The Scottish Government's Medium Term Financial Strategy

This is the fourth Medium Term Financial Strategy (MTFS) published by the Scottish Government. The MTFS provides the context for the Scottish Budget and the Scottish Parliament.

Annex B: Fiscal Framework

This Annex sets out the implications of the Fiscal Framework for the Scottish Budget. The Fiscal Framework Technical Note sets out more detail on how the Fiscal Framework operates including the evolution of the fiscal powers of the Scottish Parliament, the timelines for reconciliations and how they affect the Scottish Budget, the limits of the borrowing powers and Scotland Reserve, and the Fiscal Framework Review.[21]

This Annex details the latest BGAs published alongside the 2022-23 UK Budget on 27 October 2021, which have been updated following the publication of final outturn data for [insert which outturn has been published, which affected the final BGAs]. The latest SFC revenue and expenditure forecasts have been published alongside the 2022-23 Scottish Budget.

Tax

Table B.1 shows the latest forecasts for tax revenues from the SFC and the latest BGA estimates following the 2022-23 UK Budget.

| 2019-20 | 2020-21 | 2021-22 | 2022-23 | 2023-24 | 2024-25 | 2025-26 | 2026-27 | ||

|---|---|---|---|---|---|---|---|---|---|

| Income Tax2 | Revenue | 11,833 | 11,938 | 13,002 | 13,671 | 14,313 | 15,056 | 15,790 | 16,445 |

| BGA1 | -11,685 | -11,989 | -12,996 | -13,861 | -14,571 | -15,167 | -16,036 | -16,862 | |

| Difference | +148 | -51 | +6 | -190 | -257 | -111 | -246 | -417 | |

| LBTT2 | Revenue | 597 | 517 | 720 | 749 | 796 | 839 | 881 | 924 |

| BGA1 | -533 | -397 | -620 | -664 | -688 | -717 | -753 | -802 | |

| Difference | +64 | +121 | +101 | +86 | +108 | +122 | +128 | +122 | |

| SLfT2 | Revenue | 119 | 107 | 123 | 101 | 83 | 85 | 70 | 18 |

| BGA1 | -99 | -87 | -90 | -82 | -82 | -77 | -69 | -78 | |

| Difference | +20 | +20 | +34 | +18 | +1 | +9 | +1 | -60 | |

| Total | Revenue | 12,549 | 12,562 | 13,846 | 14,521 | 15,193 | 15,980 | 16,741 | 17,387 |

| BGA1 | -12,316 | -12,473 | -13,706 | -14,607 | -15,340 | -15,961 | -16,859 | -17,742 | |

| Difference | +233 | +89 | +140 | -86 | -148 | +20 | -117 | -355 | |

Note 1: The BGAs shown are calculated using the Indexed Per Capita (IPC) indexation method. This method in practice determines the BGAs applied to the budget.

Note 2: The 2019-20 Income Tax, LBTT and SLfT and 2020-21 LBTT and SLfT revenue and Block Grant Adjustment are outturn figures.

Figures may not sum due to rounding.

The forecasts of tax revenues and BGAs for 2022-23 inform the Scottish Budget.

Forecasts of future years provide an indication of the level of revenues that the SFC anticipates, but these figures will not be used to set future budgets, which will draw upon updated SFC forecasts.

Social Security

Table B.2 shows the SFC's latest expenditure forecasts for social security benefits and the latest BGA estimates following the 2022-23 UK Budget. Executive competence for Cold Weather Payments (CWP) will transfer to the Scottish Government in 2022-23 and BGAs were agreed for CWP for the first time alongside the 2022-23 UK Budget.

| 2020-21 | 2021-22 | 2022-23 | 2023-24 | 2024-25 | 2025-26 | 2026-27 | ||

|---|---|---|---|---|---|---|---|---|

| Attendance Allowance | Expenditure | -528 | -519 | -545 | -575 | -600 | -628 | -653 |

| BGA1 | 521 | 521 | 545 | 579 | 605 | 630 | 648 | |

| Difference | -6 | +2 | 0 | +4 | +5 | +3 | -5 | |

| Personal Independence Payment | Expenditure | -1,626 | -1,734 | -1,948 | -2,322 | -2,588 | -2,806 | -3,034 |

| BGA1 | 1,585 | 1,723 | 1,933 | 2,176 | 2,390 | 2,619 | 2,820 | |

| Difference | -41 | -11 | -15 | -146 | -198 | -187 | -214 | |

| Disability Living Allowance | Expenditure | -722 | -700 | -710 | -721 | -712 | -699 | -687 |

