The Scottish Government's Medium-Term Financial Strategy

This is the sixth Medium-Term Financial Strategy (MTFS) published by the Scottish Government and provides the context for the Scottish Budget and the Scottish Parliament.

4. Scotland's Spending Outlook

4.1 Resource Spending Outlook

The 2022 MTFS was published alongside the Resource Spending Review (RSR), which set out the Scottish Government's resource spending plans until 2026-27 and provided a strategic framework for the Scottish Government, its public bodies and other delivery partners to plan effectively for the future. The MTFS recognised the challenging and volatile economic and fiscal context for the RSR, which was published in a week when inflation reached a then 40-year high of 9%.

By the end of 2022, inflation had peaked at 11.1%, the highest UK rate since 1981. This has had a severe impact on business and households, and the OBR were forecasting at the time that average real household disposable income (which is often used as a measure of living standards) would fall by 7.1% in real terms from 2021-22 to 2023-24. In the Emergency Budget Review (EBR) in November 2022 and in setting the 2023-24 Budget, the Scottish Government chose to use its fiscal powers to mitigate the pressures being felt by people in Scotland and support our public services. Social Security benefits were uprated by 10.1% - the Consumer Price Index (CPI) rate in September 2022, when benefits rates are reviewed - to reflect the increased cost of living, an additional £1 billion was allocated to the health and social care budget, and over £900 million was reallocated to enhance public sector pay awards.

In all, the Budget set in December for 2023-24 was £1.7 billion higher than envisaged at the time of the RSR in May 2022, supported by changes in income tax and LBTT which asked those who are best able to contribute more to pay more.

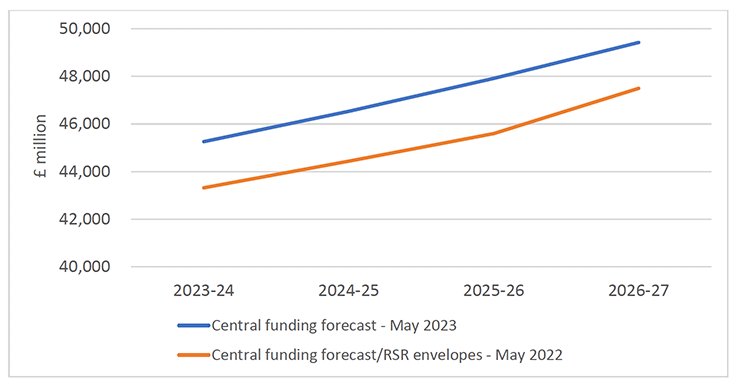

These decisions have a recurring impact on the Scottish Budget and have changed both spending and funding baselines. Figure and Table 12 illustrates the increase in the central funding outlook compared to the funding outlook at the time of the RSR. Scottish Government spending plans as reflected in the RSR were set within the central funding outlook. The funding outlook is explored in Chapter 3.

Source: Scottish Government

| 2023-24 | 2024-25 | 2025-26 | 2026-27 | |

|---|---|---|---|---|

| Central funding outlook/RSR envelopes - May 2022 | 43,321 | 44,439 | 45,600 | 47,498 |

| Central funding outlook - May 2023 | 45,260 | 46,535 | 47,917 | 49,415 |

Source: Scottish Government, SFC, OBR

This chapter will explore the drivers of growth in public spending in Scotland from the starting point of the 2023-24 Budget. This approach assumes, for the purpose of illustrating the drivers of public spending and pressures on the Scottish Budget, that the Scottish Government's current policies and services continue. Chapter 1 sets out the Scottish Government's strategy to manage the fiscal challenge and the policy choices we have ahead of us.

Underpinning the spending outlook is the OBR forecast of inflation. Growth in public spending is usually measured against the GDP deflators published quarterly by the OBR, and we have assumed that, in general, public spending is constant in real terms – i.e. grows in line with the GDP deflators. The OBR forecasts that inflation under this measure will fall rapidly from 5.7% in 2022-23 to 2.5% in 2023-24, and will stabilise at under 2% during the forecast period of this MTFS (Table 13). This means that, while the effects of high inflation seen in the past year will have a lasting effect on the level of public spending, that rate of growth is unlikely to be sustained. Section 4.3 explores spending risks, including the impact on the Scottish Budget if inflation does not reduce as forecast by the OBR.

| 2024-25 | 2025-26 | 2026-27 | 2027-28 | |

|---|---|---|---|---|

| Year-on-year growth | 1.6% | 1.0% | 1.2% | 1.7% |

Source: OBR

There are elements of the Scottish Budget where GDP deflators may not fully capture the inflationary pressures experienced by the Scottish public sector, and we expect greater pressure on public spending. These are explored below.

