The Scottish Government's Medium-Term Financial Strategy

This is the sixth Medium-Term Financial Strategy (MTFS) published by the Scottish Government and provides the context for the Scottish Budget and the Scottish Parliament.

3. Scotland's Funding Outlook

3.1 How Scotland's funding outlook is determined

This chapter outlines the Scottish Government's 'central' funding outlook over the five years from 2023-24 to 2027-28. It sets out the assumptions and decisions that underpin this, and how the outlook has changed compared to last year's MTFS.

The Scottish Government's funding outlook is affected by decisions by both the UK and Scottish Governments, as well as Scotland's economic performance relative to the rest of the UK. The projections therefore combine independent forecasts of tax and spending provided by the SFC and OBR, with information published by His Majesty's Treasury (HMT), and the Scottish Government's own assessments of future risks inherent in the current funding framework, drawing on a range of sources as well as historic trends.

There is a significant level of uncertainty within the funding outlook. Alternative scenarios, setting out a more optimistic and pessimistic outlook, are presented at the end of this chapter.

The Scottish Government is committed to being open and transparent about its multi-year funding outlook and the risks and uncertainties that might lead to the actual position being higher or lower than this, to support Parliament and other stakeholders to fully scrutinise the sustainability of the Scottish Government's spending plans. In this MTFS, we have therefore put a greater emphasis on discussing upside and downside funding risks than in previous editions.

This chapter sets out:

- The central outlook for overall resource funding, which informs the Scottish Government's spending plans,[24] and the assumptions underpinning this;

- The central outlook for each component of the Scottish Government's resource funding position;

- The overall central outlook for overall capital funding;

- The Scottish Government's capital borrowing policy;

- Funding risks including upside and downside scenarios; and

- How the Scottish Government manages these risks, within the limitations of powers available.

3.2 Summary of Scotland's funding outlook

The Scottish Government's funding outlook is comprised of five high level categories, each of which is discussed in detail in this chapter:

- The Block Grant – this is the single largest source of funding for the Scottish Government. The Barnett Formula determines the Block Grant and annual growth is dependent on the UK Government's overall fiscal plans and its spending priorities.

- Devolved taxes – the Scottish Government receives the revenue from these taxes, the largest of which is Scottish Income Tax. The Scottish Budget is then reduced based on how quickly revenues of the corresponding tax have grown in the rest of the UK (rUK) on a per head basis.

- Non-domestic rates (NDR) – this revenue is raised by Local Authorities on non-domestic properties. All revenue raised is ultimately returned to Local Government via the Local Government Settlement.

- Social Security Block Grant Adjustments – this is funding provided by the UK Government for devolved social security payments, based on the growth in expenditure on the corresponding payment in rUK on a per head basis.

- Other income and expenses – other revenue and costs including resource borrowing and associated costs as well as revenues from the Scottish Crown Estate.

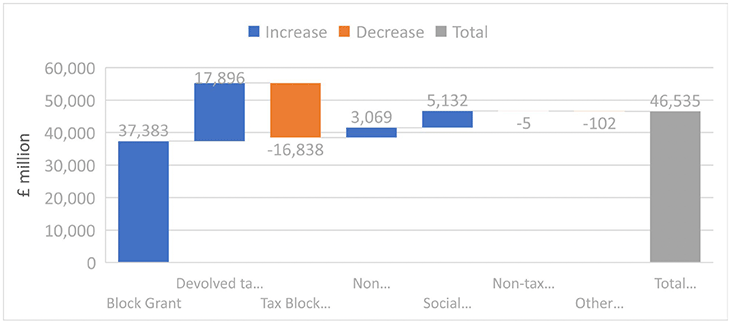

Overall, we expect the cash funding available to the Scottish Government to grow steadily from £45,260 million in 2023-24 to £50,971 million by 2027-28, (Table 1), an overall cash increase of 12.6% and a real terms increase of 6.8%. This is due to increases in the Block Grant and significant growth in the net tax position over this period. However, these increases will vary significantly between years. Pressures on funding will be most severe in 2024-25 when overall resource funding (including NDR) is forecast to grow by only 1.2% in real terms. Figure 5 illustrates the composition of the funding outlook for 2024-25.

| Figures in £million | current prices | Forecast | |||

|---|---|---|---|---|---|

| Resource Funding | 2023-24* | 2024-25 | 2025-26 | 2026-27 | 2027-28 |

| Block Grant | 36,832 | 37,383 | 38,153 | 39,038 | 40,135 |

| Net tax position | 574 | 1,058 | 1,240 | 1,344 | 1,661 |

| Of which: | |||||

| Devolved tax revenue | 16,674 | 17,896 | 18,658 | 19,513 | 20,654 |

| Tax Block Grant Adjustment | -16,100 | -16,838 | -17,418 | -18,168 | -18,993 |

| Non-domestic rates (NDR) distributable amount | 3,047 | 3,069 | 3,158 | 3,437 | 3,328 |

| Social Security Block Grant Adjustment | 4,434 | 5,132 | 5,435 | 5,697 | 6,003 |

| Non-tax income & block grant adjustments | -5 | -5 | -5 | -5 | -5 |

| Other income/expenses | 378 | -102 | -63 | -96 | -151 |

| Total resource funding, inc NDR income** | 45,260 | 46,535 | 47,917 | 49,415 | 50,971 |

*Based on funding position as set at Budget 2023-24 so net position figures differ from latest SFC forecasts. **Totals may not sum due to rounding.

Source: Scottish Government

Annex F provides a full breakdown of the resource funding envelope.

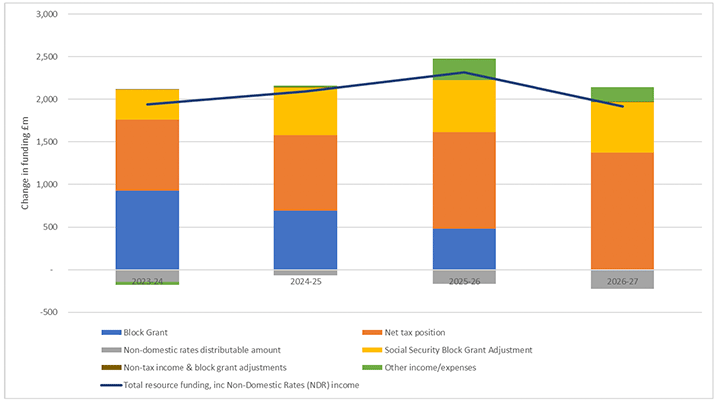

Changes since May 2022: The economic and fiscal landscape has changed significantly since last year's MTFS, with implications for the funding outlook. As illustrated in Figure 6 the total resource funding outlook (including NDR) has improved significantly in cash terms, by an average of £2.1 billion per annum over the period 2023-24 to 2026-27.

