Scottish economic insights: September 2025

Provides a summary of latest key economic statistics, forecasts and analysis on the Scottish economy.

Economic developments in first half of 2025.

Global Context

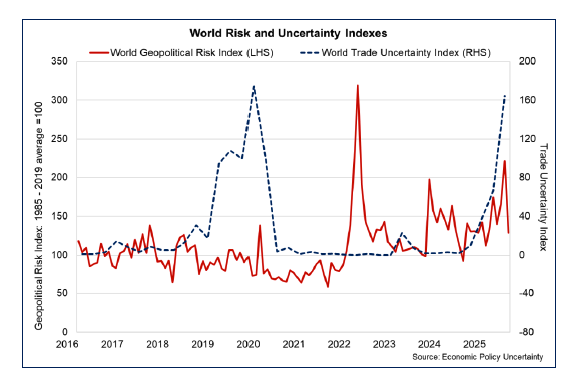

At a global level, the raft of US tariff announcements since April, and the responses from other countries, have added to a challenging global environment, as reflected by the sharp rise in the World Trade Uncertainty Index this year.[1]

These challenges remain compounded by the wars in Ukraine, Russia and the Middle East. The World Geopolitical Risk Index has remained elevated in the first half of 2025, in part reflecting the evolution of the conflicts in those regions, which continue to impact on and present risks and uncertainties for global supply chains and commodity prices.[2]

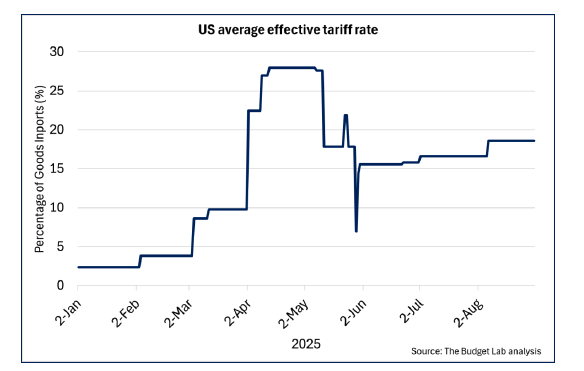

The increase in tensions also reflects the scale of the change in trade policy. Following the increase in US import tariffs announced in April, the US average effective tariff rate rose to 28%. The trade negotiations and agreements since then have resulted in the average effective rate falling to around 18% at the end of August, its highest rate since the 1930s.[3] However, this is likely to change further as more announcements and agreements are made.

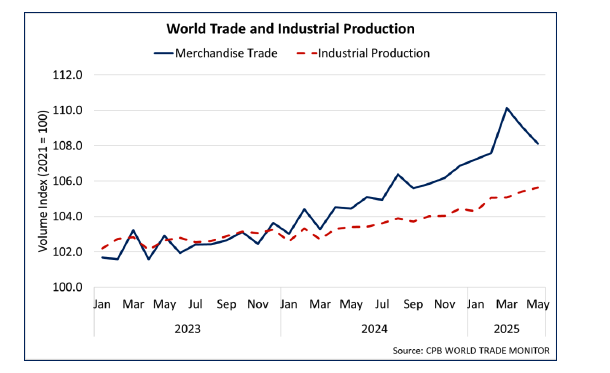

Trade uncertainty has impacted trade movements since April with evidence of some frontloading of trade in advance of the tariff announcements in April. This has built in some resilience in activity in the first half of the year which – coupled with the easing back of the US average effective tariff rate following the original announcements – has held up growth expectations more than was initially expected. However, these reflect short-term factors, and the full effects of tariff changes are likely to still be feeding through.

