Scotland's fiscal outlook: medium-term financial strategy

This is the seventh Medium-Term Financial Strategy published by the Scottish Government. It provides the economic and fiscal context for the Scottish Budget and sets the medium-term strategy for sustainable public finances.

Chapter 2: Scotland’s Funding Outlook

2.1 How Scotland’s funding outlook is determined

This chapter outlines the Scottish Government's central funding outlook over five years from 2025-26 to 2029-30. It sets out the policy decisions and assumptions that underpin this, and how the outlook has changed compared to the last MTFS in 2023.

The Scottish Government's funding outlook is affected by decisions by both the UK and Scottish Governments, as well as Scotland's economic performance relative to the rest of the UK. The projections combine independent forecasts of tax and spending provided by the SFC and OBR, alongside forecasting judgements and policy decisions made by the Scottish Government.

The Block Grant forecast presented incorporates the outcome of the UK Government’s Spending Review on 11 June 2025. While this increases the level of certainty in the funding outlook, other drivers of uncertainty remain. Therefore, the chapter also includes potential alternative scenarios, setting out a more optimistic and pessimistic outlook.

2.2 Summary of Scotland’s funding outlook

The Scottish Government's funding outlook is comprised of five high-level categories, each of which is discussed in detail in this chapter:

- The Block Grant is the single largest source of funding for the Scottish Government. The Barnett formula determines the Block Grant received from the UK Government. Annual growth is dependent on the UK Government's overall fiscal plans and spending priorities.

- Devolved taxes provide revenue to the Scottish Government, the largest of which is Scottish Income Tax. The Scottish Budget is then reduced based on how quickly revenues of the corresponding tax have grown in the rest of the UK on a per person basis.

- Non-Domestic Rates (NDR) are revenue raised by Local Authorities on non-domestic properties. All revenue raised is ultimately returned to Local Government via the Local Government Finance Settlement.

- Social Security Block Grant Adjustments (BGAs) is funding provided by the UK Government for devolved social security payments and is grown in line with how expenditure on comparable social security benefits grows per person in the rest of the UK.

- Other income and expenses covers revenue and costs including resource borrowing and associated costs, and Crown Estate Scotland revenues.

The Scottish Government’s central funding outlook forecasts total funding to grow by an average of 2.6 per cent a year in nominal terms over the period 2025-26 to 2029-30, 0.7 per cent a year in real terms. Table 2.01 shows the central funding outlook covering both resource and capital funding.

Resource funding is expected to grow by an average of 2.9 per cent in nominal terms, or 1.0 per cent in real terms, a year to 2029-30. Within this, the Block Grant is expected to grow by an average of 0.8 per cent a year in real terms. The Block Grant accounts for the majority of the increase in the total resource funding, followed by increases in the net tax position and Social Security BGAs.

Total capital funding, including FTs, is expected to remain broadly constant in nominal terms and fall by 1.8 per cent a year in real terms over this period. Within this the capital Block Grant is set to fall in real terms, while FTs are set to increase in both nominal and real terms.

| Resource Funding | 2025-26 | 2026-27 | 2027-28 | 2028-29 | 2029-30 |

|---|---|---|---|---|---|

| Block Grant | 41,622 | 42,714 | 43,840 | 45,018 | 46,215 |

| Net tax position | 1,207 | 1,361 | 1,762 | 2,067 | 2,314 |

| Of which: | |||||

| Devolved tax revenue | 21,544 | 23,019 | 24,301 | 25,398 | 26,554 |

| Tax Block Grant Adjustment | (20,336) | (21,657) | (22,540) | (23,331) | (24,239) |

| Non-domestic rates distributable amount | 3,114 | 3,549 | 3,480 | 3,534 | 3,861 |

| Social Security Block Grant Adjustment* | 5,725 | 6,191 | 6,440 | 6,680 | 7,001 |

| Non-tax income & Block Grant Adjustments | (4) | (4) | (4) | (4) | (4) |

| Other income/expenses | 959 | 163 | (283) | (195) | (288) |

| Total resource funding, incl. NDR | 52,623 | 53,975 | 55,235 | 57,100 | 59,099 |

| Capital Funding | 2025-26 | 2026-27 | 2027-28 | 2028-29 | 2029-30 |

|---|---|---|---|---|---|

| Total Capital Block Grant | 6,256 | 6,689 | 6,595 | 6,640 | 6,665 |

| Ringfenced funding and City Deals | 122 | 120 | 110 | 119 | 102 |

| Capital borrowing and other funding per policy | 472 | 300 | 300 | 300 | 300 |

| ScotWind | 341 | - | - | - | - |

| Other | 40 | - | - | - | - |

| Total capital funding (excl. FTs) | 7,230 | 7,109 | 7,004 | 7,059 | 7,067 |

| Financial Transactions (incl. reserve) | 192 | 245 | 252 | 311 | 361 |

| Total Capital Funding (incl. FTs) | 7,422 | 7,354 | 7,256 | 7,370 | 7,429 |

| Total funding from all sources | 60,045 | 61,329 | 62,491 | 64,470 | 66,528 |

*Of which around £120 million each year is anticipated increase in funding from the UK Government Winter Fuel Payment policy change. Updated OBR forecasts alongside the UK Government autumn fiscal event will confirm the forecast funding impact.

It is useful to compare the current multi-year outlook with the one presented in the previous MTFS (May 2023) and the 2025-26 Scottish Budget.

Table A.01(a) (Annex A) shows the change in the outlook compared to the figures presented in the previous MTFS publication. The change is presented for the years where forecasts overlap between the two publications.

The funding outlook has improved substantially in nominal terms since the previous MTFS, by an average of £6.0 billion over the three years. This increase is mostly driven by an improvement in resource funding and mainly reflects changes in UK Government spending, announced at fiscal events over the last two years.

For example, the UK Autumn Budget (October 2024) increased the Block Grant by £1.4 billion in 2024-25 and by £1.5 billion in 2025-26,[20] and there was a further £28 million increase to the core resource and capital Block Grants at the UK Spring Statement on 26 March 2025 and an additional £117 million in non-recurring resource consequentials at the 2025-26 Main Estimates. The 2025 UKSR confirmed the multi-year UK Government funding, which again changed the forecast resource and capital position.

