Mobilising private investment in natural capital: report

This report looks at how to encourage responsible private investment into peatland restoration, including how to overcome barriers to scaling voluntary carbon markets to restore peatland in Scotland.

Section 5: Stakeholder engagement findings

The stakeholder engagement process was designed to gather the views of a representative sample of organisations involved in, or impacted by, nascent natural capital markets in Scotland, with a particular focus on peatland and on carbon markets. The process aimed to determine if support from any of the key stakeholder groups is currently lacking and identify the reasons behind any reluctance to engage in peatland restoration.

Stakeholder interviews focused on identifying the key barriers and enablers to peatland restoration, as well as testing interest in the SCF and PFG mechanisms and potential design features. The interviews also aimed to understand the key factors influencing stakeholders' decision to undertake or take part in peatland restoration.

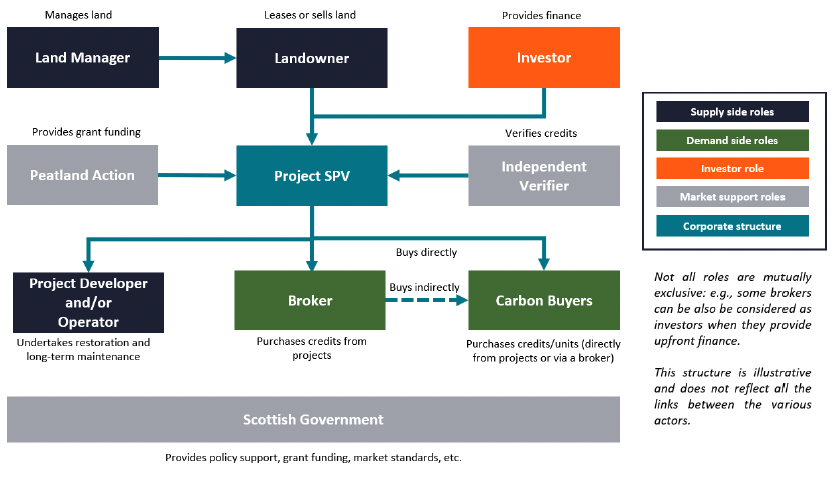

Figure 4 below summarises the main stakeholder groups involved in the peatland carbon market and their roles.

The various stakeholders involved in peatland restoration were classified into 3 main categories:

Supply side: includes landowners, land managers and project developers/ operators. These actors are directly involved in the delivery of peatland restoration, and include both privately-owned and community-owned estates.

Investors: refers to market actors providing finance to peatland restoration projects, typically to achieve a financial return. This category focuses on large institutional fund managers that are managing money often on behalf of large institutional clients, such as pension funds, insurance and corporations, or retail investors such as private individuals.

Demand side: refers to the buyers of credits, mostly corporate entities and brokers/ intermediaries.

Additionally, a few stakeholders providing market infrastructure support, such as the Scottish Nature Finance Pioneers and the Peatland ACTION scheme, were also contacted.

Engagement with supply side: findings

Landowners

Scotland has one of the most concentrated land ownership patterns in Europe. As such, the ability to scale peatland restoration hinges on the decisions made by a relatively small number of large landowners.

Finance Earth engaged with both private and community-owned estates. All estates consulted had some involvement in peatland restoration. However, the areas restored were often small. To-date, estates have mostly experimented with pilot projects to understand key success factors and test approaches to the physical work involved in peatland restoration projects. Estates' restoration activities have been financed mostly through Peatland ACTION grant funding and, in some cases, the upfront sale of PIUs.

Altitude, deer grazing and movement, effects of climate change, public access rights, the short annual window in which to carry out restoration work, the short supply of quality contractors, and difficulties in accessing peatland sites were all mentioned as factors significantly affecting restoration success. These many factors create a significant level of uncertainty and risk for peatland restoration projects, a problem that is compounded by the limited track record of existing peatland restoration projects (few projects are older than 10 years in the U.K.). As a result, several stakeholders suggested that insurance mechanisms might help to mitigate some of the risks affecting the success of projects.

Several estates also communicated a desire to preserve their autonomy and independence, and to manage their land according to their own priorities. Although most estates are comfortable with long term planning, the use of Peatland ACTION funding, private finance, and the PC all come with a set of restrictive conditions which have the potential to create material long-term liabilities. For instance, the minimum length for a peatland restoration project registered under the PC is 30 years (but in practise minimum length is rarely under 50 years) and several estates highlighted concerns over the long-term maintenance requirements and associated financial liabilities, noting that there are few peatland restoration projects older than 10 years in the UK, making it difficult to assess their long-term performance.