Source: Scottish Government, SFC, OBR

The main driver for this is the significant improvement in the forecast net tax position, which has increased by an average of £1.1 billion per annum over the period 2023-24 and 2026-27, compared to last year's MTFS. This is due to a number of factors, including better than expected Income Tax outturn data for 2020-21, strong in-year performance for 2022-23, and policy changes in 2023-24 – but most importantly significant shifts in the underlying forecasts of relative economic performance compared to the rUK. As noted by the SFC, significant revisions to the outlook for the net tax position are quite common. In this instance, the improvements in the medium term are driven by divergence between the two forecasters' judgements about future earnings growth: the OBR forecasts growth in nominal earnings to average 2.0% between 2024-25 and 2027-28 which is lower than the SFC's forecast of 2.6% over this period and below historic trends. Risks to the net tax position are discussed further in section 3.10.

Improvements in the net tax position also feed through to a significant improvement in 'other income' in 2025-26 as latest forecasts suggest positive, rather than negative, reconciliations for 2022-23 and hence no requirement for potential resource borrowing in that year.

Increases to the Block Grant announced at the UK Government Autumn Statement,[25] published in November 2022, and at the Spring Budget,[26] published in March 2023, also contribute to the improved outlook. The improvement, compared to last May, is most significant in the early years of the outlook with no change in the outlook for 2026-27. Increases to the social security Block Grant Adjustments contributed around a further £530 million on average per year, although these are fully offset by higher forecasts of spending on social security benefits in Scotland over the same period.

3.3 Components of Scotland's funding outlook

This section sets out the assumptions underpinning the elements of the central resource funding outlook (Table 2). The approach to these funding assumptions has not changed substantially from that taken in the May 2022 MTFS.[27]

Overall, the Scottish Government views the assumptions underpinning the central funding outlook as reasonable. This judgement is echoed by the SFC, which is tasked with reviewing the robustness of the Government's central funding scenario and underpinning assumptions as part of their remit. The Scottish Government also considers these assumptions to be prudent, with a relatively balanced likelihood of both more and less funding when looking at all elements in the round.

Table 2: Central resource funding assumptions

Funding Component / Source of central funding assumption

Block Grant:

- 2023-24 and 2024-25 figures in line with the latest Barnett and ringfenced funding settlements provided by HM Treasury (HMT) at Main Estimates.

- 2025-26 to 2027-28 Barnett projections in line with the March 2023 OBR projections for Public Sector Current Expenditure (PSCE) growth in RDEL (Resource Department Expenditure Limits).

- Ringfenced funding, such as the Rail Resource Grant and replacements for EU funding, held at 2024-25 levels in cash terms.

Net tax position:

Devolved tax revenue: May 2023 SFC Forecasts

Block Grant Adjustment: March 2023 OBR Forecasts

Social Security Block Grant Adjustments: March 2023 OBR Forecasts

Non-Domestic Rates (NDR): May 2023 SFC Forecasts, adjusted to reflect outturn adjustments in the NDR pool and taking into account the policy to bring the pool back into balance in 2024-25

Other Income and Expenses: Reconciliations implied by SFC and OBR forecasts; other projections based on assumptions and decisions made by the Scottish Government

Source: Scottish Government

3.4 Block Grant

The Block Grant is the core source of the Scottish Government's funding and is made up of two elements: the baseline Block Grant plus any changes to the core funding, also known as consequentials, which are determined by the Barnett formula. In essence, the formula provides the Scottish Budget with a population share of the change in 'comparable' UK Government departmental spending in England.

Therefore, the Block Grant is not only determined by how much the UK Government expects to spend in total, but also how it prioritises resource departmental spending (RDEL) and capital departmental spending (CDEL) across devolved and reserved spending areas within a given funding envelope. For example, considering recent policy decisions at Spring Budget 2023,[28] higher UK Government spending on devolved policy areas, such as childcare, results in more funding being available to the Scottish Government while increased spending in reserved areas, such as Defence, will not generate any Barnett consequentials.

The UK Government has also used Part 6 of the UK Internal Market Act 2020 to fund activity in devolved policy areas. This includes funding streams under its Levelling Up agenda, including the Community Renewal Fund, the Community Ownership Fund, the Levelling Up Fund and the UK Shared Prosperity Fund. This funding should have been provided directly to the Scottish Government to allocate in line with national priorities. The Scottish Parliament did not consent to the Internal Market Act and the remains opposed to it. It enables the UK Government to bypass devolved decision making and override democratic processes for allocating funding in wholly devolved policy areas in Scotland, which risks incoherence, stakeholder confusion and inefficiency in public spending.

As set out in Table 3, the approach to the central forecast is broadly consistent with the methodology in last year's MTFS. However, unlike last year, the Scottish Government no longer assumes additional consequentials in the remaining years of the Spending Review (SR) period given that the end of the period is approaching and there is less certainty over any assumed consequentials materialising.

As a result, the Barnett resource Block Grant is expected to grow by 3.3% in real terms between 2023-24 and 2027-28 although annual rates vary significantly across years. In 2024-25, the block grant is expected to fall marginally by 0.1% but it is projected to grow by 1.1% in real terms from 2025-26 onwards.

| Figures in £million | current prices | Forecast | |||

|---|---|---|---|---|---|

| Resource Funding | 2023-24 | 2024-25 | 2025-26 | 2026-27 | 2027-28 |

| RDEL Block Grant as at UKSR 21 | 34,942 | 35,577 | N/A | N/A | N/A |

| Additional consequentials from subsequent UK fiscal events | 1,176 | 1,091 | |||

| Assumed Block Grant beyond SR period | 37,438 | 38,323 | 39,420 | ||

| Non-Barnett ringfenced funding and Rail Resource Grant | 715 | 715 | 715 | 715 | 715 |

| Total RDEL Block Grant | 36,832 | 37,383 | 38,153 | 39,038 | 40,135 |

Source: Scottish Government, OBR

3.5 Net impact of devolved tax revenue & Block Grant Adjustments

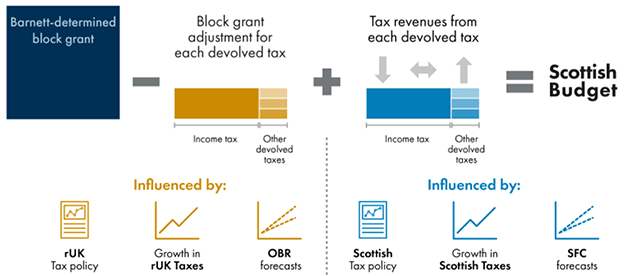

The Scottish Government receives the revenue from fully and partially devolved taxes – namely Scottish Income Tax (SIT), Land and Buildings Transaction Tax (LBTT) and Scottish Landfill Tax (SLfT).[29] As illustrated in Figure 7, as the Scottish Government now raises devolved tax revenue, a corresponding BGA is made to account for the tax revenue that is foregone by the UK Government.

