The Scottish Government's Medium-Term Financial Strategy

This is the sixth Medium-Term Financial Strategy (MTFS) published by the Scottish Government and provides the context for the Scottish Budget and the Scottish Parliament.

2. Scotland's Economic Outlook

This chapter provides an update on the latest state of the Scottish economy[15]; a summary of the latest economic forecasts from the Scottish Fiscal Commission (SFC)[16] and the Office for Budget Responsibility (OBR),[17] and what these imply for the Scottish Budget.

2.1 Economic Context

Economic conditions in Scotland and the UK continue to remain challenging as inflationary pressures continue to create a cost of living crisis for households and businesses across the country and increase pressure on public services. However, there is evidence that the Scottish economy has proved to be more resilient than previously expected with the latest economic outturn data showing that, despite the scale of the global energy price shock, Scotland avoided entering a technical recession towards the end of 2022 as had been forecast.

Inflation in March 2023 remained above 10%,[18] and is forecast to fall to around 3% by the end of 2023 - although uncertainty on this remains high. However, as highlighted by the International Monetary Fund[19] (IMF), falling energy prices in early 2023, stronger than expected economic data from Europe and the US, and the ending of strict COVID-19 quarantine policies in China, have all helped boost the outlook for the global economy this year – albeit an outlook that still remains subdued. The IMF singled out the UK as being particularly exposed to some of the recent global economic headwinds - and in April forecasted the UK to be one of the worst performing major economies in the world this year.

Despite this challenging outlook, the Scottish labour market has continued to remain robust with high levels of employment and near-record low levels of unemployment. The number of vacancies in the economy are still estimated to be significantly higher than pre-pandemic levels, although there is evidence that the number of people that are economically inactive due to long-term sickness has risen relative to before the pandemic.

In response to high inflation, average pay growth accelerated towards the end of 2022, with the labour market remaining tight. However, pay growth has failed to keep pace with inflation, causing reductions in the real purchasing power of households. Although inflation has begun to fall, prices are expected to be around 20% higher by the end of 2023 than they were at the start of 2020, meaning that household finances will continue to face significant pressures. This is also having a disproportionate effect on lower income households, who spend more on energy and food, with 16% of low income households reporting that they have had to eat less or skip meals in response to the cost of living crisis.[20]

Uncertainty in the economy also remains high, particularly for the future outlook for rates of inflation in the UK and how monetary policy and interest rates evolve in tandem. The scale of any further future changes in UK monetary policy will continue to have significant implications for businesses and households in Scotland, whether via their return on savings and investments, changes in household mortgage payments, or how costly it is to service existing, or take on new levels of debt.

2.2 Latest Economic Forecasts for Scotland

Our medium-term analysis is underpinned by the latest forecasts from the independent Scottish Fiscal Commission (SFC), which continue to show a fragile outlook for the economy.

While the SFC's overall economic outlook is not significantly different from their last forecast in December, they are now forecasting for the Scottish economy to avoid entering a technical recession this year (two consecutive quarters of negative economic growth). However, the overall size of the economy is forecast to remain relatively flat across 2023, and Scotland is still set to experience a record fall in living standards, with average real disposable incomes falling 4.1% from 2021-22 to 2023-24, in the face of high inflation, and are not set to recover to pre-pandemic levels until around 2026-27.

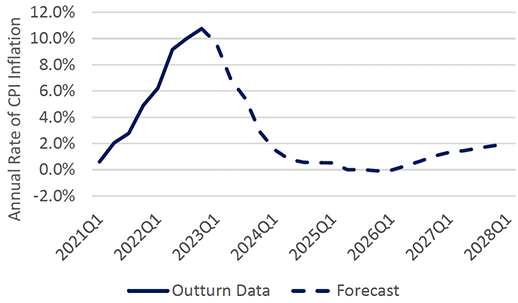

The SFC continue to mirror the inflation outlook of the OBR, shown in Figure 3, which sees the annual growth rate of the Consumer Price Index (CPI) falling sharply to 2.9% by the end of 2023 – although it will still average 6.1% across the year as a whole. Much of this outlook is driven by base effects, where inflation falls because prices rose to high levels last year. However, the SFC note the level of variation in price increases across different goods and services, with for example, food price inflation continuing to increase and currently sitting at around 20%.

