Mobilising private investment in natural capital: report

This report looks at how to encourage responsible private investment into peatland restoration, including how to overcome barriers to scaling voluntary carbon markets to restore peatland in Scotland.

Section 8: Price Floor Guarantee

Overview of the mechanism

A PFG is a risk reduction or transfer mechanism. A PFG is well suited to early-stage markets in which demand is uncertain. The mechanism offers confidence in project revenues over a fixed period, which significantly reduces the downside risk profile for both investors and project developers. This is supportive of those projects that wish to hold some, or most, PIUs to verification.

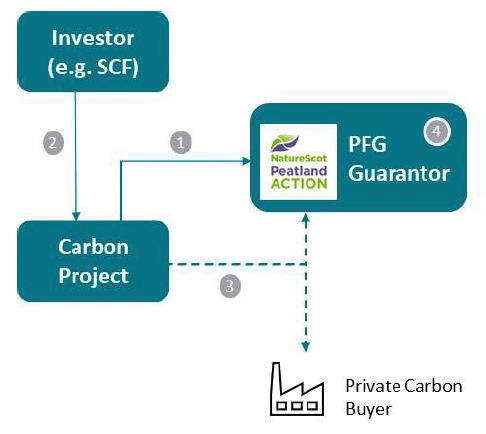

The price floor should operate as an aligned mechanism rather than an alternative to the SCF. Additionally, the guarantee should be accessible to projects that are not financed by the SCF too.The proposed structure of the guarantee is illustrated in Figure 19 and explained below.

How a PFG mechanism works:

1. The project submits a bid to secure a price floor agreement for the future sale of their PCUs to the PFG Guarantor. Typically, projects would aim to bid above their cost base, in order to ensure profitability or at least break even.

2. The project secures investment at an attractive rate from the investor as a result of the risk reduction offered by the guarantee. This could be the SCF.

3. Income is generated by the project from the sale of either PIUs or PCUs to corporates or brokers, or where market prices fall below the price floor, to the guarantor at the pre-agreed price threshold.

4. The guarantee reduces downside risk to participants. Where designed effectively, and if carbon prices are increasing over the period during which the guarantee operates, this is achieved with minimal government pay out to participants.

Managing Risk with a Price Floor Guarantee

Investors and Project Developers are exposed to two forms of risk, project risk and market risk.

Project risk refers to risks at the project level, such as cost overruns, or risks associated with validation and verification that impact the number of PIUs / PCUs a project is able to sell. A price floor does not reduce project level risk. Project risk can be mitigated by diversifying investment across a portfolio of projects and through other tools, such as contractual agreements with landowners and third party contractors.

Market risk relates to future carbon pricing and liquidity (i.e. ease of sale) of carbon credits. This risk is common to all projects. Market risk is driven by a variety of external economic and political factors. Where a price floor is agreed, the downside risk is reduced by the guarantor, with the price floor representing a revised “worst case scenario”. If the price of carbon rises above the price floor the investor benefits from the market pricing; should the price fall, the investor is protected by the price floor mechanism.

Under normal market conditions, the target or ‘risk adjusted’ return required to attract investors is proportionate to the perceived risk taken. By reducing market risk, the target return required to attract investment can be reduced, translating to a lower cost of investment

Recommended design options

The stakeholder engagement process evidenced mostly positive market feedback on the proposed PFG mechanism. Investors in particular noted the attractiveness of this mechanism to limit the downside risk of their investments given the difficulties associated with assessing the demand for carbon credits over very long timescales.

Some stakeholders noted that the guarantee would need to be designed carefully to avoid undue complexity, potentially limiting participation, or a "race to the bottom" in which only low quality projects with a low cost base would manage to secure a guaranteed price.

The mechanism also compares well when evaluated next to other alternatives which have limitations, as detailed in Table 14 below.

| Mechanism |

Headline Considerations |

|---|---|

| Buyer Of Last Resort (BOLR) mechanism |

|

| Revenue Guarantee |

|

| Contracts for Difference (CfDs) |

|

In conclusion, the PFG is best adapted to the current level of development of the peatland carbon market. The mechanism uses a reverse auction process for efficient price discovery. It also leaves the delivery risk in the hands of the projects, and ensures that appropriate project design and delivery is incentivised.

Setting the Price Floor

When structuring an effective PFG, setting an appropriate floor price is key. Pricing can be set in two main ways, administratively or through a reverse auction process.

Administrative pricing: The guarantor defines the floor price internally based on an assessment of the market (or negotiation with stakeholders). All eligible projects applying to the guarantee are accepted until funding capacity is exhausted. OFGEM's Feed-in-Tariff Export programme is an example of an administratively set price floor.