Source: Scottish Parliament Information Centre

The difference between the amount of revenue the Scottish Government receives from these taxes and the corresponding BGA determines the net impact of devolved tax on the Scottish Budget, otherwise referred to as the 'net tax position'; this is the spending power available to the Budget.

Under the current Fiscal Framework,[30] the overall impact of tax devolution on the Scottish Budget depends on the performance of tax receipts per person in Scotland relative to the rest of the UK. If tax receipts per person in Scotland grow faster than in the rUK, there will be additional funding for the Scottish Budget, and vice versa. The performance of the Scottish economy, alongside Scottish and rUK tax policy decisions, influence the scale of tax revenues, and whether the Scottish Budget is larger or smaller than it would have been without the devolved powers.

The net tax impact in the central funding outlook, as presented in Table 4, is based on the latest SFC and OBR forecasts. However, for 2023-24 the position for Income Tax is set at the level incorporated into the 2023-24 Budget (£325 million).

| Figures in £million | current prices | Forecast | |||

|---|---|---|---|---|---|

| Resource Funding | 2023-24* | 2024-25 | 2025-26 | 2026-27 | 2027-28 |

| Income Tax | |||||

| Revenue* | 15,810 | 17,080 | 17,808 | 18,591 | 19,646 |

| Block Grant* Adjustment | -15,485 | -16,239 | -16,722 | -17,359 | -18,092 |

| Net Income Tax* position | 325 | 841 | 1,086 | 1,232 | 1,554 |

| Land and Buildings Transaction Tax | |||||

| Revenue | 772 | 733 | 792 | 905 | 992 |

| Block Grant Adjustment | -519 | -508 | -612 | -723 | -809 |

| Net LBTT position | 254 | 225 | 179 | 183 | 183 |

| Scottish Landfill Tax | |||||

| Revenue | 92 | 83 | 58 | 16 | 16 |

| Block Grant Adjustment | -96 | -91 | -84 | -87 | -92 |

| Net SLfT position | -5 | -8 | -26 | -71 | -76 |

| Total net tax impact | 574 | 1,058 | 1,240 | 1,344 | 1,661 |

*Figures shown for 2023-24 are based on the SFC and OBR forecasts as at the Scottish Budget 2023-24 Budget, published in December 2022. The latest SFC and OBR forecasts for 2023 will affect the Scottish funding position through reconciliations. **Some figures may not sum due to rounding.

As illustrated in Table 4, tax devolution is forecast to make a positive net contribution to the Scottish Budget and therefore presents a vital additional source of revenue.

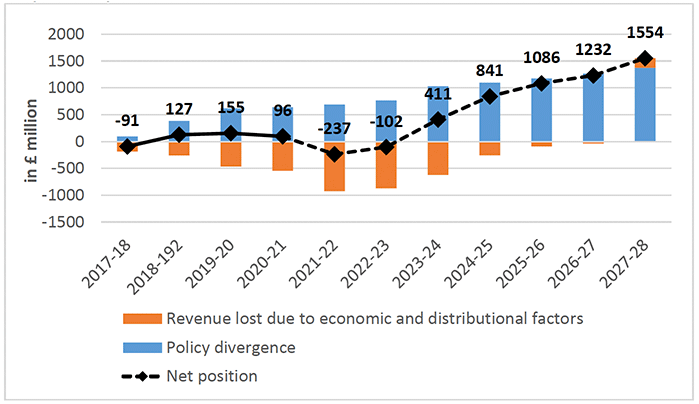

Income Tax: As noted above, fiscal devolution means that the Scottish Budget is now more closely linked to Scotland's relative economic and tax performance. However, the relationship between the economy and tax is complex, and reflects a range of factors, including macro-economic performance, regional and sectoral issues, demographics, the composition of the tax base as well as differences in government economic and tax policy. Figure 8 illustrates the contributions of these different components to the Income Tax net position, based on outturn data and latest forecasts.

Source: Scottish Government, SFC, OBR

The Scottish Government estimates that the Scottish Budget will benefit by up to around £1 billion in 2023-24, when compared with matching Income Tax policy in the rUK (blue bars).[31] This is in line with SFC estimates from the December budget. However, relatively weaker economic performance on employment and earnings growth, alongside differences in the income distribution, partly offset this (orange bars). Therefore, the SFC now forecasts Scottish Income Tax to be only £411 million greater than the corresponding BGA in 2023-24 (black line). While this is above the £325 million estimate from forecasts accompanying the Budget (see Table 4), there is no impact on Scottish Government spending power in 2023-24 as figures for Income Tax are "locked in" until outturn becomes available. and the final reconciliations are calculated.

Scotland's labour market outcomes have broadly matched, if not exceeded, the UK performance in recent years, with high employment and low unemployment. The relatively weaker performance of Scottish Income Tax primarily reflects weaker earnings growth, particularly amongst higher rate taxpayers, and distributional factors. As discussed in the 2021 and 2022 MTFS publications, this weaker relative performance since Income Tax was devolved is associated with lower receipts in the North East of Scotland, caused by the downturn in the oil and gas industry, at the same time as strong growth in rUK receipts in London and the South East, driven by growth in the financial services sector. However, even if the Scottish and UK economies were growing at similar rates, it would not necessarily be the case that the respective tax bases would grow similarly as well, for example if particular sectors that contain a disproportionate number of high-income taxpayers were going through cyclical or structural change.

The Scottish Government continues to monitor the key drivers of Scotland's tax performance as more evidence and data become available. Although tax performance remains a key risk to the resource funding position, recent evidence across a range of indicators suggests that the relatively weaker economic performance has lessened. Provisional in-year Pay As you Earn (PAYE) tax data for the first 11 months of 2022-23 suggest that growth in Scottish PAYE income tax receipts has outperformed the rest of the UK. Indicative analysis for the first six months of the financial year also suggests that these improvements in relative tax performance are broad based across all sectors. However, a full assessment of Real Time Information RTI tax performance in 2022-23 will only be available when data for the full financial year, including the bonus season, will be published alongside HMRC Scottish Income Tax Outturn 2021-22 in summer 2023. We will consider opportunities to update Parliament at this point.

These improvements are also reflected in the latest set of forecasts by the SFC and the OBR which suggest that Scotland's net position will continue to improve further in the medium term. While positive, the Scottish Government is not complacent and is therefore taking further action to help boost the long-term and sustainable growth of the Scottish tax base and ensure this improvement is realised.

