Financial and Business Services

Introduction

The financial and business services sector is one of Scotland’s largest export sectors. The sector incorporates a broad range of sub sectors, which are set out in Table 1 below. It is a major employer, predominately in Edinburgh and Glasgow.

In 2017, the sector accounted for 19.3 per cent of total enterprises in Scotland (34,030 enterprises) and 17.2 per cent of employment (333,460 employees) (Table 1).

Half of the employment in this sector is accounted for by business support activities. All the other sub-sectors also account for a notable proportion of employment in this sector.

Table 1: Financial and Business Services, Number of Enterprises, Employment and Turnover, 2017

| All Private Sector VAT/PAYE Registered Enterprises |

||||||

| Sector/Sub-sector |

Enterprises |

Employment |

Turnover (£ million) |

Enterprises (% of total) |

Employment (% of total) |

Turnover (% of total) |

| Financial and Business Services |

34,030 |

333,460 |

N/A |

100% |

100% |

N/A |

| Financial Support Activities |

1,615 |

24,270 |

N/A |

5% |

7% |

N/A |

| Business Support Activities |

12,290 |

165,720 |

11,698 |

36% |

50% |

N/A |

| Management Consultancy |

15,670 |

45,680 |

4,957 |

46% |

14% |

N/A |

| Financial Service Activities |

580 |

46,480 |

N/A |

2% |

14% |

N/A |

| Legal and Accounting |

3,835 |

39,170 |

3,131 |

11% |

12% |

N/A |

| Insurance and Pensions |

45 |

12,150 |

N/A |

0% |

4% |

N/A |

Source: Inter-departmental Business Register (IDBR). Proportions may not sum to 100% due to rounding.

Export Performance

In 2017, the financial and business services sector accounted for around 10.3 per cent (£3.4bn) of Scotland’s total international exports and 27.1 per cent (£13.2bn) of Scotland’s total exports to the rest of the UK. International exports in this sector have increased reasonably consistently over time, despite a brief dip during the 2007/8 financial crisis. Exports to the rest of the UK have also increased over time, though the impact of the financial crisis is more apparent, with exports yet to return to their pre-crisis peak (Figure 1).

Figure 1:

Scotland’s Financial and Business Services Exports, International and Rest of UK, 2002-2017

