The Scottish Government's Medium Term Financial Strategy

This is the fourth Medium Term Financial Strategy (MTFS) published by the Scottish Government. The MTFS provides the context for the Scottish Budget and the Scottish Parliament.

1. Scotland's Economic Outlook

This chapter provides an update on the Scottish economy, with a summary of the latest official economic and tax forecasts from the Scottish Fiscal Commission (SFC) and the Office for Budget Responsibility (OBR). The chapter also looks at the impact these updated economic forecasts have on the Scottish Budget and discusses the actions the Scottish Government is taking to deliver a fairer and greener recovery from the pandemic.

1.1 State of the Economy

The Scottish economy has continued to recover across 2021 as restrictions on economic activity have largely been lifted. However, the recent emergence of the Omicron COVID-19 variant and associated uncertainty will weigh on consumer and business confidence. The Organisation for Economic Co-operation and Development's (OECD) latest assessment from 1st December 2021 is that it could intensify imbalances that are slowing growth, raising costs, and could delay the world economy's return to pre-pandemic levels.[3]

Scotland's Gross Domestic Product (GDP) continued to edge back towards its pre-pandemic level in September and is now 1.1% below that level, having fallen over 20% at the start of the pandemic.[4] The pace of growth generally slowed in recent months, reflecting both the moderation of the boost in output from restrictions easing over the second quarter and the impact of volatile industries such as energy production. This is alongside the intensifying global supply chain issues and rising levels of inflation seen in the global economy, alongside the UK Government withdrawing COVID-19 fiscal support policies domestically.

Labour market conditions have continued to improve. The number of payrolled employees is now above pre-pandemic levels, having fallen almost 4% during 2020. Although 80,000 jobs in Scotland were still on the furlough scheme when it ended in September, emerging survey data suggests many furloughed workers have since returned to work, which should contribute to long-term economic scarring being lower than initially feared.

Trading conditions remain challenging for businesses at this stage of the pandemic, as supply chain disruption and inflationary pressures on input costs have intensified and have presented new cash flow challenges for many businesses. Businesses have also been more immediately exposed to the recent sharp rise in energy costs, particularly those without access to financial instruments that can help hedge or manage such risks.

The latest data indicates that businesses are partly absorbing some of these higher costs, but some businesses are beginning to pass these cost pressures through to consumers. As a result, inflation could rise further in the months ahead. This is largely expected to be temporary as the economy continues to rebalance, but it could still create new pressures on households' budgets and spending power.

1.1.1 Latest Economic Forecasts of the Scottish and UK Economies[5]

The outlook for the Scottish and UK economies is significantly more positive than at the time of the previous Scottish Budget, although the pandemic continues to weigh upon the economy and uncertainties remain elevated.

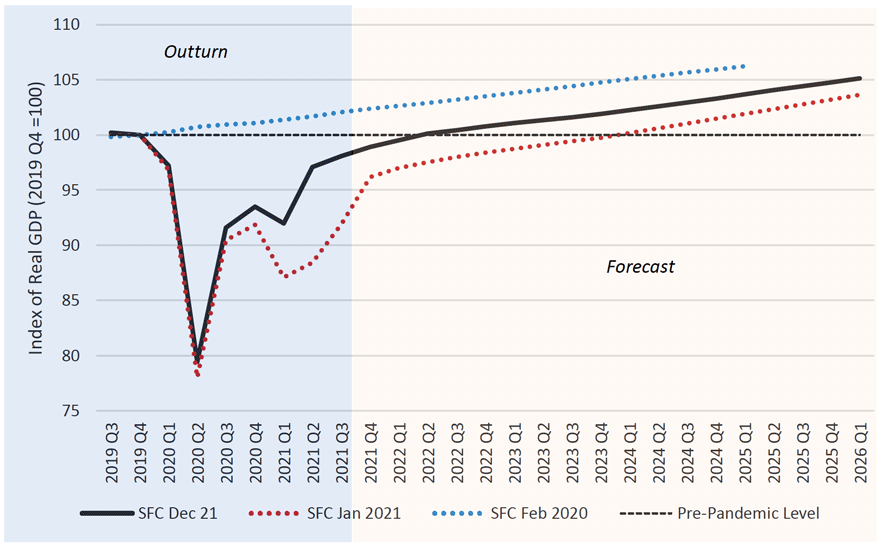

The latest forecasts from the SFC show the Scottish economy recovering to pre-pandemic levels by Apr–Jun 2022, almost 2 years earlier than forecast at the previous Scottish Budget in Jan 2021. This is only slightly slower than the OBR's latest forecast for the UK economy, which is now expected to return to pre-pandemic levels in Jan–Mar 2022.