Fully devolved taxes: For LBTT, the expected medium-term net position over the next five years remains positive and similar to what it was at the time of the Scottish Budget. Across the period, a slight weakening of this positive net position is anticipated from 2025-26 onwards. This is in part due to the temporary increase in the UK's Stamp Duty Land Tax (SDLT) residential nil rate band coming to an end on 31 March 2025 and the impact of this on SDLT revenues.

The medium-term LBTT forecast in total has not changed significantly since the Scottish Budget 2023-24. However the residential LBTT forecast is a little more optimistic, based on house prices rising more than expected at that time, while there is a more negative view of non-residential LBTT, largely based on 2022-23 outturn data.

The net position for LBTT is close to where it was six months ago, reflecting the fact that the Scottish and rUK residential property markets have historically tended to track each other in terms of general direction as they are subject to the same base rate and mortgage rate changes.

For SLfT, the net position is expected to be negative in each year of the funding outlook. The negative net position for SLfT accelerates sharply from 2026-27 when the ban on landfilling biodegradable municipal waste (BMW) in Scotland will come into operation. Before the ban comes into effect (31 December 2025), the volume of waste going to landfill is expected to decline as waste is diverted to other means of disposal, such as energy from waste.

3.6 Block Grant Adjustments for devolved Social Security benefits

For the social security BGAs, the central funding outlook is based on the OBR's March 2023 forecasts for benefit expenditure in England and Wales. The growth in social security BGAs over time will be affected by both economic factors and the policy decisions made by the UK Government. This can include changes to the eligibility for certain benefits, changes to the generosity of certain payments or decisions on how payments are uprated over time.

The social security BGAs that inform the funding envelope are set out in Table 5.

| Figures in £million | current prices | Forecast | |||

|---|---|---|---|---|---|

| 2023-24 | 2024-25 | 2025-26 | 2026-27 | 2027-28 | |

| Attendance Allowance | 646 | 714 | 728 | 733 | 744 |

| Personal Independence Payment | 2,500 | 2,840 | 3,095 | 3,347 | 3,609 |

| Disability Living Allowance | 826 | 900 | 915 | 906 | 920 |

| Carer's Allowance | 367 | 404 | 421 | 441 | 465 |

| Industrial Injuries Disablement Scheme | 84 | 84 | 80 | 77 | 74 |

| Severe Disablement Allowance | 6 | 6 | 5 | 4 | 3 |

| Cold Weather Payments | 5 | 5 | 5 | 5 | 5 |

| Pension Age Winter Heating Payment[32] | N/A | 179 | 184 | 185 | 183 |

| Total social security BGA | 4,434 | 5,132 | 5,435 | 5,697 | 6,003 |

Source: Scottish Government, OBR

The forecast BGA is set to increase annually, from £4,434 million in 2023-24 to £6,003 million in 2027-28. The latest forecast for the 2023-24 social security BGA is £73 million higher than the BGA used in the Scottish Budget 2023-24 and £352 million higher than in the 2022 MTFS.

The upward revision since May 2022 reflects wider post-pandemic trends of ill-health in the UK population which translates into higher-than-expected recent caseloads, which the OBR assume will persist throughout the forecast period. Their judgement about caseloads reflects new claims for disability-related benefits rising further above pre-pandemic levels. The rise in new claims for benefits such as Personal Independence Payment (PIP) has also been compounded by an increase in the success rate of those claims.

Moreover, the UK Government's decision – mirrored in Scotland – to uprate benefits in 2023-24 in line with much higher inflation (10.1%) than anticipated in May last year has also increased social security spending in England and Wales, and hence the BGAs the Scottish Government receives.

Annex E sets out details of the assessment of the distributional impact of the Scottish Government's Income Tax and social security policy choices.

3.7 Non-Domestic Rates (NDR)

NDR are administered and collected by councils. NDR revenue raised is pooled centrally and may be in deficit or surplus at any point in time, but all revenues are ultimately distributed back to Local Authorities over time. The Scottish Government guarantees the sum of General Revenue Grant funding and NDR income, thereby bearing any volatility risk with NDR revenue between forecast and outturn. NDR policy decisions including the poundage and reliefs are made annually by Scottish Government at the Budget.

The central estimate of the NDR Distributable Amount – the amount guaranteed to Local Authorities each year – draws directly from the SFC's forecasts of NDR revenues (the Contributable Amount) adjusted to reflect the closing balance of the NDR pool from the previous financial year, estimated prior year adjustments and taking into account Scottish Government policy on clearing the NDR pool deficit in 2024-25. From 2025-26 onwards, it is therefore assumed that the Distributable Amount will equal the forecast Contributable Amount.

The SFC forecasts reflect the revaluation which took effect on 1 April 2023, as well as policies announced at the Scottish Budget 2023-24, such as reforms to the Small Business Bonus Scheme. To better reflect market circumstances this revaluation was based on one year 'tone' date for the first time, and transitional reliefs were introduced to protect those seeing the highest increases in rateable value. The next revaluation is scheduled for 2026. Reforms to the appeals system were also introduced on 1 April 2023 and are intended to encourage swifter resolution at an early stage. One effect of this would be to provide greater revenue certainty.

| All figures in £million, current prices | 2023-24 | 2024-25 | 2025-26 | 2026-27 | 2027-28 |

|---|---|---|---|---|---|

| Non-Domestic Rates – Distributable amount | 3,047 | 3,069 | 3,158 | 3,437 | 3,328 |

Source: Scottish Government, SFC

3.8 Other income

This category aggregates all the smaller components of the resource funding envelope not covered above and accounts for less than 1% of the total. Each of these line items was assessed independently using existing policies (where applicable) but given the inherent volatility of these items, the interdependencies across them, and also the scope for discretion, a collective view was also taken in determining final funding assumptions. Table 7 sets this out in detail.

The material elements are:

- Reconciliations - These relate to OBR and SFC forecast error in past years. They occur after tax outturn data becomes available and, for Income Tax, affect the financial year three years after the tax year to which they relate (i.e. the reconciliation that affects the 2024-25 Scottish Budget relates to the 2021-22 tax year). Estimates of future reconciliations are directly derived from latest SFC and March OBR forecasts for the period 2023-24 to 2026-27. No assumption is made for 2027-28 as this is beyond the reconciliations forecast period. A significant reconciliation is expected for the 2024-25 Budget in relation to Income Tax which exceeds the Scottish Government's current borrowing powers.

- Resource Borrowing - This provides funding to offset the impact of adverse Income Tax reconciliations in future years. Borrowing amounts are maintained at levels assumed for the 2023-24 Scottish Budget (£41 million and £300 million for 2023-24 and 204-25 respectively) and have changed from the assumptions made in the 2022 MTFS due to significant shifts in the estimated reconciliations.

- Borrowing costs - These are derived directly from capital and resource borrowing assumptions.

