Technology, Digital and Media

Introduction

The technology, digital and media sector contains the following sub-sectors:

- Manufacture of computer, electronic and optical products,

- Digital industries,

- IT and telecommunications and

- Publishing and audio visual.

The analysis in this report is based on the sector definitions from Scotland’s Export Performance Monitor. This definition allows for consistent analysis to be carried out and eliminates the risk of double-counting companies across multiple sectors. This sector covers a broad range of activities from the manufacturing of computer equipment to software development and parts of the creative industries.

While this definition is organised to best match the sector definition used by our enterprise agencies and Scottish Development International (SDI), the support they provide covers a wider range of action than that described in this analysis. For example, in addition to the activities covered here, our enterprise agencies support the role of digital technologies within the whole economy (i.e. the supporting infrastructure and development of digital technologies in every industry).

In 2017, the technology, digital and media sector accounted for 6.4 per cent of total registered enterprises in Scotland, 4.2 per cent of employment and 7.2 per cent of total turnover.

Table 1: Technology, Digital and Media, Number of Enterprises, Employment and Turnover, 2017

| All Private Sector VAT/PAYE Registered Enterprises |

||||||

| Sector/Sub sector |

Enterprises |

Employment |

Turnover (£ million) |

Enterprises (% of total) |

Employment (% of total) |

Turnover (% of total) |

| Technology |

11,325 |

80,810 |

18,711 |

100% |

100% |

100% |

| Manufacture of Computer, Electronic and Optical Products |

365 |

9,740 |

1,912 |

3% |

12% |

10% |

| Digital Industries |

8,160 |

33,100 |

10,958 |

72% |

41% |

59% |

| IT and Telecommunications |

840 |

22,740 |

4,402 |

7% |

28% |

24% |

| Publishing and Audio Visual |

1,965 |

15,230 |

1,439 |

17% |

19% |

8% |

Source: Inter-departmental Business Register (IDBR). Proportions may not sum to 100 due to rounding.

