Scottish economic insights: September 2025

Provides a summary of latest key economic statistics, forecasts and analysis on the Scottish economy.

Labour market conditions.

Employment and unemployment

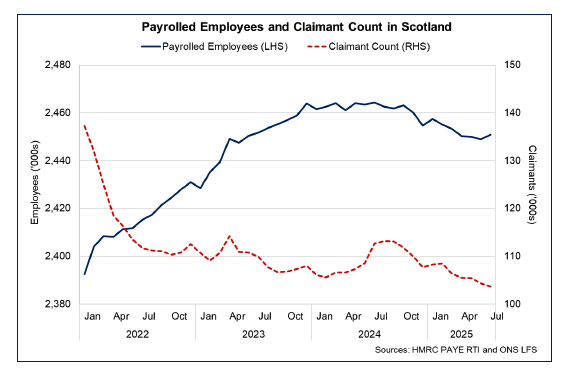

Over the first half of the year, Scotland’s labour market continued to indicate robust performance with low unemployment and high employment. However, falls in payrolled employment indicate loosening in the labour market which is further underlined by a reduction in recruitment activity.

The headline unemployment rate for Scotland has remained low over the first half of the year and in May-July was 3.5%, down from 4.2% in February-April. The continuation of low unemployment over the past year has also been reflected in the claimant count unemployment rate. Scotland’s claimant count unemployment rate in August was 3.5% with the number of claimants falling by 9,000 (7.6%) over the year. The rate has been broadly consistent through the first half of the year.[13]

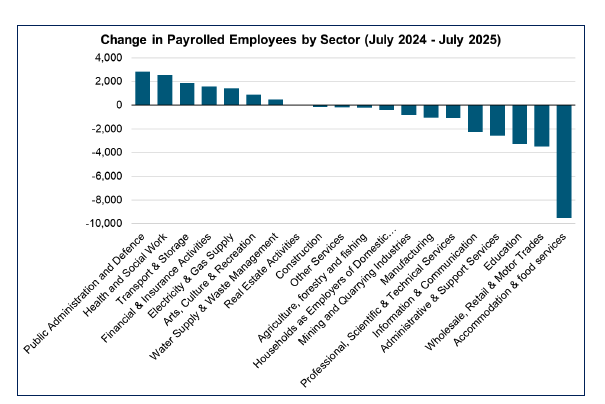

The number of payrolled employees in August remained high (2.45 million), albeit has fallen by c.16,000 employees (0.7%) over the past year, indicating continued loosening in the labour market. In July, the largest fall in the number of employees was in the Accommodation and Food Service Activities sector (c. -9,500 employees), offsetting an increase of c. 2,800 employees in the Public Administration and Defence sector. The fall in employment in the Accommodation and Food Service Activities sector (which is a labour intensive sector) accounted for 37.9% of the total fall in employee numbers in Scotland over the year.

A possible catalyst for the fall in employment in the sector may be from the increased employers’ National Insurance Contributions (NICs), announced in the UK Autumn Budget and the increase in the minimum wage, both introduced in April. The increase in costs for employers may have resulted in reduced hiring in lower-paying sectors, including Accommodation and Food Services, Admin and Support, and Wholesale and Retail.

Recruitment activity

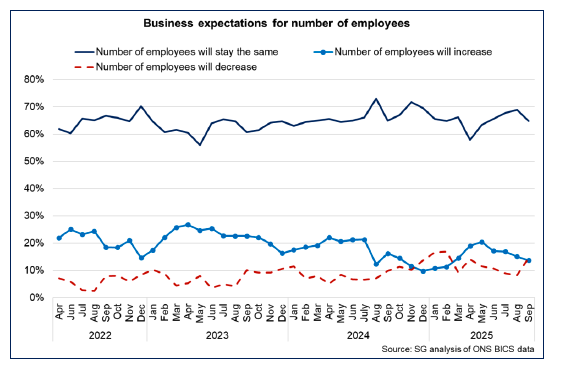

The evidence on loosening in the labour market is further supported by BICS data, with 14.6% of businesses expecting employee numbers to decrease in September, up from 8.3% in August. More broadly, the share of businesses expecting the number of employees to decrease remains higher than reported during 2024.

This is particularly evident in the Accommodation and Food Services where 37.8% of businesses expect reductions in headcount in the coming month. This potentially ties in with the number of payrolled employees falling over the past year; however, it also accounts for seasonal changes in labour demand within the sector.

