Making the Case for Nature: insights from Scotland's Natural Capital analyses

This report is an analytical review consolidating Scotland's Natural Capital evidence base. Synthesises over a decade of analyses to distil key insights to help inform better decision-making across government, business, and society.

Introduction

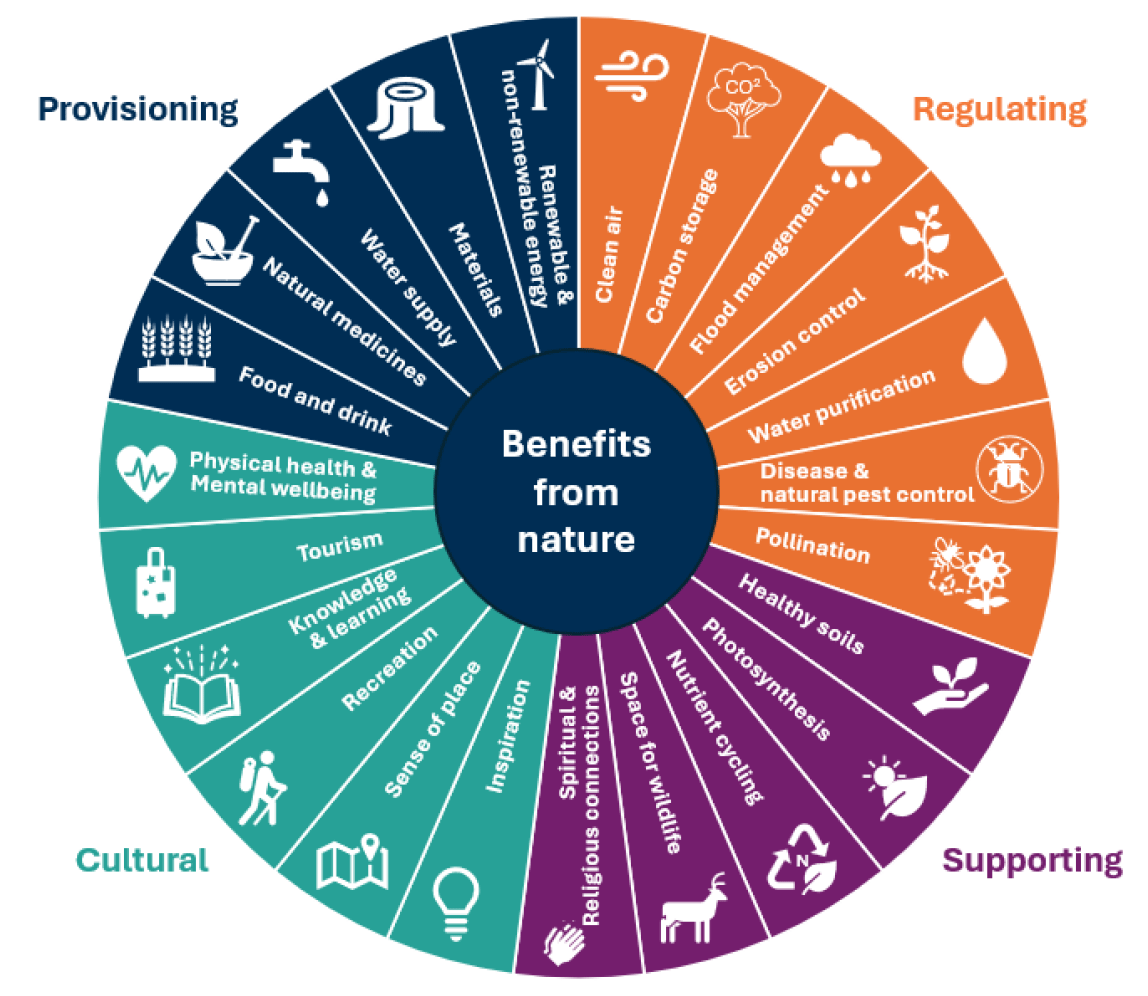

Scotland has a rich and diverse environment made up of mountains and moorlands that cover around 60% of our land, more than 30,000 freshwater lochs, native woodlands, such as Caledonian pinewoods, and large areas of farmland [1]. Scotland also includes around 800 islands and about 18,000 km of coastline. Marine habitats are made up of sea lochs, burrowed mud, kelp, and coral reef. These natural assets - natural capital - provide flows of services (ecosystem services), which deliver benefits to the economy and people. Examples of ecosystem services such as timber, carbon sequestration and recreation are shown in Figure 2. There is increasing recognition of the role of natural assets in addressing the twin nature degradation and climate change crises.