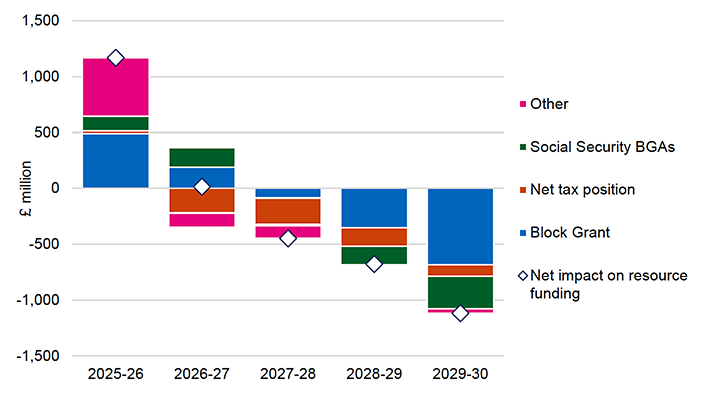

Figure 2.01 and Table A.01(b) (Annex A) compare the current funding outlook to the one presented in the 2025-26 Scottish Budget.[21] The comparison with the forecasts included in the most recent Budget reflects changes announced in the UK Spring Statement, at the 2025-26 Main Estimates and the UK 2025 Spending Review, as well as changes in the SFC and OBR forecasts and the Scottish Government’s own provisional outturn figures for 2024-25.

Source: Scottish Government

The position set out in the 2025-26 Scottish Budget was based on the SFC forecasts available at the time and on forecast Block Grant settlements. In the absence of further information, the Barnett-based funding was assumed to grow broadly in line with the OBR’s forecast for the total UK Resource Departmental Expenditure Limit (RDEL) and Capital Departmental Expenditure Limit (CDEL) envelopes. However, the 2025 UKSR has since confirmed a lower Block Grant as illustrated by the blue bars in the figure above.

The total funding position is now forecast to improve in the short term (by £1.2 billion in 2025-26) but worsen over the medium term (by £1.2 billion in 2029-30) relative to projections set out in December 2024.

The short-term increase is largely explained by the higher amount of RDEL carried forward through the Reserve (included in category ‘Other’ in Figure 2.01) and higher Block Grant compared to the December 2024 position. The increase in the Block Grant in part reflects Barnett consequentials relating to employer National Insurance Contributions (NICs) which were not confirmed until the 2025 Main Estimate.

The medium-term impact is largely driven by the confirmed UKSR Block Grant settlement being lower than had been expected (£685 million lower by 2029-30). In addition, UK Government policy on disability benefits announced in the Spring Statement, as well as other factors, led to lower Social Security BGAs (£408 million lower by 2029-30). However, HM Treasury indicated to the Scottish Government that the UK Government’s decision to expand eligibility for the Winter Fuel Payment (announced in June) is likely to increase the corresponding BGA by around £120 million in 2029-30, partially offsetting the overall reduction compared to the December 2024 funding position. Furthermore, the net tax position has been revised downwards (£102 million lower by 2029-30), following updated forecasts from the OBR and SFC. These changes are discussed in more detail in the individual sections later in this chapter.

2.2.1 Resource Block Grant

The Block Grant is the main component of the Scottish Government’s funding. The UK Government’s spending decisions fully shape the size of the Block Grant. The Block Grant comprises the baseline Block Grant established through a Spending Review and the ‘Barnett consequentials’ flowing from any changed spending decisions set out at subsequent UK Government fiscal events, using the Barnett formula. It is also impacted by Block Grant Adjustments (BGAs) which involve changes to funding that reflect the devolution of some tax and social security powers to Scotland. The baseline Block Grant and subsequent Barnett consequentials reflect a population share of changes in comparable spending in devolved areas in the rest of the UK, and the level of BGAs is tied to UK policy decisions affecting taxes and benefits that are devolved in Scotland.

The 2024 UK Autumn Budget set out the overall departmental spending for 2025-26 to 2029-30. These plans were updated in the Spring Statement in March 2025. The 2025 UKSR confirmed the allocation of spending between departments for 2026-27 to 2028-29 for resource and for 2026-27 to 2029-30 for capital.

The UK Government allocated a higher share of spending to the Department for Health and Social Care which is a devolved area in Scotland and therefore feeds through to the Block Grant. However, it also increased spending on reserved areas, retained local growth funding and set out efficiency and reform plans. Some departments face increases in real terms and others face real-terms reductions over the Spending Review period. Some of those facing real-terms reductions have a material impact on the Scottish Block Grant as a result of relatively high comparability factors under application of the Barnett formula.

For example, reductions to Department for Transport and Home Office settlements have contributed to lower overall growth in the Scottish Block Grant. The Home Office’s budget is seeing a real-terms decrease of 1.7 per cent per annum across the Spending Review period as the UK Government intends to significantly reduce the cost of the asylum programme.

Despite being a reserved matter, this reduction in asylum spending is directly impacting the Scottish Government’s Block Grant. This is because the application of the Barnett formula at a UKSR is undertaken on a departmental basis rather than at a programme level. Due to a high comparability factor of 73.3 per cent on the Home Office for Scotland, we’re seeing a large impact of these decisions flowing through at the UKSR. Similarly, the Department for Transport’s resource budget will see an average 5 per cent real terms cut across the Spending Review.

Another factor which has driven a lower settlement for the Scottish Government is the interaction with UK Government Business rates and non-domestic rates, which are fully devolved to Scotland. In England 50% of business rate revenues are retained by local government while 50% are passed back to HM Treasury to support spending on public services. To avoid the Scottish Government receiving Barnett on spending supported by a revenue source that’s fully devolved, we see a reduction in funding equivalent to any increases to the amount retained. Over this SR period that reduction will be £200 million higher per annum than the 2025-26 baseline figure. This reflects an end to a UK policy whereby several councils enjoyed a 100% retention agreement with HMT, and were not required to pass back funding.

