Scottish economic insights: September 2025

Provides a summary of latest key economic statistics, forecasts and analysis on the Scottish economy.

Household conditions.

Inflation

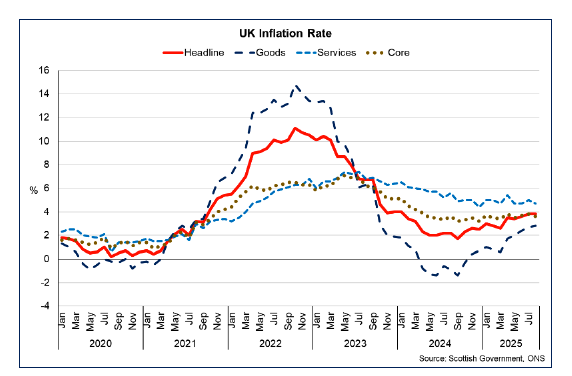

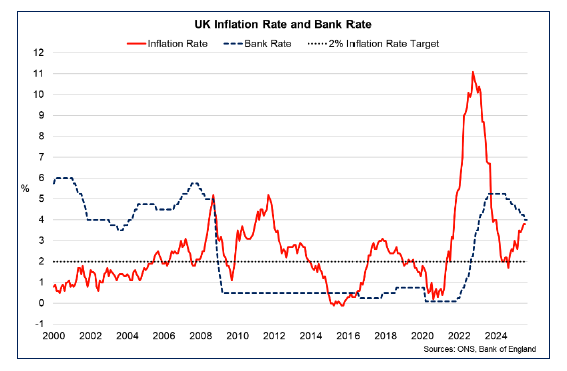

Over the first half of 2025, inflation has risen slightly, outpacing expectations at the end of last year, with consumer price inflation decreasing from 3% in January 2025 to 2.6% in March before rising again to 3.8% in July. Latest data for August shows that inflation has remained stable from last month, remaining at 3.8%.[19]

Underpinning the up-tick in inflation in the second half of the year, goods price inflation has risen from 1% in January 2025 to 2.8% in August. Over that same time period, services price inflation has remained largely stable, dipping from 5% to 4.7%. Core inflation (excluding energy, food, alcohol and tobacco) has held steady, falling from 3.7% in January to 3.6% in August.

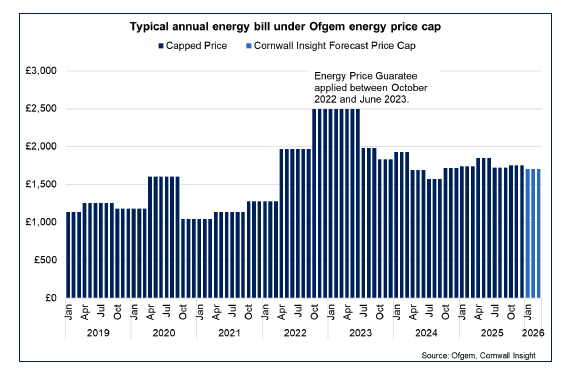

More volatile components of inflation, such as energy price inflation and food prices, have picked up over the course of the year. Whereas at the end of 2024 annual inflation in electricity, gas and other fuels was negative, this component has increased to 9.3% in August. This in part reflects increases in the energy price cap, which has risen from £1,717 annually for a typical household at the end of last year to £1,849 in Q2 2025. After falling in Q3, the price cap will increase by 2% to £1,755 for the final quarter of the year and is forecast by Cornwall Insight to fall to £1,701 at the start of 2026.[20] [21]

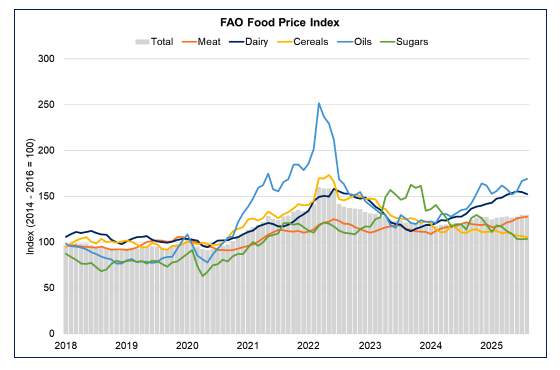

Similarly, the Food and Non-Alcoholic drinks component of CPI inflation has also picked up from the start of the year, rising from 2% at the end of 2024 to 5.1% in August. The upside risk to inflation owing to increased food price inflation has also been noted by the Bank of England given the potential impact of increased food prices on broader inflation expectations.

In their latest Monetary Policy Report (MPR), the Bank of England set out the wholesale market developments which have driven up costs of, for example, beef, dairy, coffee and cocoa beans, which has been partially attributed to unfavourable weather conditions in the locations these goods are produced. Increases in wholesale food prices are also identified in the FAO Food Price Index, which shows that the price of oils, dairy and, albeit to a lesser extent, meats are substantially elevated from their average across 2014-2016 and rising. In latest data for August, the overall index rose to 130.1, representing a 30% increase in food prices from this reference period, up from 121.7 the same time last year, albeit largely flat from last month.[22]