4.1.1 Pay

Pay accounts for over £24 billion of resource expenditure across the devolved public sector in Scotland (including Local Government).

The RSR spending plans assumed that pay awards would average 2% a year across the public sector, which was based on the Scottish Government's 2022-23 Pay Policy - published in December 2021 – which established pay parameters equivalent to a 1.6% pay award for those bodies covered by the Pay Policy. However, circumstances swiftly changed and pay awards (excluding pay progression) averaged around 6.4% in 2022-23 as Ministers sought to set fair pay deals to support public sector workers through the cost of living crisis and avoid costly disruption to public services from industrial action. These deals included the 7% equivalent average pay award for NHS Agenda for Change, and Local Government staff.

The Scottish Government's 2023-24 Public Sector Pay Strategy published on 22 March 2023[35] sets the framework to deliver fair, affordable pay awards, and a sustainable workforce to drive innovative and efficient public services. Each public body covered by the Pay Strategy must ensure their pay proposals are affordable and sustainable within their financial settlement for 2023-24, drawing as appropriate on business efficiencies and workforce changes as part of ongoing public service re-design and wider reform.

The key features of the 2023-24 Public Sector Pay Strategy are:

- the implementation of the real Living Wage rate of £10.90 per hour, including internships and Modern Apprentices;

- a suggested cash underpin of £1,500 for public sector workers who earn £25,000 or less;

- pay uplift for Chief Executives is capped at the same cash amount as the lowest paid;

- setting a pay award floor of 2%; and

- recommending a central metric of 3.5% and setting both an award ceiling and pay envelope maximum of 5%.

The high rate of inflation has driven the growth in public sector pay. The Office for National Statistics (ONS) and OBR forecast that inflation will drop below the Bank of England's 2% inflation target from 2024-25. As a result, pay growth is assumed to return to more normal levels between 2024-25 and 2027-28, at a level which is consistent with assumptions made in the RSR. To illustrate future pay bill costs across the devolved public sector, three theoretical public sector pay award scenarios are modelled below (see Table 14).

| Baseline | |||||

|---|---|---|---|---|---|

| (2023-24) | 2024-25 | 2025-26 | 2026-27 | 2027-28 | |

| Illustration of 2% pay award in 2023-24, and 1% pay award from 2024-25 onwards | |||||

| Total | 24,306 | 24,549 | 24,795 | 25,042 | 25,293 |

| Additional cost | 243 | 245 | 248 | 250 | |

| Illustration of 3.5% pay award in 2023-24, and 2% pay award from 2024-25 onwards | |||||

| Total | 24,477 | 24,966 | 25,465 | 25,975 | 26,494 |

| Additional cost including Basic Award | 490 | 499 | 509 | 519 | |

| Illustration of 5% pay award in 2023-24, and 3% pay award from 2024-25 onwards | |||||

| Total | 24,617 | 25,355 | 26,116 | 26,899 | 27,706 |

| Additional cost including Basic Award | 738 | 761 | 783 | 807 | |

Notes: These projections include the cost of the Local Government workforce. 2023-24 costs reflect agreed pay settlements for Health, Fire and Teachers which are above 3.5%. This table assumes workforce numbers remain at 2023-24 levels throughout the period. Figures may not sum due to rounding.

Source: Scottish Government

4.1.2 Workforce

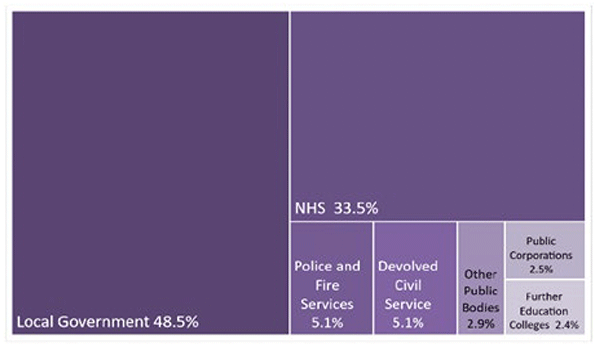

The devolved public sector full-time equivalent workforce (FTE) is around 460,400 FTE, and has historically grown by around 2% per annum over the last 5 years.