Source: Scottish Fiscal Commission; Office for Budget Responsibility

Consequently, the SFC note that the outlook for inflation remains one of the key sources of uncertainty in their forecast, particularly around the future path of "core inflation" which excludes energy and food prices but has remained elevated. The Bank of England noted in their latest Monetary Policy Report that in the UK, Eurozone and the US there is evidence of headline inflation falling, but core inflation has remained elevated and stronger than projected.[21]

The SFC continue to forecast that the Scottish labour market will remain tight over the medium-term. They forecast that unemployment will remain near historic lows, increasing slightly to their assumed long-term trend rate of unemployment of 4.1%, but remaining lower than the 4.7% peak unemployment rate in their previous forecast.

The SFC is also forecasting slightly stronger employment and earnings growth at the beginning of the forecast. The upward revision to earnings growth in 2023-24 is driven by the relative tightness of the labour market putting further upward pressure on nominal pay growth and by inflation. The upward revision to employment growth in 2023-24 reflects recent labour market outturn data and an upward adjustment to Scotland's adult economic activity rate.

2.3 Fiscal Implications for the Economic Outlook

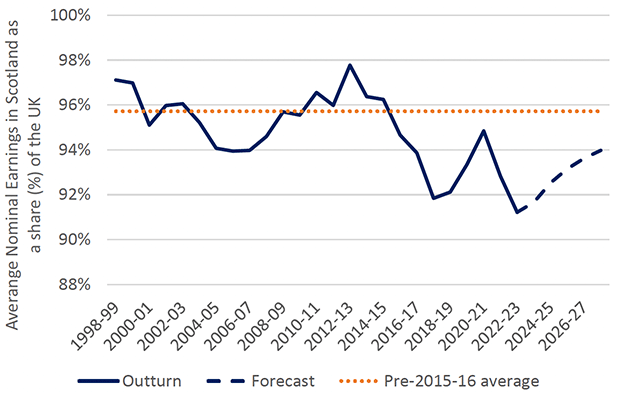

As set out in last year's Medium Term Financial Strategy,[22] tax receipts can be sensitive to the performance of particular sectors. In particular, relatively poorer earnings performance in the North East of Scotland, and strong earnings in financial services in London and the South East, has contributed towards average earnings in Scotland having grown more poorly relative to the rest of the UK.

Earnings are a key determinant of fiscal performance. Figure 4 below shows the SFC's historic estimate of Scotland's earnings as a share of the UK average and how that improves steadily when comparing their latest forecasts and those of the OBR. Due to the operation of the Fiscal Framework, this relatively faster earnings growth will generally improve the Scottish funding outlook. This is discussed further in Chapter 3.

Source: Scottish Fiscal Commission analysis, May 2023.[23]

The SFC have also made a small upward revision to their house price forecast in response to slightly lower interest rate rise expectations relative to December 2022 and consequently have revised up their forecast of Land & Buildings Transaction Tax (LBTT) revenues.

2.4 Economic Outlook Summary

The SFC's economic outlook has improved slightly since the Scottish Budget was published in December 2022 with the Scottish economy now forecast to avoid entering a technical recession in 2023.

However, the medium-term is still forecast to remain challenging, with relatively subdued growth in 2023 and households to see record falls in living standards which aren't set to recover to pre-pandemic levels until 2026-27. The outlook for inflation and the indirect impact that then has on tax revenue growth and spending pressures over the medium-term remains highly uncertain and this is complicated further by the intricacies of the Fiscal Framework.

Chapter 3 sets out these complexities and uncertainties and what this means for the medium-term funding outlook for the Scottish Budget in more detail.

Contact

Email: sophie.osborn@gov.scot