Scottish Income Tax: 2018-19 policy evaluation

A policy evaluation of Scottish Income Tax in 2018-19

7. Economic growth test

Economic growth test - changes in Income Tax policy, and the accompanying change in public spending, must support the economy.

This section sets out analysis on our understanding of the macroeconomic impact of Income Tax policy. Given the uncertainty inherent in modelling and forecasting the economy as a whole, these results are necessarily more uncertain than the analysis of impacts on individuals and households above.

7.1 Key findings

- Our modelling indicates that the 2018-19 Income Tax policy, alongside additional government spending as a result of the policy change, had a relatively negligible impact on the size and growth rate of the economy in the short-term.

- This impact was anticipated at the time of setting the 2018-19 Draft Budget, where it was concluded that the economic impacts of the tax rise would be relatively small.

- These results are consistent with the SFC's views, stated in their December 2017 forecast, that the policies announced at Draft Budget 2018-19 were not expected to have a significant impact on the economy over the five-year forecast period.

- This analysis only considers the short-term static impact of the change in Scottish Government fiscal policy. In the long-run, higher tax rates and higher government expenditure may also influence economic growth through a variety of other channels and these longer term considerations could form part of future studies.

7.2 Impacts on economic growth

This section sets out the methodology used to assess to what extent the 2018-19 policy met the economic growth test, and aims to evidence whether the reform impacted economic growth, positively or negatively.

Evaluating the impact of a change in tax policy on economic growth can be challenging as it is often difficult to isolate the direct or indirect effects of a specific tax policy change on economic activity relative to the many other factors that can influence an economy over time, many of which are outside of the Scottish Government's control. For example, firms' and households' decisions can be affected by changes in: monetary policy; how quickly prices or wages in the economy are rising; or even how confident businesses and consumers are feeling at any given time.

In the short term, the policy increased the average level of Income Tax in the Scottish economy. In isolation, we would generally expect this to decrease the spending power of households or individuals affected. This could, in turn, reduce the demand from in the Scottish economy.

However, this effect could be countered by the fact that the revenue raised from the policy was used to fund higher government spending. In general, higher government spending would generally be expected to increase economic activity in the short run, though the size of the effect will depend on the type of government spending that is increased. Consequently any increase in government spending could potentially offset the negative impact of higher taxation on economic activity.

Overall, due to the relatively small size of the tax change (the revenue the tax policy is estimated to be worth only around 0.2% of GDP in 2018-19 prices) and the associated government spending increase, we would expect the net short-run impact of this policy change on the economy to be relatively small. While we would expect the impact of the tax increase in isolation to be negative, when it is combined with the associated increase in government spending the net impact could feasibly be positive, negative, or zero depending on which factor outweighs the other.

Quantifying this net impact can be challenging, especially as macroeconomic performance often varies year-on-year. Table 8 below shows that 2018-19 was generally one of the stronger years recently for the Scottish economy, in terms of GDP growth, earnings growth and unemployment. This performance was driven by factors in the Scottish, UK and global economies that are likely far larger in impact than the relatively small change in Income Tax policy and government spending. While it is possible that the policy change may have affected economic growth in 2018-19, separating that impact from a host of wider changes would be very challenging.

| 2014-15 |

2015-16 |

2016-17 |

2017-18 |

2018-19 |

2019-20 |

2020-21 |

|---|---|---|---|---|---|---|

| GDP Growth (%) |

||||||

| 2.0% |

0.1% |

1.0% |

0.9% |

1.2% |

-0.3%* |

-10.3% |

| Unemployment Rate (%) |

||||||

| 5.9% |

5.9% |

4.8% |

4.1% |

3.7% |

3.8% |

4.5% |

| Average Earnings Growth (%) |

||||||

| N/A** |

-0.4% |

1.6% |

2.2% |

6.2% |

-0.3% |

3.9% |

| House Price Growth (%) |

||||||

| 5.6% |

2.1% |

1.6% |

4.3% |

3.3% |

1.7% |

4.7% |

Source: Scot Govt; UK Govt; ONS

* 2019-20 growth is partially affected by including 2020 Q1 and the early impacts of COVID-19. The Annual growth rate for 2019 as a calendar year was 0.7%

** RTI Earnings data only goes back to July 2014 and hence can't be used to construct an annual growth rate for 2014-15

Scenario Analysis

Using an economic model to estimate the broad magnitude of the impact of a tax change provides useful insight as to the relative importance of the different ways a tax change might affect economic activity.

