provision of clean energy from offshore wind. The Scottish Parliament is required to approve any proposals for contingent liabilities that relate to discretionary policy decisions over £2.5 million and the Scottish Government must notify the Parliament of any between £300,000 and £2.5 million.

The Scottish Government’s annual accounts provide further detail on a number of our contingent liabilities, including their gross exposure, which represents a worst-case scenario if the contingent liability was called in full. In reality, very few contingent liabilities present a significant exposure once the risk of crystallisation and available mitigations and security packages are taken into account (known as net exposure).

The Scottish Government has robust processes in place to monitor and manage our contingent liabilities within the parameters of in-year financial management and annual budget setting processes. In addition, contingent liabilities are reviewed in-year and as part of the year-end accounts process.

Whilst we consider that the risks are manageable within the current controls, we are looking to strengthen these processes with the establishment of the contingent liabilities group, and we are developing our approach to assess net exposure so that we can more closely monitor potential risks going forward. There are also a range of actions available to mitigate our exposure such as ensuring a diverse range of contingent liabilities across different sectors and developers, and calling on security packages. We deem it unlikely that the whole portfolio of contingent liabilities would crystallise at one time, and financial exposure in the event of any crystallisation may be spread over a number of financial years.

3.4.5 Ageing assets

Infrastructure underpins the public services that the Government delivers. Higher construction costs in a constrained funding environment means that fewer new investments are affordable, and maintenance budgets are under strain. The asset base of the Scottish public sector is ageing and without adequate maintenance and renewal there is a risk that public services are becoming less accessible and available. Strategic prioritisation of capital allocations and the infrastructure pipeline is required to ensure that the public asset base is fiscally sustainable and makes service delivery resilient to changing demand and delivery risks.

3.4.6 Management of unanticipated risks

There are a range of risks which cannot be anticipated with any certainty, but which must be managed should they arise. These include epidemics, financial crises, adverse weather impacting people and infrastructure, and geopolitical conflict. The extent to which these events impact the Scottish Budget depends on relative impacts to the wider UK. The SFC report on Climate Change noted the increasing risk of climate change damage could make the Scottish Budget more vulnerable to volatility and create pressures on spending that require reprioritisation of commitments within the financial year[53].

We have seen increasing instances of unanticipated events in recent years and the Scottish Government must be prepared to take action where there is an impact on Scotland. Responding to these risks creates challenges for in-year financial management when additional spending, which was not budgeted for, is required. The additional costs must be met through in-year savings from elsewhere in the budget. The Scottish Government has robust in-year financial management practices in place to manage in-year risks should they occur, and to ensure that Parliament and the public are kept up to date with any changes to the public finances. The Scottish Government reviews expenditure including on workforce, in line with spend controls with accountable officers assessing this against overall budgets.

The Budget Act is typically amended twice a year through a Scottish Statutory Instrument (SSI), known as the Autumn and Spring Budget Revisions. These budget revisions allocate any additional funding and reflect spending patterns emerging from monthly budget monitoring. This is part of the usual process to support financial scrutiny and to allow the Scottish Parliament to authorise any changes to the Budget Act. The Scottish Government publishes a provisional and final outturn statement each year. This sets out the changes between the published budget and actual spending. The latest Outturn Report was published on 24 June 2025.

Contact

Email: Scottish.Budget@gov.scot