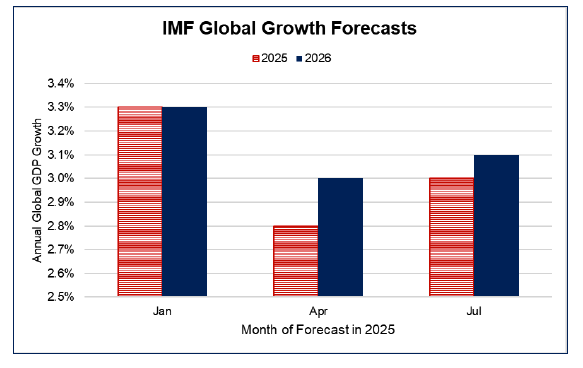

Moreover, indirect effects of tariff uncertainty and the double-sided risks they pose to global inflation and interest rate expectations continue to generally weigh negatively on business sentiment and investment intentions. The IMF forecast global economic growth to slow from 3.3% in 2024 to 3% in 2025 and 3.1% in 2026, reflecting increased global headwinds to growth and trade.[4]

This forecast is notably slower than forecast at the start of the year (3.3% in 2025 and 2026); however it is a slight improvement from April, in line with the resilience in activity owing to some front-loading of activity to earlier in the year and recent trade agreements that are less restrictive than were proposed in the initial US tariff proposals.

Box 1: Long-run economic impacts of a stylised US tariff increase

In our previous Economic Insights Report we looked at Scotland’s exports to the US.[5] Building on this, we use a Computable General Equilibrium (CGE) model to explore the long-run economic impact on Scotland of a 10% increase in US tariffs on UK goods; we also consider the impact of symmetric UK retaliation. We define the long run as approximately ten to twenty years after the shock occurs, once capital stocks, labour markets, and trade flows have stabilised.

While the simulation is stylised and does not model industry-specific tariffs, exemptions or third-country dynamics, the modelling isolates how a US-UK tariff increase ripples through Scotland’s economy in the long-run and which industries are most exposed. The results for Scotland are broadly consistent with modelling by the Northern Irish Government for Northern Ireland and the OBR for the UK.[6]

The simulation models a 10% increase in price to non-EU trade for the goods-producing industries in our Scotland and rest-of-UK (rUK) CGE model, scaled by US shares of trade. To calculate the shares we use HMRC Regional Trade Statistics for 2024 mapped to the industrial classifications in our CGE model. Spillover effects are identified by comparing results from a Scotland-only shock and a Scotland and rUK shock.

The model captures both demand and supply-side dynamics. The tariff increase reduces export demand, lowering domestic output, employment, and wages. Lower business and household income leads to lower investment, tax revenue and government spending. The retaliatory tariff raises consumer and producer prices, lowering demand and supply, deepening the impact.

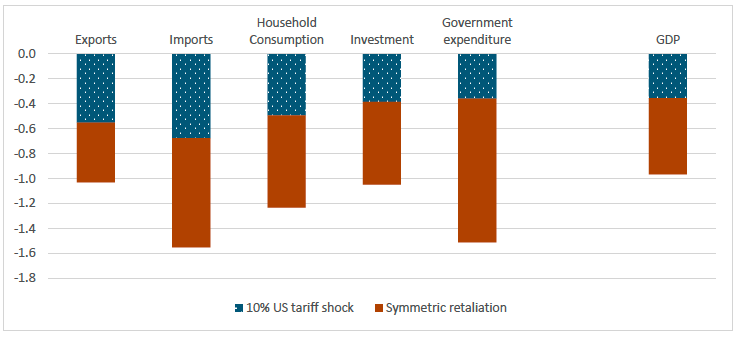

The tariff increase lowers Scotland’s GDP by 0.4% in the long run. Around a third of the impact on Scotland’s GDP is driven by spillover effects from the shock to the rUK economy. If the UK Government retaliates with a 10% tariff on US imports, Scotland’s long-run GDP is 1.0% lower than baseline.