Source: Scotland’s Export Performance Monitor

Export Performance by Sub-sector – International

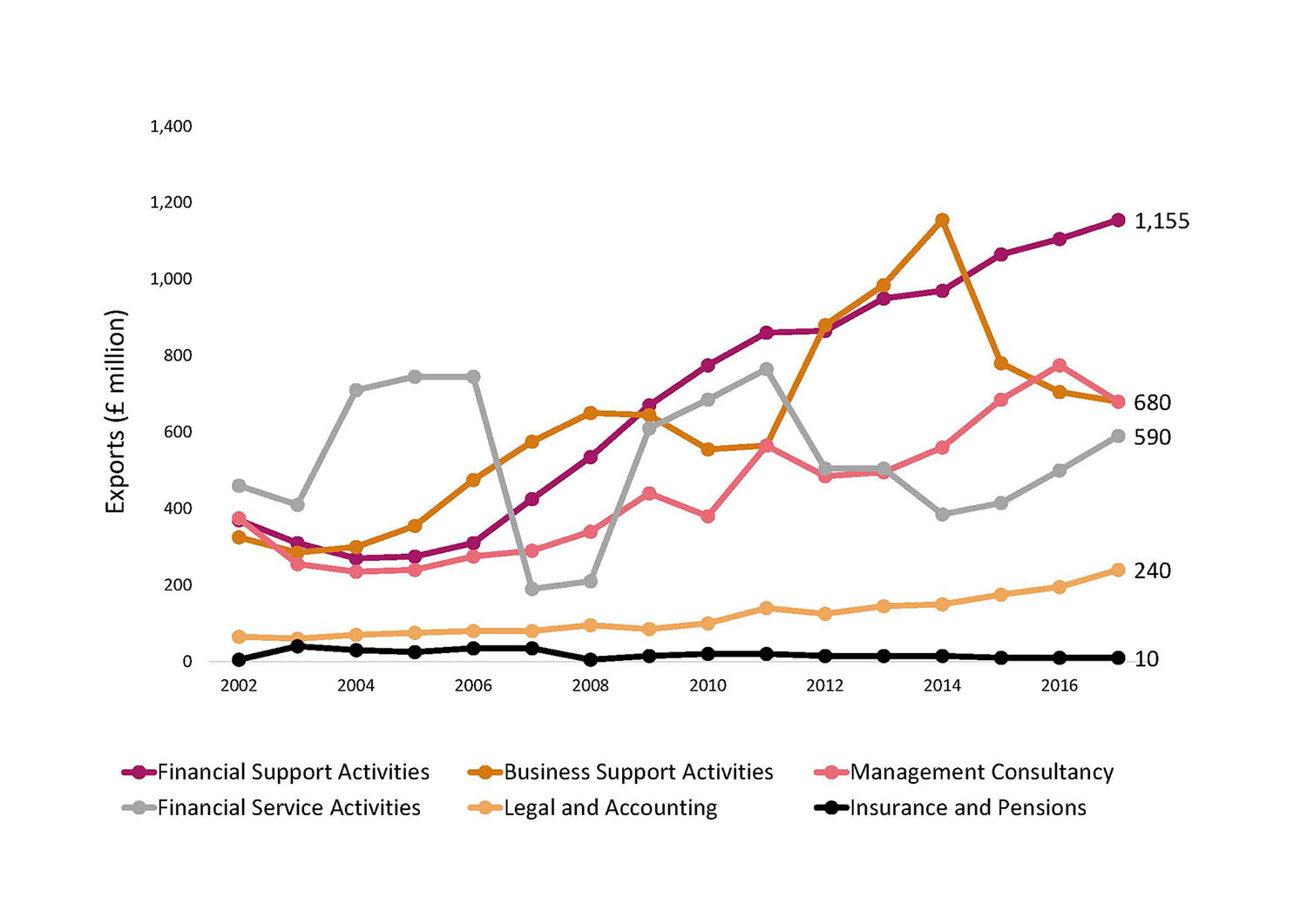

The financial support activities sub-sector accounted for around 34 per cent (£1.2bn) of total international exports in the financial and business services sector in 2017. Exports from this sub-sector have been steadily increasing since 2006. The other sub-sectors also made significant contributions to international exports, though growth has been more volatile over time (Figure 2).

Figure 2: Financial and Business Services International Exports by Sub-sector, 2002-2017