| BGA1 | 721 | 687 | 687 | 692 | 664 | 639 | 657 | |

| Difference | -1 | -13 | -23 | -29 | -48 | -61 | -29 | |

| Carer's Allowance2, 3 | Expenditure | -296 | -301 | -315 | -348 | -380 | -412 | -445 |

| BGA1 | 291 | 295 | 323 | 351 | 378 | 413 | 453 | |

| Difference | -5 | -6 | +8 | +3 | -3 | 0 | +8 | |

| Industrial Injuries Disablement Scheme | Expenditure | -83 | -81 | -81 | -81 | -80 | -79 | -78 |

| BGA1 | 81 | 79 | 79 | 80 | 78 | 77 | 75 | |

| Difference | -1 | -1 | -1 | -1 | -2 | -2 | -3 | |

| Severe Disablement Allowance | Expenditure | -7 | -7 | -6 | -6 | -5 | -5 | -4 |

| BGA1 | 8 | 7 | 6 | 5 | 4 | 4 | 3 | |

| Difference | 0 | 0 | 0 | 0 | -1 | -1 | -2 | |

| Cold Weather Payments | Expenditure | N/A | N/A | -21 | -21 | -21 | -21 | -22 |

| BGA1 | N/A | N/A | 14 | 14 | 14 | 14 | 14 | |

| Difference | N/A | N/A | -7 | -7 | -7 | -7 | -8 | |

| TOTAL SS | Expenditure | -3,262 | -3,343 | -3,626 | -4,074 | -4,387 | -4,650 | -4,922 |

| BGA1 | 3,207 | 3,313 | 3,587 | 3,898 | 4,134 | 4,395 | 4,670 | |

| Difference | -55 | -30 | -38 | -176 | -253 | -255 | -252 | |

Note 1: The BGAs shown are calculated using the Indexed Per Capita (IPC) indexation method. This method in practice determines the BGAs applied to the budget.

Note 2: The 2020-21 Social Security expenditure and Block Grant Adjustment are outturn figures.

Note 3: Carer's Allowance Expenditure Forecast does not include Carer's Allowance Supplement expenditure.

Note 4: There are minor differences in the methodology used to calculate the SFC's spending forecasts and the BGA forecasts, which are based on expenditure outturn and OBR forecasts, so comparisons should be interpreted with caution.

Figures may not sum due to rounding.

Benefits Yet to Commence

Responsibility for Winter Fuel Payments has yet to be transferred to the Scottish Government and therefore these payments are not funded from within the Scottish Budget. The Department for Work and Pensions will continue to make these payments to people in Scotland for winter 2022-23. An update will be provided in due course.

Reconciliations and implications for the Scottish Budget

The forecasts for Scottish tax revenues and social security expenditure, and the corresponding BGAs, are based on the latest available information at the time of the Budget. Once outturn data are available, reconciliations are made to the Scottish Budget to ensure that the funding available ultimately corresponds to actual revenues and the BGAs based on the outturn data.

Reconciliations are made for both the revenues and the BGA for Income Tax. For Fully Devolved Taxes (LBTT and Scottish Landfill Tax), Social Security, and Non-Tax Revenues (Fines, Forfeitures and Fixed Penalties - FFFP), reconciliations are only made to the BGA element of funding.

In relation to Income Tax, a reconciliation for both revenues and the BGA for the 2019-20 financial year will be applied to the 2022-23 Scottish Budget. Updated forecasts for the other past years - 2020-21 and 2021-22 – do not have any immediate impact on the Scottish Budget. Under the Fiscal Framework, a single reconciliation takes place three years after the original Budget was set and the updated forecasts in the interim have no direct impact.

In relation to the Fully Devolved Taxes, Social Security benefits and FFFP, reconciliations for the BGAs for 2020-21 financial year will be applied to the 2022-23 Scottish Budget.

The Fully Devolved Taxes and Social Security BGAs are also subject to an additional in-year reconciliation which takes place within each financial year, based on the latest OBR forecasts. There is no in-year reconciliation for FFFP.