Employment (headcount) in the public sector in Scotland was 594,500 as of December 2022, representing over a fifth (21.9%) of all employment in Scotland.[36] The proportion of people in employment in the public sector across the UK as a whole was 17.7%

Of the total number of people employed in the public sector in Scotland, just over 90% are working in the devolved public sector.

The breakdown of the devolved public sector (headcount) is illustrated in Figure 13. Over 80% of people in the devolved public sector are employed in either Local Government or the NHS.

Note: Totals may not equal the sum of the individual parts due to rounding

Source: Scottish Government

For many public bodies, the pay bill is the most significant element of their budget and the Pay Strategy requires all public bodies to satisfy themselves of the affordability and sustainability of the pay awards within existing budget allocations. The RSR launched a programme of work to pursue a twin-track approach to reform, which asks public bodies to identify opportunities for both further efficiencies and joined-up service delivery that directs collective resources towards shared priorities. This requires and supports public bodies to consider the size and shape of the workforce, alongside opportunities around, for example, digital reform, revenue generation, estates rationalisation and improved procurement.

As a result of this ongoing reform and the rapid growth in the pay bill in 2023-24, we have assumed that public bodies will have both the need, and the tools to manage growth in their workforces at a lower rate than we have seen in recent years. As such, we have illustrated an overall 1.1% per annum workforce growth assumption from 2023-24 to 2027-28 in the central scenario, with the lower scenario at 0.3%, and an upper scenario at 2.2% per annum, which takes account of variable growth rates across the public sector (see Table 15). We have assumed higher than average rates of growth for the Health workforce in each scenario. The actual rate of growth will be determined by a number of factors including affordability, service demand and labour supply.

Where a reduction in workforce is required for a public body to remain sustainable, we would expect this to be through natural turnover wherever possible and we restated our commitment to no compulsory redundancies in this year's Public Sector Pay Strategy.[37] Individual public bodies must ensure their policies, practices and systems comply with their equalities and Fairer Scotland obligations.

| Baseline (2023-24) | 2024-25 | 2025-26 | 2026-27 | 2027-28 | |

|---|---|---|---|---|---|

| Low Scenario - 2% pay award in 2023-24, and 1% pay award from 2024-25 onwards, 0.3% workforce growth | |||||

| Total | 24,306 | 24,627 | 24,953 | 25,284 | 25,619 |

| Difference from Central Scenario | -171 | -613 | -1,075 | –1,556 | -2,058 |

| Central scenario - 3.5% pay award in 2023-24, and 2% pay award from 2024-25 onwards, 1.1% workforce growth | |||||

| Total | 24,477 | 25,240 | 26,028 | 26,840 | 27,677 |

| High Scenario - 5% pay award in 2023-24, and 3% pay award from 2024-25 onwards, 2.2% workforce growth | |||||

| Total | 24,617 | 25,738 | 26,912 | 28,140 | 29,426 |

| Difference from Central Scenario | 140 | 498 | 884 | 1,300 | 1,749 |

Notes: These projections include the cost of the Local Government workforce. 2023-24 costs reflect agreed pay settlements for Health, Fire and Teachers which are above 3.5%.

Source: Scottish Government

4.1.3 Health and social care

While key cost drivers such as demographics and inflation affect all areas of public spending, the impact is particularly pronounced for health and social care. For example, recent pressures relating to pay, drugs and medicine costs have exceeded previously modelled growth, and in contrast to other areas technological and scientific advances lead to increased rather than decreased costs as both expectations and demand grow. This is especially relevant in the context of an ageing population, as explored in section 4.3.3, which is likely to create growing physical and mental healthcare needs and a greater demand on social care services. Overall, the annual disease burden is forecast to increase by 21% for the Scottish population over the next two decades.[38] These changes in disease burden are based only on projected demographic change and assume stable prevalence of disease but provide helpful insights to demonstrate the scale of increased pressures and efforts needed to mitigate the underlying causes of ill health and support people to live longer lives in good health.

Considering these cost pressures, our previous modelling assumptions of 3.5% in the 2018 Medium Term Financial Framework for Health and Social Care, and the SFC's recent Fiscal Sustainability Report, which projected that health spending would grow more quickly than other public services, we have applied a higher growth rate of 4% per annum to Health and Social Care expenditure.