This modelling only looks at the short-term direct or static effect of the policy change. In the long-run, higher tax rates and correspondingly higher government expenditure may also influence economic growth through a variety of other channels, such as affecting individuals' and firms' decisions around: saving; investing; spending; and how many hours to work; or whether to start or expand a business.

These longer-term dynamic impacts on growth could be positive or negative, and the economic literature on this topic is inconclusive. These long-term impacts are, by definition, also very challenging to identify with a relatively recent policy change. For these reasons, we focus only on the short-term impacts of the policy change on economic growth.

To estimate the impact of the tax policy changes we have used the Scottish Government's Global Econometric Model (SGGEM). SGGEM is a modified version of the National Institute of Economic and Social Research's (NIESR) Global Macroeconomic Model NiGEM, which is an internationally recognised macroeconomic model, used by institutions such as the OECD, European Central Bank and the Bank of England. It is well suited to examining the macroeconomic impact of various scenarios, including changes in direct tax rates. It has been calibrated by NIESR to Scottish data to reflect the observed behaviour of the Scottish economy.

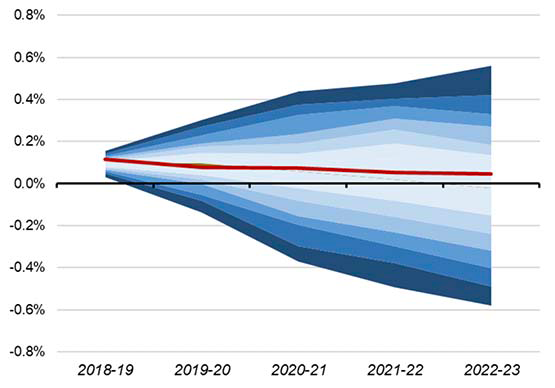

Chart 11 below shows the estimated impact on the level of GDP from an increase in both tax revenue and government spending each equivalent to around 0.2% of GDP. Full details of the approach and scenario analysis can be found in Annex A.

Source: Scottish Government Global Econometric Model (SGGEM)

The red line indicates the central estimate from the model, which shows a small positive impact of the policy change over time. This results in the size of the Scottish economy being around 0.05% larger by 2022-23. However, modelling of this type is highly uncertain, and for comparison we show a confidence interval (the blue bands). These show the area in which we would expect the outcome to fall about 70% of the time when further sensitivity analysis is undertaken (see Annex A for more details). This shows a broad range of possible outcomes, and importantly includes both positive and negative impacts on economic activity. This is consistent with our expectations that the net impact of the policy would be small, and could feasibly be either above or below zero.

These conclusions are also consistent with the SFC's views stated in their December 2017 forecasts:

"The policies announced at Draft Budget 2018-19 are not expected to have a significant impact on the economy over the five-year forecast period."

" … the Commission's judgement is that these policies are not of a large enough magnitude to have a significant aggregate impact on the Scottish economy, in particular with respect to our forecasts of earnings and employment. While they may have some impact on household consumption and business investment through their impact on taxes, this will be offset in part by changes to Scottish Government expenditure."

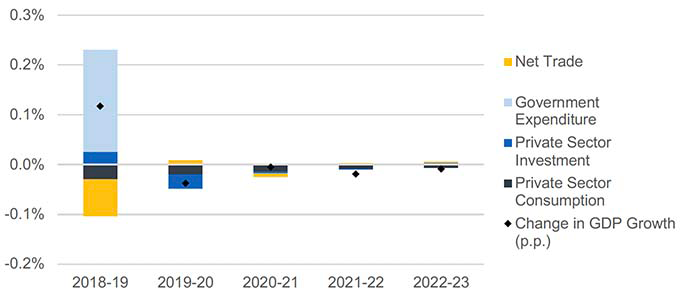

Another key finding is that the short-term static impact only affects the level of GDP. As can be seen in chart 12 below, the growth rate of the economy is slightly faster than it otherwise would have been in 2018-19 as the economy adjusts to a higher level, but then eventually returns to its original path.

Source: Scottish Government Global Econometric Model (SGGEM)

Consequently, although the size of the economy may have changed, there is no persistent impact on the growth rate of the economy.

However these estimates of the impact on economic growth are not definitive, and are the results from only one model. Other economic models might generate different results, or show different impacts with the benefit of more data over a longer time horizon.

Overall, though, the short-term static modelling suggests that the net impact of the tax policy change is likely to be relatively small. The central estimate is for the size of the Scottish economy to be around 0.05% larger by 2022-23, with no persistent impact on annual economic growth rates.

Contact

Email: martin.davidson@gov.scot