Consumer sentiment

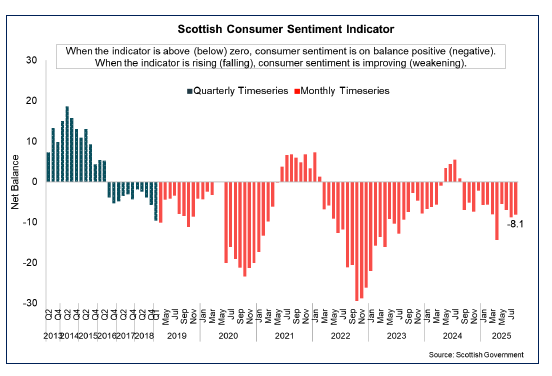

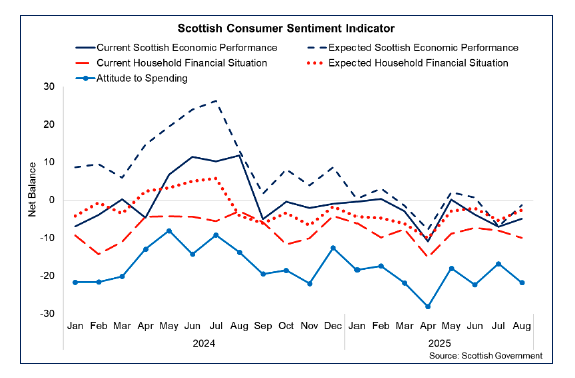

Rising prices, alongside lower real-terms earnings growth and increased economic and international trade uncertainty have likely contributed to declining consumer sentiment over the year. The Scottish Consumer Sentiment Indicator stood at -8.1 in August, up 0.7 points from the previous month, though is notably lower than the end of 2024.[23]

Sentiment across all five sub-Indicators of sentiment covering current and expected economic performance and household finances, and attitudes to spending, have fallen between December 2024 and August. Attitudes to spending remain the most negative sub-indicator, while sub-indicators on economic performance, which indicated stronger sentiment earlier last year, have broadly converged with the levels of sentiment reported on household finances.

This is in line with consumer sentiment at a UK level, with latest data from the GfK Consumer Confidence Barometer indicating a slight monthly increase in sentiment from July to August despite following a sharper drop in sentiment earlier in the year.[24]

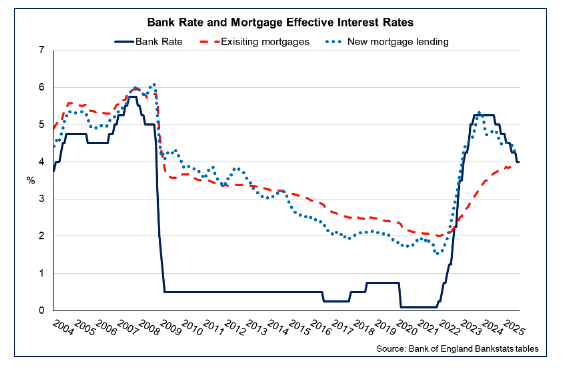

However, falling interest rates are gradually feeding into a stronger outlook for households, particularly with lower mortgage and other borrowing costs. Interest rates have been lowered three times this year by the Bank of England’s Monetary Policy Committee (MPC) from 4.75% in January to 4% in August.

This has slowly fed-through to the effective interest rates offered on new mortgages and on the effective interest rate on the total stock of mortgages. While at first rising in line with increasing central bank interest rates, the effective interest rate on new mortgages has fallen from 4.5% at the start of the year to around 4.3%, in turn stabilising the effective interest rate on the total mortgage stock which has risen from 3.8% in January to 3.9% in July.[25]

Savings ratio

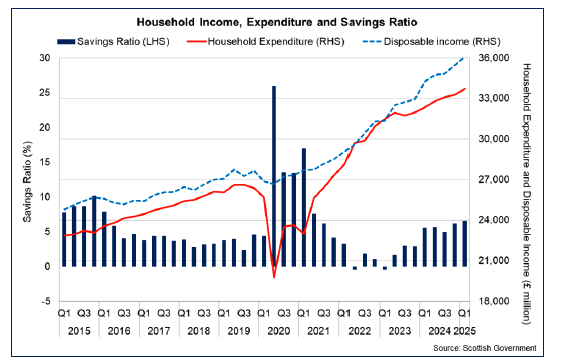

In line with elevated levels of economic uncertainty among consumers, quarterly national accounts data for Q1 2025 suggests consumers are exhibiting increased spending restraint. The Savings Ratio, a measure of funds that are available for adding into savings, including into pension funds, or paying off debt, stood at 6.6% in the latest data, rising from 6.2% in the previous quarter and up from 5.6% from the same time last year.[26]

This latest data continues the trend of increasing savings as real earnings growth continues to be positive while inflation has become relatively more stable in comparison to recent years. This comes after gross savings increased significantly during the pandemic before more recently eroding as the price shock following Russia’s invasion of Ukraine impacted household finances.

The increase in the Savings Ratio is driven by the relative growth of household expenditure and disposable income, with the former growing more slowly at 3.8%, on a four-quarter rolling average, while disposable income has increased at 6.8%. While the gap between these two measures has narrowed in the latest quarter, this reflects that incomes are rising faster than expenditure, allowing for more money to be set aside for savings.

The increase in gross savings alongside relatively weak consumer sentiment suggests households remain cautious of economic conditions and, therefore, are restrained in their consumption, presenting a key risk to the economic outlook and growth prospects.

Contact

Email: economic.statistics@gov.scot