The Scottish Government's Medium Term Financial Strategy

This is the fourth Medium Term Financial Strategy (MTFS) published by the Scottish Government. The MTFS provides the context for the Scottish Budget and the Scottish Parliament.

2. Scotland's Fiscal Outlook

Under the Fiscal Framework, three factors determine the available funding for the Scottish Budget:

- UK Government spending decisions: Through the Barnett formula, the change in the Scottish Government's Block Grant each year is determined by the change in the UK Government's spending on areas devolved to the Scottish Parliament.

- Relative growth in Scottish Government and UK Government devolved tax revenues: Under the Fiscal Framework, if Scottish devolved tax revenue per person grows relatively faster than in the rUK, the Scottish Budget is better off and vice versa. This means that Scotland's budget is influenced not only by tax policy and economic performance in Scotland, but also by tax policy and economic performance in the rest of the UK.

- Relative growth in Scottish and UK social security expenditure: Under the Fiscal Framework, if Scottish devolved social security expenditure per person grows relatively faster than in the rUK, the Scottish Budget is worse off. If UK expenditure per person grows relatively faster, additional funds are available within the Scottish Budget. Again, this means that Scotland's budget is influenced not only by policy changes within Scotland, but also what happens in the rest of the UK.

This chapter sets out possible scenarios for the Scottish Government's funding outlook based on these three factors and the latest economic and fiscal forecasts from the OBR and SFC.

2.1 The central scenario for the resource funding outlook

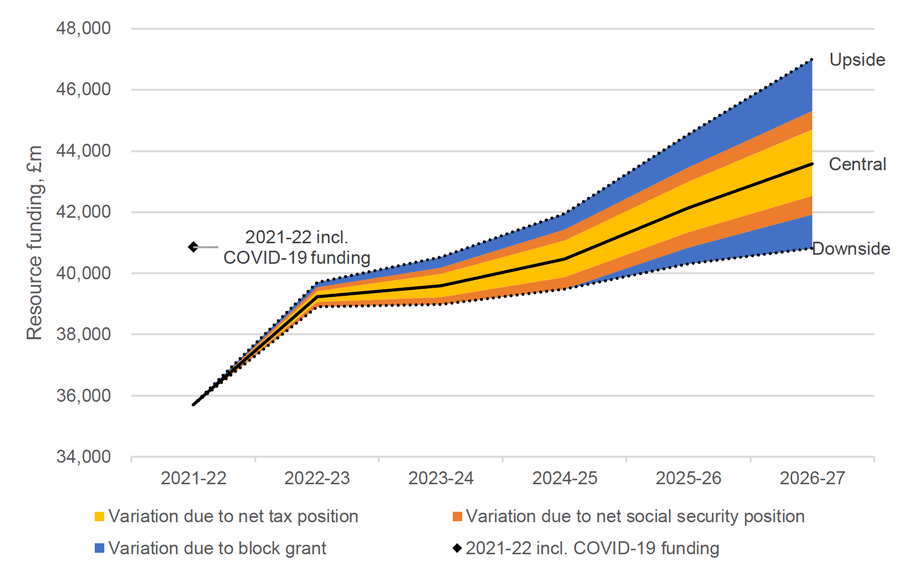

Figure 4 below presents the central resource funding outlook for the Scottish Government over the five-year forecast horizon of the MTFS. This is broadly driven by decisions taken by the UK Government in its Spending Review and the economic and fiscal forecasts provided by the SFC and OBR on the basis of Scottish and UK Government policies, subject to some adjustments discussed below. It also presents an upside and downside scenario for funding, indicating plausible alternative funding paths. These are discussed in more detail in sections 2.2 and 2.3 below.

| £ million | 2021-22 | 2022-23 | 2023-24 | 2024-25 | 2025-26 | 2026-27 | |

|---|---|---|---|---|---|---|---|

| Resource funding | Upside | 35,704 | 39,702 | 40,529 | 41,956 | 44,541 | 46,997 |

| Central | 35,704 | 39,236 | 39,595 | 40,463 | 42,143 | 43,576 | |

| Downside | 35,704 | 38,907 | 38,980 | 39,485 | 40,308 | 40,817 | |

2021-22 figures do not include COVID-19 funding.

2.1.1 Block Grant

Block Grant funding from the UK Government is still the largest single component of funding for the Scottish Government, and the Barnett formula is used to determine the annual change in the grant based on new spending announced by the UK Government.

The UK Government's October 2021 Spending Review set out departmental spending plans for 2022-23, 2023-24 and 2024-25. This sets out the level of the Scottish Government's Block Grant over the same period and gives a degree of certainty about future funding.

The UK Government has not made spending commitments for 2025-26 and 2026-27, so funding for those years remains more uncertain. For the central funding outlook, we have assumed that the Block Grant in these years grows in line with the OBR's forecasts for overall UK Government resource spending growth.

While the Spending Review theoretically sets the envelope for future expenditure, historically there have been changes to spending plans within a Spending Review period. Any changes to the UK Government's spending plans in future years represents a risk for the Scottish Government's funding outlook.