Source: OCEA modelling

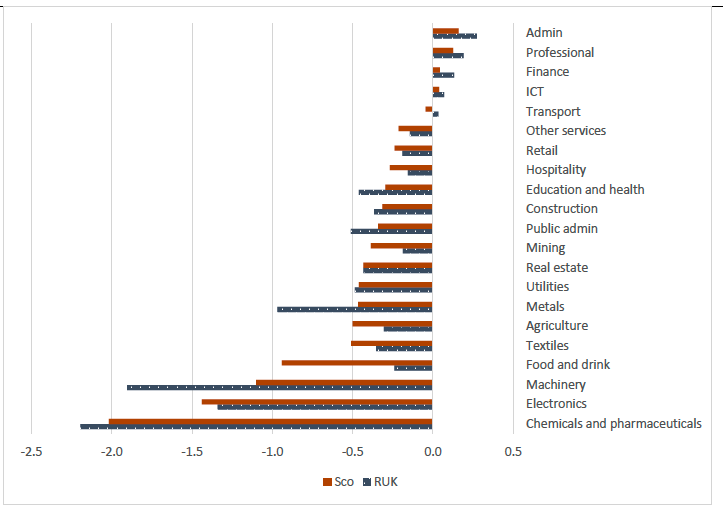

Industries for which US exports account for a greater share of economic activity, such as chemicals and pharmaceuticals, experience the greatest shortfalls in output. The overall shortfall is comparable for both Scotland and the rest of the UK, however, there are some sectoral differences. For example, Scotland’s food and drink industry is more exposed, largely due to whisky exports, while in the rest of the UK the machinery industry is more exposed, driven by road vehicle exports. Lower demand overall has wider impacts across the economy, decreasing output. However, some service industries like administration and professional roles are insulated from the demand shock and benefit slightly from labour and capital reallocation from tariff-affected sectors.

Source: OCEA modelling

Overall, the modelling shows that in isolation, an increase in US tariffs on UK goods exports leads to Scotland’s economic output being lower in the long run than it would otherwise be. The greatest impact is on goods-producing industries with higher exposure to the US market. Retaliatory tariffs significantly amplify the economic impact by shocking both demand and supply.

For more information please consult the supporting technical paper available here: Modelling the long-run economic impacts of a stylised US tariff increase: technical paper

Overview of risks

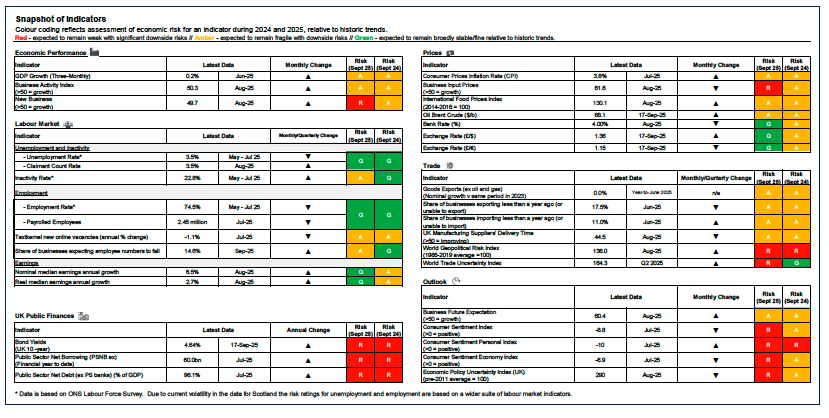

The impacts of recent developments on UK and Scottish growth and inflation remain uncertain. The table below focusses on the current risk profile across a range of economic outturn indicators in 2025, based on their position related to historical trends.[7] It illustrates that the risks around GDP growth and the labour market are broadly unchanged, albeit that aspects of risks have risen due to weakness in new business activity and looser labour market conditions. Inflation risks have also been relatively stable, with easing monetary policy counterbalancing increasing business cost pressures. Despite this and the strength of earnings growth, the current weakness in consumer sentiment raises the risks of weakening demand, which may also be linked to the elevated level of geopolitical risks and global trade uncertainty. Risks around the UK public finances remain high and suggest that there is a prospect of fiscal tightening at the UK budget in November.

Contact

Email: economic.statistics@gov.scot