Income Tax

For Scottish Income Tax, outturn data is normally available around 16 months after the end of the financial year. Given this long lag of availability of outturn data, Income Tax revenue and BGAs are fixed for three years from the time the Budget is set. A single reconciliation is then applied to the Budget three financial years after the Budget is set, e.g the reconciliation for 2018-19 Income Tax was applied to the 2021-22 budget. Provisional outturn data for 2019-20 Income Tax was published 22 July 2021, which has been confirmed by HMRC's publication of its Trust Statement[22]. Table B.3 shows the confirmed 2019-20 Income Tax reconciliation applying to the 2022-23 Budget.

| 2022-23 Income Tax | Revenues | BGA* | Net Position |

|---|---|---|---|

| Forecast as of Budget 2019-20 | 11,684 | -11,501 | +182 |

| Outturn | 11,833 | -11,685 | +148 |

| Outturn against forecast | +149 | -184 | -34 |

* The BGA has been revised upward – this has a negative effect on net revenues.

Figures may not sum due to rounding.

The potential scale of the reconciliations applying to the 2023-24 and 2024-25 Budgets are shown in tables B.4 and B.5 using the latest forecasts.

| 2020-21 Income Tax | Revenues | BGA | Net Position | Forecast Reconciliation |

|---|---|---|---|---|

| Forecast as of Budget 2020-21 | 12,365 | -12,319 | +46 | |

| Latest forecast | 11,938 | -11,989 | -51 | -97 |

| Change | -427 | +330 |

Figures may not sum due to rounding.

| 2021-22 Income Tax | Revenues | BGA | Net Position | Forecast Reconciliation |

|---|---|---|---|---|

| Forecast as of Budget 2021-22 | 12,263 | -11,788 | +475 | |

| Latest forecast | 13,002 | -12,996 | +6 | -469 |

| Change | +739 | -1,208 |

Figures may not sum due to rounding.

Based on the latest forecasts, the reconciliation to the Scottish Budget 2023-24 for 2020-21 Income Tax is expected to be negative £97m. A reconciliation of negative £469 million is expected to apply to the Scottish Budget 2024-25 to account for 2021-22 Income Tax.

However, these forecasts are not certain and the final position will not be known for sure until outturn receipts are available for 2020-21 in summer 2022, and for 2021-22 in summer 2023.

Fully Devolved Taxes

Revenue Scotland manages and collects Land and Buildings Transaction Tax (LBTT) and Scottish Landfill Tax (SLfT) and these revenue streams feed in to the Scottish Budget as they are collected. There is no reconciliation required for these revenues; the Scottish Government manages any variance between what was forecast and actual revenues as part of its in-year budget management process. The latest 2021-22 revenue forecasts for LBTT and SLfT and the previous revenue forecasts are shown in Table B.6.

| LBTT | SFC Revenue Forecast – Budget 2021-22 | 586 |

|---|---|---|

| SFC Revenue Forecast – Budget 2022-23 | 720 | |

| Change | +134 | |

| SLfT | SFC Revenue Forecast – Budget 2021-22 | 88 |

| SFC Revenue Forecast – Budget 2022-23 | 123 | |

| Change | +35 |

Figures may not sum due to rounding.

The BGAs for these taxes are reconciled in two stages. An in-year reconciliation is made within the same financial year. This is usually on the basis of OBR forecasts produced alongside the UK Autumn Budget. The in-year reconciliations for 2021-22 LBTT and SLfT are shown in table B.7.

| LBTT | Forecast BGA – UK Spending Review November 2020 | -515 |

|---|---|---|

| Forecast BGA – 2022-23 UK Budget October 2021 | -620 | |

| In-year reconciliation to 2021-22 Budget | -104 | |

| SLfT | Forecast BGA – UK Spending Review November 2020 | -95 |

| Forecast BGA – 2022-23 UK Budget October 2021 | -90 | |

| In-year reconciliation to 2021-22 Budget | +5 |

Figures may not sum due to rounding.

As set out in Table B.8, the net effect on the Scottish Budget 2021-22 of the latest fully devolved revenue forecasts, when compared to the in-year BGA reconciliations, is +£71m, (comprising £30m for LBTT and £41m for SLfT).

| 91. Fully Devolved Tax 92. | 93. In-Year BGA Reconciliation | 94. Change in SFC revenue forecast from 2021-22 Scottish Budget | 95. Net Position |

|---|---|---|---|

| 96. LBTT | 97. -104 | 98. 134 | 99. +30 |

| 100. SLfT | 101. 5 | 102. 35 | 103. +41 |

| 104. TOTAL | 105. -99 | 106. +170 | 107. +71 |

108. Figures may not sum due to rounding

Outturn data becomes available in the autumn following the end of each financial year. Using these outturn figures, a final reconciliation is applied to the Block Grant in the financial year two years after the Budget was set. Table B.9 shows the final reconciliations for 2020-21 LBTT and SLfT BGAs applying to the 2022-23 Scottish Budget.

