The Scottish Government's Medium Term Financial Strategy

This is the fourth Medium Term Financial Strategy (MTFS) published by the Scottish Government. The MTFS provides the context for the Scottish Budget and the Scottish Parliament.

4. Managing Fiscal Risks

This chapter brings together the funding and spending scenarios and discusses the different sources of fiscal risk that need to be managed, as well as our ability to manage those risks with the available fiscal tools - namely the Scotland Reserve and resource and capital borrowing powers.

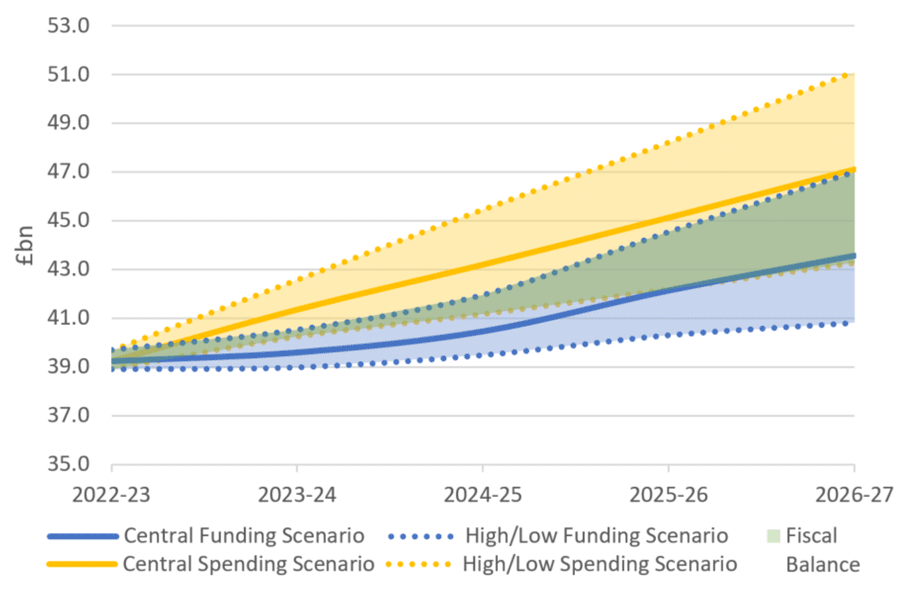

Figure 6 below shows how the funding and spending scenarios compare. As with last year's document, the funding scenarios are from section 2.1 based on the SFC forecasts and the information we have from the UK Government about projected levels of spend at UK level and the shape of the block grant. This year, rather than being based on percentage increases, the illustrative spending scenarios were developed to support the upcoming Resource Spending Review Framework consultation. They therefore reflect a more detailed understanding of spending pressures in the medium term, including new commitments. In reality, we know that public spending will mirror the funding forecasts set out in the MTFS, unless there are significant changes to the Fiscal Framework or our tax measures.

The drivers of public spending identified in chapter 3 illustrate the variable and growing demands on public funding over the spending review period. If we compare our central funding forecast with our mid spending projection, this suggests a growing gap which reaches approximately £3.5 billion in 2026-27. At the extremes, the low funding compared with the high spending trajectory opens an estimated gap of approximately £10.3 billion in 2026-27, while a high funding combined with a low spending trajectory gives a £3.7 billion surplus.

These are not forecasts, and the wide range demonstrates the inherent uncertainties. However, they illustrate the need for a robust Resource Spending Review to help us make informed decisions about how we best use the funding available to meet the evolving needs of the population.

With limited resources, increased investment in the Scottish Government's priorities will require efficiencies and reductions in spending elsewhere: we need to review long-standing decisions and encourage reform to ensure that our available funding is delivering effectively for the people of Scotland. The Resource Spending Review will, through evidence and consultation, develop four-year spending plans with the aim of managing the financial risks we face and maximising the impact of our available funding.

4.1 Short, medium and long-term fiscal risks

The Scottish Government operates within a tight Fiscal Framework, with limited fiscal powers and levers.

On the funding side, the Scottish Budget is subject to volatility from in-year consequentials, arising from UK spending decisions. It also experiences volatility as a result of forecast error relating to devolved tax receipts, and the Block Grant Adjustments for devolved tax receipts and social security spending.

On the spending side, under or overspending on budgets is a risk that requires constant management. In particular, demand-led social security spending is a source of substantial uncertainty, where actual spending can diverge from forecasts, in response to contingencies occurring in real time. The Scottish Government's financial management needs to be agile to respond to this volatility, using the limited budget management tools available to us.