Taken together, these spending allocations have led to a small 0.8 per cent real-terms growth on average up over the UKSR period, less than the 1.2 per cent real-terms average growth in total UK day-to-day spending. For the purposes of projecting the funding outlook into 2029-30, we assume a constant rate of spending growth into 2029-30 but that is subject to decisions by the UK Government at future Spending Reviews. These assumptions are the basis of the central Block Grant forecast used in this chapter.

The UK Government committed to providing additional funding for higher employer NICs costs for public sector employees. The Scottish Government has had confirmation through the Mains Estimates process that the Barnett consequentials will be £339 million in 2025-26. This additional funding does not cover the full costs of NICs rises to the Scottish public sector, with the full costs estimated to be significantly higher at over £700 million.[22] This means that the additional funding will need to be found elsewhere in the budget to cover these costs, which represents an additional risk.

2.2.2 Devolved taxes and Block Grant Adjustments

The Scottish Government receives revenues from Income Tax, Land and Buildings Transactions Tax (LBTT) and Scottish Landfill Tax (SLfT). Table 2.02 provides forecasts for the revenues, Block Grant Adjustments and the net position for each tax.

Forecasts of devolved tax revenue are produced by the SFC, and are influenced by Scottish tax policy and the growth and composition of the Scottish tax base.

The Block Grant Adjustments are calculated based on the forecast growth in equivalent tax revenues in the rest of the UK, on a per person basis. They are forecast by the Office for Budget Responsibility, and are driven by UK Government tax policy, population growth, and the growth and composition of the tax base in the rest of the UK.

The net tax position is the difference between devolved tax revenue and the Block Grant Adjustments. This represents the spending power available to the Scottish Government as a result of tax devolution. In general, it will improve when tax revenue grows faster, on a per person basis, in Scotland than in the rest of the UK, or vice versa.

Table 2.02 shows the positive contribution that the net tax position makes to the Scottish Government’s funding position. Income Tax is the largest component of the overall net position, based on the latest forecasts.

| (Figures in £million, current prices) | 2025-26 | 2026-27 | 2027-28 | 2028-29 | 2029-30 |

|---|---|---|---|---|---|

| Income Tax Revenue | 20,477 | 21,901 | 23,139 | 24,186 | 25,288 |

| Income Tax BGA | (19,639) | (20,830) | (21,614) | (22,287) | (23,107) |

| Net Income Tax Position | 838 | 1,072 | 1,526 | 1,899 | 2,182 |

| LBTT Revenue | 1,029 | 1,093 | 1,138 | 1,187 | 1,240 |

| LBTT BGA | (637) | (773) | (892) | (1,010) | (1,096) |

| Net LBTT Position | 393 | 320 | 246 | 177 | 144 |

| SLfT Revenue | 38 | 24 | 24 | 25 | 25 |

| SLfT BGA | (60) | (55) | (35) | (34) | (36) |

| Net SLfT Position | (23) | (31) | (10) | (9) | (11) |

| Total Net Tax Position | 1,207 | 1,361 | 1, 762 | 2,067 | 2,314 |

Source: Scottish Fiscal Commission, Office for Budget Responsibility.

Note that Income Tax figures are locked in for 2025-26 funding position (based on the position set out in the 2025-26 Scottish Budget).

Income Tax: Overall, Income Tax revenue and BGA forecasts have continued to increase, with the net position currently set at £838 million in 2025-26, rising to £2.2 billion by the end of the forecast period. However, there is substantial downside risk associated with the net position in later years. The sharp rise in the net position over the forecast horizon is driven by the divergent earnings growth assumptions of the SFC and OBR. The implied earnings divergence comparing the forecasts from the two Independent Fiscal Institutions is greater than has historically been the case (Figure 1.01 in Chapter 1), suggesting the sharp increase in the net position after 2025-26 is unlikely to be fully realised. In their publication, ‘Scotland’s Economic and Fiscal Forecasts – December 2024’[23], the SFC described it as an asymmetric downside risk. The potential scale of this risk is explored as part of the wider downside scenario for the Scottish Government’s resource funding (Section 2.3 and Annex B). To illustrate the scale of the risk, were earnings growth in the rest of the UK to converge with earnings growth in Scotland over the forecast period, that would result in a reduction to the net position of around £950 million in 2029-30.

Land and Buildings Transaction Tax (LBTT): Both Land and Buildings Transaction Tax revenue and the corresponding BGA are forecast to increase in 2025-26, reflecting the overall expected positive growth in property prices and transactions that generate LBTT and Stamp Duty Land Tax (SDLT) respectively.

The net position for the Land and Buildings Transaction Tax is estimated to remain positive over the forecast period, although there is variance across the period. The net position is currently forecast to be £393 million in 2025-26 but is expected to decrease to £144 million by 2029-30. This net position is impacted negatively from 2026-27 onwards because of a number of factors, such as the OBR forecasting faster growth in transactions in the rest of the UK than those being forecast for Scotland; a higher assumed rate of sales turnover in the UK dwelling stock; and the assumed effects of planning reforms in England, which are forecast to increase SDLT revenues and thus help boost BGAs relative to LBTT revenues.

The task of forecasting activity in UK and Scottish residential and commercial property markets involves many inherent risks as property markets are subject to several external, uncontrollable factors such as the behaviour of consumers and businesses who may have the choice to postpone, cancel or bring forward property transactions in response to wider economic changes. Additional risks include the possibility of further UK Government tax and housing or commercial property policy divergence, which could pose a fiscal risk for the Scottish Budget.

Scottish Landfill Tax (SLfT): The net position for the Scottish Landfill Tax is estimated to be negative over the forecast horizon, levelling out at around -£10 million per annum from 2027-28. This position is mostly driven by an explicit waste policy choice that the Scottish Government has made – the Biodegradable Municipal Waste ban which will prevent most types of waste from being landfilled from 31 December 2025. This ban does not apply in the rest of the UK. The SFC have stated previously (for example in their December 2024 forecast) that uncertainties remain around the impact of the Biodegradable Municipal Waste ban in terms of the volume of waste post-ban that will be legally landfilled and cannot be incinerated. There is further uncertainty (and therefore fiscal risk) around the waste industry’s response to the recent increases in incineration capacity in Scotland as well as to the ban itself.