Administrative pricing is simple to administer but may be less effective than an auction (as a market based mechanism) at identifying the most efficient pricing because the Scottish Government would have to make assumptions on aggregate peatland projects' cost structure to determine an appropriate level for the price floor (i.e., a level that allows projects to breakeven).

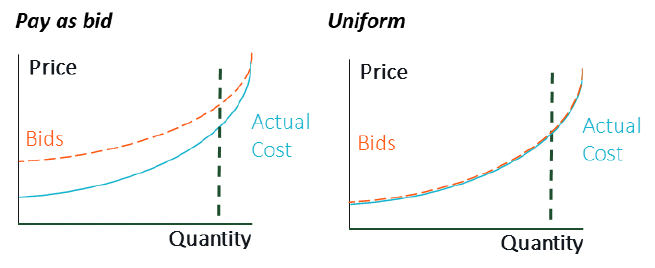

Auction based pricing: Eligible projects bid into a reverse auction held periodically by the government to set a price. Projects are ranked by price and are accepted sequentially until the funding capacity is exhausted (or an administratively set reserve price cap is hit). Through this project, two key mechanisms have been assessed:

- Uniform pricing: in which all successful projects receive the same guaranteed price (equivalent to the highest bid approved), regardless of their bid price point; and

- Pay as bid pricing: in which all successful projects are awarded a guaranteed price according to their own bid price point.

The difference between these two pricing models is illustrated in Figure 20.[55] In both cases, bids are ordered from lowest to highest cost. Price is represented on the Y axis with bids distributed from left to right along the X axis. The total capacity of the auction (funding available from the guarantor) is represented by the quantity line in green on the X axis. Projects to the right of the dotted quantity line are not funded because all the funding available from the guarantor has been used.

Under a pay-as-bid model, successful participants receive a PFG based on their submitted bid price. Participants with a lower cost of delivery are (inadvertently) incentivised to approximate the maximum price at which their bid may be accepted, a practice known as "sniping". As represented, this may lead to a divergence of bid pricing from the true price point that bidders would be willing to transact (represented in blue).

By contrast, under a uniform price auction, the price floor received is not linked to the bid price submitted. This removes incentives for participants to bid above the true delivery cost of restoration activities (or minimum price at which they would be willing to transact). In theory, this transparency may lead to a lower auction clearing price and more equal treatment of bidders. In addition a uniform price point may allow for more transparent long-term administration with a single price threshold.

For these reasons, it may be more cost efficient to operate a uniform price auction than a pay-as-bid model. Notably, the Entrade Poole Harbour nutrient trading scheme shifted from a pay-as-bid to the uniform price auction to test the comparable effectiveness of these approaches. Working in partnership with the University of Exeter Land, Economics, Environment and Policy Institute a uniform price auction structure was designed and implemented. A significant reduction in costly bidding behaviours was observed under the uniform pricing approach, leading to a greatly improved spending efficiency for Wessex Water.[56]

It should be emphasised however that in different scenarios, other factors (e.g. other grant programmes or revenue streams, incomplete understanding of the mechanism or uncertainty over delivery and maintenance costs) may also drive participant behaviour. This is particularly true given the wide variety of interventions required by different peatland restoration projects. Designed poorly, auction based mechanisms can incentivise lower cost rather than better value, but can be managed actively to avoid perverse incentives. Different auction based mechanisms for a government-backed price floor should be further explored to better understand their suitability for peatland carbon markets in Scotland.

Duration and Capacity

Under the PC, restoration projects can span from 30 to 100 years in length.[57] PIUs are verified on a linear basis across the lifetime of the project. A PFG could be offered to projects for their full life, or for a fixed period. The longer the term of the PFG, the greater the benefit to the project. A shorter term guarantee (e.g. 5-10 years) is likely to offer limited benefit to projects. Notably the Woodland Carbon Guarantee has a maximum duration of 35 years.[58] The benefit of a long duration will need to be weighed up against the challenges for Scottish Government of managing this type of long-term liability.

Another challenge is that it remains difficult to forecast demand for carbon credits over long time periods (many peatland restoration projects will continue to generate credits for up to 100 years). This is being driven by the current focus of carbon buyers on purchasing credits to meet their near-term offsetting needs. Additionally, the SBTi framework, which drives the climate commitments of numerous organisations, favours the use of carbon removal credits (such as woodland carbon credits), over carbon reduction credits (such as peatland carbon credits), particularly over the period after 2050. As such, establishing a price floor that extends beyond 2050 could improve confidence in the long-term economic viability of projects.

