Scottish Income Tax: 2018-19 policy evaluation

A policy evaluation of Scottish Income Tax in 2018-19

Annex A: Scenario Analysis

Evaluating the impact of a change in tax policy on economic growth can be challenging as it is often difficult to isolate the direct or indirect effects of a specific tax policy change on economic activity relative to the many other factors that can influence an economy over time.

One solution to this problem is to use economic models to help examine some of the channels through which a tax policy change may influence the economy and in helping assess or quantify the broad magnitude of the impact that a change in fiscal policy may have.

To do so, we use the Scottish Government's Global Econometric Model (SGGEM) to perform some scenario analysis on how a change in tax policy could affect the Scottish economy. SGGEM is an economic model that was commissioned from the National Institute of Economic and Social Research (NIESR) and one of its strengths is that it is a modified version (splitting the UK into Scotland and the rUK) of NIESR's own Global Macroeconomic Model NiGEM[40], which is an internationally recognised and scrutinised macroeconomic mode which has been used by institutions such as the OECD, European Central Bank and the Bank of England. Consequently, the model is a robust general equilibrium model that is well suited to examining the macro economic impact of various scenarios, including changes in direct tax rates and government spending.

However, this scenario analysis only looks at the short-term / static effects of the policy change. In the long-run, higher tax rates and higher government expenditure may also influence economic growth via other channels, such as affecting people's decisions to save, spend, work, or start a business.

The impacts on growth could be positive or negative, and the economic literature on this topic is not conclusive. These long-term impacts are, by definition, also going to be very challenging to identify with a relatively recent policy change. For these reasons, we focus only on the short-term / static and/or direct impacts of the policy change on economic growth.

Methodology

The 2018-19 tax policy has been estimated to increase Scottish NSND Income Tax Revenue by around £200m to £300m - equivalent to roughly 0.2% of Scottish GDP in 2018-19. This estimate can then be used to calibrate two assumptions used in the scenario analysis. First, to calibrate a change to the "direct tax rate" within SGGEM which is a proxy for taxes applied to individuals (for example real personal disposable income in the model is a function of personal income minus direct taxes). A tax rate increase is then calibrated which increases overall direct tax revenue by 0.2% of GDP in the model. Second, to calibrate a change to government expenditure in the model which assumes any increased tax revenue is spent with the resultant increase in government expenditure equal to 0.2% of GDP within the model.

Any shock is assumed to be permanent across the scenario horizon beginning in 2018 Q2 and it is assumed that consumers and firms are forward looking and have rational expectations. It is also assumed that interest rates in the UK as a whole are unchanged and that monetary policy is exogenous within the scenario.

Results

Chart 13 below shows the impact on the level of real GDP from a direct tax rate revenue increase worth 0.2% of GDP that is also accompanied by an equivalent sized expansion of government expenditure. The immediate impact is estimated to increase the level of GDP by around 0.1% in the short-term and by around 0.05% by 2022-23.

Source: Scottish Government Global Econometric Model (SGGEM)

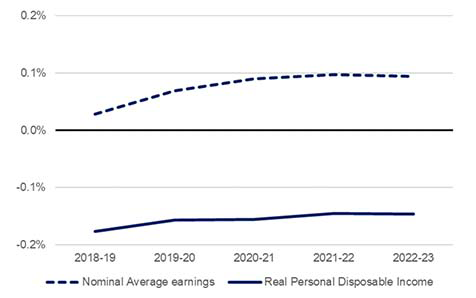

The increase in direct taxation has a negative effect on real personal disposable income as post-tax earnings falls. However this is partly mitigated by the small increase in nominal average earnings as a result of the overall positive increase in activity in the economy.

Source: Scottish Government Global Econometric Model (SGGEM)

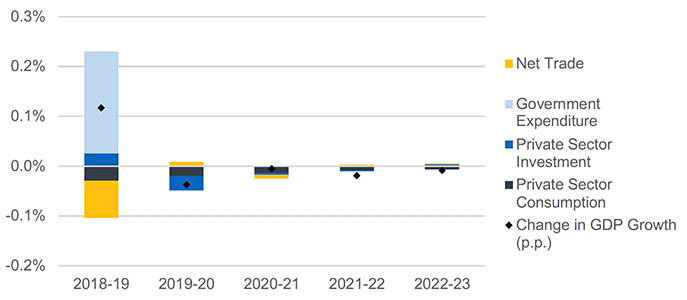

As a result of the lower levels of real disposable income, aggregate private sector consumption (which accounts for around two thirds of economic activity) is smaller than otherwise would have been the case. The increase in government spending is estimated to offset the negative impact on economic growth from the fall in private sector consumption. However, as a result of the stimulus generated from additional government expenditure, there is also a corresponding rise in demand for goods and services across the economy (some of which is imported). Consequently, net trade deteriorates acting as an additional drag on the economy, as imports are estimated to rise whilst exports remain relatively unchanged. This then partially offsets some of the positive GDP impact of higher government spending, although the net impact is still positive.