Our ability to manage the short and medium to long-term risks across Scottish Government funding and spending can often be constrained by the limitations on our budget management tools. Table 8 and Table 9 set out some of these risks in more detail as well as the potential mitigation strategies and some of the limitations the Scottish Government currently faces.

Table 8: Summary of key short-term risks to fiscal sustainability

Risk: UKG spending decisions

Mitigation

In both 2020 and 2021, the UK Government held its Budget close to the start of the next financial year. As a result, the Scottish Government had to undertake its Budget without clarity on UK Government tax policy and using provisional BGAs. That is not the case this year, so there is greater clarity on the funding envelope for the Scottish Budget (though it remains a risk for future years).

However, there remains a continued risk of the Scottish Budget having to manage significant in-year changes, resulting from UK Government decisions to increase or decrease spending.

While there is potential for in-year changes in any budget year, COVID-19 increases this risk at present. To date, however, the UK Government has not agreed to requests for further measures to support the management of such volatility, for example, by extending the previous Barnett guarantee, or automatic flexibility to carry over funds received late in the financial year, beyond the limitations of the Scotland Reserve.

Without additional powers, the Scottish Government can use draw-downs and carry-forwards through the Scotland Reserve as well as reprioritising spending to manage this risk. However, it cannot use resource borrowing and the limits on the available powers are so restrictive that it is impossible to guarantee the ability to fully control for unpredicted UK spending decisions.

Risk: Forecast "error"

Mitigation

All forecasts are inevitably subject to error and the Scottish Budget is therefore exposed to volatility when devolved tax revenue and social security expenditure turn out to be different from their original forecasts.

The Scottish Government can, subject to given limits, use resource borrowing and the Scotland Reserve to manage any negative reconciliation repayments that occur as a result of forecast error. However, historical reconciliations have already exceeded the annual £300 million borrowing limit to deal with forecast error, and this is likely to occur more regularly in the future as the current borrowing and reserve powers are not protected in real terms.

Risk: In-year revenue volatility caused by asymmetrical economic performance between Scotland and the rUK

Mitigation

A significant part of the Scottish Budget is now funded via devolved tax revenue and is therefore, directly exposed to the performance of the Scottish economy.

The Fiscal Framework does protect the Scottish Budget from symmetrical economic shocks that affect both the Scottish and rUK economies to a similar degree. For example, any change to tax revenues should be offset by a broadly equal change in the corresponding Block Grant Adjustment, leaving the Scottish Budget no better or worse off.

However, the Scottish Budget is not protected from asymmetric economic risk where the Scottish economy is affected to a greater or lesser degree than the rUK, such as due to sectoral composition differences between both economies.

The Scottish Government can, subject to given limits, use resource borrowing (for any forecast error caused by an asymmetric shock) and / or the Scotland Reserve to manage any direct impact on the net position, however due to the limits and restrictions on these powers reprioritising spending is likely to be required to manage this risk.

Table 9: Summary of key medium- to long-term risks to fiscal sustainability

Risk: Reduction in Block Grant growth caused by UK spending decisions

A key downside risk to the Scottish Budget over the medium-term

Mitigation

Given the current funding arrangements, affordability of spending over the medium-term is largely driven by UK Government decisions and spending.

This was illustrated by previous UK Government decisions on austerity prior to the pandemic, where the resource block grant given to the Scottish Government by the UK Government in 2019-20 was over £1.2 billion lower in real terms than in 2010 -11.

The Scottish Government has the option to take different decisions on devolved taxes to keep the Scottish fiscal position in balance, but these powers remain limited. Similarly, it can make use of its limited reserve and capital borrowing powers to smooth the budget trajectory. However, such action limits the ability to use these instruments for in-year volatility management.

While this risk has been reduced somewhat by the publication of a 3-year UK Spending Review, residual risk remains a challenge for the Scottish Government to manage, given we have no guarantee of the consequentials we will receive.

Risk: Changes to the Block Grant Adjustments

Mitigation

The Block Grant Adjustments applied to the Scottish Government budget are currently calculated using the Indexed Per Capita (IPC) method which fully protects the Scottish Budget from slower overall population growth. However, the IPC method does not protect from demographic changes such as changing labour force participation rates or an ageing population. Many key levers to address demographic risk, including migration policy, remain reserved to the UK Government.