| LBTT | Forecast BGA – 2021-22 Scottish Budget January 20211 | -391 |

|---|---|---|

| Outturn | -397 | |

| Reconciliation to 2022-23 Budget2 | -6 | |

| SLfT | Forecast BGA – 2021-22 Scottish Budget January 20211 | -87 |

| Outturn | -87 | |

| Reconciliation to 2022-23 Budget2 | +0 |

Note 1: As a UK Budget had not been published at the time of the Scottish Budget in January 2021, provisional Block Grant Adjustments (BGAs) were used to inform the Scottish Budget as directed under the Fiscal Framework. Updated BGAs were produced at the UK Budget in March. However, the provisional BGAs were used to inform the Scottish Budget.

Note 2: The final BGA reconciliation effectively calculates the difference between the in-year forecast of the BGA (used to calculate the in-year reconciliation) and the outturn data.

Figures may not sum due to rounding.

Table B.10 shows the confirmed net effect on the budget for 2020-21 LBTT and SLfT and compares outturn to forecasts.

| Revenues | BGA | Net Position | ||

|---|---|---|---|---|

| LBTT | Forecast as of Budget 2020-21 | 641 | -557 | +85 |

| Outturn | 517 | -397 | +121 | |

| Outturn against forecast | -124 | +160 | +36 | |

| SLfT | Forecast as of Budget 2020-21 | 116 | -87 | +29 |

| Outturn | 107 | -87 | +20 | |

| Outturn against forecast | -9 | 0 | -9 | |

Figures may not sum due to rounding.

Social Security

The latest 2021-22 expenditure forecasts for Social Security and the previous expenditure forecasts are shown in Table B.11.

| Attendance allowance | SFC Expenditure Forecast – Budget 2021-22 | -550 |

|---|---|---|

| SFC Expenditure Forecast – Budget 2022-23 | -519 | |

| Change | +30 | |

| Personal independence payment | SFC Expenditure Forecast – Budget 2021-22 | -1669 |

| SFC Expenditure Forecast – Budget 2022-23 | -1734 | |

| Change | -65 | |

| Disability living allowance | SFC Expenditure Forecast – Budget 2021-22 | -696 |

| SFC Expenditure Forecast – Budget 2022-23 | -700 | |

| Change | -5 | |

| Carer's allowance | SFC Expenditure Forecast – Budget 2021-22 | -306 |

| SFC Expenditure Forecast – Budget 2022-23 | -301 | |

| Change | +5 | |

| Industrial injuries disablement scheme | SFC Expenditure Forecast – Budget 2021-22 | -80 |

| SFC Expenditure Forecast – Budget 2022-23 | -81 | |

| Change | -1 | |

| Severe disablement allowance | SFC Expenditure Forecast – Budget 2021-22 | -7 |

| SFC Expenditure Forecast – Budget 2022-23 | -7 | |

| Change | +0 | |

| Total social security | SFC Expenditure Forecast – Budget 2021-22 | -3,308 |

| SFC Expenditure Forecast – Budget 2022-23 | -3,343 | |

| Change | -34 |

Figures may not sum due to rounding.

As with the fully devolved taxes, the BGAs for benefits are reconciled in two stages. An in-year reconciliation is made within the same financial year. This is usually on the basis of OBR forecasts produced alongside the UK Autumn Budget. The in-year reconciliations to the 2021-22 Social Security BGAs are shown in Table B.12.

| Attendance allowance | Forecast BGA – UK Spending Review November 2020 | 546 |

|---|---|---|

| Forecast BGA – 2022-23 UK Budget October 2021 | 521 | |

| In-year reconciliation to 2021-22 Budget | -25 | |

| Personal independence payment | Forecast BGA – UK Spending Review November 2020 | 1,682 |

| Forecast BGA – 2022-23 UK Budget October 2021 | 1,723 | |

| In-year reconciliation to 2021-22 Budget | +42 | |

| Disability living allowance | Forecast BGA – UK Spending Review November 2020 | 685 |

| Forecast BGA – 2022-23 UK Budget October 2021 | 687 | |

| In-year reconciliation to 2021-22 Budget | +2 | |

| Carer's allowance | Forecast BGA – UK Spending Review November 2020 | 309 |

| Forecast BGA – 2022-23 UK Budget October 2021 | 295 | |

| In-year reconciliation to 2021-22 Budget | -14 | |

| Industrial injuries disablement scheme | Forecast BGA – UK Spending Review November 2020 | 81 |

