Scotland's fiscal outlook: medium-term financial strategy

This is the seventh Medium-Term Financial Strategy published by the Scottish Government. It provides the economic and fiscal context for the Scottish Budget and sets the medium-term strategy for sustainable public finances.

Chapter 1: Scotland’s Economic Outlook

This chapter provides an update on the state of the Scottish economy, incorporating the latest economic forecasts from the SFC and the Office for Budget Responsibility. There is a focus on Scotland’s economic performance and how this impacts the fiscal outlook, as the Scottish Government’s funding outlook is in part determined by how relative tax revenues in Scotland and the rest of the UK are forecast to perform.

1.1 Economic context

There has been a marked rise in global macroeconomic and geopolitical uncertainty in 2025, in particular due to a range of tariff announcements from the United States this Spring, many of which have since been paused or amended. Rising energy prices, inflation, and growing geopolitical instability contribute to an uncertain outlook.

Despite these challenges there have been encouraging signs for Scotland’s economy at the start of 2025, with Scottish Gross Domestic Product (GDP) growing 0.4 per cent in the first quarter of 2025, picking up from 0.1 per cent growth in the final quarter of 2024, buoyed in particular by the Services and Production sectors[12].

More recent business survey data has indicated a slight improvement in business activity going into the second quarter of 2025. The Royal Bank of Scotland Growth Tracker[13] reported that business activity in May increased for the first time in six months, although indicators for new business orders remained slightly negative. Furthermore, weakening demand remains a key concern for business and the recent fall in consumer sentiment[14] in April to its lowest level in two years underlines this risk.

After falling last year, inflation has increased at the start of 2025 following increases in regulated prices as well as impacts from employer National Insurance Contributions, and was 3.4 per cent in May[15]. However, the Bank of England has gradually reduced interest rates from their peak of 5.25 per cent last year to 4.25 per cent in May, although uncertainty remains about the outlook for inflation and interest rates, with ongoing global trade disputes and uncertainty over the persistence of domestic prices pressures.

Despite this, the Scottish labour market remains robust with unemployment at 4.2 per cent[16] and earnings continuing to grow faster than inflation, although the number of payrolled employees fell slightly over the past year[17]. This correlates with evidence of weaker labour demand from business survey data in recent months, although the latest data does indicate a broader stabilisation in this measure.

1.2 Latest economic forecasts for Scotland

Our analysis is underpinned by the latest forecasts from the SFC[18].

The SFC has downgraded its short-term outlook for the Scottish economy, forecasting 1.2 per cent growth in 2025-26, down from 1.6 per cent forecast in December 2024. This reflects poorer than expected economic data in the second half of 2024 when Scottish economic growth stalled (0.1 per cent in the fourth quarter, down from 0.3 per cent in the third quarter).

Despite a weaker outlook for growth in the short term, the medium-term outlook has slightly improved with the SFC incorporating new population data published by the Office for National Statistics (ONS). The size of the population in Scotland was revised upwards, and consequently the overall size of the economy as well.

Table 1.01: Key economic indicators from the latest SFC and OBR forecasts

| % | 2024-25 | 2025-26 | 2026-27 | 2027-28 | 2028-29 | 2029-30 | 2030-31 |

|---|---|---|---|---|---|---|---|

| SFC - May 2025 | 1.2 | 1.2 | 1.8 | 1.7 | 1.6 | 1.6 | 1.6 |

| OBR - Mar 2025 | 1.0 | 1.2 | 1.9 | 1.7 | 1.7 | 1.8 | - |

| % | 2024-25 | 2025-26 | 2026-27 | 2027-28 | 2028-29 | 2029-30 | 2030-31 |

|---|---|---|---|---|---|---|---|

| SFC – May 2025 | 0.5 | 0.6 | 1.3 | 1.3 | 1.3 | 1.4 | 1.4 |

| OBR – Mar 2025 | 0.0 | 0.7 | 1.5 | 1.4 | 1.3 | 1.4 | - |

| % | 2024-25 | 2025-26 | 2026-27 | 2027-28 | 2028-29 | 2029-30 | 2030-31 |

|---|---|---|---|---|---|---|---|

| SFC - May 2025 | 0.2 | 0.1 | 0.6 | 0.5 | 0.4 | 0.4 | 0.4 |

| OBR - Mar 2025 | 1.2 | 0.8 | 0.6 | 0.7 | 0.6 | 0.7 | - |

| % | 2024-25 | 2025-26 | 2026-27 | 2027-28 | 2028-29 | 2029-30 | 2030-31 |

|---|---|---|---|---|---|---|---|

| SFC - May 2025 | 4.5 | 3.7 | 2.9 | 3.0 | 2.9 | 3.0 | 3.0 |

| OBR - Mar 2025 | 4.7 | 3.7 | 2.2 | 2.1 | 2.3 | 2.5 | - |

| % | 2024-25 | 2025-26 | 2026-27 | 2027-28 | 2028-29 | 2029-30 | 2030-31 |

|---|---|---|---|---|---|---|---|

| CPI* Rate (%)** | 2.3 | 3.2 | 1.9 | 2.0 | 2.0 | 2.0 | - |

| Interest Rate (%)** | 4.9 | 4.0 | 3.8 | 3.8 | 3.8 | 3.8 | - |

* Consumer Price Index (CPI)

**The SFC aligns its inflation and monetary policy outlook to that of the OBR

Source: Office for Budget Responsibility (OBR); Scottish Fiscal Commission (SFC)

The SFC’s economy assumptions are aligned with the Office for Budget Responsibility’s central forecast. This includes the economic impact of the increased trade policy uncertainty in the run-up to January 2025, without directly adjusting for any specific tariffs introduced since January. Similarly to the OBR, the SFC have used scenario analysis to highlight the impact of increasing trade tariffs as a potential downside risk to their economic outlook.