Source: Scotland’s Export Performance Monitor

Source: Scotland’s Export Performance Monitor

Export Performance by Sub-sector – Rest of the UK

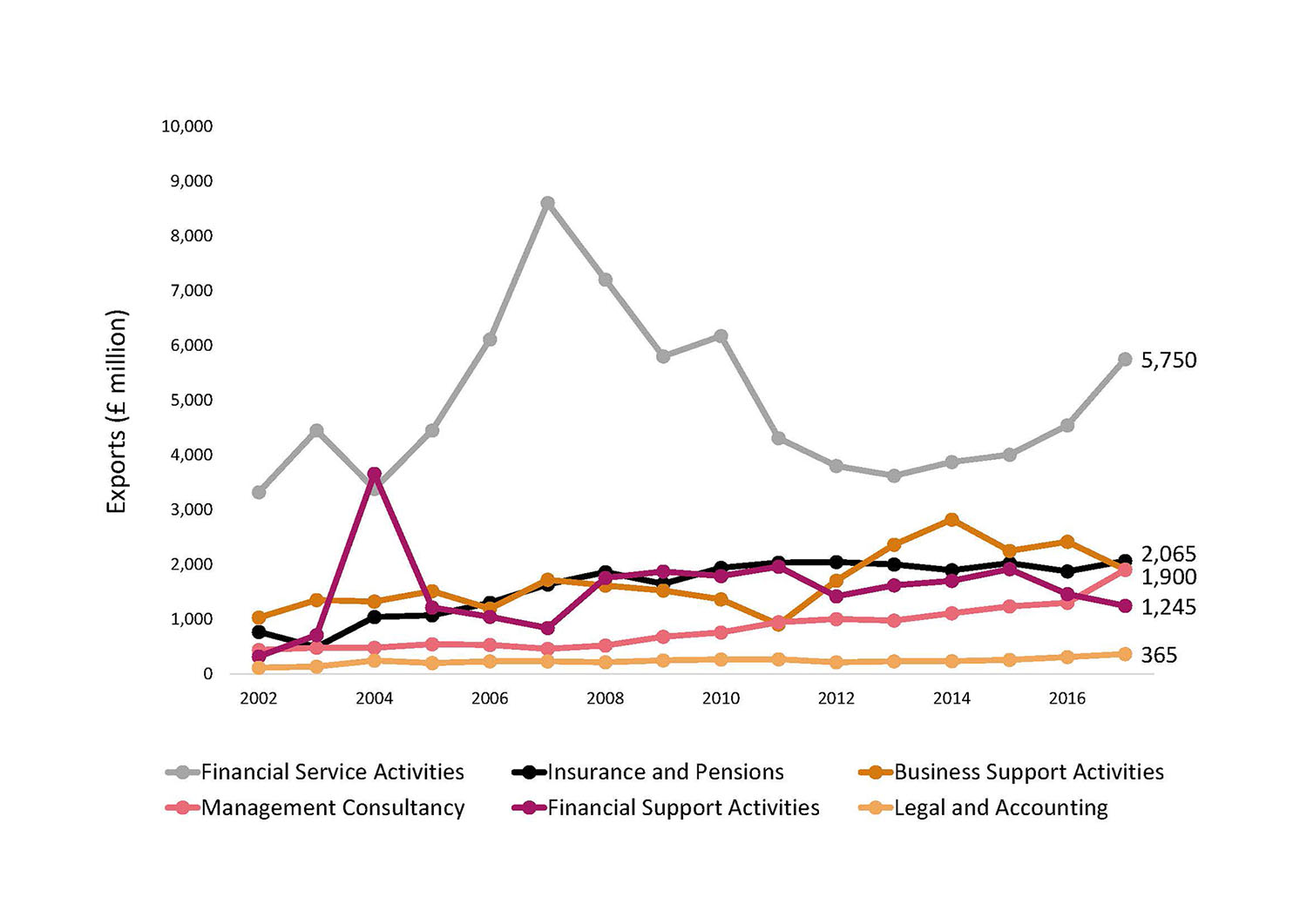

The financial services activities sub-sector accounted for around £5.8 billion (43.5%) of exports to the rest of the UK in 2017. Rest of the UK exports from this sub-sector peaked in 2007 and declined significantly in subsequent years. That said, exports in this sub-sector have improved more recently. The other sub-sectors also made significant contributions to exports to the rest of the UK.

Figure 3: Financial and Business Services Exports to Rest of UK by Sub-sector, 2002-2017

Source: Scotland’s Export Performance Monitor

Source: Scotland’s Export Performance Monitor

Our Strengths

- Strong growth in international exports over time, increasing by 5.0 per cent on average per annum from £1.6bn in 2002 to £3.4bn in 2017. A number of sub-sectors have contributed to this strong performance.

- A cost base that is 30-40% lower than London that makes Scotland an attractive base of operations.

- A strong history of innovation in the financial services sector that continues to the present day.

- Financial services includes banking (monetary intermediation) such as central banking, retail banking, corporate banking, building societies, and investment banks. Scotland has a long and distinguished history in banking and is home to the headquarters of some of the largest banking institutions e.g. RBS, Clydesdale Bank, Tesco Bank, Virgin Money and Bank of Scotland (part of Lloyds Banking Group). Many other UK and international banks have sizeable operations in Scotland, such as HSBC and Barclays.