2.1.2 Devolved Taxes

While the Block Grant still accounts for most of the funding for the Scottish Budget (and hence creates the greatest source of uncertainty in future funding), the devolution of significant tax and social security powers has also exposed the Scottish Budget to the relative performance of the Scottish and rUK economies and the policy decisions made by the Scottish and UK Governments.

For devolved taxes, if tax revenue per head in Scotland grows faster than in the rUK, then the Scottish Budget is made better off. This means that faster economic growth in Scotland or policies that increase tax revenue per person relative to the rUK increase the funding available to the Scottish Budget. However, the converse is also true – slower economic growth in Scotland or policies that reduce tax revenue per person will reduce the funding available to the Scottish Budget.

However, it is worth highlighting that the Fiscal Framework broadly protects the Scottish Budget from economic shocks that affect both Scotland and the rest of the UK equally, as in theory any change in Scottish tax revenues should be broadly offset by an equal change in the respective Block Grant Adjustment (BGA) for that tax.

Consequently, the risk to the Scottish funding outlook over time reflects not how the Scottish economy is doing in isolation, but how it is performing relative to the rUK. A stronger (or weaker) relative economic performance over time in Scotland will result in a larger (or smaller) pool of funding available for the Scottish Government. Risks to the funding outlook include whether Scotland is more or less exposed to an economic shock or changing economic conditions than the rUK, perhaps due to differences in the sectoral composition between the two economies.

The other source of risk to the Scottish Budget reflects the policy choices made by both the UK and Scottish Governments. For example, the decision of the UK Government to freeze the Higher Rate Threshold for Income Tax until 2025-26 will increase the amount of Income Tax collected in the rest of the UK and, unless an equivalent policy change is made in Scotland, will make the Scottish Budget worse off.

2.1.3 Social Security expenditure

For devolved social security expenditure, in a similar manner to devolved taxes, what matters for the Scottish Budget is the relative growth in expenditure per head between Scotland and the rUK.

In addition to economic factors, the growth in social security expenditure over time will be heavily affected by the policy decisions made by both governments. This can include technical changes to the eligibility of certain benefits, changes to the generosity of certain payments or decisions around the rate at which payments are increased or uprated over time.

2.1.4 Central Scenario

The central funding scenario includes the central outlook on UK Government spending from the Spending Review, alongside the latest tax revenue forecasts by the SFC and Block Grant Adjustments based on the latest OBR forecasts, which are based on the stated Scottish and UK Government policy.

Given that the Scottish Budget's funding outlook is driven by changes to UK fiscal policy, the relative economic performance of Scotland and the rUK and differences in devolved tax and social security policy between both governments, this implies that despite a degree of certainty created by the UK Government's 3-year Spending Review, the future funding outlook retains a level of volatility.

The central scenario described here is considered the most likely outcome, and is the main scenario used by the Scottish Government for planning purposes. However, it is also useful to consider alternative scenarios to help illustrate the risks to the Scottish Budget funding outlook (both positive and negative) should UK fiscal policy change in the future, or the economic and fiscal forecasts prove to be inaccurate.

Figure 4 above illustrates the resource funding outlook under a central, upside and downside scenario. In the upside and downside scenarios, different assumptions have been used about each of these three drivers of the Scottish fiscal position. These scenarios apply feasible alternative assumptions to generate plausible paths for the resource funding available to the Scottish Government. They do not represent the full range of possible outcomes, nor is it possible to assign a probability to each scenario.

The assumptions used to generate the upside and downside scenarios are described in more detail below.

2.2 Upside funding scenario: stronger Scottish tax performance and a looser UK fiscal stance

Under the upside scenario, there is an additional £470 million funding available in 2022-23, rising to £3.4 billion in 2026-27. This is driven principally by making more optimistic assumptions about UK Government fiscal policy, Scottish economic performance relative to the rest of the UK, and, to a lesser extent, the social security Block Grant Adjustment.

In this scenario, we assume the Block Grant grows somewhat faster (an additional 0.5% points per year) than currently forecast during the Spending Review period, and then substantially faster (an additional 1.5% points per year) in the final two years of the scenario. This could represent a stronger than expected recovery, providing space for the UK Government to increase spending while still meeting its fiscal rules. It could also reflect the UK Government changing its fiscal rules in response to a changed economic outlook. Box 1 discusses the current UK fiscal rules and their implications in more detail.

This scenario also assumes a relatively stronger growth in earnings and employment in Scotland compared to rUK. This increases Scottish Income Tax revenue at a greater rate than tax revenue in rUK, which under the Fiscal Framework increases the Scottish Budget. The divergence in earnings and employment growth between Scotland and rUK (0.5% points and 0.7% points in each year, respectively) is high by historical standards but provides a useful illustration of the degree of volatility that changes in relative economic performance can generate.

The upside scenario also assumes a higher Block Grant Adjustment for social security, accumulating by on average around 2 additional % points per year compared to the central forecast. This is based on the average forecast error for the OBR's Great Britain level forecasts of social security payments.