| Forecast BGA – 2022-23 UK Budget October 2021 | 79 | |

| In-year reconciliation to 2021-22 Budget | -1 | |

| Severe disablement allowance | Forecast BGA – UK Spending Review November 2020 | 7 |

| Forecast BGA – 2022-23 UK Budget October 2021 | 7 | |

| In-year reconciliation to 2021-22 Budget | -1 | |

| Total social security | Forecast BGA – UK Spending Review November 2020 | 3,310 |

| Forecast BGA – 2022-23 UK Budget October 2021 | 3,313 | |

| In-year reconciliation to 2021-22 Budget | +3 |

Figures may not sum due to rounding.

Table B.13 sets out the net effect on the Scottish Budget 2021-22 of the latest total devolved social security expenditure forecasts when compared to the total in-year BGA reconciliations, is negative £31m.

| Fully Devolved Tax | In-Year BGA Reconciliation | Change in SFC expenditure forecast from 2021-22 Scottish Budget | Net Position |

|---|---|---|---|

| 117. Total social security benefits with a BGA1 | +3 | -34 | -31 |

1) Carer's Allowance, Attendance Allowance, Child Disability Payment, Disability Living Allowance, Adult Disability Payment, Industrial Injuries Disablement Allowance, Severe Disability Allowance

Figures may not sum due to rounding

Outturn data becomes available in the autumn following the end of each financial year. Using these outturn figures, a final reconciliation is applied to the Block Grant in the financial year two years after the Budget was set. Table B.14 shows the reconciliation for the 2020-21 Social Security BGAs applying to the 2022-23 Scottish Budget.

| Attendance allowance | Forecast BGA – 2021-22 Scottish Budget January 20211 | 531 |

|---|---|---|

| Outturn | 521 | |

| Reconciliation to 2022-23 Budget2 | -9 | |

| Personal independence payment | Forecast BGA – 2021-22 Scottish Budget January 20211 | 1,555 |

| Outturn | 1,585 | |

| Reconciliation to 2022-23 Budget2 | +30 | |

| Disability living allowance | Forecast BGA – 2021-22 Scottish Budget January 20211 | 719 |

| Outturn | 721 | |

| Reconciliation to 2022-23 Budget2 | +2 | |

| Carer's allowance | Forecast BGA – 2021-22 Scottish Budget January 20211 | 289 |

| Outturn | 291 | |

| Reconciliation to 2022-23 Budget2 | +1 | |

| Industrial injuries disablement scheme | Forecast BGA – 2021-22 Scottish Budget January 20211 | 84 |

| Outturn | 81 | |

| Reconciliation to 2022-23 Budget2 | -2 | |

| Severe disablement allowance | Forecast BGA – 2021-22 Scottish Budget January 20211 | 8 |

| Outturn | 8 | |

| Reconciliation to 2022-23 Budget2 | 0 | |

| Total social security | Forecast BGA – 2021-22 Scottish Budget January 20211 | 3,185 |

| Outturn | 3,207 | |

| Reconciliation to 2022-23 Budget2 | +22 |

Note 1: As a UK Budget had not been published at the time of the Scottish Budget in January, provisional Block Grant Adjustments (BGAs) were used to inform the Scottish Budget as directed under the Fiscal Framework. Updated BGAs were produced at the UK Budget in March. However, the provisional BGAs were used to inform the Scottish Budget.

Note 2: The final BGA reconciliation effectively calculates the difference between the in-year forecast of the BGA (used to calculate the in-year reconciliation) and the outturn data.

Figures may not sum due to rounding.

Table B.15 shows the confirmed net effect on the budget for 2020-21 Social Security benefits and compares outturn to forecasts.