4.1.4 Social security

The Scottish Government is committed to building a modern social security system with dignity, fairness and respect at its heart. Social security is key to helping us substantially reduce levels of child poverty in Scotland and provides vital financial support to households, including those struggling because of the cost of living crisis.

To maintain the real terms value of Scottish Benefits, the Scottish Government uprated all Scottish benefits by 10.1% from 1 April 2023, including those without a statutory requirement to uprate. Benefits are uprated by the CPI rate in the previous September, so reflect a higher rate of inflation than the GDP deflators applied to our modelling of other public spending. To further support low-income families with children, the Scottish Child Payment was increased from £20 per week per eligible child to £25 when it was rolled out to eligible children under 16 in November 2022.

High rates of inflation have not otherwise had a major effect on demand for devolved social security benefits in Scotland. The main reason for this is that disability benefits account for the majority of devolved social security expenditure (80% in 2023-24), and eligibility for these benefits is less sensitive to macroeconomic changes than for income replacement benefits, such as Universal Credit, which are mainly delivered by the Department for Work and Pensions (DWP) in Scotland. Demand for disability benefits fluctuates more directly with changes in the 'health of the nation'. In its December 2022 forecast, for example, the SFC highlighted a significant increase in demand for disability benefits across the UK, including Personal Independence Payments, commenting that reasons for this likely increase could include factors such as increased NHS waiting times following the Covid-19 pandemic, the increasing number of people who are economically inactive because of long-term sickness, and financial pressures on individuals in the cost of living crisis. The same factors are likely to apply to the demand for Scottish disability benefits.

These developments, together with certain revisions to modelling assumptions, are taken into account by the SFC in preparing revised social security expenditure forecasts. As shown in Table 16, in the latest forecast, expenditure will increase by around £0.5 billion a year from 2024-25 above the forecast which informed spending plans in the RSR in May 2022. However, a substantial proportion of the funding for this additional expenditure, for example, statutory uprating requirements and health related increases in expenditure on disability benefits is provided by the UK Government through Block Grant Adjustments (BGAs). In each year of the RSR, the total increase in forecast expenditure compared to the May 2022 forecast is funded entirely through increases in BGA funding forecasts, as shown in Table 17, reflecting that the increases in expenditure are largely due to wider economic and UK policy changes.

| £million | 2023-24 | 2024-25 | 2025-26 | 2026-27 |

|---|---|---|---|---|

| Resource Spending Review - May 2022 | 5,072 | 5,725 | 6,108 | 6,490 |

| Latest forecasts - May 2023 | 5,290 | 6,192 | 6,638 | 7,000 |

| Growth | +218 | +467 | +530 | +510 |

Source: Scottish Government, SFC

| £million | 2023-24 | 2024-25 | 2025-26 | 2026-27 |

|---|---|---|---|---|

| Resource Spending Review - May 2022 * | 4,082 | 4,574 | 4,825 | 5,103 |

| Latest forecasts - May 2023 ** | 4,434 | 5,132 | 5,435 | 5,697 |

| Growth | +352 | +558 | +610 | +594 |

* Based on the OBR's March 2022 forecast

** Based on the OBR's March 2023 forecast

Forecast social security expenditure also covers new Scottish benefits for which there are no UK equivalents, such as Scottish Child Payment, and the replacement of existing DWP benefits in Scotland. The SFC currently forecast the total additional investment from Scottish benefits compared to BGA funding as rising from £756 million in 2023-24 to £1,274 million in 2027-28. This difference will need to be funded from elsewhere within the Scottish Budget, through tax and spending changes. It will help those with the greatest need, supporting low-income families with their living costs and older people to heat their homes in winter, and enable disabled people to live full and independent lives.

New social security benefits, which are only available in Scotland, account for £620 million of this forecast additional expenditure in 2027-28. This includes forecast expenditure of £436 million on Scottish Child Payment. This is a significant investment which the Scottish Government has made in the people of Scotland. It is key to helping us substantially reduce levels of child poverty in Scotland and drive progress toward the 2030 targets.

Deliberate policy choices made to benefits as they are devolved, coupled with improvements in delivery of replacement benefits driven by a social security system founded on the principles of dignity, fairness, and respect are forecast by the SFC to account for the remaining £654 million forecast additional expenditure in 2027-28. Much of this results from improvements made to Adult Disability Payment (ADP), which replaces Personal Independence Payment in Scotland. Changes include reforms to improve the experience of people applying for the benefit, introduction of longer awards in appropriate circumstances, and changes to terminal illness rules.

