Scottish economic insights: March 2026

Provides a summary of latest key economic statistics, forecasts and analysis on the Scottish economy.

Household conditions

Inflation

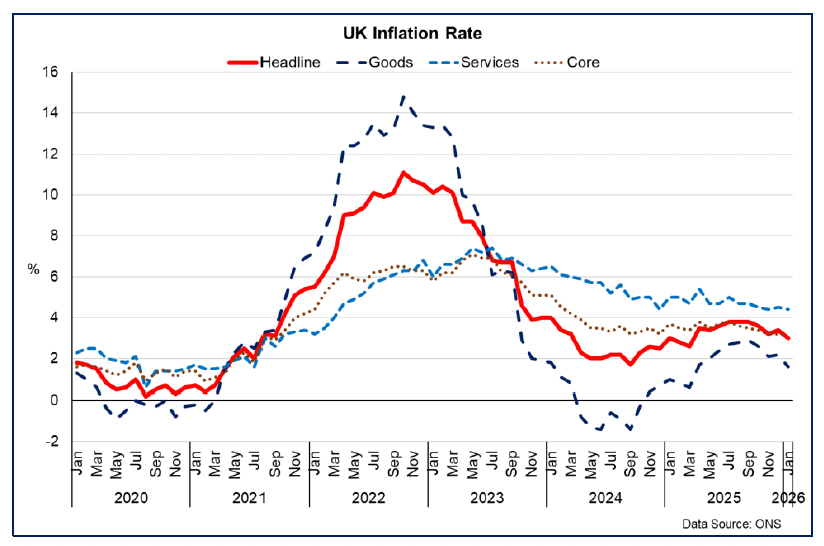

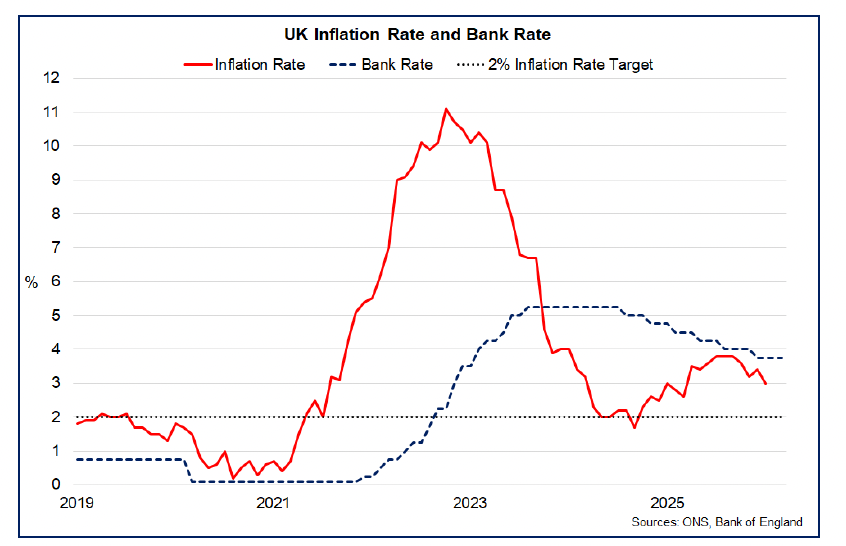

UK inflation picked up in 2025 from 3% at the start of the year and peaked at 3.8% during the third quarter before slowing to 3.4% in December and 3.0% in January.[33]

The easing in headline inflation has been reflected across its main components. Goods price inflation has fallen from 2.9% in September to 1.6% in January while the fall in services price inflation from 4.7% to 4.4% has been more moderate. Core inflation (excluding energy, food, alcohol and tobacco) has maintained its downward trajectory, falling from 3.5% in September to 3.1% in January.

More volatile components of inflation such as energy price inflation and food prices, eased in the second half of 2025 having picked up during the first half of the year. Electricity, gas and other fuels inflation fell from 9.4% in September to 2.1% in January while food and non-alcoholic beverages inflation fell from 5.1% in August to 3.6%. As important aspects of the household budget, the conflict in the Middle East has the potential to impact these aspects of the cost of living, depending on how prolonged the conflict is and the duration of impact on oil and gas prices and wider commodity prices.

Prior to the conflict in the Middle East, inflation was forecast to fall to around 2% in April, which partly reflects the 7% fall in the Energy Price Cap in that month, which will protect households from any increase in average energy bills until the next price cap at the start of July.[34]

Reflecting the recent sharp spike in heating oil prices, the UK Government also announced a £53 million support package for heating oil users in rural communities. However, the increase in energy prices has already led to road fuel prices increasing, and inflation is now expected to be higher over the coming months than it otherwise would have been.