More broadly, the potential imbalance of power between large investors and landowners, which could result in the unequitable split of benefits, was perceived as a key risk. For instance, the upfront sale of carbon to a large investor or project developer presents the risks of insufficiently provisioning for long-term maintenance costs, capping the upside for landowners and concentrating proceeds in the hands of the current generation at the expense of future generations that will have to maintain the project without receiving carbon revenues. Additionally, some landowners were concerned about selling carbon that could be needed in the future to meet their own carbon insetting requirements.

In short, landowners appear to be one of the main stakeholder categories that remains to be convinced to scale up restoration beyond small pilot projects. They will require a compelling value proposition that preserves some of their independence, and provides mechanisms to share long-term delivery risks and rewards for land use changes.

Case study: Rottal Estate

Located in the south-east corner of the Cairngorms National Park sits the ~3,200 ha Rottal Estate. Over the last 15 years, the estate has undergone a transition from a focus on traditional upland activities, such as grouse shooting and deer stalking, to a more holistic approach to estate management. Habitat restoration at a landscape scale, including the planting of over 250,000 native trees, the restoration and re-naturalisation of rivers and burns and the creation of wetlands, has resulted in significant improvements in water quality and reduced flood risk in regions downstream of the estate, and delivered improvements in the population numbers of peregrines and Atlantic salmon.

In 2020, using funding from Peatland ACTION, the Rottal Estate took 27 ha of upland peatland out of agricultural and sporting use for restoration and carbon purposes, blocking historical agricultural drains and revegetating areas of bare peat. With support from Caledonian Climate Partners, the restoration project was certified and validated under the Peatland Code, issuing 5,493 PIUs to the project for the emissions reductions that the restoration is expected to achieve over the 100-year duration of the projecti. Rather than claiming a lump sum at the start of the project through selling all these PIUs upfront, Rottal Estate have chosen to hold onto PIUs until they vest into PCUs over time. Through this approach, the estate is able to benefit from any future increases in carbon prices, whilst also generating a sustainable revenue stream to support the long-term maintenance obligations of the project.

Given the success of this 27ha pilot, the Rottal Estate are now looking to scale peatland restoration efforts over 300 ha, delivering carbon and wider ecosystem services benefits.

Land managers and advisors

Land managers (providing estate management services to private landowners) were also able to provide additional insights about a more diverse set of landowners.

Some indicated that landowners are reluctant to undertake peatland restoration because it is perceived as an activity directly conflicting with their other economic activities, such as deer and game hunting.

Additionally, several estates are managed for leisure purposes and securing additional financing, whether through carbon markets or other sources, is not necessarily a motivating factor. For these estates, the point was made that a "stick", such as peatland emission pricing / taxation, might be more effective than a "carrot", such as the ability to generate income through the sale of carbon credits.

At the same time, land managers also pointed out that a significant portion of their clients are indeed curious about – and considering – natural capital markets (carbon markets in particular) as a potential new revenue stream to add to their existing economic activities. It is notable that, in many cases, land managers increasingly have dedicated employees specialised in natural capital and carbon markets, evidencing the heightened interest in these emerging opportunities.

Project developers

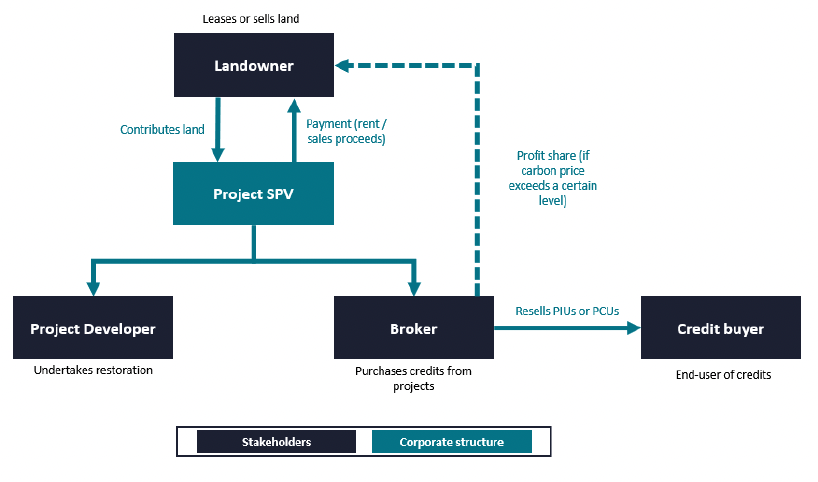

Project developers often assume several roles in the peatland restoration market. In addition to developing projects, they can also act as carbon brokers and finance providers to landowners looking to restore their peatlands – often in exchange for the sale of PIUs.

