Scottish economic insights: March 2026

Provides a summary of latest key economic statistics, forecasts and analysis on the Scottish economy.

Recent economic developments

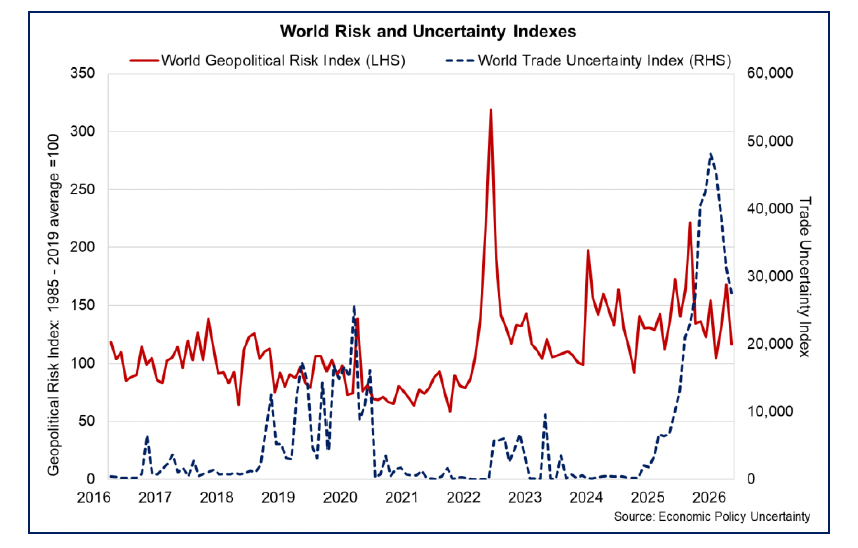

Global context

Global economic uncertainty and risks to the economic outlook have risen significantly following the military conflict in the Middle East. Since the US and Israel air strikes at the end of February and subsequent retaliation by Iran, the widening of military impacts on countries across the region and the significant disruption to oil and gas supplies from the region has resulted in a notable rise in the potential global economic implications in both the near and medium term. This comes on the back of a range of global geopolitical and trade tensions over the past year which have presented a challenging global environment for businesses and households to navigate.

The Middle East accounts for around 3% of global GDP, however its importance in the global production of oil and gas, other commodities such as fertiliser components, and as hubs of international travel, mean that the disruption to the regional economy presents significant supply and inflationary risks across a range of energy and commodity markets and into sectors including international travel and tourism.

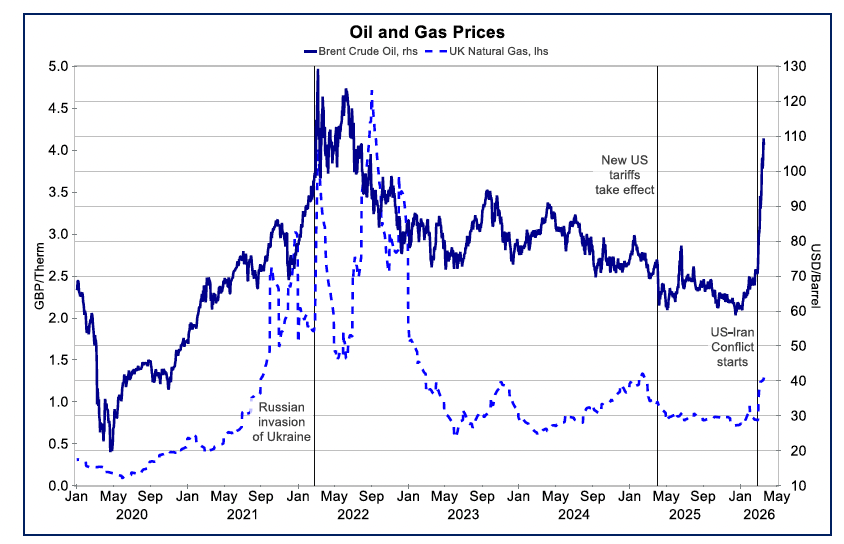

The most prominent impact at this point in the conflict is the significant disruption to oil and gas production and supply from the region and the implications this could have for global inflationary pressures the longer the disruption continues. The Middle East accounts for c. 30% of global oil production and c. 20% of global natural gas production, however the shipping of exports through the Strait of Hormuz has been brought to a virtual standstill due to the risks of attack, while military action has directly impacted on refinery and gas facilities in countries including Saudi Arabia and Qatar.