- Scotland Reserve - The Scotland Reserve provides the Scottish Government limited ability to manage spending across financial years. No Scotland Reserve assumption is included for future years. The Scottish Government's approach to the Scotland Reserve is discussed in section 3.11.

- ScotWind Revenue - In 2022-23, the Crown Estate Scotland concluded the first round of offshore wind leasing which generated in excess of £756 million of income. Consistent with last year's MTFS, deployment of ScotWind income is maintained at £310 million in 2023-24 and £350 million in 2024-25. Decisions on profiling of other offshore leasing Crown Estate Revenues, including Innovation and Targeted Oil and Gas (INTOG) revenues, will be taken when they can be reliably quantified.

- Migrant Surcharge - This is income derived from charges on migrants for using NHS Services and is redistributed to devolved governments on a Barnett basis. The funding assumed is £160 million per annum, broadly in line with recent outturn data.

| 2023-24 | Forecast | ||||

|---|---|---|---|---|---|

| 2024-25 | 2025-26 | 2026-27 | 2027-28 | ||

| Reconciliations | 46 | -687 | 88 | 86 | - |

| Resource Borrowing | 41 | 300 | - | - | - |

| Resource Borrowing Costs | -114 | -124 | -166 | -174 | -120 |

| Capital Borrowing Costs | -103 | -127 | -150 | -173 | -197 |

| ScotWind | 310 | 350 | - | - | - |

| Scotland Reserve | - | - | - | - | - |

| Migrant Surcharge | 160 | 160 | 160 | 160 | 160 |

| King's and Lord Treasurer's Remembrancer (KLTR) | 5 | 5 | 5 | 5 | 5 |

| Other* | 33 | 21 | - | - | - |

| Total other income | 378 | -102 | -63 | -96 | -151 |

*Other includes corrections to historic UK funding settlements and machinery of government transfers due to be received

Source: Scottish Government

3.9 Scotland's Capital Funding Outlook

This section sets out the central capital funding outlook (Table 8) and the assumptions underpinning this, which are largely unchanged from last year. This is structured around four categories:

1. The Capital Block Grant – this is the single largest source of funding for the Scottish Government's capital budget, which is driven by the UK Government's spending priorities and overall fiscal plans and determined through the Barnett Formula.

2. Capital Borrowing – Under the Fiscal Framework, the Scottish Government can borrow additional capital up to a maximum of £450 million per annum and £3 billion in total.

3. Ringfenced funding and City Deals – Funding received through the Block Grant but outside of Barnett arrangements include network rail ringfenced funding and City Deals.

4. Financial Transactions - Financial Transactions (FTs) are a type of funding allocated to the Scottish Government by HMT. They can only be used to make loans to or equity investments in private sector entities. The funds must ultimately be repaid by the Scottish Government to the UK Government.

Table 8: Central capital funding assumptions

Funding Component / Source of central funding assumption

Block Grant:

- The 2023-24 and 2024-25 figures are the latest Barnett funding provided by HMT at Main Estimates.

- The 2025-26 to 2027-28 projections are based on the March 2023 OBR projections for Public Sector Gross Investment (PSGI) growth.

Capital Borrowing:

- Current Scottish Government capital Borrowing policy which assumes £450 million additional funding will be available through borrowing and other funding in each year.

Ringfenced funding and City Deals:

- The 2023-24 and 2024-25 figures for Ringfenced funding are the latest provided by HMT at Main Estimates.

- City Deals are maintained at £100 million per annum for the duration of the period.

Financial Transactions:

- No Financial Transactions funding is included for years beyond 2024-25. This is in line with our understanding of HMT's latest plans.

Source: Scottish Government, OBR

As illustrated in Table 9, total capital funding excluding FTs is expected to fall by around 1.6% in cash terms between 2023-24 and 2027-28. This reflects the UK Government's plans to hold capital spending broadly flat in cash terms beyond 2024-25. This means that capital funding is projected to fall in real terms by 6.7%. This real terms fall is felt most acutely in 2024-25, where funding is projected to fall by 3.7%

| All figures in £million, current prices | 2023-24 | 2024-25 | 2025-26 | 2026-27 | 2027-28 |

|---|---|---|---|---|---|

| Total CDEL Block Grant | 4,820 | 4,691 | 4,700 | 4,720 | 4,727 |

| Ringfenced funding and City Deals | 734 | 732 | 732 | 732 | 732 |

| Capital Borrowing and other funding per policy | 450 | 450 | 450 | 450 | 450 |

| Total Capital Funding excl FTs | 6,004 | 5,873 | 5,882 | 5,902 | 5,909 |

| Financial Transactions | 410 | 176 | |||

| Total Capital Funding incl FTs | 6,414 | 6,049 | 5,882 | 5,902 | 5,909 |

Source: Scottish Government, OBR

The overall capital funding outlook has worsened since the last MTFS, with the 2022 UK Government Autumn Statement indicating that the capital block grant will remain broadly flat in cash terms for three years from 2025-26. The other driver of the weaker position relates to FTs. In May 2022, Government included in the central funding scenario an additional £400 million in FTs split over 2023-24 and 2024-25 as a result of previous years' adjustments due to be made by HMT. As of May 2023, the UK Government has agreed to provide £187.6 million but no agreement has been reached over the remaining £212.6 million FTs. This outstanding amount is therefore not included in the central outlook.

Annex F provides a full breakdown of the capital funding envelope.

3.9.1 Capital Borrowing

Under the Fiscal Framework, the Scottish Government can borrow additional capital up to £3 billion cumulatively with an annual limit of £450 million. In taking annual borrowing decisions, the Scottish Government also takes into consideration the affordability of ongoing debt repayments.

While the Scottish Government can borrow commercially or issue bonds for capital investment purposes, the National Loans Fund currently remains the preferred source of capital borrowing. Given the medium-term impact on resource costs, this remains the optimum compromise between value for money, resource cost impact and maximising the use of the Fiscal Framework limits.

In 2022 the Scottish Government amended its Capital Borrowing policy to assume £450 million of additional annual funding would be available through a combination of borrowing, the Scotland Reserve and other capital funding. Within this £450 million total, £250 million will initially be assumed to be funded through borrowing.

The Scottish Government can borrow £250 million annually at a 15-year tenor, almost indefinitely, even within the existing cumulative limit of £3 billion imposed by the Fiscal Framework. Where capital borrowing is required to be greater than £250 million the tenor will be amended to balance the resource cost impact and longer-term fiscal sustainability.

As the medium-term Barnett outlook for capital is constrained in real terms, there is an increasing likelihood that to achieve the full additional £450 million per annum, actual borrowing would need to be greater than the £250 million assumed. Decisions on the nature and scale of capital borrowing will be made at the end of each financial year, based on the resource and capital funding outlook at the point where drawdown decisions are finalised.