ADP has been in place nationally for less than a year and it is not yet possible to draw any firm conclusions on how the operation of the new system in practice will change how much is spent nationally in Scotland on ADP specifically or disability benefits more generally. The SFC recognises that elements of the disability payment forecasts contain more judgements than other parts of the forecast and are therefore more uncertain, with uncertainty growing towards the latter part of the forecast period. This introduces a significant amount of uncertainty into the Scottish Government's spending projections and into the management of the public finances over the medium-term.

4.1.5 Resource spending outlook: summary

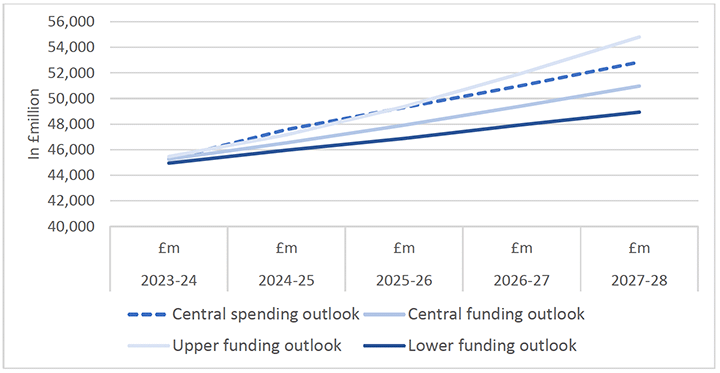

Applying historic rates of growth to the 2023-24 baseline suggests a central resource spending scenario which increases from £45.2 billion in 2023-24 to £52.8 billion in 2027-28. Forecast growth averages 3.6% per annum in the final years of our medium-term horizon, which is higher than forecast inflation of 1% - 1.7% from year to year and, more significantly for the public finance outlook, higher than forecast funding growth which averages 3.1% under the central funding scenario for 2025-26 to 2027-28.

This small divergence in the central funding and spending scenarios compounds the particular challenge we face in 2024-25 when, from a balanced outturn in 2023-24, forecast spending increases by 5.1% due in part to the £0.9 billion forecast increase in social security expenditure from year-to-year due to the continuing effect of high inflation and the launch of three new benefits. In the same year, we face significant funding constraints due to an expected negative tax reconciliation and limited growth in the block grant in the final year of the UK Spending Review. This means our central spending outlook for 2024-25 is £1.0 billion (2%) higher than the central funding scenario and £409 million higher than the high funding scenario.

Source: Scottish Government

| 2023-24 | 2024-25 | 2025-26 | 2026-27 | 2027-28 | |

|---|---|---|---|---|---|

| Central spending outlook | 45,260 | 47,575 | 49,304 | 51,013 | 52,846 |

| Central funding outlook | 45,260 | 46,535 | 47,917 | 49,415 | 50,971 |

| Surplus/(Shortfall) | 0 | -1,040 | -1,387 | -1,598 | -1,875 |

| Upside funding scenario | 45,466 | 47,166 | 49,363 | 51,973 | 54,805 |

| Surplus/(Shortfall) | 206 | -409 | 59 | 960 | 1,959 |

| Downside funding scenario | 44,951 | 45,965 | 46,882 | 47,945 | 48,933 |

| Surplus/(Shortfall) | -309 | -1,610 | -2,422 | -3,068 | -3,913 |

Source: Scottish Government, SFC, OBR

The Scottish Government is required to balance its budget each financial year, so must absorb these pressures. The Emergency Budget Review (EBR)[39] in November 2022 is an example of the quick response required by the Scottish Government when fiscal risk materialises in-year. With no ability to increase borrowing or change income tax rates in the middle of a financial year, Ministers delivered in-year savings through the EBR to meet the additional costs arising from high inflation and the war in Ukraine – neither of which could have been foreseen when the Budget was set in December 2021.