Scottish Aggregates Tax (SAT): This will replace the UK Aggregates Levy (UKAL) in Scotland. This new tax will increase the number of devolved taxes, and the proportion of the Scottish Budget raised in Scotland.

The Aggregates Tax and Devolved Taxes Administration (Scotland) Act received Royal Assent on 12 November 2024, and the Scottish Aggregates Tax will come into force on 1 April 2026.

During the transfer of powers, the Scottish Aggregates Tax rate in 2026-27 will align with the UK Aggregates Levy 2026-27 rate, to ensure stability and certainty. The Scottish Aggregates Tax rate beyond the first year of introduction will be a decision for the next session of the Scottish Parliament. Future decisions on the tax rate will be taken as part of the annual Scottish Budget process.

Discussions regarding the BGA arrangements for SAT are underway between the UK and Scottish Governments, and will be agreed in advance of SAT introduction.

Box 2.01: Forecasting Scottish Aggregates Tax

The UK Government is not able to estimate the Scottish share of UK Aggregates Levy revenue from existing tax returns due to the limited nature of the information gathered from current taxpayers. Up until their published forecasts of 25 June 2025, SFC have therefore provided illustrative forecasts for SAT based on the production of aggregates in Scotland as laid out in the Minerals Year Book[24]. These forecasts did not, however, allow for the export (and import) of aggregate from (or to) Scotland and thus included exported aggregate for commercial exploitation that takes place either in the rest of the UK or overseas. Such material would, however, not be subject to SAT from 2026-27 and as a result it must be excluded from SAT revenue forecasts.

Based on survey information from the British Geological Survey, expected to be published in mid-2025, the updated SAT forecast now accounts for estimates of both exported (and imported) material. SFC have updated their approach, and their latest forecast is for SAT revenue in 2026-27 to be £37 million. In 2026-27, the first year of SAT, the tax rate will align with UKAL and rise to an assumed (but not actual) £2.15 per tonne. Revenue in 2026-27 is expected to be £37 million (rounded to the nearest £1 million). The SFC has assumed under their policy baseline that the tax rate will be uprated in line with forecast inflation, giving a rate of £2.41 per tonne in 2030-31. SAT revenue is expected to increase to £38 million by the end of the forecast period.

Table A.02 (Annex A) shows how the components of the net tax position have changed since the last published MTFS (May 2023). Both the SFC and OBR Income Tax forecasts have increased substantially over this period, although the BGA has risen by more, largely as a result of an increase in earnings growth forecasts from the OBR between the two Budget events. The 2024-25 Scottish Budget introduced the Advanced rate and raised the Top rate by 1 pence, while the 2025-26 Scottish Budget contained some smaller policy changes affecting the Starter and Basic rate bands, with other bands remaining frozen. The SFC has changed their approach to baselines, meaning that from 2027-28 onwards Higher, Advanced and Top rate Income Tax bands are no longer assumed to be frozen. This is consistent with their published approach to setting policy baselines[25]. This states, “we interpret neutrality with respect to policy baselines to mean that price inflation alone does not lead to changes in real tax revenue, real take-home pay, or the real value of social security payments as a result of our policy baseline assumption.”

Compared to the forecasts at the 2025-26 Scottish Budget, in 2025-26, the net Income Tax position has worsened, reflecting further convergence in the earnings growth forecasts from the OBR and SFC. From 2026-27 onwards there is an average reduction in the net position of around £180 million.

For LBTT, the net position has improved relative to 2023 MTFS, reflecting higher revenues across three years than previously forecast. This is largely driven by 2023 forecasts assuming a much lower growth in property prices. In part, this stronger performance is also driven by an increase in the Additional Dwelling Supplement (ADS) tax rate. The forecast for 2025-26 has risen modestly by £11 million since the December 2024 forecasts to £1.029 billion. This forecast increase is due to an increase in expected non-residential property LBTT. This, together with a more favourable BGA forecast in the Spring Statement, means the net position for LBTT has improved by £37 million since the December 2024 forecasts, though the overall net position is expected to reduce significantly after 2025-26.

The SLfT forecast for 2025-26 has fallen by £3 million since the December 2024 forecasts to £38 million. It is expected to stabilise at £24 to £25 million thereafter as the Biodegradable Municipal Waste ban will be fully in place. This reduction, together with a less favourable BGA forecast in the Spring Statement, means the net position for SLfT has fallen by £7 million since the December 2024 forecasts. No significant movement in the net position is expected from 2027-28 onwards.

2.2.3 Social Security Block Grant Adjustments

The Social Security BGAs reflect the funding from the UK Government to the Scottish Government to recognise the costs incurred by the Scottish Government for benefits that have been devolved. This transfer is based on what the benefits would cost the UK Government in Scotland, if they had not been devolved. Table 2.03 provides an outlook for the Social Security BGAs across devolved benefits.

