Food and Drink

Introduction

Food and Drink is one of Scotland’s key growth sectors – domestically and internationally – with a broad range of activity from farming, fishing and aquaculture to processing of raw ingredients into products like smoked salmon and whisky.

The sector as a whole has a unique export model, with a deep and successful partnership forged between the Scottish Government, SDI and the industry, through Scotland Food and Drink. The partnership is strategic in identifying priority markets and its delivery is shaped by a single operating plan. It is one of the most successful and internationally recognised public sector/ industry partnerships and is a model we would like to replicate elsewhere.

Food and drink are best considered as distinct sub-sectors with different drivers and dynamics:

- The drink sector is concentrated in a small number of mainly multinational enterprises

- The food sector is mainly smaller firms, including single employee or family businesses

Table 1: Number of Enterprises, Employment and Turnover, 2016

| All Private Sector VAT/PAYE Registered Enterprises |

||||||

| Sector |

Enterprises |

Employment |

Turnover (£ million) |

Enterprises (% of total) |

Employment (% of total) |

Turnover (% of total) |

| Food and Drink |

17,320 |

112,000 |

13,922 |

100% |

100% |

100% |

| Drink |

210 |

9,000 |

4,255 |

1% |

8% |

31% |

| Food |

17,110 |

103,000 |

9,667 |

99% |

92% |

69% |

Source: Scottish Government Growth Sector Database. Proportions may not sum to 100% due to rounding.