Figure 7 shows a simplified financing structure for a project selling PIUs upfront to finance restoration and maintenance costs. Some projects are structured using a profit sharing model that enables landowners to benefit if carbon prices pass a pre-determined threshold.

Several project developers are of the opinion that the current structure of the peatland restoration market is not yet favourable to private investment and limits the growth of the market. This is due to a range of factors, such as low carbon prices affecting the economic viability of projects, Peatland ACTION funding for capital costs crowding out private investors, uncertainty regarding future changes in government policies, verification methodologies and carbon prices, and the perceived complexity of the PC.

To be noted, although the PC was perceived as complex, Verra's "VM0036 Methodology for Rewetting Drained Temperate Peatlands" and Gold Standard's "Soil Organic Carbon Framework Methodology" are more complex and costly, and less well suited to small scale peatland projects, which represent the majority of the restoration opportunities in Scotland. Innovations being introduced by Wilder Carbon are likely to appeal to some segments of the carbon offsetting and insetting market, but the longer project durations are unlikely to appeal to most private landowners.[37]

In conclusion, project developers were not identified as a major barrier to scaling up the peatland restoration market. They broadly perceived the SCF and PFG as useful in shaping the market and unlocking some of the key barriers associated with peatland restoration. However the lack of contractors on which projects developers rely to perform the physical restoration works was seen as a significant barrier.

Community groups

Farmers and crofters are key community stakeholders whose geographical distribution overlaps significantly with Scotland's peatlands. Most land in Scotland is either under crofting or farming management agreements which involve activities such as sheep grazing on common land, crop planting on arable land, forestry and sometimes peat cutting (for fuel and growing media).

In their majority, bodies representing farmers and crofters have adopted a cautious approach to carbon markets. For instance, the National Farmers Union of Scotland (NFUS) recommends that its members do not engage in the sale of carbon credits until the integrity of the market improves. One of the main concerns is related to the impact of carbon markets on land use change, as crystalised in this quote: "NFUS is concerned that unregulated trading [of carbon] could lead to a reduction of land which would be best used to produce sustainable food."[38] In recent years, farmers have experienced significant increases in land prices, in part due to tree planting programmes fuelled by organisations aiming to offset their GHG emissions and are concerned that peatland restoration could further exacerbate the trend of shifting land from agricultural use to other uses.

One key question for tenant farmers and crofters relates to carbon ownership rights and how rewards are split between tenants, landowners and investors. In particular, tenant farmers are concerned that most of the rewards from the sale of carbon benefits generated by their interventions would accrue to landowners and investors, and thus have little incentive to participate. As such, a peatland restoration model which provides tenant farmers and crofters with a financial reward for their participation could help to incentivise their involvement in the market. Crucially, involving farmers could also help to alleviate capacity constraints around the supply of qualified contractors that is currently hampering the scaling of peatland restoration projects. However, this solution would also require further training and investment – which could be provided by Peatland ACTION and/or could be incorporated into new market mechanisms, such as the SCF.

The importance of education and awareness raising efforts to explain the benefits of carbon markets (and peatland restoration) was mentioned as a key factor in obtaining buy-in from the agricultural sector. This requires working with farmers to look beyond food towards a broader set of ecosystem services as a source of revenue.

This shift is already being encouraged in England through the proposed Environmental Land Management scheme (ELM) under development by Defra. Under the largest ELM programme, the Sustainable Farming Incentive (SFI), farmers are remunerated for taking specific steps to generate positive outcomes for nature.[39] In Scotland, the Agricultural Bill consultation recognises the important role that both public and private investment in Scotland's natural capital can play in delivering net-zero targets, alongside wider environmental and social benefits.[40] Ahead of the forthcoming Agricultural Bill, the Scottish Government is rolling out the National Test Programme [41](NTP) over the next three years. The NTP gives farmers, crofters and land managers access to new guidance on financial support for activity that will improve awareness of their climate performance, for example information on how to make a claim toward the cost of carbon audits. Creating the right incentives framework and land use framework for the farming and crofting sector, as well as ensuring that tax and inheritance rules do not penalise farmers undertaking nature restoration will be key to creating the right incentives to unlock nature restoration that benefits communities.