The capacity, or amount of funding committed through the guarantee will need to be considered alongside duration. Auction capacity should be frequently revisited to ensure that market demand is met, while ensuring the process remains competitive.

Timing and frequency

Alongside the duration of the guarantee, auction designers will also need to consider the timing and frequency of auctions for the PFG.

Auctions should be designed so that applicants are also able to apply to other schemes. Some projects will only be able to proceed if successful in applications to both grant funding and the PFG. In particular this will include coordination with Peatland ACTION funding. Auction designers can build in flexibility for participants by providing extended application windows, clearly advertising timings in advance and holding multiple auction cycles annually (in order to provide frequent opportunities for new projects to apply for the guarantee).

Eligibility and delineation

Eligibility criteria can be used to target support towards projects with specific characteristics. Such criteria can be used to both limit access to the PFG to only those projects that fulfil minimum requirements, and to provide different levels of support to projects with different characteristics. This provides an important protection against the delivery of low quality projects or a "race-to-the-bottom effect. As an example, within the Woodland Carbon Guarantee's fifth auction, 50% of the available budget was allocated to 'predominantly native woodland' projects in order to incentivise the creation of native woodlands.[59]

Eligibility criteria can be used strategically to provide additional support to less economical projects which exhibit other 'desirable' features aligned with Scottish Government policy objectives. This additional support can be allocated as aligned grant funding (such as further targeted grants from Peatland Action for projects that include desired features), or through the operation of multiple auctions for projects with different characteristics (e.g. holding separate auctions for those projects that exhibit certain features, in recognition of associated higher costs). Stakeholders interviewed were asked to consider what eligibility criteria could be used to identify projects with desirable characteristics. These are considered in Table 15 below.

| Eligibility & Delineation Characteristics |

Considerations |

|---|---|

| Peatland Code Participation |

It was noted that the PC has specific eligibility requirements (e.g. minimum term of 30 years, minimum Peat depth). Some participants noted that the PC already set a high bar for eligibility and further or misaligned criteria would be unhelpful. Initially requiring PC participation may prove a simple and effective criteria to filter appropriate projects. Since the PC only requires restoration to a modified state, there may be scope for additional eligibility criteria to incentivise restoration to a near natural state. While it is possible to not link the PFG to the PC, we would strongly recommend this relationship is established to support market integrity. |

| Physical project characteristics |

Supply side stakeholders pointed to a large variance in restorations. While costs vary for different reasons, projects at high altitudes or furthest from transport networks were singled out as particularly complex to restore. It was noted that additional support may be required to restore sites in specific areas. However, this may be better provided as a package of targeted, aligned grants to improve the viability of these projects. This should be explored in further research. It was noted that actively eroding sites had a higher cost of restoration and are linked to higher project risk than drained or modified peatland sites. However, due to the significant carbon abatement benefit recognised under the PC, these sites were often the most economically viable to restore based on carbon revenues alone. |

| Community engagement / benefit |

During the stakeholder engagement process, it was noted that community engagement in delivery was aligned to the Scottish Government Interim Principles for Responsible Investment in Natural Capital. It was noted that the PC has specific requirements for projects to demonstrate community engagement and benefit sharing. Due to the diversity of community led / engaged projects, indicators of engagement tended to vary broadly. As a result these indicators may be poorly suited to identify projects for additional support via this mechanism. More in depth consultations with community organisations may be required to determine the allocation of additional support on a case by case basis. |

| Ecosystem service co-benefits |

Restored peatland landscapes can provide additional ecosystem services beyond abatement of carbon. This includes a series of biodiversity and water environment benefits (flow attenuation and quality). Biodiversity benefits include the restoration / creation of habitats for protected species including a range of ground nesting birds. Based on feedback from stakeholders, there was no evidence that peatland sites with greater biodiversity value were less economical to restore. Rather, it was noted that the greatest biodiversity benefit was achieved from restoring those sites in an actively eroding condition. As noted these sites are rewarded well through the PC. It was noted that delivery beyond "modified" condition is not well rewarded by the Peatland code. Sites that aim for higher, "near-natural" condition could receive supplementary support if desired/ targeted. Water environment services provided by restored peatland include flow attenuation and water quality benefits. The value of these benefits is geographically variable. This benefit may be monetised and stacked with carbon revenues for sites where willing payers exist and restoration would not otherwise occur (thereby meeting PC additionality criteria). In other areas with lower hydrological stresses there may be limited value in these services. For this reason, water based co-benefits are also a poor fit for eligibility criteria. |

For eligibility criteria to be used effectively to earmark projects for differentiated levels of support under a PFG mechanism, this must be clear and transparent to ensure consistent treatment of projects. While some clear cases for varied levels of funding exist, the additional complexity of this may outweigh the benefits offered. As this mechanism matures, and specific cases where supplementary grant funding is required to tackle specific project types / features, this may be implemented gradually.