The BGA forecasts in Table 2.03 are based on the OBR's March 2025 forecasts, except for Winter Fuel Payment, which reflects the UK Government’s policy change on Winter Fuel Payment announced on 9 June 2025 and includes an anticipated additional £120 million per year BGA funding. BGAs are principally driven by UK Government policy decisions and trends in social security spending in the rest of the UK at the time of the Spring Statement 2025. Updated BGAs will be calculated alongside the UK Government's autumn fiscal event, which will inform in-year changes to the BGAs for 2025-26 and the BGAs for 2026-27.

| (Figures in £million, current prices) | 2025-26 | 2026-27 | 2027-28 | 2028-29 | 2029-30 |

|---|---|---|---|---|---|

| Attendance Allowance | 803 | 859 | 890 | 920 | 955 |

| Personal Independence Payment | 3,271 | 3,608 | 3,787 | 3,982 | 4,270 |

| Disability Living Allowance | 984 | 1,031 | 1,064 | 1,078 | 1,065 |

| Carer's Allowance | 422 | 451 | 460 | 466 | 480 |

| Industrial Injuries Disablement Scheme | 84 | 83 | 81 | 79 | 76 |

| Severe Disablement Allowance | 5 | 5 | 4 | 3 | 3 |

| Cold Weather Payment | 6 | 6 | 6 | 6 | 6 |

| Winter Fuel Payment | 150 | 149 | 147 | 146 | 147 |

| Of which anticipated BGA funding from UKG Winter Fuel Payment policy change | 120 | 120 | 119 | 118 | 119 |

| Total Social Security BGA | 5,725 | 6,191 | 6,440 | 6,680 | 7,001 |

Changes in either UK Government policy relating to devolved benefits, or the OBR's forecasts of benefit demand in the rest of the UK, can affect the funding available to the Scottish Government in either direction, and the impact of social security spending on the wider spending priorities. Such changes can include the eligibility for certain benefits, changes to the generosity of certain payments or decisions on how payments are uprated over time.

The total Social Security BGA has increased relative to MTFS 2023 – most BGAs have increased. However, as shown in Table 2.04, compared to the BGA forecasts from the UK Government’s Autumn Budget in October 2024, the updated Social Security BGA funding forecast, including the anticipated funding increase from the UK Government Winter Fuel Payment policy change, shows an increase in funding of £129 million in 2025-26 and £173 million in 2026-27, followed by a decrease in funding of £7 million in 2027-28 reaching a decrease of £290 million in 2029-30.

The main reason for the decreased funding from 2027-28 onwards relates to the expenditure forecast for Personal Independence Payment (PIP) and Carer’s Allowance in England and Wales being revised downwards as a direct result of the welfare reforms announced by the UK Government in the 2025 Spring Statement.

These reforms include changes to the eligibility criteria for PIP in England and Wales from November 2026 and impact the projected PIP BGA. As changes to PIP eligibility affect the number of people eligible for Carer’s Allowance in England and Wales, there will also be a reduction to the Carer’s Allowance BGA from 2027-28 onwards.

| (Figures in £million) | 2025-26 | 2026-27 | 2027-28 | 2028-29 | 2029-30 |

|---|---|---|---|---|---|

| Scottish Budget 2025-26: December 2024 * | 5,596 | 6,018 | 6,447 | 6,846 | 7,291 |

| Latest forecasts: March 2025 ** | 5,605 | 6,071 | 6,321 | 6,562 | 6,882 |

| Anticipated BGA funding from UKG Winter Fuel Payment policy change: June 2025*** | 120 | 120 | 119 | 118 | 119 |

| Change in funding forecast | 129 | 173 | (7) | (166) | (290) |

Figures may not sum due to rounding

* Based on the OBR’s October 2024 forecast

** Based on the OBR’s March 2025 forecast

***Based on the indication from HM Treasury.

Overall, the total Social Security BGA is expected to grow by 5.2 per cent per annum in nominal terms, or by 3.2 per cent per annum in real terms. The total value of the Social Security BGAs in 2025-26 is currently 85 per cent of Social Security Assistance spending and this is forecast to reduce to around 79 per cent by 2029-30 mainly as a result of the welfare policy reforms announced by the UK Government in July 2024 and then again in the March 2025 Spring Statement. Prior to this it was expected to remain fairly steady over the next five years.

Uncertainty arising from UK Government welfare reforms in turn leads to uncertainty over the level of funding relating to devolved social security benefits. The UK Government announced on 9 June a change to its position on the Winter Fuel Payment, which we anticipate will increase the BGA funding we receive relating to the devolved Pension Age Winter Heating Payment by around £120 million per year. However, until the OBR cost and forecast the policy change alongside the UK Government’s autumn fiscal event, at which point updated BGAs will be calculated, the potential impact on the BGAs cannot be confirmed. The UK Government recently published the Universal Credit and Personal Independence Payment Bill which sets out the first set of proposed changes to ill-health and disability benefits. However, there remains uncertainty over the pace and scale of the reforms the UK Government will deliver on Personal Independence Payment with the next update from the OBR alongside the UK Autumn Budget. There is therefore higher uncertainty in the BGAs than normal.

2.2.4 Non-Domestic Rates

Non-Domestic Rates are administered and collected by councils. NDR revenue raised is pooled centrally at a Scottish Government level in the NDR Rating Account or ‘NDR pool’, and may be in deficit or surplus at any point in time, but all revenues are ultimately distributed back to Local Authorities over time. The Scottish Government guarantees the sum of General Revenue Grant funding and NDR income, thereby bearing any volatility risk with NDR revenue between forecast and outturn. NDR policy decisions including the poundage rates that apply and reliefs that are available, are made annually by Scottish Government at the Budget.

The central estimate of the NDR Distributable Amount – the amount guaranteed to Local Authorities each year – is based on the SFC’s forecasts of NDR revenues (the Contributable Amount) adjusted to reflect the closing balance of the NDR pool from the previous financial year and estimated prior-year adjustments, and takes into account Scottish Government policy on clearing the NDR pool deficit in a phased manner by 2028-29, as set out at the 2025-26 Scottish Budget.

The NDR revenues are forecast by SFC to grow over the forecast period, reflecting the fact that the tax rate is forecast to grow in line with inflation and the tax base is forecast to continue to grow. The SFC forecasts reflect policies announced at relevant budgets. Decisions on rates, reliefs and distributable amount are made at each Budget and future decisions will be accounted for in associated forecasts of income and distributable amount. Table 2.05 shows the forecasted distributable amount set by the Scottish Government.