Business survey indicators also show evidence of loosening within the labour market. The RBS Growth Tracker employment indicator remained below the 50 no-change level for the third consecutive month in August (48.5), indicating that businesses are slightly reducing headcount. This trend has been relatively consistent throughout the calendar year, with the indicator showing businesses have been reducing staff numbers for most of 2025 apart from April when employment was constant (50) and May where businesses marginally increased staff numbers (50.2).[14]

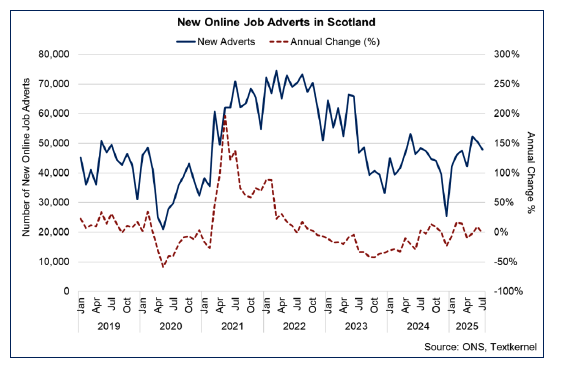

Furthermore, online vacancies data indicates that recruitment activity has been stabilising from elevated levels in 2022, and most recently, online job adverts fell by 1.1% (c. 500 job adverts) over the year to July. This indicates marginally reduced recruitment activity by businesses, and more generally, continued stabilisation in recruitment intentions over the first half of the calendar year.[15]

Earnings

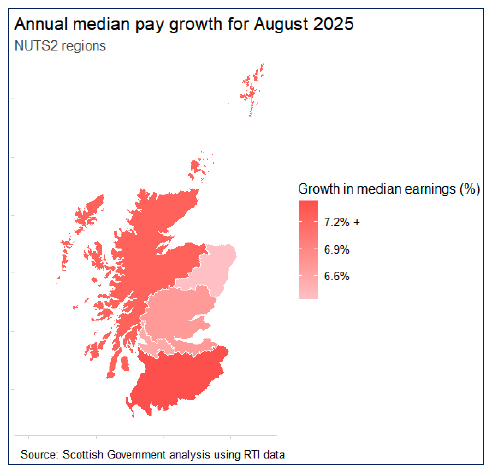

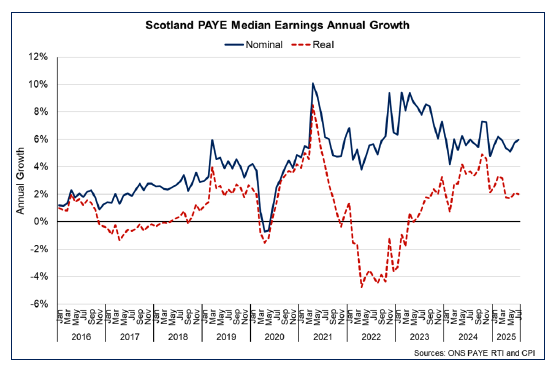

Despite continued loosening in the labour market, earnings growth has remained strong over the first half of the year, with nominal earnings growing by 6.5% in the year to August. Nominal median earnings grew robustly across all regions in Scotland, with the highest growth rate seen in Southern Scotland (7.2%) and in Highlands and Islands (7.1%). Conversely, earnings growth was slowest in North Eastern Scotland (6.3%). Earnings in the in West Central Scotland and Eastern Scotland grew by broadly the national average, at 6.5% and 6.6%, respectively.[16]

Real earnings (inflation-adjusted earnings) growth in Scotland was 2.7% in August, with inflation unchanged at 3.8%. Nonetheless, real earnings growth has remained positive throughout the year, owing to the continued robust pace of nominal earnings growth.

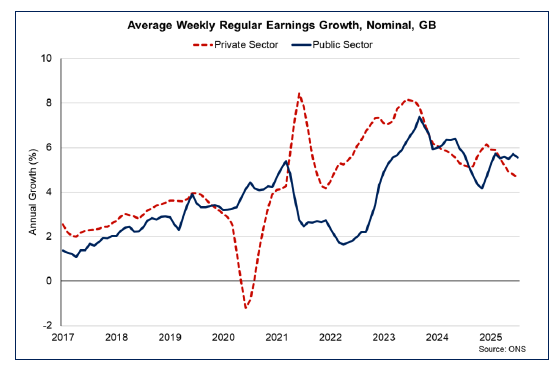

Nominal earnings growth at a GB level have remained high in both the private and public sectors throughout the first half of the year. Through the second quarter, the 3-monthly earnings growth in the public sector outpaced the private sector for the first time since August 2024. Annual growth in nominal earnings in the public sector grew by 5.6% in the three months to July, compared with 4.7% in the private sector.[17] Although pay growth remains elevated it is expected to slow significantly over the rest of the year. Results from the Bank of England in their Agents’ annual pay survey suggests pay settlements of 3.7% in 2025 with very early indications of pay settlements for 2026 in the range of 2%–4% .[18]

Contact

Email: economic.statistics@gov.scot