The latest inflation forecast for 2025-26 is now 0.6 percentage points higher than previously forecast at the time of the UK Budget in October 2024. Business and consumer confidence has weakened, and increased geopolitical tensions on global trade restrictions are viewed as key short-term risks.

The SFC continue to be more optimistic than the OBR on the medium-term outlook for nominal and real earnings growth, with the SFC forecasting annual growth around 0.7 percentage points higher on average over 2026-27 to 2029-30 than the OBR. However, there is now no difference between the forecasters’ judgements for 2025-26 with the OBR upgrading their earnings outlook. This in part reflects that there is now less evidence that the labour market in Scotland is slightly stronger than the rest of the UK.

1.3 Fiscal implications of the economic outlook

Since the devolution of further tax and social security powers in 2016, the Scottish Government’s funding is more closely linked to the economy through the performance of the Scottish tax base. In particular, the Scottish Budget is affected by relative tax performance in Scotland compared to the rest of the UK.

The outlook for earnings

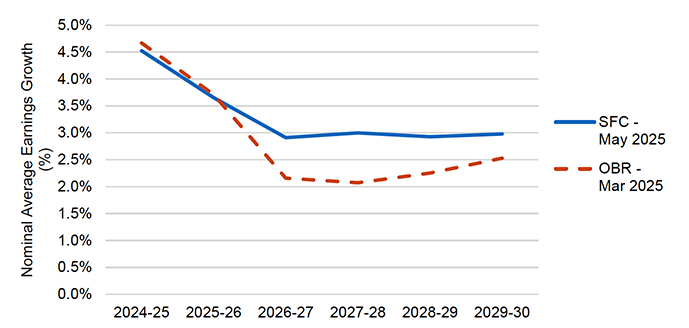

Earnings are a key factor in shaping the funding outlook for the Scottish Government, as they help determine future levels of Income Tax receipts. The latest forecasts from the SFC and OBR show a sustained gap in nominal average earnings growth between Scotland and the rest of the UK over the medium term, as can be seen in Figure 1.01 below. Both the OBR and SFC are forecasting similar earnings growth in 2025-26, but the SFC forecasts higher growth from 2026-27 onwards.

Source: Office for Budget Responsibility (OBR); Scottish Fiscal Commission (SFC)

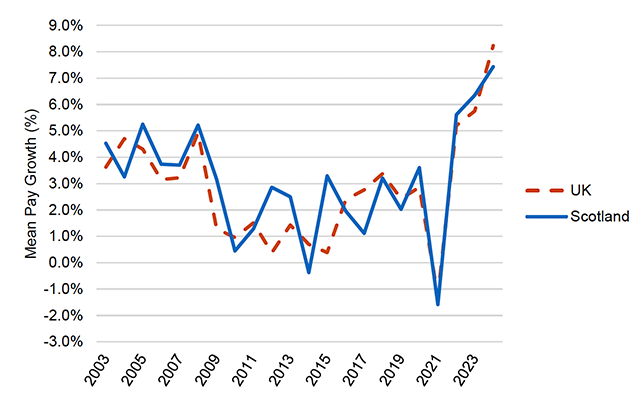

As shown in Figure 1.02 below, such a sustained divergence in earnings growth would be unusual, and the SFC have flagged that this means that it is more likely than not that the net tax position will be weaker than projected.

Source: Annual Survey of Hours and Earnings

Tariffs

As noted earlier, the SFC’s economy assumptions are aligned with the OBR’s central forecast, which includes the economic impact of the increased trade policy uncertainty in the run-up to January 2025 without directly adjusting for any specific tariffs introduced since January. In a similar approach to the OBR, the SFC have produced a separate piece of scenario analysis to examine the potential effects of tariffs on the Scottish economy[19].

The results show that the level of Scottish GDP could be around 0.4 per cent lower than their central forecast in 2025-26, 0.6 per cent lower in 2026-27 and around 0.3 per cent lower towards the end of their forecast horizon and are broadly similar in magnitude to the OBR’s own comparable scenario analysis.

Although the SFC flags the impact of tariffs as a potential downside risk to their forecasts in isolation, the SFC also show there is currently no strong evidence that there could be an asymmetric impact on Scotland relative to the rest of the UK. Consequently, as long as the economic impact of tariffs is broadly similar in magnitude for both Scotland and the rest of the UK, the current Fiscal Framework will help mitigate this risk to the long-term funding outlook.

Contact

Email: Scottish.Budget@gov.scot