Scottish Housing Market Review: Q1 2022

Summary of the latest Scottish housing market data.

Part of

Lending To Homebuyers: Mortgage Approvals & LTVs

New Mortgage Advances

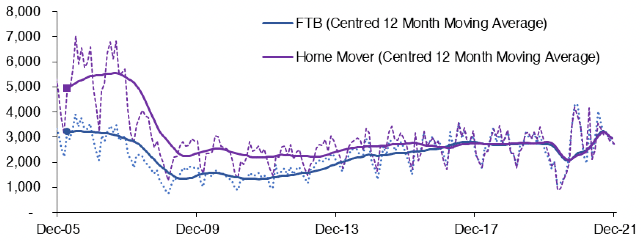

Chart 4.1 plots the monthly number of new mortgages advanced to first-time buyers and home movers in Scotland. There were 8,350 new mortgages advanced to first-time buyers in Scotland in Q4 2021, an annual decrease of 29.9% (-3,560). Meanwhile, there were 8,330 new mortgages advanced to home movers in Scotland in Q4 2021, an annual decrease of 27.9% (-3,230). Whilst the annual decreases for first-time buyers and home movers are large, this can be explained a high number of new mortgages advanced in Q4 2020 (see discussion in Sales section). Relative to the 4 year average for Q4 (2016 – 2019), new mortgages advanced to first-time buyers were up 1.0%, whilst for home movers they decreased by 2.4%. For 2021 as a whole, the annual increase in the number of new mortgages advanced to home movers (26.8%) was somewhat higher for than for first-time-buyers (22.3%), although as Chart 4.1 shows, the number of new mortgages to these two groups has been very similar since Q3 2016. (Source: UK Finance).

Source: UK Finance

Mortgage Approvals

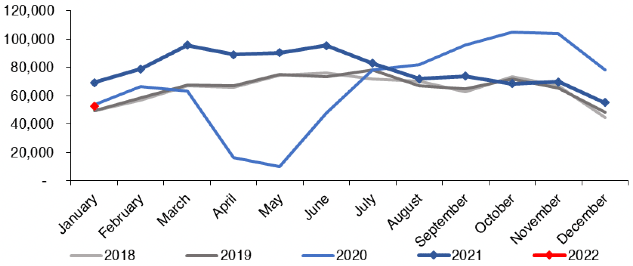

Chart 4.2 plots the monthly number of mortgage approvals across the UK for house purchase (Source: BoE). Mortgage approvals for house purchase are the firm offers of lenders to advance credit fully secured on dwellings by a first charge mortgage. This data is a leading indicator of mortgage sales as it reflects activity early in the buying process.

Mortgage approvals for house purchase across the UK rebounded strongly in the second half of 2020, with mortgage approvals increasing from 9,922 in May 2020 to 104,806 in October 2020 (see Chart 4.2). Mortgage approvals have now returned to more normal levels, with mortgage approvals for house purchase 1.5% lower in January 2022 relative to January 2020. However, this is also 24.0% below the level in January 2021, which can be explained by the unusually high level of housing market activity in the first half of 2021.

Source: Bank of England

Loan-to-Value (LTV) Ratios

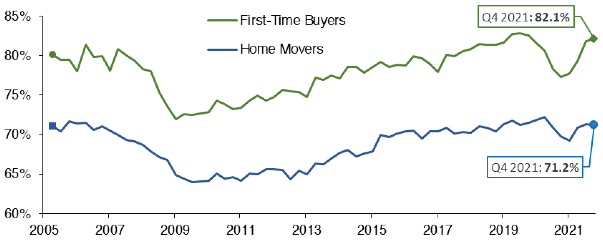

In Q4 2021, the mean Loan-to-Value (LTV) ratio on new mortgages advanced to first-time buyers in Scotland stood at 82.1%, an annual increase of 4.8 percentage points. This likely reflects the return of high LTV ratio mortgages, whose availability fell substantially during the beginning of the coronavirus pandemic. Meanwhile, the mean LTV ratio for home movers in Scotland stood at 71.2% in Q4 2021, up 1.4 percentage points over the one year period. This is shown in Chart 4.3 (Source: UK Finance).

Source: UK Finance

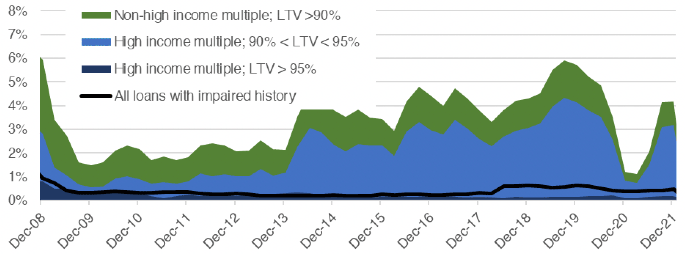

Chart 4.4 shows that there was a reduction in new lending at high LTV mortgage ratios across the UK since March 2020 but the market is starting to recover. The share of gross mortgage advances across the UK in Q4 2021 with an LTV ratio greater than 90% was 4.2%, 3.0 percentage points above the share in Q4 2020 but 1.5 percentage points lower than the share in Q4 2019. There has been a slight recovery in lending which is both high LTV and high LTI (loan-to-income) over the quarter, with the share of gross advances classified as high LTV and LTI increasing to 3.4% in Q4 2021, up by 2.4 percentage points on Q4 2020 but 0.9 percentage points lower than the share in Q4 2019.

* Higher risk lending is classified by the FCA as an LTV over 90% and an income multiple greater than or equal to 3.5 for single income purchasers, or greater than or equal to 2.75 for joint income purchaser/s

Source: FCA

There has been a substantial increase in the number of high LTV products offered by mortgage lenders, with the number of 95% LTV mortgages products increasing from 5 in March 2021 to 342 in March 2022. This recovery could in part reflect the UK Government's Mortgage Guarantee scheme. The Mortgage Guarantee Scheme aims to increase the availability of 91% - 95% LTV mortgage products by providing a government guarantee that would compensate lenders a portion of their losses in the event of foreclosure. The scheme was launched on 19 April 2021 and will close on 31 December 2022. However, a number of high LTV products have been introduced outside this scheme (Source: Moneyfacts Mortgage Treasury Report).

Contact

Email: William.Ellison@gov.scot