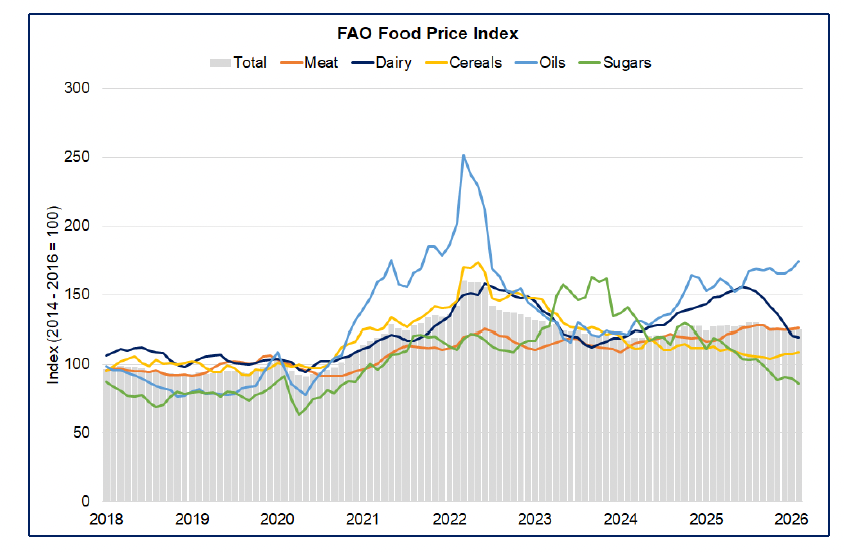

The recent easing of food price inflation is also reflected in movements in wholesale prices, with the FAO Food Price Index gradually falling from 128.6 in September to 124.2 in January, albeit it picked up slightly in February to 125.3.[35] A prolonged military conflict in the Middle East increases the risk of inflationary pressures in oil and gas spilling over into wider commodities, both directly and indirectly.

Consumer sentiment

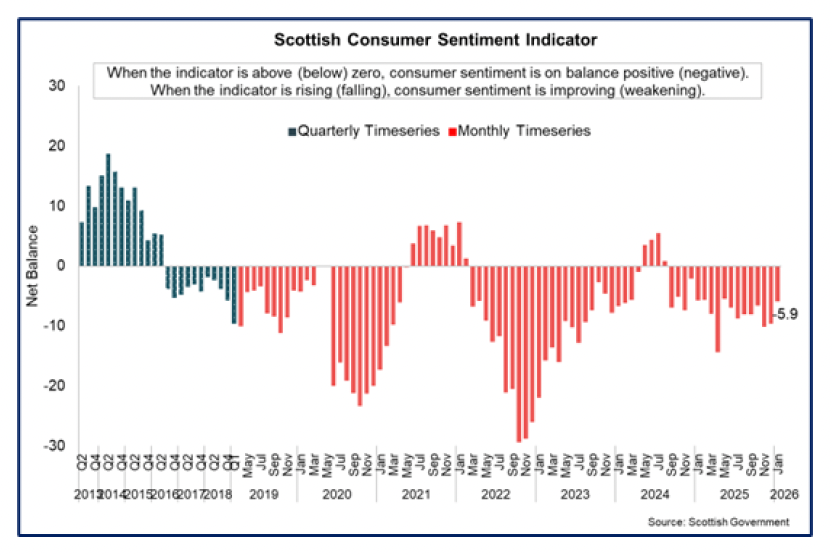

Consumer sentiment in Scotland has remained weak over the past year, likely reflecting ongoing pressures on household budgets and wider economic uncertainty at both a domestic and global level. However, it has been on an upward trend from the second half of 2025, which chimes with some of the improvements in conditions supporting consumers including the falls in inflation and interest rates.

The Scottish Consumer Sentiment Indicator stood at -5.9 in January 2026, improving by 3.7 points from -9.6 in December and reaching its highest level since May 2025, indicating a strengthening in consumer confidence at the start of the year.[36]

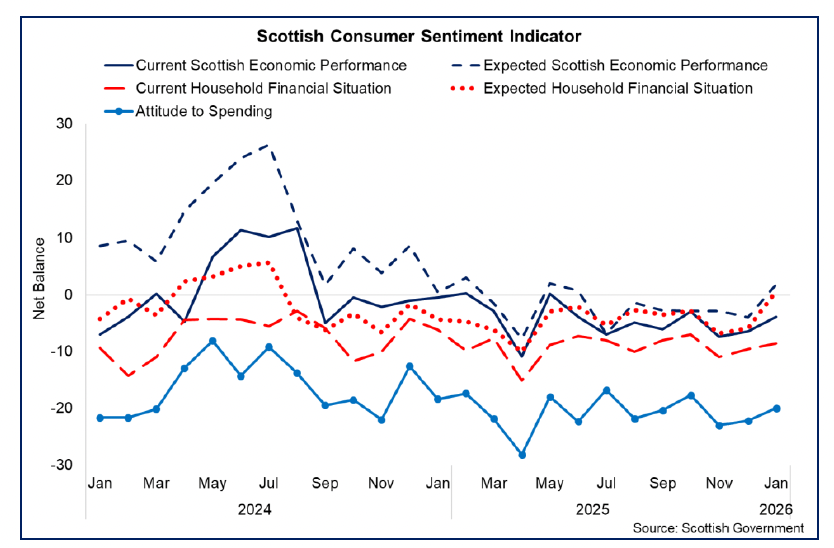

Sentiment across the sub-indicators covering current and expected economic performance, household finances and attitudes to spending remained relatively subdued through 2025. Attitudes to spending continued to be the most negative component, however it and the indicators relating to the Scottish economy and household finances all improved through the turn of the year. Notably, expectations for both the economy and household finances were positive, suggesting improving confidence in the outlook among households.