In response to this, Brent Crude oil has risen above $100 per barrel, spiking at one point at £119, while UK natural gas prices have broadly doubled and have spiked to 164 p/therm.

The extent to which this feeds through into domestic inflationary pressures in higher energy prices remains uncertain and will depend on how long the supply disruption and price pressure lasts. The most immediate impacts have been increases in heating oil prices and road fuel prices which will directly impact household costs, particularly in rural areas.

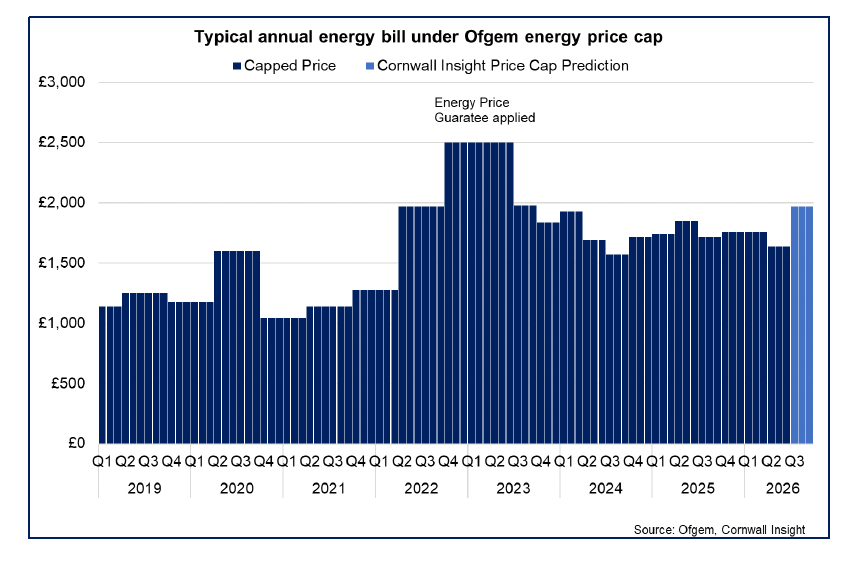

In terms of household electricity and gas prices, the Energy Price Cap is currently set for the first half of 2026, which will see a 7% fall in April for the average household (set prior to the start of the conflict). This means that the impact on energy bills will not be felt before July. Early forecasts, based on information through the first half of March, indicate a 20% increase in the cap at that point, however there remains significant uncertainty and will depend on how energy prices evolve over the coming months.[1]

In terms of the extent to which the increase in oil prices feed through to CPI inflation more broadly will depend on how long oil prices remain elevated, with external commentators providing a range of estimates. An early scenario projection from the Resolution Foundation suggests that a 20% increase and doubling of wholesale prices for oil and gas respectively, sustained for a quarter, would add around £500 to the typical annual energy bill for households on a price cap tariff, and raise the rate of inflation by around 1 percentage point.[2]

NIESR consider two scenarios based on oil prices rising to $100 per barrel and gas prices more than doubling. In a scenario which assumes that energy prices begin to normalise after one quarter this would result in a 0.3 p.p increase in inflation and a negligible impact on GDP for 2026. If the increase persisted for a year, this would increase inflation by 0.7 p.p and would reduce output growth by 0.2% in 2026.[3]

Both these estimates suggest that the impact on domestic inflation will be lower than that seen in the first year of the Russian invasion of Ukraine in 2022 which is shown in the inflation chart in the household conditions section.

