Mobilising private investment in natural capital: report

This report looks at how to encourage responsible private investment into peatland restoration, including how to overcome barriers to scaling voluntary carbon markets to restore peatland in Scotland.

Section 3: Overview of the financing mechanisms tested

This section provides a high-level overview of the two financial mechanisms that were tested through this action research project. These mechanisms could potentially be deployed independently, or in parallel. Recommendations on the proposed design and structure of these mechanisms are presented from section 5 onwards.

Scotland Carbon Fund

The purpose of the SCF would be to attract responsible private investment into eligible peatland restoration projects with repayments and returns to investors funded through revenues from the sale of carbon credits. By providing transparency, reducing transaction costs and attracting more investment into the sector, the fund would enable high quality peatland restoration to be undertaken at scale. Government leadership in the fund's creation and an initial cornerstone investment would in turn allow the Scottish Government to set a high bar for project quality and build market confidence.

Building on the learnings from the "Facilitating Local Natural Capital Investment" report, two possible fund functions were considered and tested: (1) a liquidity vehicle; and (2) a project finance vehicle.

Liquidity vehicle

As a market liquidity vehicle, the SCF would act as a guaranteed buyer of Pending Issuance Units (PIUs), holding onto these credits until they vest into verified Peatland Carbon Units (PCUs). Investor returns are generated by the increase in value of the credits over time as they are verified.

For project developers, this vehicle provides certainty that the PIUs generated through peatland restoration can be sold quickly at a transparent and guaranteed price, and also provides an option for an agreement with the fund to share in any upside in the long-term growth in the value of carbon credits. The facility would be both buying and selling credits in the market, thereby offering a "market maker" function helping to build liquidity and transparency for market actors.

Project finance vehicle

A more traditional project finance vehicle provides project developers with finance (e.g. in the form of a loan or equity injection into the project) to support the upfront capital costs of peatland restoration, bridging the time gap between project development and revenue generation. Investment returns are paid once PIUs vest into verified PCUs.

A project finance vehicle provides the upfront capital required to cover the restoration costs to enable project developers to retain PIUs until they vest into verified PCUs, thereby enabling income from carbon sales to be delivered over the lifetime of the restoration project. This distribution of carbon income ensures project developers have a steady supply of capital to meet long-term maintenance costs, which usually decline over time but still represent a significant long-term financial obligation, and reduces the risk of areas of peatland becoming a stranded asset, not generating any income for future generations.

In order to explore the suitability of the two possible fund functions, a number of questions on the potential design features were tested with key stakeholders through the research phase of the project (Table 4)

| Design feature |

Key question(s) |

|---|---|

| Fund function |

|

| Fund general characteristics |

|

| Investment mandate |

|

| Government contribution |

|

| Community benefits |

|

| Endowment |

|

| Governance |

|

Price Floor Guarantee

A PFG is a risk reduction or transfer mechanism. A PFG is well suited to early-stage markets in which demand is uncertain. Unlike the SCF, the PFG supports the underlying project by reducing revenue risk, rather than de-risking the investor directly. Price floors are used to accelerate market development by removing the risk that prices fall in the future through a guarantee to participants. This builds confidence in the cashflow generation of beneficiary projects, and in turn should improve economic viability / investability. Unlike a traditional form of subsidy support, the guarantor only pays out if market pricing falls below a pre-agreed threshold. In this way, the PFG can operate more efficiently than a traditional subsidy scheme.

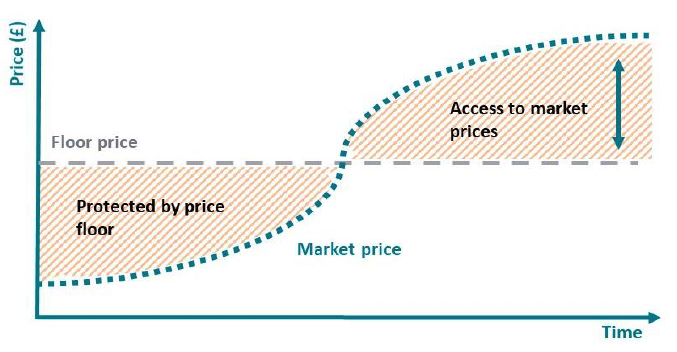

A PFG could be used by Scottish Government to de-risk investment in, and accelerate delivery of, peatland restoration. Future carbon pricing cannot be accurately predicted, and estimates vary widely. In this context, the price floor acts to remove the risk of most pessimistic outcomes ("downside") while still providing the opportunity for projects to benefit in upside scenarios. The market function of a guarantee mechanism is reflected in Figure 3 below:

As shown, beneficiary projects are protected from carbon pricing below the price floor, but are able to benefit from pricing in excess of the floor price. As a means of de-risking projects without crowding out private capital, price floor guarantees offer an interesting and cost-efficient alternative to existing subsidy regimes. The design of the guarantee can be flexible and strategic, allowing for the targeting of specific outcomes, for example by setting qualification criteria to access the price guarantee such as enhancements in biodiversity or community benefit. Table 5 provides an overview of the questions which were posed to stakeholders through the research phase of the project to elicit their views on what would be the most important design features.

| Design feature |

Key question(s) |

|---|---|

| Guarantee mechanism |

|

| Floor price setting |

|

| Eligibility and delineation |

|

| Scale and frequency |

|

| Duration |

|

| Indexation |

|

| Accounting and use of surpluses |

|

Contact

Email: peter.phillips@gov.scot