In summary, farming and crofting communities remain to be convinced that peatland restoration could provide long-term benefits to support livelihoods. For farmers, creating the right agricultural payment incentives, access to finance and an equitable split of carbon revenues might suffice. However, for crofters that consider their activities as a way of life, measures beyond economic incentives may be required, including greater awareness regarding what it means to be a good custodian of the land.

Engagement with investors: findings

Investors are becoming more aware of the importance of nature, and are increasingly seeking new greener and more sustainable investment opportunities. However, given that natural capital markets remain relatively nascent, investors remain cautious of the risks and cite several barriers hampering their participation.

Investors perceive the lack of investable pipeline as the main barrier to investing in peatland restoration. This barrier is related to a range of factors, including data gaps in the mapping of peatland condition, limited contractor and surveyor capacity, small project size and fragmentation of peatland habitats eligible for the PC. In addition, Peatland ACTION capital grant funding was seen to crowd out private capital.

Some of these barriers are being addressed. For instance, the Scottish Government is filling data gaps by developing a more accurate mapping of Scotland's peatland conditions and depths. These maps will be available to investors and landowners and should better enable the identification of suitable pipeline. Additionally, the PC v2.0 will be published in late 2022 and allow more peatland types to be eligible for restoration (e.g., lowland fens and agricultural peatland), and additional types of intervention (including raising arable peat water tables and paludiculture) which should contribute to increasing the overall area of eligible peatland.

Investors are also often interested in the additional non-monetary benefits that are associated with nature restoration projects (e.g., local job creation, access to nature). However, they often do not endorse direct transfers of monetary benefits (e.g., through profit sharing mechanisms). The sharing of monetary benefits with communities is viewed by some as an additional burden on a nascent sector within which the economic viability of projects remains uncertain compared to more established sectors. Despite these reservations, investors broadly acknowledged that financial support provided by the Scottish Government to peatland restoration (through Peatland ACTION or potentially another future mechanism) meant that community profit sharing mechanisms should be considered.

Investors consulted viewed a potential financial contribution of the Scottish Government to the SCF and creation of a PFG mechanism very positively, and as a very important stamp of approval and display of their long-term commitment to the peatland carbon market. This is particularly important for investors such as pension funds and insurance providers looking to make long-term investment decisions but are currently cautious due to the nascent nature of natural capital markets and their fiduciary duties to members

In conclusion, there is significant investor interest in peatland restoration, but there is a lack of market-ready opportunities. The limited data availability, uncertainty regarding future carbon prices, small size of the projects and generous upfront capital grant funding all currently limit the flow of private capital into peatland restoration. The SCF and PFG were perceived as an attractive combination to enable investors to gain exposure to peatland restoration while mitigating the long-term risks associated with engaging in the nascent peatland carbon market.

Engagement with demand side: findings

Engagement on the demand side was focused on brokers and end-buyers of credits, typically corporate entities and financial institutions. The engagement process uncovered evidence of demand from a wide range of corporate entities – from local Scottish Small and Medium Enterprises (SMEs) to large FTSE 100 and international companies. Two main demand drivers are currently driving purchasing decisions:

- Corporate Social Responsibility (CSR) needs whereby the buyer will use the credits to advertise their sustainability credentials; and / or

- Offsetting needs whereby the buyer will use the credits to achieve its net zero commitments or another corporate social or environmental target.

To be noted, these two drivers are not mutually exclusive and buyers might be purchasing credits to fulfil both needs. It is also notable that many buyers interviewed also value the local co-benefits associated with Scottish peatland carbon. This is illustrated by the following quote from one of the buyers interviewed: "We want to see biodiversity and community benefits in the carbon credits that we are buying". There is evidence of some buyers' willingness to pay a premium for Scottish peatland carbon and co-benefits – though it is unclear how much.

Despite positive demand signals, it was difficult to assess the robustness of demand over a multi-decade time horizon which matches the lifecycle of peatland restoration projects. Currently, most end-buyers of credits are focusing on securing PCUs or PIUs that will be vest into PCUs in the near term. This means there is a significant shortfall in supply of verified carbon in the carbon markets (both peatland and woodland) compared to demand. Although some large buyers of credits are starting to consider purchasing agreements allowing them to secure a supply of carbon over longer time periods, most of the demand for carbon remains concentrated in the near term.

Over longer time horizons, there remains a lingering preference of buyers for emission removal credits (such as woodland carbon credits) over emission reduction credits (such as peatland carbon credits), particularly after the 2050 timeframe. This is in part due to the Science-Based Target guidance for Beyond Value Chain Mitigation which recommends the use of removal credits to offset residual emissions after 2050.[42] This translates into limited demand for PIUs from peatland projects post-2050.