3.10 Funding risks

All sources of funding are subject to uncertainty due to policy risks, economic risks, and forecast error. These risks are often difficult to quantify, for example, because either the scale of the risk, or the probability of it occurring, is unknown. The identification and management of risks – both on the upside and downside – are essential for prudent stewardship of the public finances and smoothing funding variability over time. Annex D provides a summary of the risks to the funding and spending positions set out in this document.

This section presents illustrative upside and downside scenarios for the funding envelope, based on analysis of historic funding variability and forecast error for the two principal sources of variation, the Block Grant and the Income Tax net position, alongside judgements about the key challenges lying ahead.

3.10.1 Risks to the UK Government Block Grant

Changes to UK Government spending plans remain the most significant source of funding risk for both resource and capital funding. The level of uncertainty is heightened by the UK General Election due to be held before the end of 2024, with a potential change in the overall UK fiscal stance as well as the shape of Government spending.

As noted by the Institute for Fiscal Studies (IFS),[33] the current 'pencilled in' spending plans beyond the UK Spending Review period are extremely tight, "perhaps implausibly so, given the pressures on public services". Under those plans, overall day-to-day departmental spending is expected to grow by around 1% in real terms, well below the 1.8% average seen over the past 40 years and below the 2.8% average for this UK Parliament. Once likely increases on the NHS as well as commitments on childcare and defence are taken into account, this could imply real terms cuts for some departments.

Scottish Government analysis of historic trends shows that initial allocations for both resource and capital funding (in periods outside spending reviews) were ultimately increased. Based on this historic analysis, the high scenario illustrates an annual growth in resource funding 2.7% points higher each year than in the central forecast, while annual growth in capital funding is 3.1% points higher. By contrast, the low scenario assumes that annual growth is 1% point lower than in the central scenario.

3.10.2 Risks to the net tax position

The Fiscal Framework cushions the Scottish Budget against any UK-wide symmetric economic shocks. In short, if economic factors, such as inflation, or policy decisions, were to affect tax receipts in Scotland and the rest of the UK equally, the net tax position would be largely unchanged. As noted in Box 2, there is no clear evidence yet as to whether inflation – via its impact on nominal wage growth - will affect the UK and Scotland in the same way.

Box 2: Inflation and the Income Tax Net Position

Higher inflation and a relatively tight labour market, with near record low unemployment, have been contributing to upward pressure on nominal earnings growth. Growth in nominal wages across the UK was at 7.0% in the private sector and 5.6% in the public sector in January to March 2023.

Faster pay growth would boost Scottish Income Tax receipts. However, this only tells part of the story, as it is Scotland's relative performance in earnings growth compared to the rest of the UK that matters for the Scottish Budget. In other words, if higher inflation leads to higher nominal earnings growth in both Scotland and the rUK, Scottish tax receipts increase but so does the off-setting BGA. The net position will only be affected by inflation if earnings growth is different between Scotland and rUK. This is because the Fiscal Framework cushions the Scottish Budget against any UK-wide and symmetric economic shocks. However, it does not account for any sectoral, distributional and forecast risks.

Factors that might lead to a different impact on tax receipts in Scotland relative to the rest of the UK include differences in the structure of the two economies or the structure of the tax base. Data on this is still emerging but three possible drivers of differential impact are set out below:

- Differences in the relative size of the public sector. Should private sector wage growth continue to outpace public sector pay growth, this might present a downside risk to Scotland's tax performance. In 2019-20, the latest year for which detailed sectoral Income Tax data is available, around 21% of Scottish tax receipts came from Public Administration, Education and Human Health & Social Work, compared to 15% in the rUK. Hence, slow public sector wage growth has a larger impact on Scottish receipts.

- Differences in the income distribution mean that fiscal drag – whereby taxpayers are pulled into higher bands as earnings grow and thresholds remains frozen – could be more pronounced in Scotland.

- Differences in earnings growth in particular sectors may also have an impact, with recent data suggesting stronger earnings growth in Scotland than rUK in the Finance and Insurance sectors.

In summary, it is too early to draw firm conclusions as to whether inflation is impacting Scotland's relative income tax performance but the Scottish Government will continue to monitor this.

Income tax performance remains a major risk to the funding position, and there can be significant shifts in the net position from year to year, although there are encouraging signs from recent data that historic trends might have lessened. Similar to December 2022, the SFC forecasts show a period of relatively faster earnings growth in Scotland, compared to the rUK, which can have a material impact on the net position. To put this into context, as noted by the SFC, a 0.1% relative increase in Scottish average nominal earnings growth would lead to a £25 million increase in the net position. By comparison, a 0.1% relative increase in Scottish employment growth rates would lead to a £13 million increase in the net position.

Income Tax policy decisions by either the Scottish or UK Governments can also have a significant effect on Income Tax receipts. For example, the SFC forecasts are currently based on the assumption that the Higher Rate Threshold in Scotland will remain frozen over the forecast period. However, policy decisions about the rates and bands are made annually at the Scottish Budget. Should the Scottish Government decide to uprate the threshold in line with inflation, for example, this would reduce Scottish Income Tax receipts below what is set out in the 'central' funding forecast. Possible developments in UK Income Tax policy may also influence the funding outlook. With a UK General Election expected in 2024, media speculation has suggested the possibility of 1p cut to the Basic Rate of Income Tax in the rest of the UK. This may result in an improvement to the Scottish Government's position, possibly in the range of around £400 million per annum should the policy not be mirrored in Scotland.

As highlighted by the SFC, recent improvements in the Income Tax net position are partly driven by differences in the independent forecasters' judgements, in particular in relation to earnings growth. The SFC highlight that were earnings growth to be more similar in Scotland and the UK, the Income Tax net position would be materially lower than is currently projected.

Across the range of risk drivers, some are quantifiable in terms of scale but likelihood remains subject to judgement for them all. The scenarios presented in Box 3 draw on an analysis of historic forecast errors for the Income Tax net position.

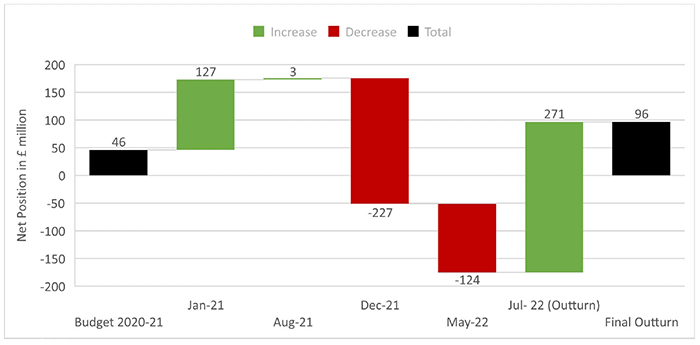

Box 3: Forecasts of the net position and funding volatility

In addition to economic and policy risks, the net tax position remains subject to significant forecast variation. Forecast error is an inherent part of forecasting. In the case of the Scottish Budget, the risk of forecast error is heightened by the Fiscal Framework drawing on two different forecast institutions, the SFC and the OBR, both forecasting a different part of the funding position.