| Expenditure | BGA | Net Position | ||

|---|---|---|---|---|

| Attendance allowance | Forecast as of Budget 2020-21 | -532 | 535 | +3 |

| Outturn | -528 | 521 | -6 | |

| Outturn against forecast | +5 | -14 | -9 | |

| Personal independence payment | Forecast as of Budget 2020-21 | -1,583 | 1,601 | +19 |

| Outturn | -1,626 | 1,585 | -41 | |

| Outturn against forecast | -43 | -16 | -60 | |

| Disability living allowance | Forecast as of Budget 2020-21 | -718 | 669 | -49 |

| Outturn | -722 | 721 | -1 | |

| Outturn against forecast | -4 | +52 | +48 | |

| Carer's allowance | Forecast as of Budget 2020-21 | -292 | 303 | +12 |

| Outturn | -296 | 291 | -5 | |

| Outturn against forecast | -4 | -13 | -17 | |

| Industrial injuries disablement scheme | Forecast as of Budget 2020-21 | -80 | 85 | +5 |

| Outturn | -83 | 81 | -1 | |

| Outturn against forecast | -2 | -4 | -6 | |

| Severe disablement allowance | Forecast as of Budget 2020-21 | -7 | 9 | +1 |

| Outturn | -7 | 8 | +0 | |

| Outturn against forecast | +0 | -1 | -1 | |

| Total social security | Forecast as of Budget 2020-21 | -3,213 | 3,203 | -10 |

| Outturn | -3,262 | 3,207 | -55 | |

| Outturn against forecast | -49 | +5 | -45 | |

Figures may not sum due to rounding.

Note 1: There are minor differences in the methodology used to calculate the SFC's spending forecasts and the BGA forecasts, which are based on expenditure outturn and OBR forecasts, so comparisons should be interpreted with caution

Non-Tax revenue

Fines, Forfeitures and Fixed Penalties

Revenue from Fines, Forfeitures and Fixed Penalties (FFFP) is paid into the Scottish Consolidated Fund after being collected by the Scottish Courts and Tribunals Service. No reconciliation takes place for revenue, as the Scottish Government deals with any variation between forecast and receipts through in-year budget management. The SFC does not provide revenue forecasts for FFFP and instead the Scottish Government calculates its own estimates.

The latest Scottish Government 2021-22 revenue forecast for FFFP and the previous revenue forecasts are shown in Table B.16.

| FFFP | SG Revenue Forecast – Budget 2021-22 | 25 |

|---|---|---|

| SG Revenue Forecast – Budget 2022-23 | 19 | |

| Change | -6 |

Figures may not sum due to rounding.

Unlike the devolved taxes, there is only one round of reconciliation for the BGA. Outturn data are normally available three months after the end of the financial year, and the reconciliation is applied to the Block Grant for the financial year thereafter (i.e. two years after the Budget was set).

Table B.17 shows the final reconciliation for the 2020-21 FFFP BGA applying to the 2022-23 Scottish Budget.

| FFFP | Forecast BGA – Budget 2020-21 | -24 |

|---|---|---|

| Outturn | -20 | |

| Reconciliation to 2022-23 Budget | +4 |

Figures may not sum due to rounding.

Table B.18 shows the confirmed net effect on the budget for 2020-21 FFFP and compares outturn to forecasts.

| Revenues | BGA | Net Position | ||

|---|---|---|---|---|

| FFFP | Forecast as of Budget 2020-21 | 25 | -24 | +1 |

| Outturn | 14 | -20 | -5 | |

| Outturn against forecast | -11 | +4 | -7 | |

Figures may not sum due to rounding.

Proceeds of Crime

Revenue seized under the Proceeds of Crime Act 2002 is also subject to a BGA. The basis on which this is carried out is currently the subject of dispute between the Scottish and UK Governments and the BGA remains at -£4m while the dispute remains unresolved.[23] The Scottish and UK Governments agreed to consider this issue as part of the review of the Fiscal Framework.

Final outturn revenue recovered under the Proceeds of Crime Act in 2020-21 is £5.2 million. The Scottish Government receives all revenues recovered under the Proceeds of Crime Act, however, outturn revenues are hypothecated for spend on community projects.[24] Due to this hypothecation of funds and the negative £4 million BGA, the net position for the Scottish Budget is negative £4 million while this BGA remains in force.

No reconciliation takes place while the BGA remains the subject of dispute between the Scottish and UK Governments.

Reconciliations applying to 2022-23 Budget

Table B.19 sets out the reconciliations which will be applied to the 2022-23 Budget.

| Income Tax 2019-20 | -34 | |

|---|---|---|

| Of which: | ||

| Final revenue reconciliation | +149 | |

| Final BGA reconciliation | -184 | |

| LBTT 2020-21 BGA reconciliation | -6 | |

| SLfT 2020-21 BGA reconciliation | +0 | |

| FFFP 2020-21 BGA reconciliation | +4 | |

| PoC 2020-21 BGA reconciliation | N/A | |

| Social Security 2020-21 BGA reconciliation | +22 | |

| Total Reconciliation Requirement | -14.7 |

Sources of Data

To view the various sources of data for Tax and Social Security that have been used to compile this Annex B, please see the data annex in the Fiscal Framework factsheet.