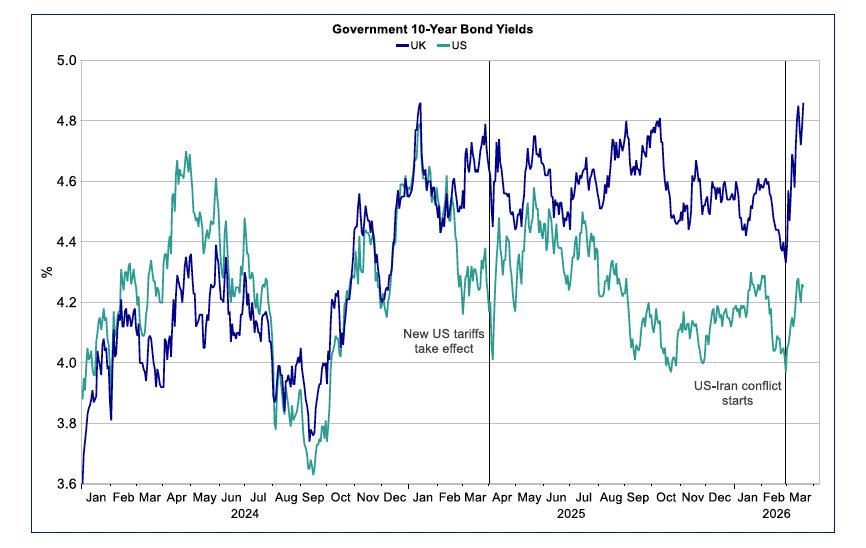

The channels through which a more prolonged military conflict and disruption to oil and gas supply would impact the global economy are broader than through energy inflationary channels. An increase in expectations that Central Banks will need to maintain interest rates higher than they otherwise would have has put upward pressure on bond yields (cost of government borrowing) and wider expectations of borrowing costs, with reports of increases in mortgage rates. Furthermore, a spillover from higher oil and gas supply disruption and pricing into other commodity and global supply chain costs, for example fertiliser and food prices, risks further exacerbating wider inflationary pressures, weighing on global and domestic trade and investment flows and growth.