In line with the Fiscal Framework Agreement, the BGA arrangements will be reviewed as part of the forthcoming Fiscal Framework Review and no default method will be assumed. Alongside consideration of other methods for adjusting the block grant, such as the Comparable Method, which does not fully protect the Scottish Budget from slower population growth, wider risks such as demographic changes should also be considered in that review.

Risk: Fundamental changes to the operation of finance in devolved policy making as a result of the UK Internal Market Act

The UK Government's use of these powers may also result in reduced funding for the Scottish Budget, blurs accountability and risks poor targeting of spend

Mitigation

The Scottish Government remains fundamentally opposed to the introduction of financial assistance powers as part of the Internal Market Act, and their ongoing use by the UK Government.

The Internal Market Act was imposed without the consent of the Scottish Parliament and undermines the devolution settlement by allowing UK Ministers to spend directly on a wide range of devolved matters - therein bypassing parliamentary scrutiny and accountability at Holyrood.

We will continue to press the UK Government to clarify how it intends to use the powers of the Internal Market Act and how it will engage Devolved Administrations to reduce the risk of duplicating or poorly targeting spend.

Risk: Structural differences in UK and Scottish economic performance

Scotland's exposure to global commodity markets, in particular the oil price, is relatively greater and there are differences in the sectoral composition of the Scottish and UK economies

Mitigation

Our economic policies are the key long-term mitigation to ensure prosperity and tax revenue growth.

For example, our forthcoming 10-Year National Strategy for Economic Transformation will build on the COVID Recovery Strategy to create a greener, fairer and more inclusive wellbeing economy. At its heart will be policies to stimulate business growth by investing in innovation, expanding opportunities internationally and supporting businesses to benefit from the transformational opportunities of digitalisation.

However, the different sectoral composition of the Scottish and rUK economies could pose a risk in the medium-term (for example, see Annex B of the January 2021 MTFS, which discusses this risk in greater detail)[11].

Risk: Compositional differences in UK and Scottish tax base

Differences in the composition of the tax base can pose a risk to the Budget.

Mitigation

As discussed in detail in Annex A, differences in the composition of the tax base between Scotland and the rUK can pose a risk to the Budget if earnings growth is unequal across the income distribution.

This includes an illustration of how such a risk could be mitigated via an alternative Block Grant Adjustment mechanism which should be reviewed as part of the Fiscal Framework Review in 2022.

Risk: Pay agreements are a key driver of public sector costs and spending

Mitigation

The Scottish Government's pay and reward policies aim to balance fairness and affordability, informed by dialogue with trade unions, alongside workforce planning that focuses on delivering governmental priorities.

Risk: Demand pressures caused by an ageing population

The fiscal pressures of an ageing population are most apparent in our health and social care system

Mitigation

We have committed to maintaining funding growth for health and social care at comparatively high levels. Nonetheless, we need to maximise the opportunities to mitigate the fiscal pressures.

Managing demands on the health system through public health improvement and prevention is a key element not only in improving people's health for better outcomes but also in managing the financial risks of health demand pressures.

We continue to shift the balance of care towards mental health, and to primary, community and social care. We know that in many circumstances outcomes improve and fewer interventions are required when care is delivered in a community setting.

4.2 Current levers for managing volatility and risk

The Fiscal Framework provides the Scottish Government with limited reserve and borrowing powers.

The Scotland Reserve allows the Scottish Government to smooth spending within and between years, carry forward underspend and assist in the management of tax volatility. Within its normal limits, the Scotland Reserve is capped in aggregate at £700 million, with an annual drawdown limit of £250 million for resource and £100 million for capital. However, the triggering of the 'Scotland-specific economic shock' provision in 2021-22, largely as a result of timing differences between the OBR's November 2020 and the SFC's January 2021 forecasts[12], means that there is no drawdown limit for the Reserve in 2021-22 through to 2023-24.

The Scottish Government can borrow to support day-to-day (resource) spending only in very specific circumstances, primarily to address forecast error in relation to devolved tax receipts and social security spending and the corresponding BGAs. For example, where there is a shortfall in forecast tax receipts or an increase in demand-led social security spending; it cannot borrow to support discretionary resource spending.

The total limit for resource borrowing is £1.75 billion and the normal annual limit for forecast error is £300 million per year. Due to the triggering of the 'Scotland-specific economic shock' provision of the Fiscal Framework, the annual borrowing limit has been raised to £600 million until 2023-24.

The total limit for capital borrowing to support investment in infrastructure is £3 billion, with annual borrowing limited to £450 million.