Capital Borrowing

The 2022-23 Scottish Budget confirmed the intention to borrow the annual maximum of £450 million capital, assumed to be over a period of 20 years. It was also assumed that £300m capital borrowing would be taken in 2023-24. Final decisions on all future borrowing will be taken over the course of the applicable financial years.

Chapter 5 sets out the Scottish Government's policy of borrowing between £250 million and £450 million over the remaining period of the National Infrastructure Mission.

On the basis of existing and planned borrowing included in the table, the Scottish Government will have accumulated £2.42 billion in capital debt by the end of 2022-23, 81% of its overall limit. However, as repayments of principle increase over time this ensures sufficient borrowing headroom will be available to support the National Infrastructure Mission in subsequent financial years.

| £million | 2017-18 | 2018-19 | 2019-20 | 2020-21 | 2021-22 | 2022-23 | 2023-24 | 2024-25 | 2025-26 | 2026-27 |

|---|---|---|---|---|---|---|---|---|---|---|

| Debt Stock at start of Year | 283 | 607 | 1,036 | 1,258 | 1,617 | 1,744 | 2,064 | 2,421 | 2,609 | 2,730 |

| New In Year Borrowing | 450 | 250 | 405 | 200 | 400 | 450 | 300 | 250 | 250 | - |

| Principal Repayments | - | 7 | 26 | 52 | 60 | 64 | 65 | 65 | 66 | 67 |

| Interest Repayments | - | 8 | 11 | 13 | 14 | 14 | 13 | 12 | 12 | 11 |

| Existing Resource Cost | - | 15 | 37 | 64 | 74 | 78 | 78 | 78 | 78 | 78 |

| Resource Cost of Projected Borrowing | - | - | - | - | - | 14 | 40 | 61 | 91 | 106 |

| Projected Total Resource Cost | 0 | 15 | 37 | 64 | 74 | 92 | 117 | 139 | 168 | 184 |

| Debt Stock at end of Year | 1,036 | 1,258 | 1,617 | 1744. | 2,064 | 2,421 | 2,609 | 2,730 | 2,829 | 2,661 |

| Percentage of Debt Cap | 35% | 42% | 54% | 58% | 69% | 81% | 87% | 91% | 94% | 89% |

| Notional Borrowing Repayments | 9.4 | 20.5 | 20.5 | 20.5 | 20.5 | 20.5 | 20.5 | 20.5 | 20.5 | 20.5 |

| Headroom | 1,964 | 1,742 | 1,383 | 1,256 | 936 | 579 | 391 | 270 | 171 | 339 |

*New In Year Borrowing from 2021-22 is projected borrowing based on the current Central Scenario.

Resource Borrowing

As set out in Chapter 5, the Scottish Government will make full use of resource borrowing in 2022-23. Table B.21 below shows the full budget impact of borrowing and reconciliations over the period.

| 2020-21 | 2021-22 | 2022-23 | 2023-24 | 2024-25 | 2025-26 | |

|---|---|---|---|---|---|---|

| Known and Forecast Reconciliations | - 207 | -319 | -15 | -97 | -470 | - |

| Planned Resource Borrowing | 207 | 319 | 15 | 97 | 300 | - |

| Projected Resource Cost of Resource Borrowing | - | 21 | 76 | 109 | 121 | 164 |

| Net Impact | - | 21 | 76 | 109 | -48 | 164 |

| YOY Net Impact | 21 | 55 | 33 | -157 | 212 |

The incremental impact of resource borrowing, the costs of resource borrowing and known and forecast Income Tax reconciliations is as follows:

- The projected resource cost of borrowing line comprises repayments of both principal and interest, both of which impact the resource budget.

- All drawdowns are based on National Loans Fund (NLF) annuity structure loans, this is the only source of resource borrowing available to the Scottish Government under the Fiscal Framework.

- These loans are priced at 11 basis points above the equivalent UK par Gilt yield. Assumptions in Table B.21 use the implied forward rates as of 23 November 2021 plus a premium of 50 basis points.

- NLF annuity loans have principal deferred in the first (semi-annual repayment) period.

- A five-year tenor is assumed in all cases (the maximum allowable under the Fiscal Framework).