Export Performance

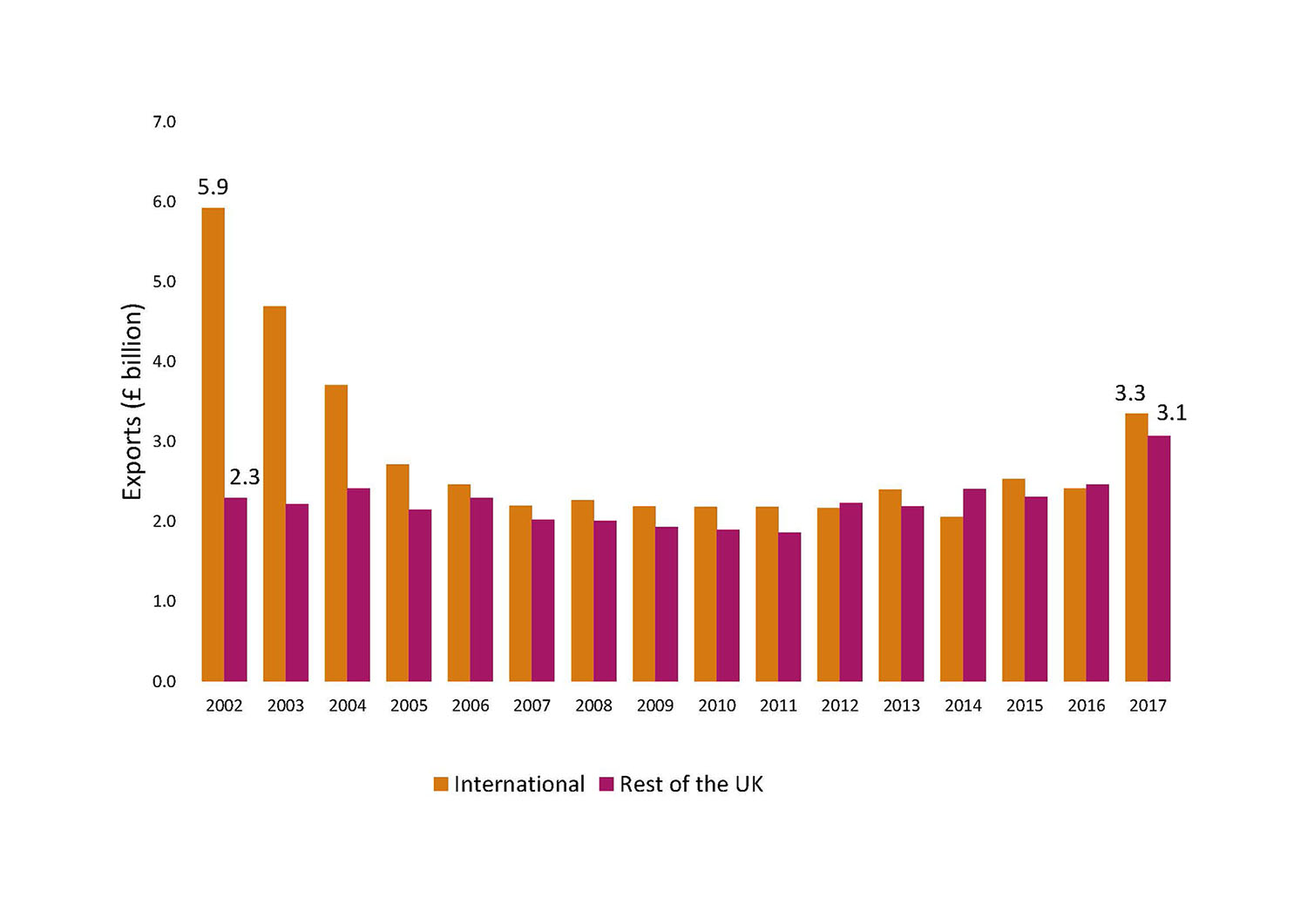

In 2017, the technology, digital and media sector accounted for 10.3 per cent (£3.3bn) of Scotland’s total international exports and 6.3 per cent (£3.1bn) of Scotland’s total exports to the rest of the UK. International exports in this sector declined significantly between 2002 and 2007 following the “dot-com bubble” in the early 2000s and the subsequent decline of Scotland’s electronics manufacturing industry. However, exports have shown some improvement in recent years (Figure 1).

Figure 1: Technology, Digital and Media Exports, International and Rest of UK, 2002-2017