- Fund management has grown in recent years and is a global market with a diverse range of companies operating within it. According to Scottish Financial Enterprise, funds under management from Scotland now stand at nearly £1 trillion.

Our Challenges

- Slower growth in international exports more recently, increasing at 3.1 per cent on average per annum between 2012 and 2017.

Our Opportunities

- There is increasing international demand for products and services in this sector and Scotland is well placed to maximise investment attraction opportunities by promoting our skilled workforce, low cost base and well-earned reputation for innovation.

Current Export Markets

The top 5 international export destinations for the sector as a whole were:

- USA

- France

- Netherlands

- Canada

- Germany

The top five international export destinations in 2017 for the sub-sectors were (Table 2):

Table 2:

Top Five Destinations for Engineering and Advanced Manufacturing Exports by Sub-sector, 2017 (1

| Financial & Business Services: |

|

| Financial Support Activities |

USA, Canada, Japan, Caribbean Islands, Netherlands |

| Business Support Activities |

USA, Ireland, UAE, Netherlands, Norway |

| Management Consultancy |

USA, Germany, Norway, Australia, France |

| Financial Service Activities |

France, USA, Spain, Germany, Italy |

Source: Scotland’s Export Performance Monitor

Key Growth Markets

Analysis for A Trading Nation, identifies 15 priority markets in which there are significant opportunities to increase Scotland’s exports as well as a further 11 where there are more specific sectoral opportunities. Table 3 below breaks down these opportunity markets for financial and business services exports:

Table 3: Potential Opportunity Markets for Scotland’s Financial and Business Services Exports Financial & Business Services:

| Category |

Countries |

| Large and growing demand for imports in this sector |

United States, Germany, Netherlands, Ireland and Canada |

| Scotland currently underperforming similar competitors in this sector |

Germany, France, Netherlands, Switzerland, Poland, Belgium, Sweden, Italy, Japan |

Source: Office of the Chief Economic Advisor calculations

Actions We Will Take

To date the SDI’s main focus in the sector has been around attracting investment. SDI overseas teams have been proactively pursuing targets from USA, France, Germany, Denmark, Switzerland, Ireland, Singapore, Australia and India. The Scottish Government, through SDI, currently proactively supports Scottish based exporters enter the Singapore market.

In the context of supporting export growth there were no overarching requests for Scottish Government intervention to support this sector from Industry Leadership Groups. However, in the context of supporting overall Scottish export growth we would hope to see the industry support the following call to action;

- For Scottish based banks to engage with DITI to develop export credit insurance products that help reduce the risk of exporting.

- For Scottish based banks to rebuild trade finance teams and, in particular, develop factoring expertise, thereby improving their ability to price risk and offer products such as invoice factoring, that assist exporter cash flow.

Stakeholder Consultation

In total, more than 30 organisations have been consulted in the development of this plan. These consultations have helped to shape the plan and have helped us to make links to other relevant work within individual sectors.

While we are not able to reflect all the comments and input we received through these consultations, some pertinent points from key consultees in this sector are captured below.

Feedback from engagement with industry bodies such as Scottish Financial Enterprise and Fintech Scotland suggested economies such as North America, Europe, China and Asia Pacific with stable, developed economies are the most attractive to enter and usually have established regulators.

These markets are investable with good current and future growth opportunities. Markets have to be attractive in scale, be orderly and stable, have the sophistication to consume the products and services and the potential to offset distribution costs.

Financial services enterprises of scale have ready access to market data and know local regulatory requirements and business practices. Outside of the EU, a requirement of local regulators for financial institutions is to establish a local branch or subsidiary to service their markets, rather than “export” from Scotland. This is different for the consultancy or business support services sub-sector, which allows overseas offices of Scottish firms to resource work from their Scottish base.

References:

(1) For some sub-sectors, the values at a destination country level are less robust. Where this is the case they have not been included in this table.