Scottish Income Tax: 2018-19 policy evaluation

A policy evaluation of Scottish Income Tax in 2018-19

3. Policy context

The Scottish Budget was historically funded exclusively via a Block Grant from the UK Government. This meant that a budget, which was set by the UK Government and Parliament based on spending decisions for England and Wales, was transferred as revenue to the Scottish Parliament, which could then decide how to allocate those funds at the Scottish Budget.

The Scotland Act 2012 gave the Scottish Parliament the power to set a Scottish Rate of Income Tax. Since 2017-18, and following the further devolution of the current Income Tax powers in the Scotland Act 2016, the Scottish Parliament has had the power to set the rates and bands that apply to non-savings non-dividend Income Tax for Scottish taxpayers (i.e. income from employment, self-employment, pensions and property). The other elements of the Income Tax system, including savings and dividend income, reliefs/exemptions and setting the tax-free Personal Allowance, remain reserved to the UK Government. HMRC also collects and administers Scottish Income Tax on behalf of the Scottish Government.

Scottish Income Tax receipts are around £12 billion annually, accounting for roughly 30% of the overall Scottish Budget. The Scottish Parliament has to pass a Scottish Rate Resolution each year to set the rates and bands that will apply to the income of Scottish taxpayers in the following tax year. This means that decisions made in the Scottish Parliament now have greater influence over the size of the Scottish Budget.

3.1 Fiscal Framework

The Fiscal Framework was introduced alongside the Scotland Act 2016 to determine how the Scottish Budget should be funded following the devolution of further powers over taxation and social security.

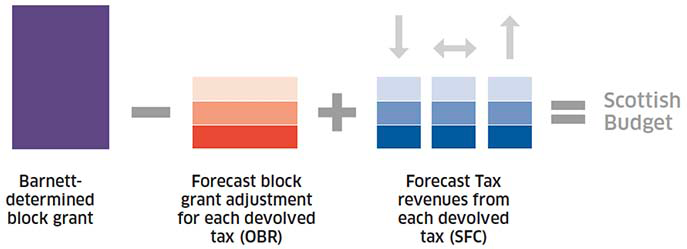

The Scottish Block Grant continues to be calculated by the Barnett formula, but an adjustment is made to reflect the fact that some of the budget is now funded by Scottish tax revenues that were previously retained by the UK Government (known as the Block Grant Adjustment (BGA)). The revenues from devolved taxes are then added back in to determine the net position for the Scottish Budget, see Figure 1.

As a result, the net impact of Scottish Income Tax on the Scottish Budget depends on the forecasts of UK tax revenues produced by the Office for Budget Responsibility (OBR), which are used to calculate the BGAs; and the forecasts of tax revenues raised in Scotland, produced by the Scottish Fiscal Commission (SFC).

The overall impact on the Scottish Budget depends on the performance of Income Tax receipts in Scotland relative to the rUK[3]. If the Scottish Government is able to grow its receipts per head faster than in the rUK, the net budgetary effect will be positive, and vice versa. This outcome is heavily influenced by changes in tax policy; economic performance; differences in the composition of the tax base; and differences in the sectorial composition of the two economies.

Inevitably, the SFC and OBR forecasts will not exactly match the amounts actually raised in Scotland or the rUK. Therefore, when outturn data is published, an adjustment (known as a reconciliation) is applied to the next Scottish Government Budget to account for the differences in the forecasts[4]. Reconciliations are a normal part of the Fiscal Framework for all taxes and should not be confused with how tax receipts are performing.

Further information can be found in the Fiscal Framework: factsheet[5].

3.2 2018-19 Scottish Budget

The 2018-19 was the second year that the Scottish Government was able to set out its Income Tax policy using the new powers provided by the Scotland Act 2016. In the first year (2017-18), there was a small divergence between the Scottish and UK Income Tax systems, when the Higher Rate threshold in Scotland was frozen at £43,000.

In advance of the 2018-19 Scottish Budget, the Scottish Government published the discussion document The role of Income Tax in Scotland's budget[6]. The document set out four key tests against which the Scottish Government believed that any future tax changes should be judged, and applied these tests to a range of scenarios, including the Income Tax proposals that the parties represented in the Scottish Parliament had in their 2016 election manifestos. The purpose of the discussion document was to inform and encourage a more open debate across Scotland on how Income Tax powers could be used.

At the 2018-19 Draft Budget presented on 14 December 2017, the then Cabinet Secretary for Finance and the Constitution announced significant reforms to Scottish Income Tax, with 1p added to the Higher and Top Rates, and the addition of two new bands to split the previous Scottish Basic Rate band. As set out in the 2018‑19 Draft Budget documentation[7], these reforms were judged to best meet the four key tests as set out in the discussion document, making the system more progressive, raising additional revenue for public services, whilst supporting Scotland's economy.

The following rates and bands were agreed to by the Scottish Parliament on 20 February 2018:

| Band | Band name | Rate |

|---|---|---|

| Over £11,850* to £13,850 | Starter rate | 19% |

| Over £13,850 to £24,000 | Basic rate | 20% |

| Over £24,000 to £43,430 | Intermediate rate | 21% |

| Over £43,430 to £150,000 | Higher rate | 41% |

| Over £150,000 | Top rate | 46% |

* The Personal Allowance is set by the UK Government

This compares to the three tax rates and bands in force in the rest of the UK in 2018-19:

| Band | Band name | Rate |

|---|---|---|

| Over £11,850 to £45,000 | Basic rate | 20% |

| Over £46,350 to £150,000 | Higher rate | 40% |

| Over £150,000 | Additional rate | 45% |

And to the three tax rates and bands for Scottish and UK Income Tax in 2017-18:

| Band | Band name | Rate |

|---|---|---|

| Over £11,500 to £43,000 | Basic rate | 20% |

| Over £43,000 to £150,000 | Higher rate | 40% |

| Over £150,000 | Additional rate | 45% |

| Band | Band name | Rate |

|---|---|---|

| Over £11,500 to £45,000 | Basic rate | 20% |

| Over £45,000 to £150,000 | Higher rate | 40% |

| Over £150,000 | Additional rate | 45% |

Contact

Email: martin.davidson@gov.scot