Scottish Fiscal Commission

The level of long-term economic "scarring" to the Scottish economy from COVID-19 has been revised down from an anticipated permanent reduction in long-term GDP of around

-3% at last year's Budget to one of around -2%, reflecting the SFC's view that the pandemic has not damaged the long-term productive capacity of the Scottish economy as much as previously feared. This is similar to the OBR's latest view of the degree of long-term scarring to the UK economy, and smaller than the 4% long-term reduction in living standards that the OBR attributes to leaving the European Union (EU).

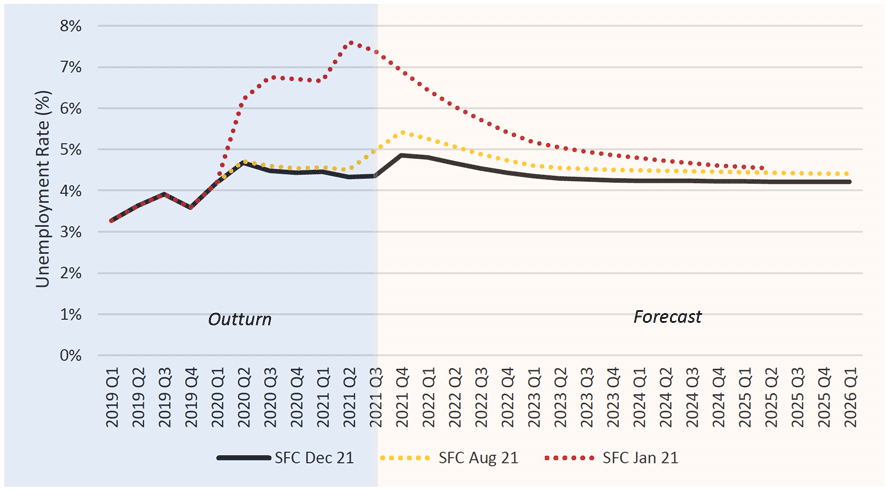

Part of this greater degree of optimism has been driven by the resilience of the labour market. In January 2021 the SFC and OBR, along with many other external forecasters, were forecasting significant increases in unemployment as it was still unclear how far the economy would be able to recover ahead of the ending of support schemes. As the vaccine programme has been delivered and economic restrictions have been removed earlier than expected at the time, the outlook for the labour market improved in tandem. The SFC now expect unemployment to peak at 4.9% in October–December 2021, reflecting a small increase after the unwinding of the Furlough scheme, although one far below the 7.6% forecast at the time of the previous Scottish Budget.

Scottish Fiscal Commission

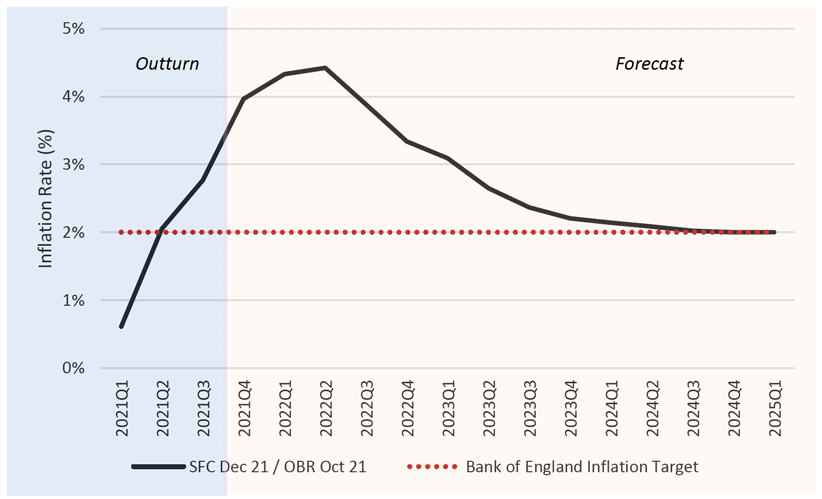

However, the SFC's outlook for inflation has changed significantly since January 2021 when it was forecast to remain low and below the Bank of England's 2% target. The latest forecast, which is aligned with the OBR's October 2021 UK inflation forecast, has been revised up with inflation forecast to peak at 4.4% in Apr – Jun 2022 before gradually returning to 2% by the second half of 2024.