The next NDR revaluation is scheduled for 1 April 2026, based on rental values as at 1 April 2025. Revaluation years bring increased forecasting risks and can introduce a degree of volatility to public finances. While the SFC expects to be able to use an imputed valuation roll in their forecasts ahead of the 2026-27 Scottish Budget, a draft valuation roll is expected to be made available from 30 November 2025 and is likely to be too late to form the foundations for these forecasts.

| (Figures in £million, current prices) | 2025-26 | 2026-27 | 2027-28 | 2028-29 | 2029-30 |

|---|---|---|---|---|---|

| Non-Domestic Rates - distributable amount | 3,114 | 3,549 | 3,480 | 3,534 | 3,861 |

2.2.5 Other income and expenses

Other income and expenses consist of funding elements which together form a relatively small share of the total funding. The Scottish Government has a greater degree of discretion over some of these, allowing some limited flexibility to manage funding volatility. The most significant items in the category include:

- Reconciliations – these relate to OBR and SFC forecast errors in past years. Estimates of future reconciliations are derived from the latest SFC and OBR forecasts from which the latest net position can be calculated. They reflect forecast error and do not reflect the performance of the Scottish Tax base or Social Security expenditure. They are a normal part of the Fiscal Framework operations and ensure that the Scottish Government’s funding is based on actual tax revenues and social security expenditure, rather than forecasts.

As an example, the Income Tax net position in 2022-23 varied significantly over time, from as low as -£428 million to as high as +£542 million before the final net position came in at +£260 million, resulting in a forecast reconciliation of positive £451 million. Outturn data for 2023-24 will be published in July this year and outturn data for 2024-25 is expected in July 2026.

The Scottish Government will continue to borrow to cover net negative reconciliations to smooth the impact on the funding position. The forecast 2023-24 income tax reconciliation to be applied to the Scottish Budget 2026-27 is positive £279 million. There is a forecast £851 million negative reconciliation for 2024-25 income tax to be applied to the Scottish Budget 2027-28. The main driver of this is stronger Income Tax revenue growth in the rest of the UK since the original forecast. This has led to a sharp increase in the Income Tax BGA for 2024-25. There is also a provisional forecast reconciliation in 2028-29 which shows a £222 million negative reconciliation.

- Resource borrowing – the Scottish Government has some ability to borrow for resource spending, but this is limited in practice to borrowing against forecast errors including reconciliations. The current policy is to borrow against net negative reconciliation which smooths the impact of the reconciliations in the funding position. No borrowing is assumed in 2026-27 as there is a large net positive forecast reconciliation. Borrowing in 2027-28 is set at the maximum of £663 million which is insufficient to fully mitigate the current forecast reconciliation with a £168 million shortfall. Borrowing in 2028-29 is set to £222 million to offset the corresponding forecast negative reconciliation.

- Borrowing costs – these are incurred by past and forecast resource and capital borrowing.

- Migrant surcharge – this is income derived from charges on migrants for using the National Health Service (NHS) and is redistributed to devolved governments on a Barnett basis. It is forecast to be £210 million across all years with the actual income confirmed in-year.

- Crown Estate Scotland Revenues – this revenue relates to option fees for the first round of offshore wind leasing (‘ScotWind’) and for Innovation and Targeted Oil and Gas (INTOG). The Scottish Government retains the flexibility to determine how this funding is deployed and at the 2025-26 Scottish Budget allocated revenues to a range of projects for longer-term benefit, including actions to tackle climate change, investments in economic growth and job creation, and projects to drive forward reform. Beyond the amounts included in the 2025-26 Scottish Budget, £350 million in Crown Estate Scotland income has been realised but not yet allocated. These amounts have not been profiled across the forecast period with decisions on their deployment to be taken at individual Budgets, in line with Scottish Government priorities.

- Scotland Reserve – the Scotland Reserve provides the Scottish Government limited ability to manage spending across financial years. A £501 million Scotland Reserve carry forward is forecast for 2025-26 based on provisional outturn position following the end of the 2024-25 financial year. The reserve assumption is set to zero in each future year.

| (Figures in £million, current prices) | 2025-26 | 2026-27 | 2027-28 | 2028-29 | 2029-30 |

|---|---|---|---|---|---|

| Reconciliations* | 500 | 272 | (851) | (222) | - |

| Resource Borrowing | - | - | 663 | 222 | - |

| Resource Borrowing Costs | (142) | (121) | (67) | (117) | (193) |

| Capital Borrowing Costs | (160) | (198) | (232) | (262) | (280) |

| ScotWind | 23 | - | - | - | - |

| Scotland Reserve | 501 | - | - | - | - |

| Migrant Surcharge | 210 | 210 | 210 | 210 | 210 |

| King’s and Lord Treasurer’s Remembrancer (KLTR) | 5 | 5 | 5 | 5 | 5 |

| Other** | 22 | (5) | (11) | (31) | (31) |

| Total | 959 | 163 | (283) | (195) | (288) |

* Note that for 2026-27 the total reconciliation includes a forecast income tax reconciliation of £279 million and a social security reconciliation deferred from 2024-25.

** Other category includes items such as Machinery of Government and Budget Transfers and other funding lines.

Table A.03 (Annex A) shows the change in the outlook for ‘Other income’ since the last published MTFS (May 2023). The change in outlook in 2025-26 is primarily driven by increased Scotland Reserve funding relative to the MTFS 2023 assumption as well as higher income tax reconciliation. The higher reconciliations in 2025-26 and 2026-27 reflect stronger performance for Scottish Income Tax than forecast at the 2022-23 and 2023-24 Budgets. However, the difference in the outlook for reconciliations in 2027-28 is negative as explained earlier in this section. The forecast reconciliations in 2027-28 and 2028-29 have worsened, with the difference being offset by increased resource borrowing, where this is possible within the borrowing limits available to the Scottish Government.