Source: Scotland’s Export Performance Monitor

Export Performance by Sub-sector – International

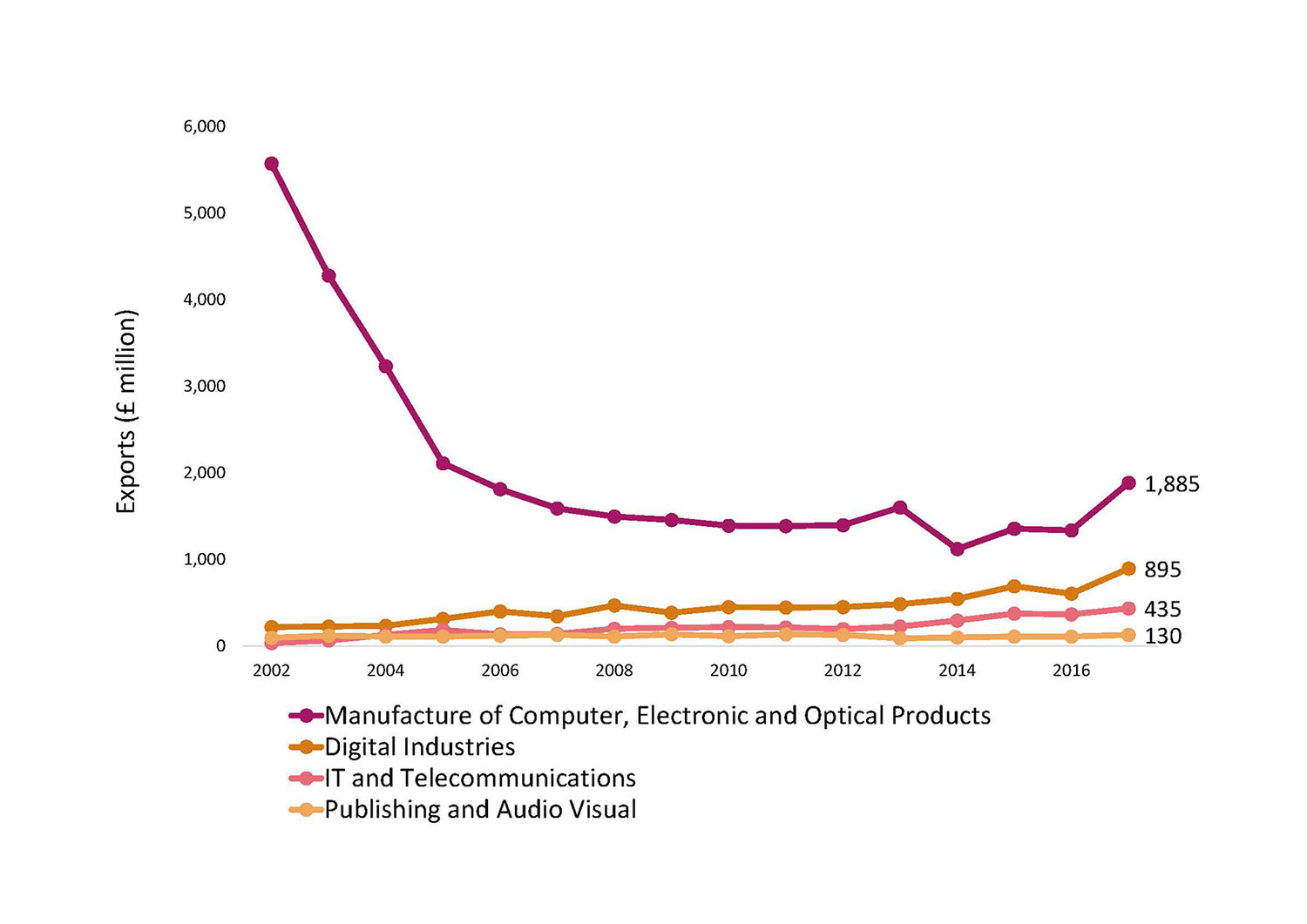

In 2017, the manufacture of computer, electronic and optical products sub-sector accounted for 56 per cent (£1.9bn) of international exports in this sector. The impact of the “dot-com bubble” is particularly apparent in this sub-sector, with international exports declining by around £1bn per year between 2002 and 2005 (Figure 2). The other sub-sectors also make notable contributions to exports in this sector. In particular, digital industries and IT and telecommunications have grown relatively consistently over time.

Figure 2: Technology, Digital and Media, International Exports by Sub-sector, 2002-2017