The Scotland Reserve is the only mechanism for the Scottish Government to retain underspent funds for future years. The limitations on the use of the Reserve and the volatility relating to forecasts mean that it is neither feasible nor desirable for the Scottish Government to build up substantial balances in the Reserve. If the Scottish Government intentionally underspent its budget to carry forward funds to future years, there is a significant risk that the Reserve limit would be breached and therefore these funds would be returned to the UK Government and lost permanently.

A key constraint faced by the Scottish Government is that all of these limits are set in nominal terms even though the size of the Scottish economy, budget, devolved tax revenues and social security benefit expenditure rises over time. Consequently, over time the Scottish Government's current levers for managing volatility and risk are being effectively eroded in their real term capacity.

For example, since 2017-18 when the limits were initially implemented had they grown in line with inflation then by 2021-22 they would have been around 7% larger. Had they grown in line with the forecast cumulative size of devolved tax revenues they would have been around 19% higher and had they grown in line with the size of the total Scottish Government fiscal resource budget (in cash terms) the limits would have been around 36% higher including additional COVID-19 funding or around 21% higher excluding additional COVID-19 funding.

There are various arguments around how such limits could be indexed, however it is clear that even over a relatively short period of time, the real term effectiveness of the Scottish Government's current levers to manage the risks and volatility within the Fiscal Framework has been eroded. It is imperative that during the upcoming Fiscal Framework review a system is implemented to index any nominal limits within the Fiscal Framework in real terms.

In the meantime, whilst it is operating within these limitations, the Scottish Government uses the following guidelines when managing the budget.

4.2.1 Scotland Reserve policy

We will prioritise use of the Scotland Reserve to carry forward any forecast underspends for use in the subsequent financial year. This retains sufficient capacity in the reserve to be able to also carry forward any additional underspend that emerges later in the budget process (i.e., at provisional and final outturn stages) and mitigates the risk of funds being lost to the Scottish Government.

From 2017-18 to 2019-20, average underspends have been in excess of £350m. By prioritising use of the Reserve for this purpose, we ensure that sufficient capacity remains, so that, where excess tax receipts or additional underspends emerge from the Provisional Outturn and Final Outturn Processes, these can be added to the Scotland Reserve for use in future years.

Our aim is to ensure that excess funds in the Reserve will be used as far as possible to smooth resource funding over time, to achieve a stable spending trajectory. However, this may be balanced against urgent and more immediate requirements such as funding COVID-19 emergent needs.

4.2.2 Resource borrowing policy

The use of resource borrowing is complementary to the use of the Scotland Reserve. The Scottish Government must balance the need for flexibility against the additional costs of borrowing compared to the Reserve to find a solution that is most appropriate to the circumstances.

Our resource borrowing powers will be used in a way that balances the principles of flexibility, stability and value for money, as set out in the 2019 Medium-Term Financial Strategy:

- Resource borrowing is an important tool to help achieve stable funding and spending trajectories, in order to ensure macroeconomic stability. Repayment terms would be as short as possible, to minimise servicing costs, subject to the need to smooth resource spending over time.

- In the context of the constraints outlined above, the scope for reductions in spending and/or use of any funds held in the Scotland Reserve would generally be considered first, before any decision is taken on resource borrowing.

The Scottish Government will assess all planned resource borrowing decisions to smooth the funding trajectory over five years. In order to promote budget stability and maintain flexibility in the Reserve, Scottish Government budgets will assume full borrowing against known and/or forecast tax and social security reconciliations. Any in-year volatility will be managed within the resulting overall budget envelope.

As noted, other than to respond to changes in demand for social security spending, resource borrowing cannot be used to respond to emerging spending pressures, for example, to respond to the impacts of COVID-19.

Given the restrictions on resource borrowing under the existing Fiscal Framework, the only risks created by borrowing are those on future years' resource budgets resulting from borrowing repayments. It is therefore prudent to consider the medium-term impact on the Scottish Budget of reconciliations, borrowing and borrowing repayments in totality. Given the annual limits and short repayment periods, there is no risk of breaching the cumulative limit, and there is also no re-financing risk.

Conversely, there are considerable risks related to forecast error, economic shocks and funding outlooks, depending on UK Government decisions. The resource borrowing powers do not address these sufficiently.

The Scottish Government will make full use of resource borrowing in 2022-23. The full budget impact of borrowing and reconciliations over the period, plus further detailed analysis on this work, can be found in Annex B

These issues, alongside the broader range of tools currently available, must be considered in depth as part of the Fiscal Framework Review in 2022.