The SFC mirrors the view of the OBR that the increase in inflation is largely a temporary phenomenon, driven by the rebound in global demand for goods and services across 2021 which has put strong pressure on supply chains, particularly in the energy sector. These pressures have resulted in temporary price increases which are expected to ease as supply chains readjust to higher levels of demand.

Scottish Fiscal Commission; Office for Budget Responsibility; Bank of England

1.1.2 Fiscal Implications for the Economic Outlook

As set out in Chapter 2, the Scottish Budget is influenced both by UK Government decisions on expenditure on devolved issues, and the relative performance of devolved tax revenues. Consequently, differences between the Scottish and UK economic forecasts can have a material impact on the funding outlook for the Scottish Government.

Ultimately, any impact on the Scottish Budget from devolved tax revenue will reflect the performance of tax revenues in Scotland relative to the rest of the UK (rUK). However, due to outturn data publication lags forecasts from the SFC and OBR are used to inform the Scottish Budget until outturn data is known. These forecasts, and the judgements of the forecasters that inform them, can then affect the funding the Scottish Government receives at each Scottish Budget. Even relatively small differences between the OBR and SFC forecasts of the Scottish and UK economies can significantly influence the short-term funding outlook for the Scottish Government.

As Table 1 below shows, there are some significant differences of view on the economic outlook between the SFC and OBR. Whilst both institutions have a very similar outlook on unemployment, the forecasters have a differing view on earnings and employment growth at the Scottish and UK level.

| 2021-22 | 2022-23 | 2023-24 | 2024-25 | 2025-26 | 2026-27 | ||

|---|---|---|---|---|---|---|---|

| GDP Growth (%) | SFC Dec-21 | 10.4 | 2.2 | 1.2 | 1.3 | 1.4 | 1.4 |

| OBR Oct-21 | 10.8 | 4.2 | 1.7 | 1.4 | 1.6 | 1.7 | |

| Unemployment Rate (%) | SFC Dec-21 | 4.6 | 4.5 | 4.3 | 4.2 | 4.2 | 4.2 |

| OBR Oct-21 | 4.9 | 4.6 | 4.3 | 4.2 | 4.2 | 4.2 | |

| Avg. Nominal Earnings Growth (%) | SFC Dec-21 | 3.8 | 2.6 | 3.0 | 3.2 | 3.3 | 3.4 |

| OBR Oct-21 | 5.2 | 4.0 | 2.5 | 2.3 | 3.1 | 3.6 | |

| Employment Growth (%) | SFC Dec-21 | 1.3 | 1.0 | 0.1 | -0.1 | -0.2 | -0.2 |

| OBR Oct-21 | -0.1 | 1.3 | 1.0 | 0.5 | 0.4 | 0.4 | |

| Inflation (%) | SFC Dec-21 | 3.3 | 3.7 | 2.3 | 2.0 | 2.0 | 2.0 |

| OBR Oct-21 | 3.3 | 3.7 | 2.3 | 2.0 | 2.0 | 2.0 | |

Scottish Fiscal Commission; Office for Budget Responsibility

The nature of the pandemic, which continues to affect the economy on a monthly basis, can make headline comparisons of annual GDP difficult. Although the Scottish and UK economies are forecast to perform differently in the short term, over the long-term Scottish and UK GDP are forecast to perform more similarly.

However, the SFC do identify sectors of the Scottish economy which have underperformed relative to the UK, and which may be particularly relevant for devolved tax receipts. Some of these are long term trends, such as demographic pressures and for which key levers such as migration policy remain reserved. Others reflect the differing structure of the Scottish and UK economies, with the Scottish economy more exposed to the downturn in the oil and gas industry, and the rUK benefitting relatively more from the strong performance of financial services sector particularly in London and the South East. As a result, overall devolved revenues are forecast to grow more slowly in Scotland than the rUK. In 2022-23, overall devolved taxes are forecast to be smaller than the Block Grant Adjustments for the first time and this is expected to continue for most of the forecast period.

However, the final net position will not be known until official outturn data are published. Even relatively minor differences in the outlook for the Scottish and rUK economies can significantly alter the forecast tax revenue net positions and it will be some time (2024 for Income Tax) before the true net position becomes clear.