2.2.6 Capital funding outlook

This section outlines the key assumptions underpinning the central capital funding outlook presented in Table 2.01. It covers in detail the following elements of the capital outlook:

- The capital Block Grant

- Capital Borrowing

- Ringfenced funding and City Deals

- ScotWind

- Scotland Reserve

- Financial Transactions (FTs)

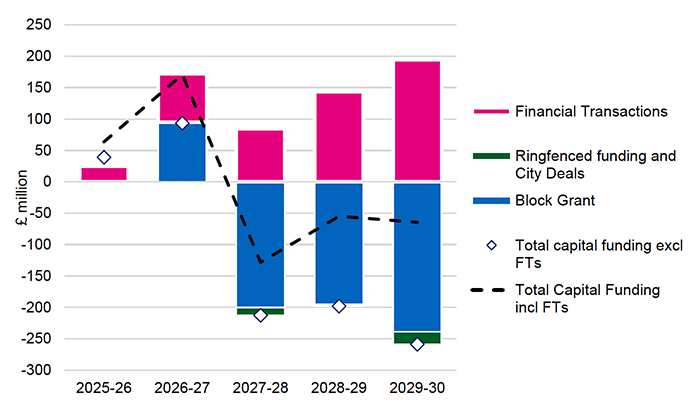

As shown earlier, total capital funding is forecast to remain broadly constant in nominal terms and reduce in real terms by 2029-30, an average real terms decrease of 1.8 per cent a year between 2025-26 and 2029-30.

The core capital Block Grant is set to grow by an average of 1.6 per cent a year in nominal terms over the period 2025-26 and 2029-30, falling by 0.3 per cent a year in real terms. The forecast capital Block Grant is lower than the estimate included in the multi-year outlook set out at the 2025-26 Scottish Budget,[26] which was informed by the OBR’s forecasted growth in the total CDEL envelope for the UK as a whole.

As with the resource Block Grant, the 2025 Spending Review provided clarity over the multi-year settlement for the capital Block Grant. However, the Scottish Government’s Block Grant for capital (including non-Barnett funding and FTs) is set to grow at a lower rate of 0.3 per cent a year in real terms compared to the 1.8 per cent rate for UK Departments on average.[27]

The UK Government has allocated a higher share of capital spending to Defence, which grows at an average annual rate of 7.3 per cent in real terms between 2025-26 and 2029-30. In contrast, total UK CDEL expenditure (including FTs) grows at 1.8 per cent a year over the same period. As a result, the share of total capital expenditure allocated to Defence rises from 18 per cent of the total to 22 per cent by 2029-30. The Scottish Government does not receive any additional funding from this increase, as Defence capital expenditure is a reserved matter. However, the Scottish Government benefits from increased capital spending on Transport.

Source: Scottish Government

The central capital funding outlook also includes UK Government funding for City Deals in each year, averaging £115 million between 2025-26 and 2029-30 as set out in the UKSR. This is lower than the previously estimated flat £122 million. City Deals funding is ring-fenced and there remains flexibility on the timing of its utilisation.

In contrast to the capital Block Grant, the FTs funding grows by over 20 per cent a year in nominal and real terms between 2025-26 and 2029-30, reflecting allocations confirmed in the 2025 UK Spending Review. FTs include loans or equity investment by the devolved governments into the private sector. FTs are £25 million higher in 2025-26 compared to the 2025-26 Scottish Budget position and £194 million higher in 2029-30. However, the level of FTs still remains below 2022-23 levels in nominal terms, and the Scottish Government’s share of the overall uplift in FTs funding is relatively low. This is because much of UK FTs funding is allocated to departments such as the Department for Energy Security and Net Zero (DESNZ), which are largely reserved, and have relatively low Barnett formula comparability factors. For example, DESNZ will see a £4.5 billion increase in FTs funding in 2029-30, against which the Scottish Government will only receive a £72 million uplift. The second largest recipient of FTs funding is Department for Housing, Communities and Local Government, which is predominantly devolved and generates the largest FTs consequentials for the Scottish Government.

2.2.7 Capital borrowing

For capital expenditure the Scottish Government can borrow up to £450 million annually, and £3 billion cumulatively, in 2023-24 prices. This means for the purposes of the 2025-26 Scottish Budget the limits are calculated as £471.7 million and £3,144.5 million respectively.

Following the Fiscal Framework Review, the Scottish Government reviewed its capital borrowing policy to ensure the facility could continue to support the capital budget over the medium term in a fiscally sustainable way. In the Scottish Government Borrowing memorandum,[28] published alongside the 2025-26 Scottish Budget, the following guidelines were adopted to assess any capital borrowing decision:

- Use £300 million of capital borrowing per annum as the default assumption;

- This will be amended as necessary to meet budget specific or in-year requirements; and

- Ensure, by way of a fiscal test, that at least £1.5 billion of capital borrowing headroom remains available for the subsequent parliamentary term.

Terms of borrowing, such as the tenor (the duration of the repayment period), will be determined when annual borrowing decisions are finalised and adjusted as necessary to ensure there remains sufficient headroom, as set out in the policy. This policy is reflected in funding assumptions for the forecast period as presented in Table 2.01. This capital borrowing policy will apply to all Scottish Government decisions on borrowing, irrespective of the source of borrowing.

The Scottish Government is progressing its due diligence on Scottish Government Bonds. This continues to suggest bonds offer a valuable tool to support the capital borrowing policy and broader fiscal and economic objectives. Preparations continue to define the structure and policy parameters for a successful inaugural bond issuance and a sustainable framework for future years. An update on progress will be provided ahead of the 2026-27 Scottish Budget.

2.3 Funding risks and alternative scenarios

2.3.1 Alternative funding scenarios

The central funding outlook presented earlier in this chapter is subject to several risks and uncertainties. While the multi-year Block Grant settlement from the UKSR has provided some certainty over the level of funding from the UK Government, some uncertainty remains over the forecast period. Risks due to unanticipated changes in UK Government spending, allocation of spending between devolved and reserved areas, volatility due to forecast errors and differences in economic performance all remain.

