Scottish economic insights: September 2025

Provides a summary of latest key economic statistics, forecasts and analysis on the Scottish economy.

Economic outlook.

The increased uncertainty coupled with existing weakness in business and consumer sentiment continue to weigh on the economic outlook for this year and next.

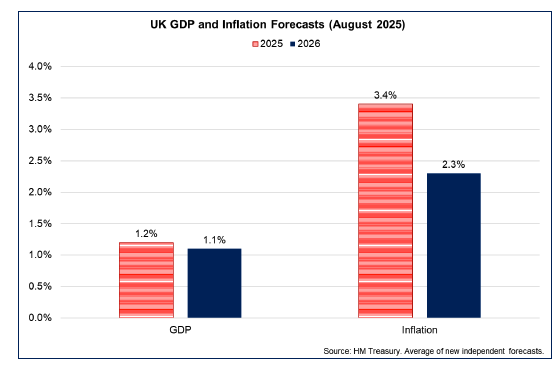

According to the latest HMT average of new independent UK forecasts from August, UK GDP growth is projected at 1.2% over 2025 and 1.1% over 2026.[27] This reflects a slightly stronger outlook than forecast in July but still indicates that the pace of economic growth is expected to remain broadly stable over the next year. Similarly, the Bank of England forecast UK GDP growth to remain stable at 1.25% in both 2025 and 2026, before picking up to 1.5% in 2027.

In Scotland, the Scottish Fiscal Commission (SFC) forecast in May that economic growth will slow to 1.1% in 2025 before strengthening to 1.8% in 2026 and 1.7% in 2027. This reflects a more subdued outlook for growth than in the SFC’s previous forecasts from December 2024.[28] Similarly, the Fraser of Allander Institute, in July, revised down its forecasts for Scottish GDP growth down to 0.8% for 2025, before rising slightly to 1% in 2026 and 1.1% in 2027.[29]

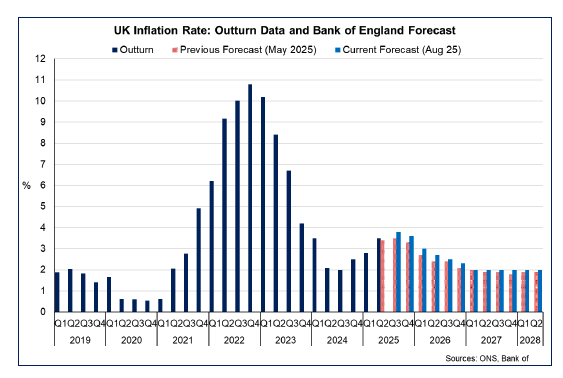

The outlook for consumers continues to be challenging. The latest HMT average of independent forecasts shows that inflation is expected to average 3.4% over 2025 and 2.3% over 2026. This reflects a higher forecast in August than in July for 2025, and the forecast for 2025 has been steadily going up since the start of the year. The latest Bank of England forecasts from August also show inflation to be more persistent than previously forecast. UK inflation is forecast to rise from its current rate of 3.8% to 4.0% in September and average 3.8% in Q3 2025 before gradually falling back to the 2% target in Q2 2027. This is a higher peak and slightly more persistent than the inflation forecast in May.

The Bank reduced the interest rate to 4% in August, reflecting the expectation that the rise in inflation this year will be temporary and that the continued gradual approach to loosening the restrictiveness of monetary policy is appropriate to meeting the 2% inflation target in the medium term. The overall decrease in the Bank Rate over the past year from 5.25% to 4% is providing improving financial conditions for consumers, however broader economic uncertainty remains a key factors that is influencing the feed through of this to consumption. The pick-up in savings ratio alongside the Scottish Consumer Sentiment Indicator’s spending sub-indicator remaining persistently negative, indicates that consumers’ attitudes to spending continues to be guarded.

Food price inflation is expected to be a key concern for households. The Bank of England highlights that global demand and supply factors influencing food and commodity prices have been key factors contributing to the current high rates and forecast rates of food price inflation. Food inflation is expected to increase from its current rate of 4.8% to 5.5% by the end of the year. The Bank notes that there is evidence showing that food price inflation can have an outsized impact on household inflation expectations. Due to this, the Bank will continue to closely monitor the impact food prices may have on household inflation expectations and any resulting risk to the disinflation process.[30]

Additional risks to the disinflation process may emerge from the fact that wages are expected to continue growing over the coming year. The Bank of England’s Agents’ pay survey results show that pay settlements averaging 3.7% in 2025 overall with very early indications of pay settlements for 2026 in the range of 2%–4%. Furthermore, the Bank’s Decision Maker Panel (DMP) for August reports that the year-ahead wage growth is 3.6%. This is, however, down from the reported annual wage growth of 4.6% in the three months to August, and demonstrates that firms expect the pace of wage growth to decline by 1 percentage point.[31] While wage growth might provide consumers some relief, it continues to risk further generating inflationary pressure which may in turn continue to impact consumer spending habits.

Overall, the growth in Scotland’s economy in the first half of 2025 has been in line with forecast, which is positive given the global economic developments which have occurred this year. The outlook for this year and next remains subdued both globally and domestically, highlighting the challenging environment and the elevated uncertainties. However, easing inflationary pressures, loosening financial conditions, the resilience in business optimism and underlying strength in the labour market provide grounds for optimism.

Contact

Email: economic.statistics@gov.scot