Graphic text below:

Benefits from nature

Provisioning:

- Food and drink

- Natural medicines

- Water supply

- Materials

- Renewable and non-renewable energy

Regulating:

- Clean air

- Carbon storage

- Flood management

- Erosion control

- Water purification

- Disease and natural pest control

- Pollination

Supporting:

- Healthy soils

- Photosynthesis

- Nutrient cycling

- Nursery habitats for wildlife

Cultural:

- Physical health and Mental wellbeing

- Tourism

- Knowledge and learning

- Recreation

- Sense of place

- Inspiration

- Spiritual experiences

- Religious connections

Natural capital is a key component of the Scottish Government’s ‘National Strategy for Economic Transformation’ [2] which embeds a Wellbeing Economy approach. The Wellbeing Economy approach sets out an economic system that serves the collective wellbeing of current and future generations within safe ecological limits. Figure 3 highlights that one of the key ambitions for the Scottish economy is rebuilding natural capital. As a key pillar of the Scottish Government’s approach to policy development and economic strategy, investing in nature is a top priority for delivering Scotland’s wellbeing economy.

Graphic text below:

A Wellbeing Economy: Thriving across economic, social and environmental dimensions. Ensuring that work pays for everyone through better wages and fair work, reducing poverty and improving life chances. Driving an increase in productivity by building an internationally competitive economy founded on entrepreneurship and innovation. Demonstrating global leadership in delivering a just transition to a net zero, nature-positive economy, and rebuilding natural capital.