In the later years of this forecast period the central spending outlook lies between the central and the upper funding scenarios. This suggests that if funding is at the upper end of forecasts and spending is held at the central outlook, there may be flexibility within the annual budget to increase investment in public services. However, it is vital that we manage Scottish public finances on a sustainable trajectory and - while seeking to strengthen revenues by growing our economy and therefore our tax base – we must recognise and prepare for the fiscal challenge we face. Chapter 1 set out the Scottish Government's approach to managing the upward pressures on public spending within the fiscal outlook

4.2 Capital Spending Outlook

The Policy Prospectus 'Equality, opportunity, community: New leadership – A fresh start',[40] sets out the importance of achieving and maintaining a balanced budget, while prioritising capital investment to reach net zero and maintain high quality public infrastructure and services across Scotland. These align with the priorities the Scottish Government used to frame the 2021 Infrastructure Investment Plan (IIP)[41] which outlines several projects to reduce Scotland's carbon emissions, increase our resilience to climate change and improve our local infrastructure.

As discussed in the May 2022 Targeted Review of the Capital Spending Review (CSR),[42] there are several pressures facing the Scottish capital programme. These include reopening the economy in the aftermath of COVID-19; new commitments to further address the global climate crisis; shortages in the supply of construction materials which had been exacerbated by the crisis in Ukraine; and labour shortages driven by the UK's exit from the European Union. These challenges continue to impact the capital budget, with construction supply chain issues coinciding with the sustained high inflation levels, which peaked in the construction sector at around 25% last summer.

Since publication of last year's MTFS there have been significant changes to the economic climate with sustained high inflation increasing interest rates and making borrowing more expensive. The increased cost of borrowing, exacerbated by supply chain issues and material inflation has resulted in revenue financed investments being more expensive than expected, and therefore impacting value for money assessments.

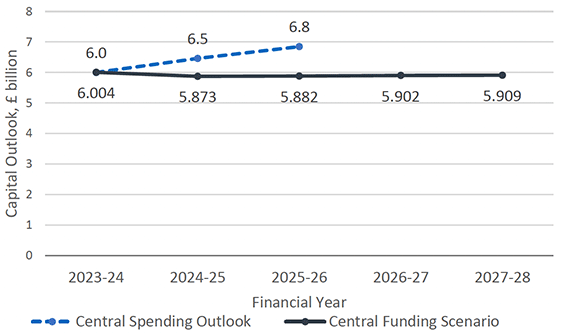

The combination of these factors and the real-terms fall in capital funding will have an impact on our ability to achieve the target set out in the National Infrastructure Mission (NIM). The NIM was introduced with the aim of raising Scottish infrastructure investment to £6.86 billion in 2025-26 to protect and create jobs in the short term and support inclusive economic growth and productivity in the long term. However, the current trajectory of funding from the UK Government and the higher cost of revenue financed investments mean that it is likely to take longer than expected to achieve the target.

Figure 15 shows that the projected capital funding (excluding Financial Transactions (FTs)) for 2023-24 to 2027-28 remains at around £5.9 billion per year, while the spending outlook for the remainder of the CSR period (up to 2025-26) steadily increases, resulting in a projected difference between funding and expected need in the region of £900 million for 2025-26. This corresponds to a 16% funding gap in 2025-26 and is driven by the prudent overcommitments identified in the Targeted Review of the Capital Spending Review and the current estimate of the inflationary pressures.

Source: Scottish Government, OBR

The challenges outlined above mean that we cannot deliver all of the Scottish Government's capital commitments within the funding available and to the original planned timescales without access to additional capital funding.

As set out in Chapter 1, the Scottish Government will publish refreshed multi-year spending envelopes for capital alongside the 2024-25 Budget, and extend the CSR and IIP period by one year to 2026-27. This will reset the spending envelopes published in CSR to reflect the new economic reality and our three critical missions for this parliament.

The Scottish Government will continue to press the UK Government to use the levers at its disposal to help mitigate the current market conditions and support infrastructure investment, but without further funding and associated fiscal flexibility through enhanced borrowing powers, tough decisions will need to be made to reprioritise the pipeline of projects set out in the IIP.

As we undertake this review and prioritisation exercise in advance of the 2024-25 Budget, we will prioritise capital spending which supports employment and the economy through the Scottish Government's infrastructure plans, and which has greatest impact on realising our three missions. This will move us towards achieving net zero and underpins the provision of high-quality public infrastructure and services across Scotland, within the budget available.

4.3 Spending Risks

4.3.1 Inflation

The modelling of the spending outlook in section 4.1.5 is underpinned by the latest forecasts from the OBR which show inflation falling below 2% by the end of 2023-24, and continuing at that lower rate. However, as considered in section 2.2, there is considerable uncertainty in the inflation forecast.