Having official independent forecasts is vital as it reduces bias and improves overall fiscal transparency. However, the differences in timing, judgement and methodology between the OBR and SFC continue to present a risk for the Scottish Government's funding outlook, contributing to continuing volatility. This is illustrated in Figure 9 which compares different rounds of forecasts over time.

The original, budget-setting, forecasts produced in February 2020 of the £46 million net position were 'locked in' until outturn data was available in summer 2022. Despite economic upheaval – original forecasts were produced prior to the full extent of Covid 19 pandemic - the final net position was only £50 million higher than originally forecast. Forecasts between the original budget-setting forecasts and final outturn projected different outcomes – some higher and some lower than the final outturn.

Source: Scottish Government, SFC, OBR

However, it also shows that there is significant volatility in the forecasts produced in between the budget setting forecasts and final outturn. This will in part reflect that the net position is the difference between the forecasts of two large numbers (income tax and the BGA), and so small changes in either forecast can result in large changes in the net position. Unlike for forecasts of Scottish and rUK receipts, these forecasts of the net position do not appear to become more accurate over time. Indeed, in this example, the forecast error of the net position was largest just two months prior to the outturn data becoming available.

This volatility in forecasts does introduce a challenge to forward planning and efforts to smooth the funding outlook over time. This is because forecasts for the anticipated reconciliation to be applied in future budgets – in the case of the 2020-21 outturn to be applied in Budget 2023-24 - inform decisions on future resource borrowing and spending. In addition, should outturn figures be significantly different from the latest available forecast, the impact on the funding outlook can be twofold: not only will anticipated reconciliations change but such updates can also impact the outlook for the future net position should the forecasters judge any unexpected improvements or deteriorations in tax revenues to have a permanent effect.

With only four years of Income Tax outturn data available at present (2017-18 to 2020-21), our understanding of these challenges is still evolving. However, our analysis of historic forecast errors over this relatively short time period indicates that the average amount of variability, the so-called standard deviation, was around £100 million across the four years. We have used this as the basis to generate a 95% confidence interval by adding/subtracting two standard deviations to the central net tax position, with further adjustments to account for greater downside risks and growth in the net tax position over time.

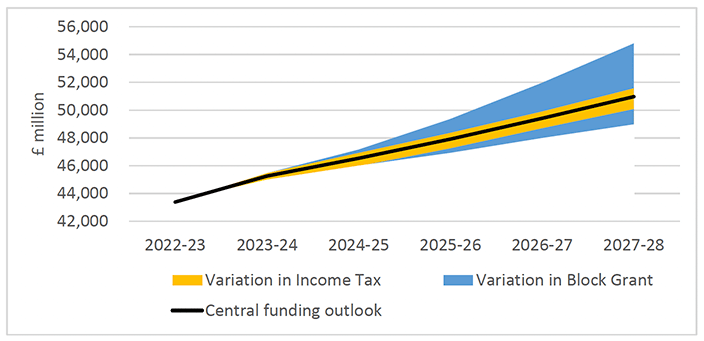

Figure 10 and Table 10 set out an illustrative upside and downside scenario for the funding outlook based on the risks to the Block Grant (blue range) and to volatility in the forecast of the net tax position (orange range). The uncertainty in the Block Grant is the most significant factor.

Source: Scottish Government

| 2022-23 | 2023-24 | 2024-25 | 2025-26 | 2026-27 | 2027-28 | |

|---|---|---|---|---|---|---|

| Central funding outlook | 43,387 | 45,260 | 46,535 | 47,917 | 49,415 | 50,971 |

| Upside scenario | 43,387 | 45,466 | 47,166 | 49,363 | 51,973 | 54,805 |

| % variation | 0.0% | 0.5% | 1.4% | 3.0% | 5.2% | 7.5% |

| Downside scenario | 43,387 | 44,951 | 45,965 | 46,882 | 47,945 | 48,933 |

| % variation | 0.0% | -0.7% | -1.2% | -2.2% | -3.0% | -4.0% |

Source: Scottish Government

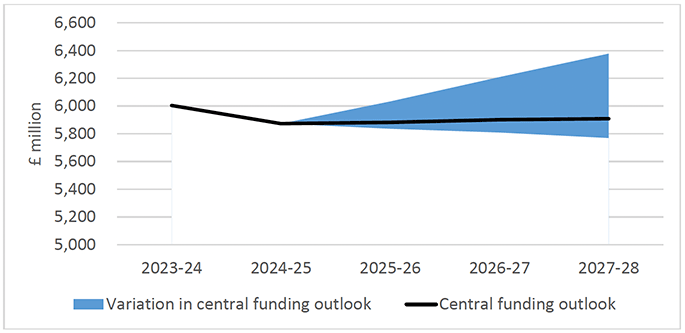

The Scottish Government has taken a similar approach to illustrative modelling of capital funding, with the upside and downside scenarios based on variation to the block grant – see Figure 11 and Table 11.

Source: Scottish Government

| 2023-24 | 2024-25 | 2025-26 | 2026-27 | 2027-28 | |

|---|---|---|---|---|---|

| Central funding outlook | 6,004 | 5,873 | 5,882 | 5,902 | 5,909 |

| Upside scenario | 6,004 | 5,873 | 6,033 | 6,209 | 6,378 |

| % variation | 0.0% | 0.0% | 2.6% | 5.2% | 7.9% |

| Downside scenario | 6,004 | 5,873 | 5,835 | 5,808 | 5,769 |

| % variation | 0.0% | 0.0% | -0.8% | -1.6% | -2.4% |

Source: Scottish Government

3.11 Funding Risk Management

3.11.1 Tools available within the Fiscal Framework

The Fiscal Framework provides the Scottish Government with limited fiscal tools to manage volatility and risk.

The Scotland Reserve enables the Scottish Government to defer funding or carry forward underspends, within set limits: the Scotland Reserve is capped in aggregate at £700 million, with an annual drawdown limit of £250 million for resource and £100 million for capital.

The Scottish Government can use Resource Borrowing in very specific circumstances - for cash management and to address tax and social security forecast error reconciliations.

The total cumulative limit for resource borrowing is £1.75 billion. The normal annual limit for all resource borrowing is £600 million but for forecast error the annual limit is £300 million and for cash management the annual limit is £500 million. Resource borrowing can only be sourced from the National Loans fund (NLF) and the term of any loans must be between 3 and 5 years.