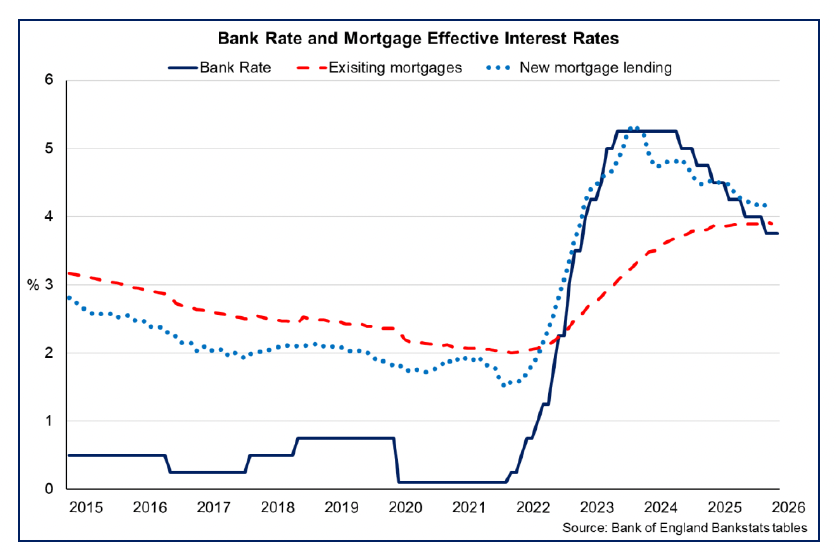

The moderation in inflationary pressures and reduction in interest rates over the past year have gradually strengthened the economic environment for consumers and households. Interest rates have been lowered four times since the start of 2025 by the Bank of England’s Monetary Policy Committee (MPC) from 4.75% to the current rate of 3.75%. However, at their meeting in March, the Bank of England (in line with the ECB and US Federal Reserve) held interest rates unchanged at 3.75% reflecting the recent increase in risks and uncertainty in the inflation outlook due to the conflict in the Middle East. The Bank now expect inflation to remain between 3% and 3.5% over the second and third quarters of this year, higher than their February forecast which projected inflation to settle around 2% over that period.[37]

The reduction in interest rates over the past year have gradually fed through to the effective interest rates offered on new mortgages and to the effective interest rate on the total stock of mortgages. The effective interest rate on new lending has eased from 4.51% at the start 2025 to 4.1 in January 2026, while the effective interest rate on the total mortgage stock, has further stabilised, rising from 3.8% to 3.9% over the same period.[38]

Savings ratio

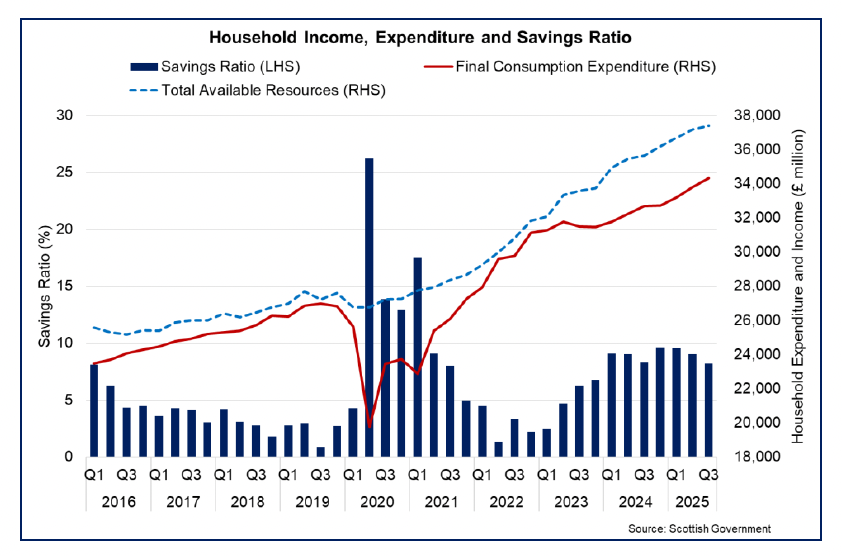

The savings ratio, a measure of funds available for saving, including pension contributions or debt repayment, stood at 8.2% in Q3 2025, down from 9.1% in the previous quarter and slightly lower than the 8.3% recorded a year earlier.[39]

Movements in the saving ratio reflect that household spending grew 5% over the past 12-months while disposable income increased by 4.8%.

While expenditure growth has recently outpaced income growth, the saving ratio continues to indicate that households retain some capacity to set aside income, providing an indication of broader trends in household sector finances.

Contact

Email: economic.statistics@gov.scot