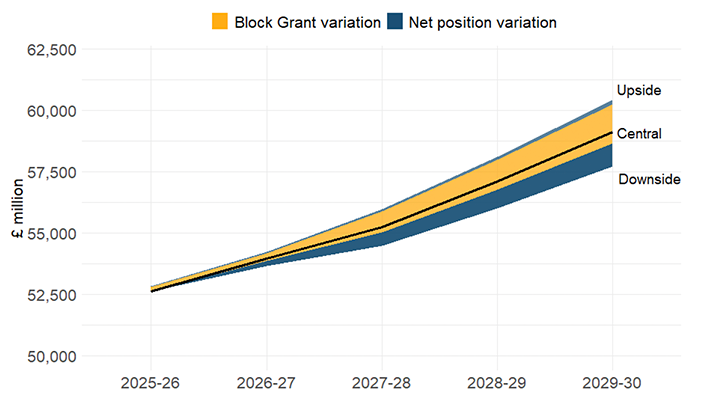

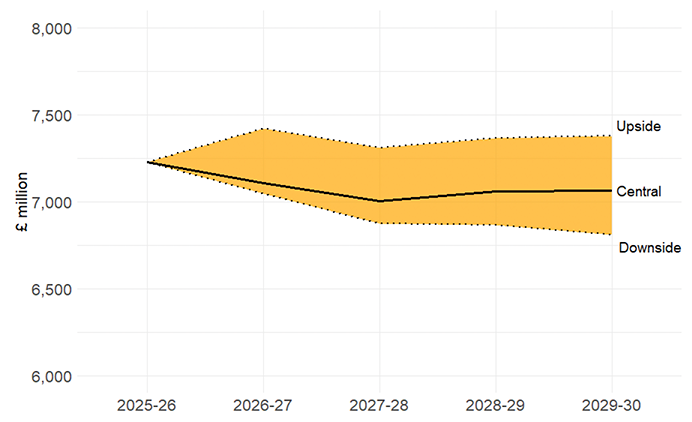

This section presents illustrative upside and downside scenarios for the funding envelope to demonstrate the scale of possible outcomes, with further detail of these set out in Annex B. Other elements of funding not considered in this modelling may also lead to divergence from the central scenario over time.

Overall, the analysis provides an indication of the direction and the magnitude of the impact if specific risks materialise for the Block Grant and the net income tax position. For resource funding, changes in both the Block Grant and the net tax position are modelled. Downside risks are assumed to be greater for the net income tax position, while for the Block Grant, the risk is greater on the upside – reflecting past trends that show higher outturns compared to Spending Review settlement. When taken together, the overall risk for resource funding is slightly skewed to the downside. For capital funding, the risk is assumed to be slightly more on the upside but the outlook is considered more volatile, reflecting historical trends.

Source: Scottish Government

Source: Scottish Government

2.3.2 Funding risk management

In the 2023 MTFS we set out a revised approach to the use of the Government’s resource borrowing and Scotland Reserve funding tools. This was to achieve the following objectives in order of priority:

a. Ensure a balanced budget by the end of each financial year;

b. Mitigate volatility in the medium-term resource funding outlook.

This approach remains in place.

By necessity, decisions on the level of borrowing and use of the Scotland Reserve are finalised at the end of each financial year. As such, best estimates are used at the time of in-year and future year funding positions.

The Fiscal Framework provides the Scottish Government with some tools to manage volatility and risk. The first review of Scotland’s Fiscal Framework was published in August 2023 and the Scottish Government outlined the changes secured through the review and their benefits alongside the 2024-25 Scottish Budget.[29]

As a result of changes agreed in the revised Fiscal Framework, borrowing and reserve limits increased as follows:

| (Figures in £million) | 2023-24 | 2024-25 | 2025-26* |

|---|---|---|---|

| Capital Borrowing (Annual) | 450 | 457.5 | 471.7 |

| Capital Borrowing (Cumulative) | 3,000 | 3,050.3 | 3,144.5 |

| Resource Borrowing (Annual) | 600 | 610.1 | 628.9 |

| Resource Borrowing (Cumulative) | 1,750 | 1,779.4 | 1,834.3 |

| Reserve | 700 | 711.7 | 733.7 |

*2025-26 cumulative limits are subject to The Scotland Act 1998 (Increase of Borrowing Limits) Order 2025 coming into force, which is anticipated to happen by June 2025.

These limits will continue to be annually uprated in line with inflation. The limits for the 2026-27 Scottish Budget will be calculated when the Office for Budget Responsibility publishes its updated deflator forecast alongside the UK Government fiscal event in the autumn of this year.

The changes to the borrowing and reserve limits improve the Scottish Government’s ability to manage fiscal risk and support infrastructure spending now and in the future. However, borrowing limits remain low in the context of the overall size of the Scottish Budget and the level of volatility that the Scottish Government is required to manage.

In the case of capital borrowing, as set out above, these changes enabled the sustainable level of capital borrowing to be increased by £50 million to £300 million per annum, to be stretched beyond this level in some years as necessary, and allow alternative sources of borrowing to be considered.[30]

The 2024-25 financial year provides an illustration of the benefits of the changes to the resource borrowing and Scotland Reserve limits. At the start of the year the Scottish Government could assign resource borrowing to offset the negative tax reconciliation in full; then when the tax and social security positions improved over the course of the year the Scottish Government was able to reduce borrowing to nil and carry forward additional funds into 2025-26. This would not have been possible to the same extent under the previous restrictions.

This ability to reduce borrowing and use the Reserve when circumstances allow demonstrates the Scottish Government’s commitment to responsible use of these increased powers. But these borrowing powers, while improved, remain heavily restricted and there is a clear case for them to be further enhanced to ensure the Scottish Government can address any tax or social security reconciliation and provide further support for infrastructure spending.

The Scottish Government continues to face the risk of negative reconciliations greater than its annual limit for resource borrowing to address forecast error. The current forecast reconciliation for 2024-25 income tax alone is negative £850 million, which is £187 million more than the forecast annual limit for 2027-28 of £663 million. Reconciliations are the product of forecast error and not the result of Scottish Government action. There is a strong argument for expanded resource borrowing to address forecast error to sufficiently mitigate against these risks. The Scottish Government has demonstrated its prudent approach to borrowing, which it would continue to apply should it be afforded strengthened borrowing powers.

The Fiscal Framework agreement calls for a formal review every five years with the next review due to take place in 2028. However, in view of the issues outlined above, the Scottish Government has called on the UK Government to agree to an earlier review.

Contact

Email: Scottish.Budget@gov.scot