Anecdotally, Scottish peatland carbon credits appear to trade at a premium to international peatland credits (verified using methodologies from Verra or Wetlands International). However, buyers also tend to perceive less reputational risk in the purchase of Scottish peatland carbon due to the high standards of the IUCN PC and the robust jurisdictional framework in Scotland.

Overall, there is good evidence of near-term demand for large volumes of nature-based carbon credits with strong co-benefits, and for verified units. As a result, the stakeholder engagement process did not identify the lack of demand for peatland carbon as a major barrier to overcome in order to scale the market. However, it remains challenging to quantify precisely the demand for Scottish peatland credits, over the longer time horizon under which peatland projects generate carbon reduction benefits.

Summary of main barriers

The main barriers encountered during the stakeholder engagement are enumerated in Table 9 below. While some of the financial barriers and non-financial barriers can be addressed by the SCF and PFG, others would require further governmental action. The detailed mapping of proposed solutions against these barriers is developed in Table 18 in the conclusion.

| Category |

Description |

Importance* |

Supply |

Investors |

Demand |

|---|---|---|---|---|---|

| Financial barriers |

Low carbon prices affecting current financial attractiveness |

Medium |

X |

X |

|

| Uncertain future demand for carbon credits, particularly reduction credits |

High |

X |

X |

X |

|

| Increasing land prices and associated social consequences |

Medium |

X |

|||

| Existing funding mechanisms crowding out private money |

Medium |

X |

|||

| Small project size raising origination and transaction costs |

Medium |

X |

|||

| Taxes, inheritance laws, Common Agricultural Policy (CAP) payments incentivise agriculture and/ or commercial forestry over nature restoration |

Medium |

X |

|||

| Money is not everything for some landowners, tenants and communities (e.g. crofters = lifestyle, estates = private interests) |

Low |

X |

|||

| Non-financial barriers |

Delivery risk and long-term maintenance obligations |

High |

X |

||

| Technical and ecological difficulties to restore peatland |

Low |

X |

|||

| Data gaps on peatland mapping and lack of transparency of delivery costs |

Medium |

X |

|||

| Capacity constraints across the supply chain |

High |

X |

X |

||

| Lack of education on the wider benefits of peatland restoration |

Medium |

X |

X |

||

| Concerns over land use changes and impacts on local livelihoods |

Medium |

X |

|||

| Perceived early mover disadvantage incentivises many landowners and tenants to wait until the peatland carbon market has matured. |

High |

X |

* Importance was estimated based on how often the barrier was mentioned during the stakeholder engagement.

Key takeaways

- There are significant barriers to achieving peatland restoration at scale. In particular, some stakeholder groups are reluctant to participate as a result of real or perceived barriers.

- Landowners remain to be convinced to scale up restoration beyond small pilot projects. They are mostly concerned about retaining optionality over the use of their lands, receiving fair remuneration for the carbon benefits generated, and limiting their exposure to the long-term liabilities associated with peatland restoration.

- Landowners perceived the SCF and PFG as useful to enable their participation in the peatland carbon market. However, they were cautious of the conditions associated with receiving financing from the SCF.

- Some estate owners are less responsive to financial incentives, especially where estates are managed for recreational activities (primarily deer hunting).

- Farmers and crofters have significant activities overlapping with areas eligible for peatland restoration. Obtaining buy-in from these communities is essential, however they currently remain to be convinced of the economic benefits of peatland restoration and are cautious of selling carbon that they might need to offset the emissions from their own activities.

- For investors, the lack of investment-ready pipeline is a major issue, which can be linked to limited peatland condition mapping data availability, the small size and fragmentation of the peatland eligible under the PC and the generous upfront capital grant funding available.

- Investors perceived the combination of the SCF with a first-loss contribution from the government and PFG as highly-attractive, and as a strong sign of commitment of the Scottish Government in the peatland carbon market.

- Although demand for peatland carbon credits remains difficult to assess, particularly over the long time horizons of the restoration projects, there is evidence of a robust near-term demand for Scottish peatland carbon and its co-benefits.

- The lack of clarity on current and future demand as well as price opacity in the carbon market limit the confidence of landowners and investors to participate in peatland restoration.

- Some of the barriers identified in the stakeholder engagement can be overcome by the SCF and PFG, but others will require different policy responses.

Contact

Email: peter.phillips@gov.scot