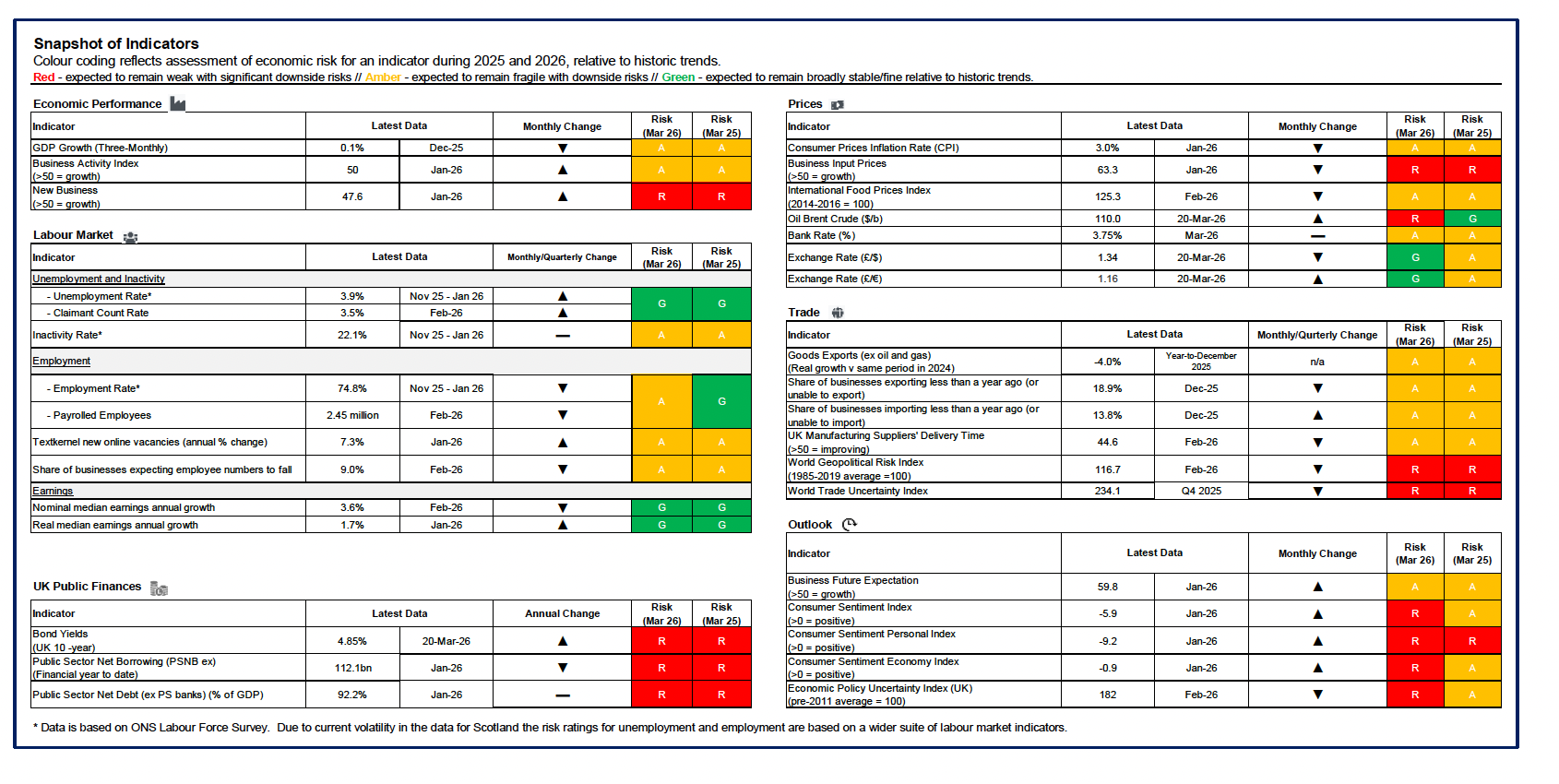

The table below presents the current risk profile to the Scottish economy across a range of economic outturn indicators in 2025 and the start of 2026 (prior to the escalation of the conflict in the Middle East), based on their position related to historical trends.

As set out above, the conflict currently presents a new inflationary risk to the Scottish economy through the increase in oil and gas prices, however the overall risk to headline inflation and wider indicators remains uncertain at this point and will depend on how prolonged the disruption to global oil supplies is.

The conflict has the potential to exacerbate the existing most notable downside (red) risks to the Scottish economy that have persisted over the past year, in part through global geopolitical and trade uncertainty channels, demand in the economy and through public finances and costs to businesses. It also risks compounding risks which have worsened over the past year in consumer sentiment and policy uncertainty.

There are a number of risks that remain fragile (amber) in the Scottish economy at this point, mainly around the relatively subdued, albeit positive, growth in GDP and business activity. Unemployment remains low in the Scottish economy, however there has been a loosening in labour market conditions around employment. Above target headline inflation remains fragile, with risks building from the conflict and potentially impacting international food prices.

Alongside low unemployment, risks in earnings growth remain stable (green), in part supported by the fall in inflation over the past year which has enabled the stabilisation in risks around interest rates and currency as the previous restrictiveness in monetary policy has been gradually loosened.

Overall, the risk profile in the economy is currently skewed to amber and red, despite there being modest improvements in a number of economic conditions. The conflict in the Middle East has increased uncertainty in the economic outlook and has increased the likelihood that the overall risk profile will worsen rather than improve over the coming year. [4]

Contact

Email: economic.statistics@gov.scot