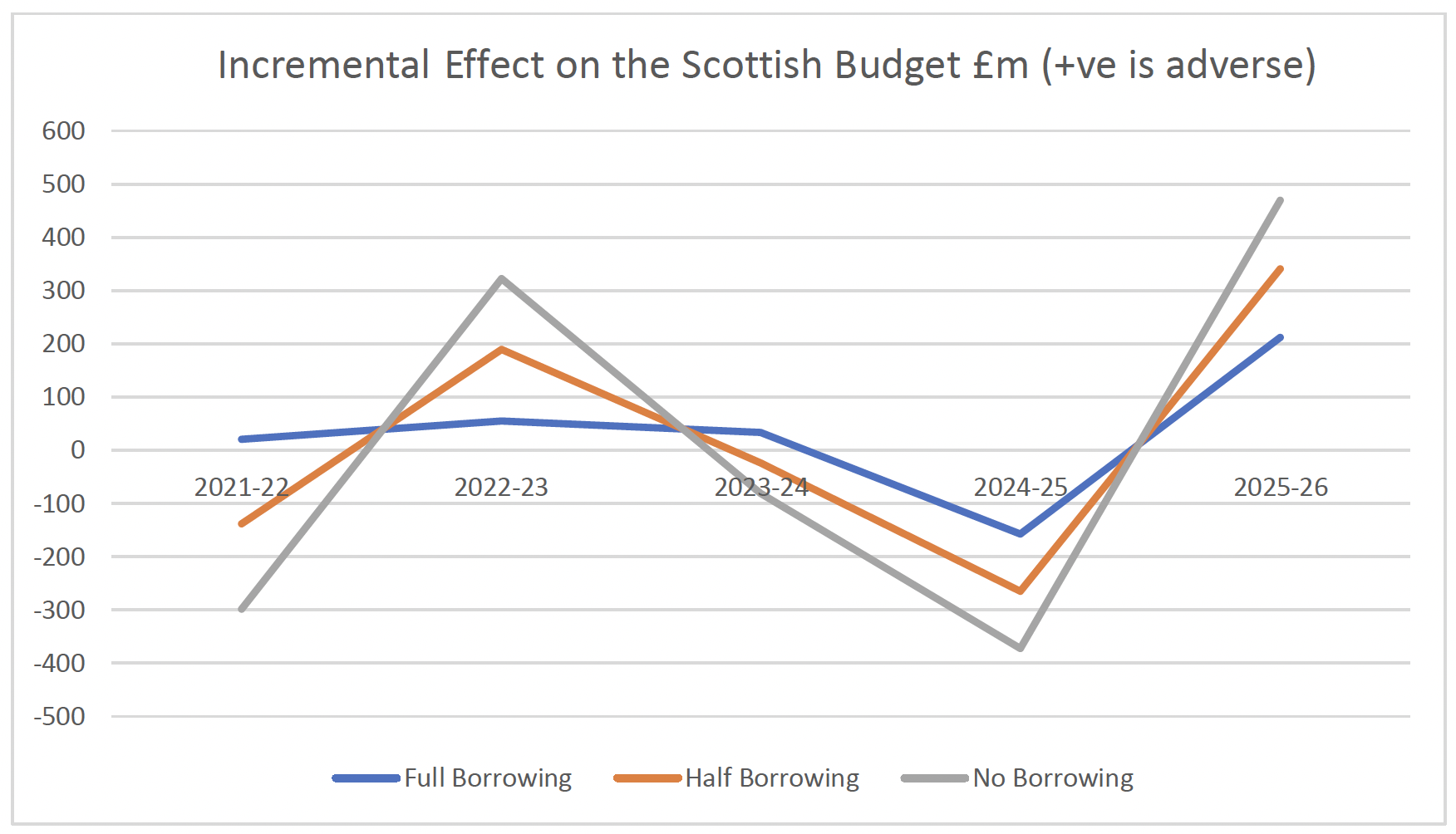

As stated in 4.1.2 The Scottish Government will assess all planned Resource Borrowing decisions to smoothen the funding trajectory over five years. The graphs below demonstrate what this trajectory would look like under three scenarios:

- Borrowing the full allowance – as per table above

- Borrowing half the available allowance

- Borrowing nothing

In the case of 'no borrowing' the swings in the funding position are most pronounced for both budgets. The graphs below show the impact in the original and future budget years, taking into consideration actual or expected borrowing for reconciliations in each of the years as well as repayment of borrowing and interest in subsequent fiscal years.

Note: Positive values connote reconciliation requirements and repayments which reduce the budget.

Contact

Email: sophie.osborn@gov.scot