4.2.3 Capital borrowing policy

The two key considerations for the medium-term with respect to capital borrowing decisions are the headroom against the cumulative Fiscal Framework limits and affordability of ongoing borrowing repayments.

Capital borrowing powers will be used in a way that balances the principles of flexibility, stability, value for money and intergenerational fairness, alongside supporting the delivery of the NIM.

The 2020-21 Budget sets out the baseline for NIM in 2019-20 of £5.3 billion, which will increase by £1.56 billion by the end of the current Parliament in 2025-26. In order to achieve this increase in investment, capital borrowing will be required as part of a combination of funding sources that also include capital grant, financial transactions and alternative revenue-finance models, including private finance.

While the Scottish Government can borrow commercially or issue bonds for capital investment purposes, the National Loans Fund currently remains the preferred source of capital borrowing. Given the medium-term impact on resource costs, this remains the optimum compromise between value for money, resource cost impact and maximising the use of the Fiscal Framework limits.

The term-structure of borrowing will be chosen to strike the right balance between flexibility (requiring shorter-term lengths); value for money (requiring shorter-term lengths); stability (suggesting longer-term lengths); and intergenerational fairness (term length corresponds to asset life).

The Scottish Government will ensure that a minimum of £300m capital borrowing headroom will be available to be drawn down in the year following the period covered by the NIM (2026-27).

Over the period of the NIM, our policy is to borrow between £250 million and £450 million annually to ensure that there is sufficient investment planned to support economic growth, and that investment increases overall year-on-year.

All borrowing drawdown decisions will take into account the in-year budget management position, the interest rate environment and the impact over the five-year term versus the assumptions made in the Scottish Budget.

4.2.4 Our fiscal levers are insufficient

The Scottish Government continues to take a proactive approach in using the powers that are available across taxation, borrowing and the reserve.

Scotland's forthcoming first Framework for Tax will set out the principles and strategic objectives that underpin our Scottish Approach to Taxation, as well as our approach to decision making, engagement and how we manage and sequence tax policy around the fiscal cycle. Deployed within the context of COVID-19 and the recovery, the Framework provides a solid foundation for the design and delivery of tax policies that support our national outcomes and our pursuit of a fairer, greener and more prosperous Scotland for everyone.

The Framework also demonstrates our commitment to open government and transparency and embodies our ambition for excellence in tax policy and delivery. It includes a high-level programme of work for this Parliament, in line with our manifesto and public commitments.

As set out in the Framework for Tax, evaluation remains a key aspect of tax policy making, assessing the extent to which changes have achieved their intended aims. It also helps examine the drivers for tax performance and underlying dynamics of the tax base. As part of this, we will shortly publish an evaluation of our 2018-19 Income Tax reforms. This will include an assessment of the scale of the behavioural effects and the amount of revenue estimated to have been raised by the policy. This evaluation will form a key part of our understanding of Income Tax performance in Scotland, alongside our ongoing analysis of the fiscal and economic risks.

However, the current devolved fiscal levers have clear limitations in terms of managing risk that restrict our ability to maintain and expand the tax base, raise devolved tax revenues and support the economy.

As set out in the January 2021 MTFS, there is a growing body of evidence that the scale of potential forecast error under the Fiscal Framework exceeds the level of flexibility provided by existing borrowing levers.

Scottish Government analysis noted that, based on the 2018/19 Budget forecasts, there was between a 5% and 17% probability of negative Income Tax reconciliations exceeding -£300 million. Updating this analysis to include all devolved taxes and social security benefits allows us to assess the total reconciliation risk. Based on the forecasts for the 2020/21 budget it is estimated that there is now between an 8% and 24% probability of total negative reconciliations breaching the £300 million annual borrowing powers for forecast error.

Part of this increase in the risk estimate reflects the inclusion of the additional fully devolved taxes (LBTT and SLfT) and social security benefits with a BGA mechanism (although Income Tax remains by far the largest driver of the overall risk). However, as noted earlier the limits on Scottish Government borrowing and reserve flexibility have been fixed since the Fiscal Framework was agreed. Since the size of the economy, and alongside that tax revenues and social security benefit expenditure, increase over time, the Scottish Government's practical ability to manage risk is therefore effectively being eroded each year.

However, even if the limits had been adjusted over time to account for this, they would still have been insufficient to allow the Scottish Government to adequately manage the volatility inherent in the forecasting process.