Experience of the financial years 2022-23 and 2023-24 has illustrated the significant impact sustained high inflation may have on the spending outlook. Across the public sector, and particularly on infrastructure programmes, we – like businesses and organisations across Scotland - have seen high inflation erode our buying power during the cost crisis. As a result, the amount we pay for the largest elements of our budget – employees and social security benefits – has increased.

Any additional expenditure arising as a result of sustained inflation must be managed within the limits of the Scottish Government's existing fiscal powers, and further stretch the fiscal challenge outlined in Chapter 1 and above.

4.3.2 Demand-led expenditure

Demand-led expenditure appears across the public sector and will always carry a degree of forecast risk. Budgets reflect expected levels of demand for, for example, concessionary travel, but expenditure will vary according to the number of people who are eligible for, and choose or need to use the service, and will be affected by behavioural and economic factors. This has become a more significant feature of the Scottish Budget with the devolution of Social Security, which is now the third largest area of public spending in Scotland, after Health and Local Government. Under the Fiscal Framework, these programmes must all be managed within the resource budget and the Scottish Government has limited levers to manage demand-led volatility. Increases in demand-led expenditure therefore reduce the funding the Scottish Budget has available for other programmes.

Expenditure on social security benefits is variable, as it is determined by the number of eligible people who apply for support, all of whom must be paid at the rate set in the respective policy. Budget allocations are based on the SFC's forecasts rather than spending limits, and the Scottish Government must meet social security expenditure as it arises, even if it differs from the SFC forecast used to set the initial medium-term spending plans or the Budget.

The risk relating to social security spending is exacerbated by the uncertainty in the related BGAs, as it relates to social security policy in the rest of the UK. Changes in either UK Government policy relating to devolved benefits, or the OBR's forecasts of benefit demand in the rest of the UK, can affect the funding available to the Scottish Government in either direction, and the impact of social security spending on the wider spending priorities. The value of the BGA is currently around 80% of social security spending, and to this point has been a source of stability as trends in UK and Scottish social security expenditure have mirrored one another. However, as Ministers choose to exercise their devolved social security powers and establish a distinctive Scottish system, expenditure on social security is set to grow in value as a proportion of the Scottish Budget, and the potential impact of any variation in the forecasts is also increasing.

Any changes between actual and forecast expenditure, and the BGA reconciliations, are managed by the Scottish Government's budget management processes, in line with the principles and policies on the use of borrowing and reserve powers as set out in Chapter 3. Further information on the BGAs and reconciliations is set out in Annex C.

Existing borrowing and reserve powers can help manage in-year forecasting risk for social security and tax, however these powers have strict annual and overall limits and there is considerable risk that the quantum of any adverse movements may exceed the applicable annual limits for any one year.

4.3.3 Demographic Change

Scotland's population is expected to undergo significant change over the medium and longer-term. Some of this change creates risks to aspects of funding and spending that the Scottish Government will need to manage going forward.

Like most western countries the Scottish population is ageing. The recent SFC report on Fiscal Sustainability,[43] published in March 2023, analyses the projected impact of demographic change on the economy and public finances over the next 50 years.

These trends are already evident in the medium-term horizon considered in this MTFS. The number of over-65s in Scotland is projected to grow by 9.7% over the next five years according to the latest population projections. At the same time, the number of younger people is expected to decline over this time, with the under-18 population projected to decrease by 5.6%. Over this period the working age population is expected to fall slightly by around 0.7%.

While population projections are inherently uncertain, the general direction of these demographic shifts is clear, both over the medium and longer-term.

As the SFC report sets out, these demographic shifts may significantly impact upon the scale and shape of Scotland's public expenditure. An ageing population is likely to put further pressures on public expenditure, in particular on health, social care and social security. The SFC project that health spending will account for half of all devolved spending by 2072-73, increasing from 35% in 2027-28. These spending pressures are further increased by increasing numbers of people with multimorbidity and more complex care needs, and the projected increase in the overall burden of disease in Scotland.

In comparison, the reduction in the number of younger people means that some of these expenditure pressures may be offset by reduced demand in other areas, such as education, and younger age health and social care services (although, as with any age cohort, this must be balanced against the level of need for these services). We will need to think strategically about how medium- and long-term structural shifts in expenditure can be managed alongside public service reform to reflect the future shape and needs of the changing population.

Contact

Email: sophie.osborn@gov.scot