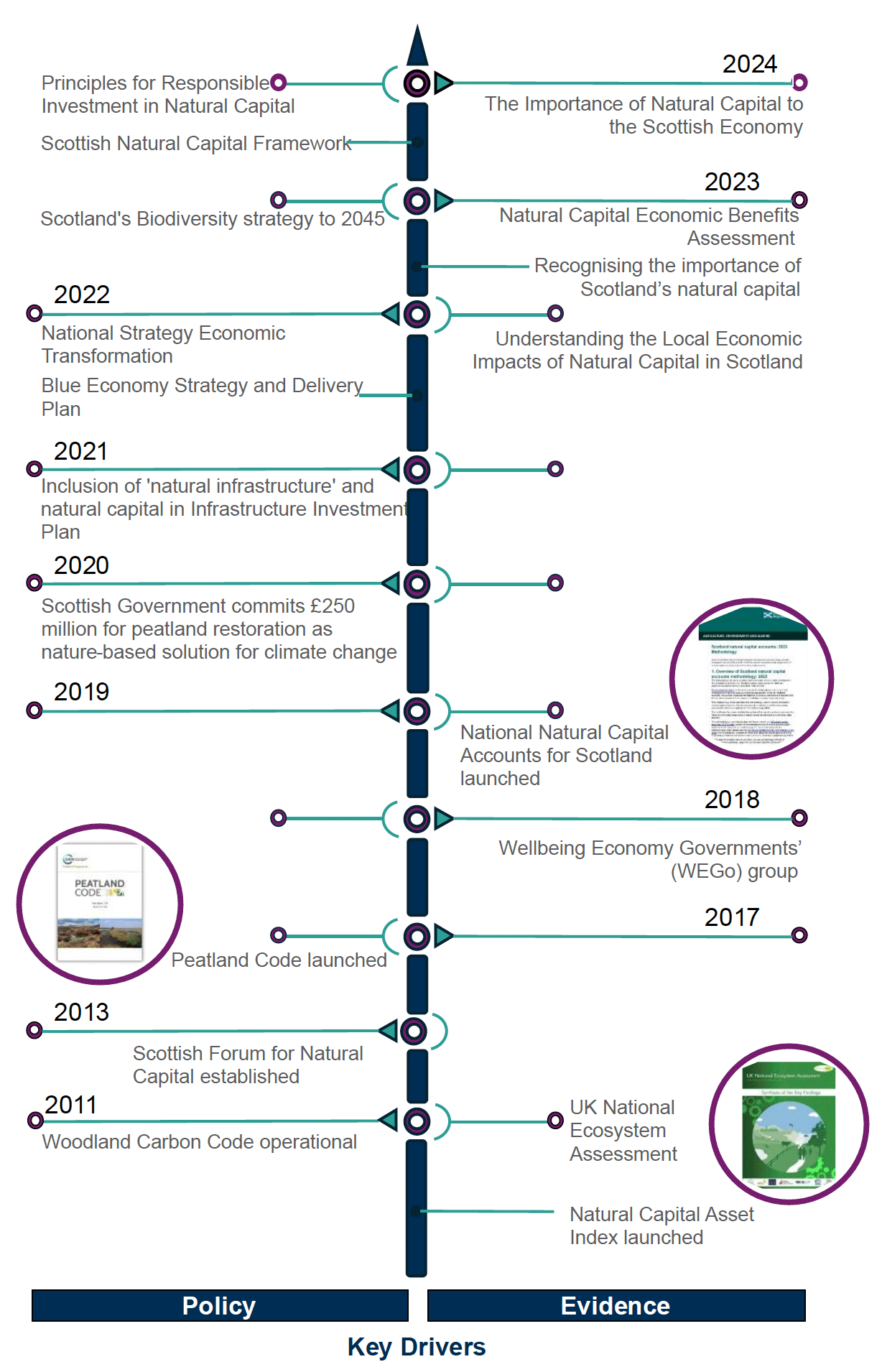

Scotland’s natural capital timeline

In 2008, the first analysis on the impact of sustainable use of Scotland’s natural environment and how it supports the economy was published in ‘The Economic Impact of Scotland’s Natural Environment’ [3]. Since the release of the UK ‘National Ecosystem Assessment’ [4] and the first edition of the Scottish ‘Natural Capital Asset Index’ (NCAI) [5], there has been a growing body of evidence on natural capital and its application to policy in Scotland. This includes the ‘National Natural Capital Accounts for Scotland’ [6] launched in 2019. These developments are outlined in Figure 4.

Internationally, the groundbreaking publication of ‘The Dasgupta Review’ [7] on the economics of biodiversity has highlighted our critical dependencies on nature and the case for action.

Since 2022, a number of key research reports and analysis on natural capital have been published by the Scottish Government such as ‘The Importance of Natural Capital to the Scottish Economy’ [8].

This makes it an opportune time to take stock of this evidence and draw out key insights from Scotland’s natural capital analysis. The purpose of this work is not to develop new analysis but instead to set out and clearly communicate the key messages and implications of the natural capital evidence to a range of stakeholders.

Graphic text below:

In 2011, the UK National Ecosystem Assessment was published, the Natural Capital Asset Index was launched, and the Woodland Carbon Code became operational. In 2013, the Scottish Forum for Natural Capital was established, followed by the launch of the Peatland Code in 2017. Scotland joined the Wellbeing Economy Governments’ (WEGo) group in 2018, and in 2019, the National Natural Capital Accounts for Scotland were introduced. In 2020, the Scottish Government committed £250 million to peatland restoration as a nature-based solution to climate change. The 2021 Infrastructure Investment Plan included references to 'natural infrastructure' and natural capital. In 2022, several strategic initiatives were introduced, including the National Strategy for Economic Transformation, the Blue Economy Strategy and Delivery Plan, and a study on the local economic impacts of natural capital. In 2023, the Natural Capital Economic Benefits Assessment was conducted, reinforcing the importance of Scotland’s natural capital and Scotland’s Biodiversity Strategy to 2045 was published. In 2024, the Importance of Natural Capital to the Scottish Economy, the Principles for Responsible Investment in Natural Capital, and the Scottish Natural Capital Framework were all published.

Contact

Email: Georgia-Lee.Smith@gov.scot