Source: Scotland’s Export Performance Monitor

Source: Scotland’s Export Performance Monitor

Export Performance by Sub-sector – Rest of the UK

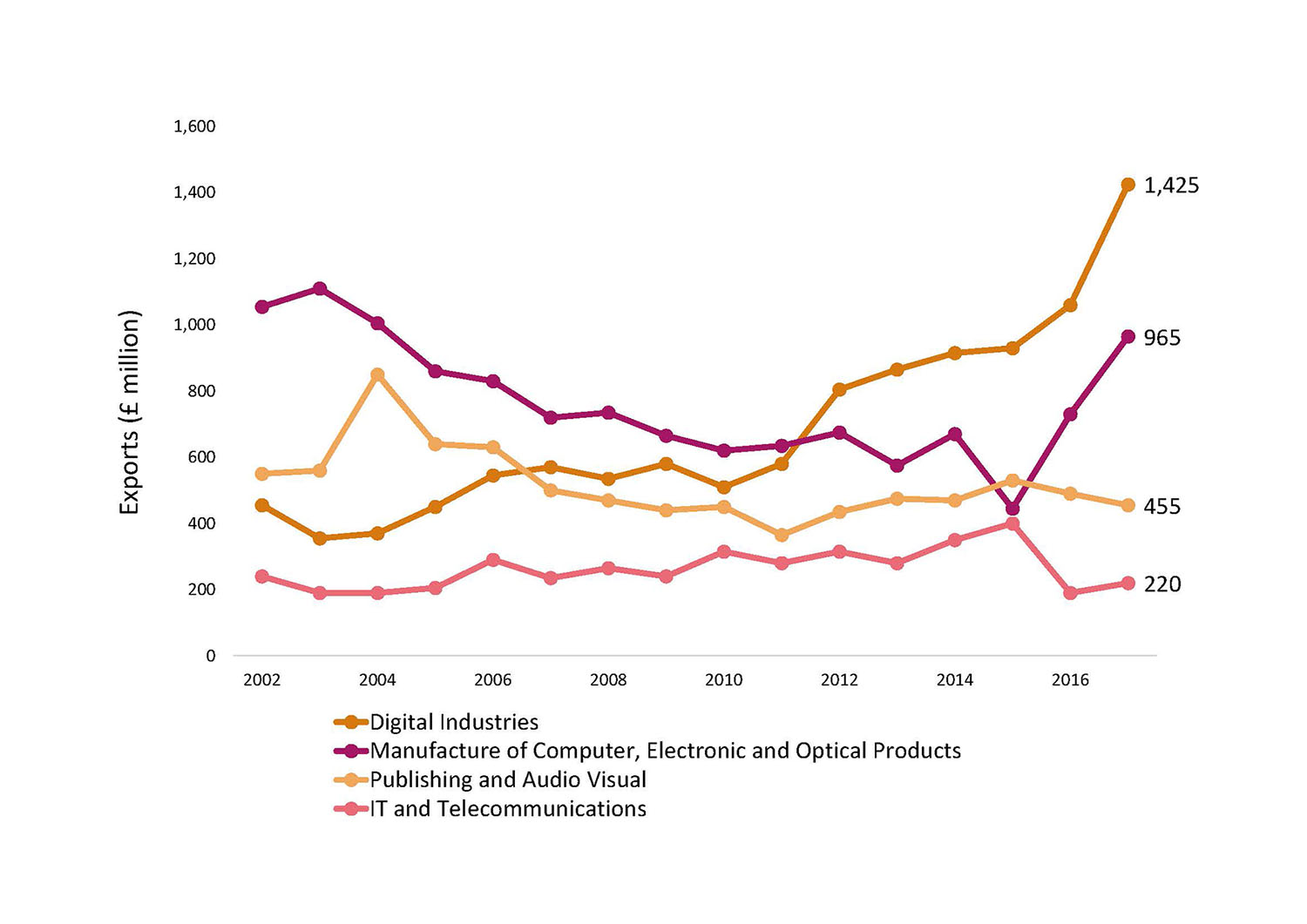

In contrast to international exports, digital industries accounted for the largest share of exports (46 per cent, £1.4bn) to the rest of the UK in this sector in 2017. Exports in this sub-sector have shown strong growth over time, particularly between 2010 and 2017 (Figure 3). Notably, the manufacture of computer, electronic and optical products sub-sector has shown strong growth since 2015, interrupting its consistent decline since 2002.

Figure 3: Technology, Digital and Media, Exports to Rest of the UK by Sub-sector, 2002-2017

Source: Scotland’s Export Performance Monitor

Source: Scotland’s Export Performance Monitor

Our Strengths

- The University of Edinburgh’s School of Informatics ranks among the best in the world with a dynamic start-up scene attracting global venture capital.

- Incremental growth in exports across broad classifications like software development and applications is indicative of Scotland’s comparative advantage in some areas of specialised technology development.

- Scotland’s vibrant creative industries are a key enabler of export performance in this sector, in particular in games, music, film and television, publishing and design.

Our Challenges

- Ensuring recent growth continues, against the historical decline in international exporting between 2002 and 2017 (due largely to the manufacturing of technology hardware industry moving out of Scotland).

- Lack of available local skilled labour (principally STEM graduates and post graduates) which hinders the sector’s growth ambitions.

- For the games sector typical constraints include difficulties accessing finance, skills shortages and discoverability issues (i.e. getting people to notice and make the choice to download or purchase your game).

- The fintech sub sector is a fast-developing opportunity for Scotland. The key challenge for businesses in this area, particularly SMEs, is making decisions about which opportunities to pursue given the range of markets and sectors at play and finding the right corporate partners to work with.

Our Opportunities

- Scotland has a strong focus across several relevant sub sectors where there is global demand; sensor systems and data analytics; “mobility as a service” and fintech; gaming (e.g. Rockstar North, Outplay Entertainment); analogue semiconductors (e.g. Cirrus Logic, ST Microelectronics); cyber security (university spin-outs like ZoneFox).

- Significant opportunities exist for the digital technology company base – or those offering digital or technology based services – in all aspects of data as a commodity”. This impacts all industries and sectors that generate volumes of data, or are dependent upon data and its interpretation and application.