1.2 Increasing prosperity

As we emerge from the pandemic, we must work together to seize Scotland's potential and build an economy for everyone by delivering greater, greener and fairer prosperity. We have taken significant action to support firms and households during the pandemic. Businesses have benefitted from over £4.4 billion of Scottish Government support, including the extension of 100% Non-Domestic Rates relief for all retail, leisure, aviation and hospitality premises, including nightclubs, for all of 2021-22. This, alongside other measures such as a reduction to the poundage, ensures that Scotland offers the most generous non-domestic rates regime in the UK.

We also know that for a successful recovery, and to ensure that no one is left behind, a focus on employability and skills is key. In 2021-22 we are investing more than £1 billion to drive forward our national ambition for jobs and to equip our workforce with the future skills it needs. Our Programme for Government commits up to £70 million for the Young Person's Guarantee, which will provide at least 24,000 new and enhanced skills and training opportunities for young people. This is part of the extra £125m allocated to enhance the National Transition Training Fund, all-age skills and employability support. A further £20m is also being spent to support the long term unemployed, working with 'No One Left Behind' partners to create new fair work job opportunities of community value within the public and third sector.

We also continue to invest in our infrastructure to boost economic wellbeing, prosperity and employment, with large-scale investment in new, emerging and high-value sectors – providing businesses with the confidence to grow and diversify. The Infrastructure Investment Plan (published in February 2021) sets out a pipeline of work that will help stimulate Scotland's economy. Around 45,000 construction and maintenance jobs will be supported annually through the total capital investment over the next five years. The Plan will also encourage the creation of green jobs and stimulate a greener economic recovery.

We are also setting out new and refreshed economic strategies tailored to meet the new challenges ahead. Our COVID-19 Recovery Strategy sets out the key outcomes that will be prioritised to tackle the inequalities that COVID-19 has highlighted, alongside specific actions being undertaken to drive these outcomes and rebuilding public services. Our forthcoming 10-year National Strategy for Economic Transformation will also look to build on these priorities into the long term to create a greener, fairer and more inclusive wellbeing economy.

1.2.1 COVID-19 Recovery Strategy

The foundations of the recovery strategy need to reflect the priorities of individuals, families, businesses and communities to address the impacts of the pandemic and build resilience for the future. The process of recovery involves supporting these groups through the losses experienced during the pandemic and the construction of a different future.

The COVID-19 Recovery Strategy[6] recently published by the Scottish Government aims to:

- Address the systemic inequalities made worse by COVID-19;

- Make progress towards a wellbeing economy;

- Accelerate inclusive, person-centred public services.

The three key outcomes of the Recovery Strategy central to achieving this vision and most likely to have the greatest impact on tackling some of the inequalities and disadvantages highlighted by COVID-19 include:

- Financial security for low-income households;

- Wellbeing of children and young people, and;

- Good, green jobs and fair work.

We have set out a summary of cross cutting actions with accompanying timelines aimed at delivering these three outcomes. There is a focus on driving job creation; increasing employee earnings; reducing the cost of living; providing early and preventative support for children and families; promoting the conditions for wellbeing to flourish; and creating the conditions for fair work and a just transition.

Specific actions include ensuring every region of Scotland has a Regional Economic Partnership (REP) to encourage and co-ordinate strategic collaboration between key economic actors within regions. Businesses will be offered help, via the Green Jobs Fund, to create green sector employment and invest in equipment and premises. A skills guarantee will also be introduced for workers in carbon-intense sectors, as part of the Green Jobs Workforce Academy. In addition, support will be offered to individuals moving into new jobs or sectors, by investing in adult upskilling and retraining and creating a new Digital Skills Pipeline.

1.2.2 10-Year National Strategy for Economic Transformation (NSET)

Our long-term vision for Scotland is one of a low-carbon, wellbeing economy – a society that is thriving across economic, social and environmental dimensions, delivering sustainable and inclusive economic prosperity for Scotland's people and places.

Our forthcoming 10-Year National Strategy for Economic Transformation will build on the COVID-19 Recovery Strategy to create a greener, fairer and more inclusive wellbeing economy. The Strategy will help put us on the path to meeting our 2030 climate targets, helping restore the natural environment, stimulate innovation, create jobs, improve wellbeing for all and further embed fair work across the economy.

The Strategy will support long-term aims such as a just transition to net zero and will bring together components of other strategies and targets, such as the recommendations of the Advisory Group on Economic Recovery[7].

We will stimulate business growth by investing in innovation, expanding opportunities internationally and supporting businesses to benefit from the transformational opportunities of digitalisation. This will help create quality employment opportunities and generate revenue to invest in public services.

Contact

Email: sophie.osborn@gov.scot