The triggering of the 'Scotland-specific economic shock' provision in 2021-22, means that some of these restrictions are relaxed until 2023-24. This includes the drawdown limits for the Scotland Reserve and an increase to the annual limit for resource borrowing for forecast error from £300 million to £600 million.

3.11.2 Limitations of powers compared with scale of the risks

The limited range of these powers means they do not fully address the fiscal risks they are intended to mitigate, or the volatility the Scottish Budget is exposed to. We have published analysis in previous Scottish Government MTFS documents illustrating that the £300 million annual borrowing limit for forecast error is insufficient to cover the degree of forecast error risk the Scottish Budget is exposed to each year. Based on the 2018-19 Budget forecasts, there was between a 5% and 17% probability of negative Income Tax reconciliations exceeding -£300 million. Updating this analysis to include all devolved taxes and social security benefits and rebasing this to the 2023-24 Scottish Budget it is estimated that there is now between a 14% and 27% probability of total negative reconciliations breaching the £300 million annual borrowing powers for forecast error.

This risk will continue to grow as borrowing powers are fixed in nominal terms, meaning their value is eroded each year in real terms.

This lack of borrowing provision is most clearly demonstrated by the forecast position in 2024-25, where reconciliations are currently forecast to be £687 million. As 2024-25 is also first year where the Scotland Specific Economic shock rules cease to apply, this creates an unmitigated exposure of £387 million.

The Scotland Reserve theoretically provides an opportunity to address anticipated forecast exposures or reconciliation shortfalls which exceed borrowing capacity, but the current limits mean that in practice this is not feasible.

The Scotland Reserve does not represent "additional" funds, it is simply the rolling forward of funds not spent in previous financial years, whether as a result of planned deferral of funding or unanticipated late adjustments at the end of a financial year. In order to use the Reserve to address an anticipated future reconciliation, the Scottish Government would need to plan to underspend its budget in one financial year at a point where the full extent of the in-year funding position is not clear.

Such underspending would generate additional risks for the Scottish Government. As only £250 million of resource funding can (normally) be drawn down in one financial year, the Scottish Government would have almost no margin for error to avoid funds being locked in the reserve (and unable to access them), or have funding surrendered to HMT if the £700 million total reserve cap was breached.

Lifting of the drawdown limits and an increase in the reserve cap to a more sustainable level would go some way to improving the Scottish Government's practical ability to manage volatility in its funding position.

The planned review of the Fiscal Framework (see Box 4) is an important opportunity to address the limitations of borrowing and reserve powers, among others.

Box 4: Fiscal Framework Review

The Fiscal Framework is due for review in 2023, following agreement between both the Scottish Government and the UK Government to jointly commission an independent report on the Block Grant Adjustment arrangements.

The review is anticipated to be a negotiation between both governments, resulting in an updated framework agreement. The final version of the independent report has been submitted to both governments for consideration, but the timing and arrangements for its publication are still under discussion with the UK Government. Discussions are ongoing between governments about the timing and process for the subsequent review.

The Scottish Government is clear that the review must minimise the volatility currently inherent in the operation of the framework. It must also ensure that Scotland has the necessary powers to manage the risks within our devolved responsibilities, and to support economic recovery.

The revised Fiscal Framework should provide the Scottish Government with budget levers commensurate to the forecast errors it has to manage - including, for example, the £687 million negative reconciliation that is forecast to occur in 2024-25.

Heading into the review the Scottish Government will aim to:

- Ensure the BGA methodology continues to protect the Scottish Budget from potential slower population growth in Scotland than in rUK.

- Secure greater budgetary flexibility and appropriate budget management tools.

- Continue to protect the Scottish Budget from economic shocks that affect the Scottish and UK economies equally.

- Ensure that the Scottish Government has the appropriate suite of policy levers and is not unduly exposed to risks outside of its control.

In the longer term, the Scottish Government believes that independence is the best route to ensuring the economy and public finances can be managed effectively and in a way that meets the needs of Scotland. Independence would also give the Scottish Government the power to design immigration policy tailored to Scotland's needs, and return the right to free movement in the EU, both of which are critical to the economy.

3.11.3 Policy Approach to the management of funding risks

Whilst the combined risks across the funding outlook are significantly greater than the tools available to manage them, it is nonetheless important to consider the full spectrum of risks in any decisions on the use of discretionary funding tools such as drawdowns from the Scotland Reserve and borrowing. The Scottish Government has considered the interaction of these risks and mitigations available and this has led to a slight revision to Reserve and Resource borrowing policy for this MTFS.

Previous approach

Previous iterations of the Scottish Government's MTFS have outlined the following Scotland Reserve and Resource Borrowing policies:

- The Scottish Government prioritised use of the Scotland Reserve to carry forward any forecast underspends for use in the subsequent financial year. This was intended to ensure that there was sufficient capacity in the reserve to be able to also carry forward any additional underspend that emerges later in the budget process (i.e., at provisional and final outturn stages) and mitigate the risk of funds being lost to the Scottish Government.

- The Scottish Government assessed all planned resource borrowing decisions to smooth the funding trajectory over five years. This was by considering the net effect of the forecast reconciliations, resource borrowing and repayments of resource borrowing.

The principles behind these policies are intended to balance risks; ensuring budgets are balanced, funding is not lost, and that borrowing is maintained at sustainable levels.

Experience to date has shown that the reconciliations are themselves so volatile that it is difficult to measure the efficacy of any borrowing decisions by these specific metrics. It is also the case that by restricting measurement to reconciliations and costs, the wider impact of resource funding volatility in year, and across years, is not fully considered. Borrowing and Scotland Reserve decisions need to be taken together, given the relationship between them. Finally, the Scottish Government does have some discretion in other sources of income which are fully devolved and unrestricted by an HM Treasury budget limit or Fiscal Framework limit defined in statute. An example includes the receipts from the Kings Lord Treasurer Remembrancer (KLTR). These items allow some minimal additional flexibility in some financial years.

Consequently, the Scottish Government's approach is being adjusted to one which applies to all discretionary funding tools in order to maximise the impact of the collective fiscal tools available.

Current approach

The Scottish Government will use its limited discretionary funding tools, such as the Scotland Reserve and Borrowing, to achieve the following in objectives in order of priority:

1. Ensure a balanced budget by the end of each financial year,

2. Mitigate volatility in the medium term resource funding outlook.

By necessity decisions on borrowing and the Reserve will be finalised at the end of each financial year and use the best estimates at the time of in-year and future year funding positions.

Projections of discretionary funding for future years, where required for establishing the Central Funding Outlook, will be considered on a case-by-case basis, balancing these two key objectives. Projections remain subject to change with drawdown decisions taken in March of any financial year.

Contact

Email: sophie.osborn@gov.scot