There is no reason to believe the three 'optimistic' assumptions used to generate the upside scenario will necessarily occur together. For example, we are not explicitly assuming that a change in the UK Government's fiscal stance would be more or less likely to occur alongside a relatively stronger economic performance in Scotland. Figure 4 decomposes how much of the variation in the upside scenario from the central is due to each assumption. This shows the funding outlook for adjusting only one of these assumptions in isolation from the others.

Box 1: UK fiscal targets

In October the UK Government announced its new fiscal targets. These include a revised fiscal mandate and three supplementary targets.

The new fiscal mandate is:

To have public sector net debt (excluding the Bank of England) as a share of GDP falling by the third year of the rolling forecast period.

The three supplementary targets are:

- To balance the current budget by the third year of the rolling forecast period.

- To ensure that public sector net investment does not exceed 3% of GDP on average over the rolling five-year forecast period.

- To ensure that a subset of expenditure on welfare is contained within a predetermined cap and margin set by the Treasury (the 'welfare cap').

Successive Chancellors have announced 11 different fiscal targets in the last seven years prior to this most recent announcement. Most of these have been missed before being abandoned. As such, the new fiscal rules will not necessarily bind the UK Government, and may be changed or abandoned if they look likely to be missed.

While this flexibility is welcome in some respects, allowing policy to adapt to major shocks like COVID-19, it also means these fiscal targets may not be a good guide to future UK Government spending. In their most recent forecasts, the OBR expect all these targets to be met individually, but note that the space for doing so is very limited. Given past experience, a change in economic circumstances that made meeting the fiscal targets more challenging could result in either a reduction in spending, or simply a change to new fiscal targets that are easier to meet. As such, UK fiscal targets do not typically provide a strong long-term basis for anticipating what funding the Scottish Government might receive if economic and fiscal conditions change.

2.3 Downside scenario: weaker Scottish tax performance and a tighter UK fiscal stance

Under the downside scenario, funding is reduced by £330 million in 2022-23, with the reduction increasing to £2.8 billion in 2026-27. The underlying assumptions are mostly symmetric to the assumptions used to generate the upside scenario. This includes the tax revenue forecasts, which assume Scottish earnings and employment growth 0.5% points and 0.7% points slower in each year of the forecast. The social security Block Grant similarly diverges from the central estimate, resulting in slower growth, by around 2% points in each year of the forecast, mirroring the upside scenario.

The exception is the growth in the Block Grant during the Spending Review period, which is assumed to match the central scenario. This reflects the fact that substantial reductions in resource spending plans announced through a Spending Review are generally unlikely, outside of a major economic shock. Such a shock would likely affect the funding and spending outlook of the Scottish Government substantially, likely outside the bounds of the scenarios presented in this publication. Beyond the Spending Review period, the downside risk to the Block Grant is assumed to be equal to the upside risk (i.e. 1.5% points slower growth per year than currently forecast), reflecting the wide range of possible fiscal paths the UK Government could adopt in future.

As above, there is no reason to believe the assumptions that generate the downside scenarios will be correlated with one another. Some could occur alongside components of the upside scenario. For example, an uneven recovery where economic activity improved faster than expected in rUK, but remained more subdued in Scotland, could support a looser fiscal stance from the UK Government, while weakening the Scottish Budget position through weaker tax revenue.

2.4 Outlook for capital funding

The drivers of capital funding are relatively simple compared to the factors that affect the resource funding outlook. Capital funding is primarily provided by the Block Grant and Financial Transactions (FT) allocations, with the latter determined by the UK Government's capital spending plans. The remaining sums arise from income and receipts, deployment of Scottish capital borrowing powers, from innovative financial and revenue finance models, and from recycling repayments from earlier FT loans.

Table 3 below shows the funding outlook for the capital Block Grant, including an upside and downside scenario. As with the resource outlook, the UK Government's Spending Review settlement provides a degree of certainty over the next three financial years. In 2025-26 and 2026-27, we have assumed that the capital grant funding available to the Scottish Government will grow with the OBR's forecasts for UK wide public sector investment. However, this is highly uncertain, and capital spending is typically subject to more variation than resource spending.

For example, the UK Spending Review in October 2021 provided a Scottish capital grant allocation considerably lower than our expected allocation based on OBR forecasts. On this basis, we have adopted an assumption of the capital allocation remaining fixed in cash terms as the downside scenario.

The wide range between these scenarios demonstrates the limitations on the Scottish Government's ability to set multi-year spending plans. A more cautious approach to the funding outlook may be required in the future, which may in turn hamper our efforts towards delivering the infrastructure investment needed to achieve our National Outcomes as set by our National Infrastructure Mission.

| £ million |

£ million |

2021-22 |

2022-23 |

2023-24 |

2024-25 |

2025-26 |

2026-27 |

|---|---|---|---|---|---|---|---|

| Block Grant capital funding, excluding financial transactions |

Upside |

5,520 |

5,897 |

5,874 |

5,748 |

6,047 |

6,048 |

| Central |

5,520 |

5,897 |

5,874 |

5,748 |

5,968 |

5,880 |

|

| Downside |

5,520 |

5,897 |

5,874 |

5,748 |

5,748 |

5,748 |

Contact

Email: sophie.osborn@gov.scot