Source: Scottish Government Global Econometric Model (SGGEM)

Sensitivity Analysis

As mentioned this scenario only consider the direct impacts of a tax and government expenditure change. SGGEM is a dynamic general equilibrium model and does automatically account for some indirect impacts from higher taxes and government expenditure (such as changing prices) but there are parts of the model structure that does not automatically or endogenously incorporate additional indirect impacts that may occur.

For example, labour productivity in the model is exogenous - the model does not automatically make any assumption about how changes in taxation or government expenditure may affect it. If there are arguments that higher or lower taxes or government expenditure could have a long-term impact on labour productivity, then this would have to be incorporated directly as an additional productivity assumption into the scenario analysis.

Second, there are a wide variety of estimates around the relationship between different economic variables. For example, a 1% increase in government spending may be estimated to increase GDP by a certain percentage on average over time. However, these estimates are not always unconditional – they can often be sensitive towards the type of government expenditure being undertaken such as day-to-day spending on the NHS relative to the economic impact of investing in a new railway. They are also often specific to the state of the current economy. So for example, every additional £1 of government expenditure spent, or every £1 less paid in tax during a recession could have a different effect on the economy (when there may be higher levels of unemployment, and lower levels of demand for goods and services) than during a period of strong economic growth when demand is already high.

To address some of these concerns some additional sensitivity analysis is undertaken. The process involves looking at how the key equations in the model have performed in explaining historical data and using a "bootstrap" approach to take random draws from the values these equations would predict over time relative to actual historic outturn data to create a stochastic database of residuals for these key equations. These can be thought of as measurements of uncertainty in how the model has done in actually explaining how the economy has performed historically.

This stochastic database can then be used to generate hundreds of additional scenarios where random stochastic shocks are introduced to some of the key equations over time. In particular a subset of core equations are selected that were deemed to likely be sensitive to fiscal policy changes, such as the level of employment, average number of hours worked per employee, nominal wages and other personal income. This can then help compensate for some of the uncertainties and caveats of the central scenario analysis.

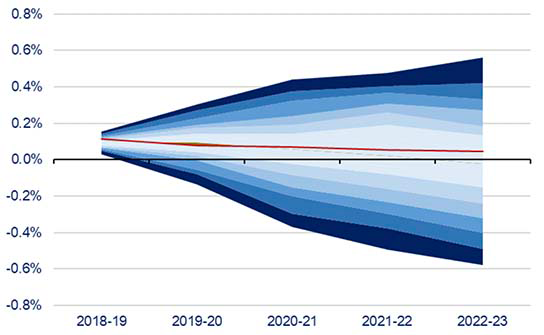

Chart 16 below shows the central estimate of the scenario analysis accompanied by a confidence interval generated from the 250 additional sensitivity scenarios. There was evidence that around 70% of the additional scenarios that included the stochastic uncertainty shocks over time resulted in an economy between 0.6% larger to around -0.6% lower by 2022-23.

Source: Scottish Government Global Econometric Model (SGGEM)

To some degree these sensitivity results are arbitrary and are not directly associated with some of the specific modelling uncertainties to do with fiscal policy changes. However, they do help measure the historical performance of the model in explaining real outturn data and hence are useful to give a degree of sensitivity to the core estimate.

Conclusion

Overall, there is evidence from the scenario analysis that, primarily due to the relatively small size of the tax and government expenditure change from the 2018-19 tax policy, any direct / static impact on the short-term size of the economy is also likely to be relatively small. Our central estimate is that a tax rise accompanied by an equal sized increase in government expenditure will have a small positive impact on the size of the economy, although the sensitivity analysis suggests that the confidence intervals around this estimate are quite wide and do not exclude the possibility of a negative impact.

However, the central estimate and the sensitivity analysis does provide some evidence that the overall impact on the short-term size of the economy is not likely to be substantial.

These conclusions are also consistent with the SFC's views stated in their December 2017 forecasts:

"The policies announced at Draft Budget 2018-19 are not expected to have a significant impact on the economy over the five-year forecast period."

"… the Commission's judgement is that these policies are not of a large enough magnitude to have a significant aggregate impact on the Scottish economy, in particular with respect to our forecasts of earnings and employment. While they may have some impact on household consumption and business investment through their impact on taxes, this will be offset in part by changes to Scottish Government expenditure."

These estimates of the impact on economic growth are not definitive, and are the results of one model. Other economic models might generate different results, or show different impacts with the benefit of more data over a longer time horizon.

Contact

Email: martin.davidson@gov.scot