Mobilising private investment in natural capital: report

This report looks at how to encourage responsible private investment into peatland restoration, including how to overcome barriers to scaling voluntary carbon markets to restore peatland in Scotland.

Section 10: Establishing good financial governance

Scaling peatland carbon markets without building strong financial governance could have disastrous consequences for the Scottish Government's peatland and climate objectives. Projects without appropriate financial governance are more likely to fail, undermining market confidence and potentially creating unforeseen long-term liabilities for farmers and landowners. Projects must clearly demonstrate how restored peatland will be maintained in the long term and crucially how this will be funded in order to build confidence in their long-term viability. Analysis carried out under this project based on project costing data provided by RSPB Scotland and Peatland ACTION indicate that upfront delivery costs represent a mere 35% of lifetime costs (on a net present value (NPV) basis for a 50 year project). As such, the three mechanisms covered above (namely the SCF, PFG and Operating Payments) are well suited to support the establishment of financial governance practices in the Peatland Carbon market in Scotland.

The benefit of good financial governance is illustrated in the two illustrative cashflow graphs below. The first represents a restoration project with poor financial governance, defined as no / limited planning for long term maintenance liabilities. The second graph represents a project with stronger financial governance, supported by private investment and the three mechanisms explored in this report. In this scenario each of the mechanisms play a key role in directly de-risking investors ( in particular the SCF), reducing price and liquidity risk to the project as a whole (in particular the PFG) and providing confidence in financial governance and carbon outcomes (in particular the Operating Payments). As illustrated, the benefit of these mechanisms in tandem is substantially greater than the sum of the parts. All assumptions used to design these scenarios are included in Annex E.

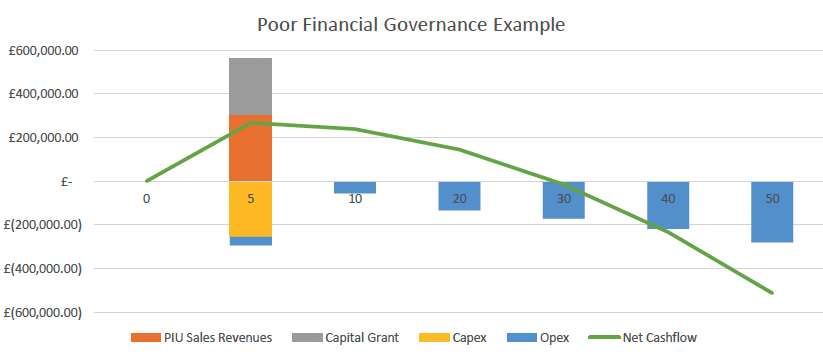

In this first scenario, capital costs are fully funded by a capital grant from Peatland ACTION, as illustrated in Figure 23. The project generates a short term surplus from the sale of 100% of PIUs at a price of £20 per PIU. In this scenario, this surplus is placed in an interest yielding account and appreciates at a rate of 1.5% per annum, with funds used to meet operating costs. Funds are sufficient to meet costs for a period of 28 years (and the landowner does not make any profit from the sale of carbon as all the proceeds from the sale are used to cover maintenance costs). Without the interest generated, this would be a period of 24 years. After this period, costs of maintenance fall to the responsible entity (e.g. landowner). If the landowner is unable to service costs, the project may revert to its pre-restoration condition due to a lack of maintenance.

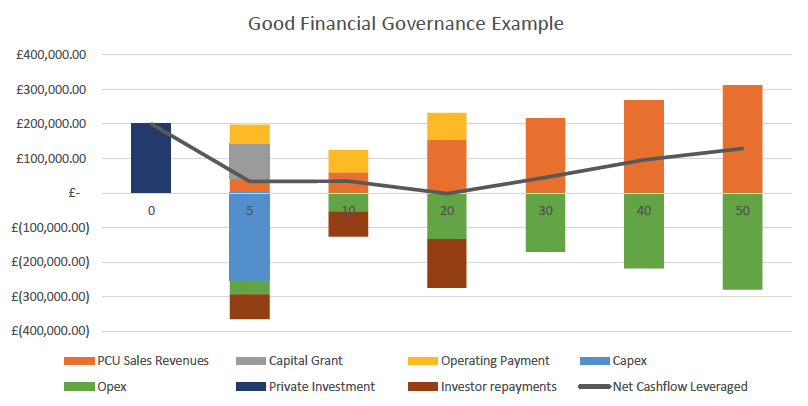

In this second scenario, a set of strong financial governance arrangements allow projects a better chance to remain cashflow positive for the full 50 year term, as set out in Error! Reference source not found.. All other project assumptions (as set out in Annex E) remain equal. The same amount of grant funding is provided to the project (on an NPV basis) but a portion of this is provided as an annualised operating payment spread over 15 years. In this scenario, capital costs are funded by a smaller capital grant (40%), and a fully amortising term loan (a loan which is completely paid off by the end of its term). This loan could be secured from the SCF, or from a third party investor. Investors are attracted to the SCF due to the existence of first-loss capital, as well as the PFG which both reduces market risk as well as provides a minimum annual cashflow to projects. The project is able to meet capital repayments and maintenance costs through the regular sale of verified PCUs and through operating payments. Following the repayment of the capital, PCU sales remain sufficient to meet operating costs and generate a small annual surplus for the project manager/ developer/ landowner (indicated by the net cashflow leveraged line on Figure 24).

Good Finance Governance Example – How it works

- In the scenario illustrated in Figure 24, we see investment raised at the start of the restoration project used to fill the capital need left by reduced grant funding.

- Alongside the capital grant, this investment covers the cost of restoration and early maintenance.

- Capital is repaid over a term of 25 years from the revenues generated by the project.

- Both financing and operating costs are met by the sale of verified carbon on a recurring basis, and operating payments provided for the first 15 years.

- Carbon sales continue to support the project until the end of the project term.

- The project is able to raise investment at establishment against confident future carbon revenues, because these ongoing carbon revenues are supported by a PFG, providing confidence to funders.

Supporting strong financial governance is not only desirable, but is necessary to unlock private investment at scale. Impact investors will not support projects unless they can demonstrate their ability to deliver target outcomes with confidence. The SCF and PFG are well suited to support scale up, create and share best practises, and drive improvements in financial governance. but should be designed in tandem with changes to the public sector funding infrastructure to unlock investment and ultimately scale the market.

Contact

Email: peter.phillips@gov.scot