There is a clear and reasonable case to revise the current borrowing and reserve powers, ensuring appropriate and sufficient budget management tools. The forthcoming review of the Fiscal Framework provides an ideal opportunity to make these much-needed changes, to facilitate adequate risk management over the medium-term.

4.3 The need for a robust, comprehensive and timely review of the Fiscal Framework

The Fiscal Framework Agreement states that a review of the Fiscal Framework should be undertaken by the Scottish and UK Governments after the Scottish Parliament elections in 2021, and that this will be informed by an independent report that will be presented to both governments by the end of 2021.

In October 2021, the Scottish and UK Governments agreed to commission an independent report focusing on the Block Grant Adjustments, including a call for stakeholder input, prior to a broader review of the Fiscal Framework. Both governments are working towards the Review beginning as early in 2022 as possible.

Views from stakeholders other than the two Governments will be sought as part of the process.

As set out in the Programme for Government in September 2021, the Scottish Government will use the Fiscal Framework review to push for a substantial increase in the fiscal power of the Scottish Parliament, to allow us to begin to manage our key risks over the medium-term:

- Removal of the caps on capital borrowing, which constrain our ability to invest in the economy and public services, to be replaced by a prudential borrowing scheme – the same power local authorities already enjoy.

- Removal of the restriction on resource borrowing to fund day‑to‑day costs, an increase in the borrowing cap for forecast errors to £600 million, and an increase in the Scotland Reserve drawdown to £700 million per year.

- Strengthening of Scotland's tax powers with the devolution of VAT, and full powers over Income Tax and National Insurance contributions.

In addition, there is a range of additional substantive issues to be covered as part of the Review. These issues were discussed in detail in the MTFS published in January 2021, having previously been identified in the joint working group report between the Scottish Government and the Scottish Parliament's Finance and Constitution and Social Security Committees.[13] It remains crucial that the Review considers the arrangements for intergovernmental engagement and co-ordination. This should include how we minimise friction in interactions between the two governments' tax and social security regimes to ensure that the Scottish Government has maximum flexibility in its policy choices and ability to manage the impacts of UK policy choices through the Fiscal Framework and vice versa.

We also continue to seek a resolution on the outstanding dispute concerning the disproportionate impact of personal allowances increases on Scottish revenues, and the appropriate application of the spillover provision in the current Fiscal Framework Agreement. While the scale of the financial impact is disputed, both parties accept that a direct spillover effect arises from the UK Government's changes to the Personal Allowance and that the Scottish Government is due a transfer of funding. The Scottish Government will seek to conclude the dispute process at the earliest possible opportunity to ensure that the funding is available to support the funding position for 2022-23. Issues relating to the spillovers provisions should be considered in more detail as part of the forthcoming review of the Fiscal Framework.

4.4 The Resource Spending Review Framework

Within the limitations of the current Fiscal Framework, however, controlling expenditure is our primary lever to maintain a sustainable trajectory for Scotland's public finances.

The Resource Spending Review Framework is published alongside this year's MTFS. The Resource Spending Review will develop spending plans for the remainder of this parliamentary term which support the government's ambitions and provide stakeholders, delivery partners and organisations and individuals across Scotland with some certainty on which to base their own forward planning. The Framework sets the scene for the development of those spending plans and launches the public consultation. The intention is to publish multi-year spending plans in May 2022 to provide stakeholders, delivery partners and organisations and individuals across Scotland with some certainty on which to base their own forward planning.

The mission for the Resource Spending Review is to deliver effective services for the people of Scotland and maintain sustainable public finances. It must do this within a tight budgetary envelope and challenging fiscal outlook as explored in Chapters 1 and 2 of this MTFS. That means that choices must be made about how funding is allocated and our priorities for investment.

To do this, the Resource Spending Review will adopt an approach which is outcomes focused, evidence informed and consultative. Spending plans will be assessed against three core priorities, which draw on the commitments the Scottish Government has made in the Programme for Government and COVID-19 Recovery Strategy:

- To support progress to meet our child poverty targets;

- To address climate change, and;

- To secure a stronger, fairer, greener economy

Underpinning these priorities is our core public finance principle of fiscal sustainability. We must adapt and future-proof our public services, using our limited resources as efficiently and effectively as possible, and investing in long-term preventative measures to ensure that we are able to meet the needs of future generations as well as our own.

Contact

Email: sophie.osborn@gov.scot