As noted, the eligibility criteria embedded within the PC already set a high bar for participating projects. It will be important for the Scottish Government to continue to engage with the PC to ensure that alignment between national objectives and existing eligibility requirements continue.

Indexation

The indexation of a floor price was perceived as a key desirable feature of the guarantee mechanism for investors. In particular, large institutional investors have a strong appetite for "index-linked" products which provide protection from variable levels of inflation over long periods of time. Three broad options are available in the design of a PFG:

- No Indexation: The price floor will not increase over time and will stay fixed at the agreed price. Under this approach the "real" value of the price floor will decrease over time (due to inflation). This may undermine the function of the price floor as after a 20 to 30 year period, funds may be worth a small fraction of their current value;

- Fixed inflation: The price floor will increase annually by a fixed percentage. This may be aligned to a target value (e.g. the long term Bank of England inflation target of 2%[60]). This de-links the price floor from indexation and allows for accurate government forecasting of liabilities, but is less attractive to investors than a fully index linked product; and

- Indexation: Linking a price floor to an established index such as the Retail Price Index (RPI), provides investors with confidence that the "real" value of the floor is maintained. Both the Woodland Carbon Guarantee, and Feed-in-Tariff Export have linked price floors to RPI. This model is the most attractive to investors.

An Index-linked approach will be most suitable for attracting low cost investment into peatland restoration projects. We recommend this approach is pursued if wider policy and economic constraints facing Scottish Government allow.

Surplus Management and Value Recovery

In the design of a PFG, the Scottish Government will need to consider how funds are accounted for and used over time.

The Scottish Government will need to account for commitments under the price floor as a contingent liability until participating projects decide whether or not to exercise their rights under the guarantee (i.e. to sell their verified carbon credits via the guarantee and not to a private buyer). If funds are set aside (likely as a forecast budget cost) to meet the contigent liabilities generated by the price floor, this will include considering how funds are repurposed if the price floor is not exercised (as expected given expectations of increasing carbon prices).

Similarly, if projects do sell their carbon through the price floor, the Scottish Government will have the choice to retire credits, or resell these in the market to recover value through the scheme. Resale could significantly improve the efficiency of this mechanism if market pricing is close to the guarantee price. However this should be weighed up against the benefits of directly retiring credits, and the risk of deflating the market further through the resale of credits.

Key takeaways

A PFG offers an exciting way to unlock new investment in restoration and support longer term planning for carbon projects. The PFG is a highly flexibly mechanism and can be designed in a range of ways. However, the benefits of these additional features should be weighed up against the risks and cost of building complexity.

It may be most effective to develop the PFG over time starting with a simple model and refining this gradually. It is important that the PFG provides index-linked price support for an extended period (such as 30 years or more) to provide long-term confidence for investors. Importantly, the PFG should be designed in the context of other mechanisms and aligned grant funding to ensure that an appropriate level of support is offered to varying project types. Designed well, the PFG offers good value for money to Scottish Government and could have a transformative impact on the rate of peatland restoration in Scotland.

Table 16 below provides a summary of the potential risks associated with the PFG mechanism concept and the mitigations identified through the proposed design and action research process.

| Risk |

Mitigations |

|---|---|

| The PFG is set too high and may expose the government to large costs |

An auction based approach, with a fixed reserve price will cap the total liability to government and drive cost efficiency. Where projects do sell via the price floor the government is still spending effectively on restoration objectives. Moreover value may be recovered through onward unit sales if desired. |

| The PFG triggers a race to the bottom with the delivery of low quality projects |

The use of a uniform bid approach, coupled with clear eligibility criteria will reduce the risk of a race to the bottom. |

| Less economically viable projects are not supported |

The PFG is flexible and can use delineation criteria to shift support to underrepresented project types. This could also be supported by the use of targeted aligned grants to set all projects on an equal footing in carbon markets. |

| The complexity of the mechanism disincentivises participation |

The mechanism should be developed gradually with complexity and nuance added over time. Clear communication and outreach to market participants will help to build knowledge and awareness. |

Contact

Email: peter.phillips@gov.scot