- Fintech Scotland’s strategy, Fintech Bridges & Connections, identifies potential global market opportunities through small specialised groups of companies partnering with global ”fintech hubs”. Working closely with partners, SDI helps SMEs in markets where large financial service companies (predominantly banks/insurance firms) are looking for innovative solutions.

Current Export Markets

In 2017, the top five international export destinations for the technology, digital and media sector as a whole were:

- USA

- Germany

- Ireland

- Sweden

- Netherlands

The top five international export destinations vary between sub-sectors. A more detailed breakdown is provided below (Table 2).

Table 2: Top Five Destinations for Technology, Digital and Media Exports by Sub-sector, 2017 (1)

| Sub Sector |

Countries |

| Manufacture of Computer Electronic and Optical Products |

USA, Germany, Sweden, Italy, France |

| Digital Industries |

USA, Ireland, Qatar, Netherlands, Taiwan |

Source: Scotland’s Export Performance Monitor

Key Growth Markets

Analysis for A Trading Nation, identifies 15 priority markets in which there are significant opportunities to increase Scotland’s exports as well as a further 11 where there are more specific sectoral opportunities. Table 3 below breaks down these opportunity markets for technology, digital and media exports:

Table 3: Potential Opportunity Markets for Scotland’s Technology, Digital and Media Exports Technology, Digital and Media

| Category |

Countries |

| Large and growing demand for imports in this sector |

United States, Germany, China, Japan, Mexico, Singapore, South Korea |

| Scotland currently underperforming similar competitors in this sector |

United States, Germany, France, Netherlands, Switzerland, Norway, Ireland, Japan, Australia, India |

Source: Office of the Chief Economic Adviser calculations

The priority markets identified by the analysis for A Trading Nation broadly align with those markets SDI current focus on. SDI identifies priority market opportunities on either a broad market or sub-sector basis. Some of the markets that SDI has identified as presenting significant country-level opportunities across the Technology sector include: Germany, France, Spain, Switzerland, Nordics, North Americas. Other potential growth markets identified include the Middle East and Asia (in particular China and Singapore/ASEAN).

Actions We Will Take

- Industry-SDI-Scottish Government partnering on market development plans in selected subsectors and markets.

- Working with industry bodies on sector specific export plans.

- Addressing access to high quality graduate and technical talent supply.

- Ensuring a continued pipeline of skilled overseas employees (post-Brexit).

- Championing access to business finance linked to export growth plans.

- Identifying GlobalScots/Trade Envoys who are in a position to provide advice/support/ introductions to benefit businesses in this sector.

Stakeholder Consultation

Technology Scotland

In total, more than 30 organisations have been consulted in the development of this plan. These consultations have helped to shape the plan and have helped us to make links to other relevant work within individual sectors.

While we are not able to reflect all the comments and input we received through these consultations, some pertinent points from key consultees in this sector are captured below.

Key consultees in this sector included Technology Scotland and ScotlandIS.

Technology Scotland represents much of the ‘hardware’ end of digital technologies and were keen that the plan recognises the importance of enabling technologies, in particular photonics and electronics, and the contribution that they make across all Scottish Government growth sectors.

In support of this, Photonics Scotland has launched its Vision 2030 document which sets out action required to treble the size of Scotland’s Photonics Sector by 2030, including seeking out new export opportunities and attracting talent and investment to Scotland.

They also suggested that the next iteration of the plan should consider which sub sectors of the broad technology “family” to focus on, based on refining export data and more detailed market opportunity discussions with SDI, industry partners and others.

ScotlandIS’s annual Scottish Technology Industry Survey 2018 sets out a variety of evidence on the exporting capacity, industry successes, challenges and areas of potential opportunity for their members:

Top trends within the survey results include:

- Continued growth and optimism in domestic and international markets • Rising demand for talent

- Skills requirements – the two most important being software and web development and commercial and business support skills

Main activity of business; software solutions and services (20%) and software products (14%). The 2018 survey introduced several new categories – cyber information security, data science, digital agency, digital media – to better capture the variety of businesses in the sector.

The three key challenges for 2018 were identified as being:

- Staff recruitment and retention (45% of respondents indicated this)

- Sales and new business (34% of respondents indicated this)

- The current political situation (17% of respondents indicated this).

Additional challenges for businesses relate to managing growth and business scaling, followed by staff recruitment and retention.

References:

(1) For some sub-sectors, the values at a destination country level are less robust. Where this is the case they have not been included in this table.