Export Performance

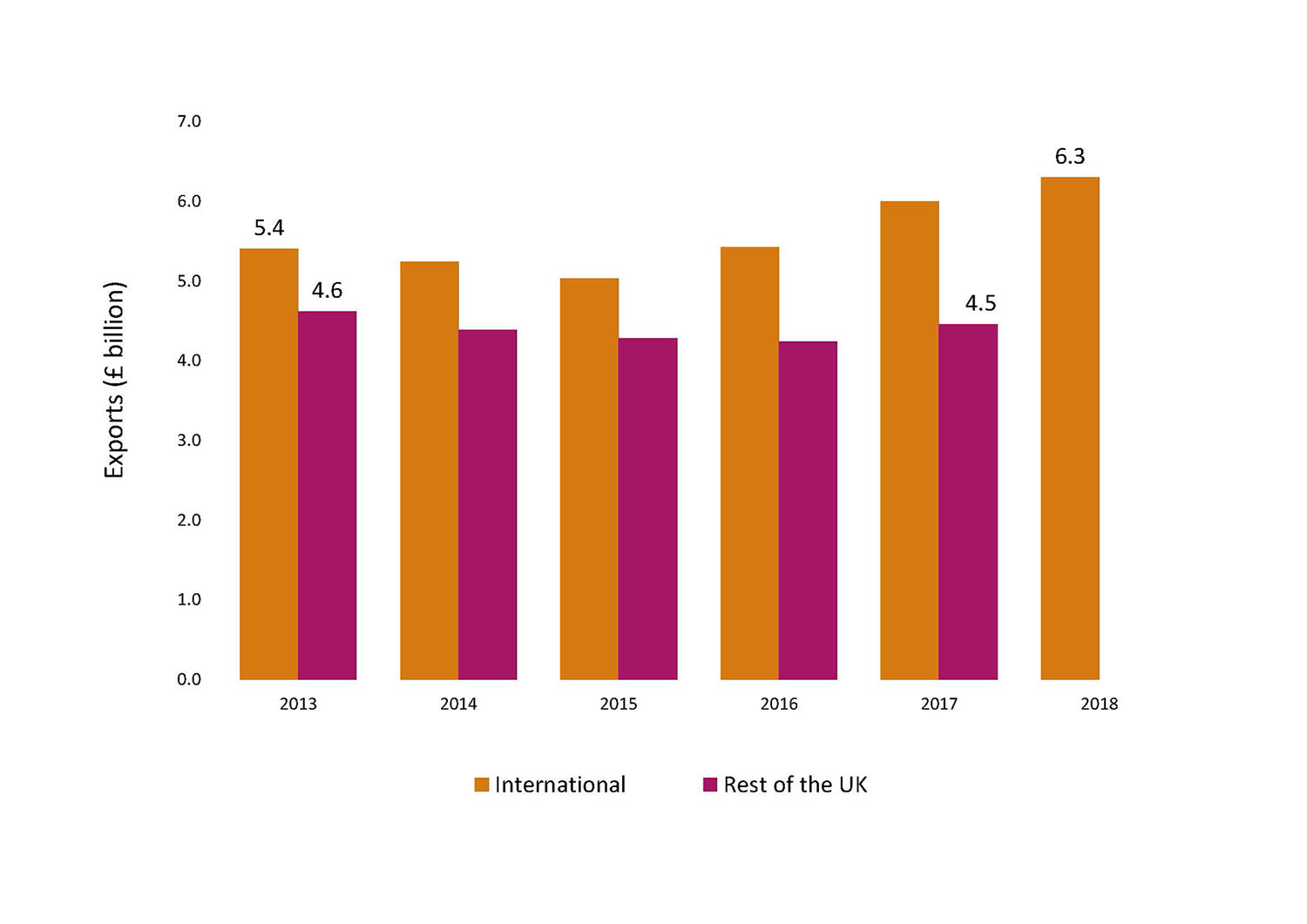

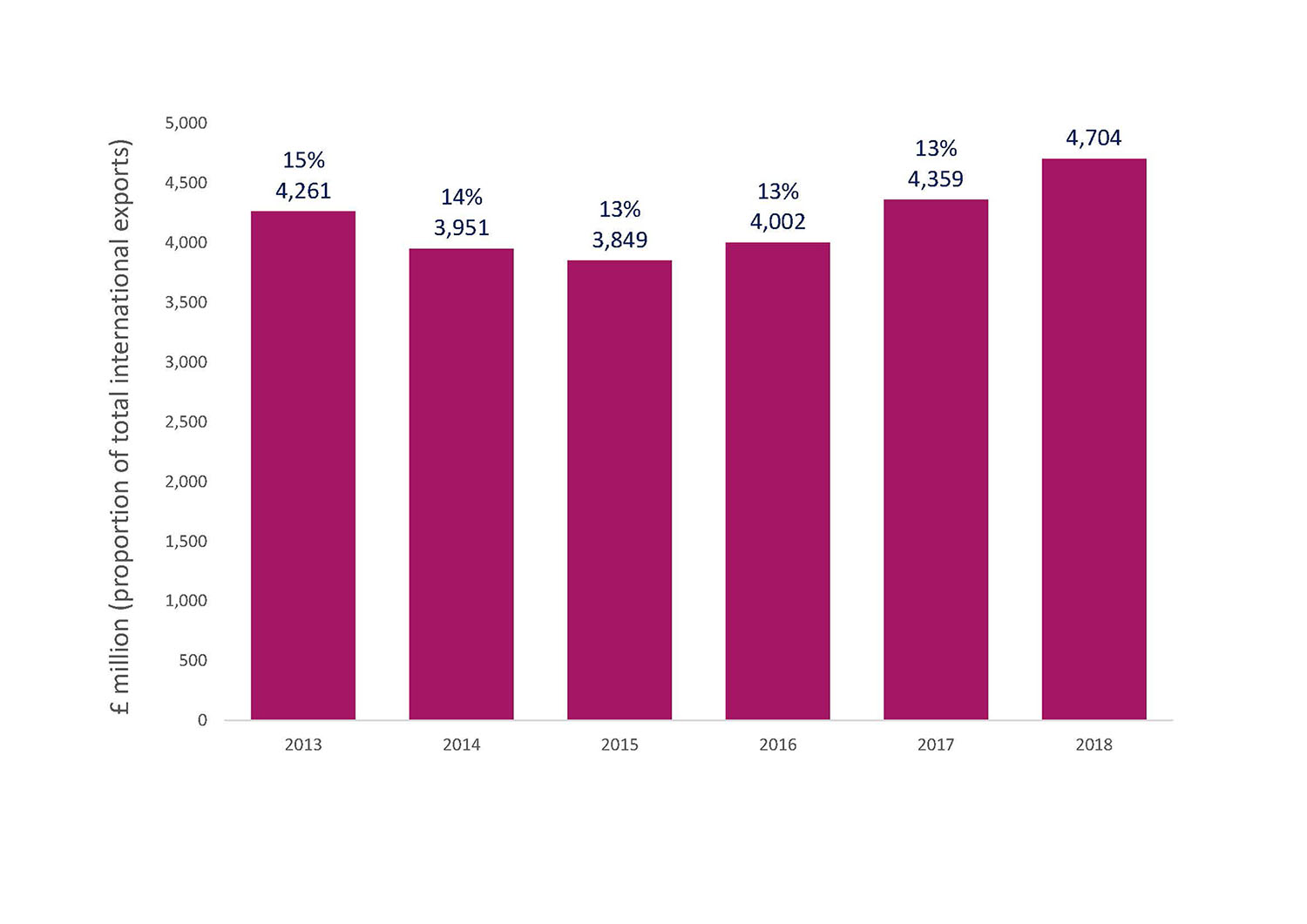

Food and drink continues to be Scotland’s top international export sector, with the latest HMRC statistics showing these exports to be worth £6.3bnin 2018. Scotland’s exports of food and drink to the rest of the UK were estimated to be worth £4.5bn in 2017. Between 2013(1) and 2018, international exports of food and drink increased by 17 per cent (Figure 1).

Figure 1: Scotland’s Food and Drink Exports, International and Rest of UK, 2013-2018

Source: HMRC (International), Scotland’s Export Performance Monitor (RUK)

Note, International exports data available to 2018. However Rest of the UK exports data only available to 2017.

Export Performance by Sub-sector – International

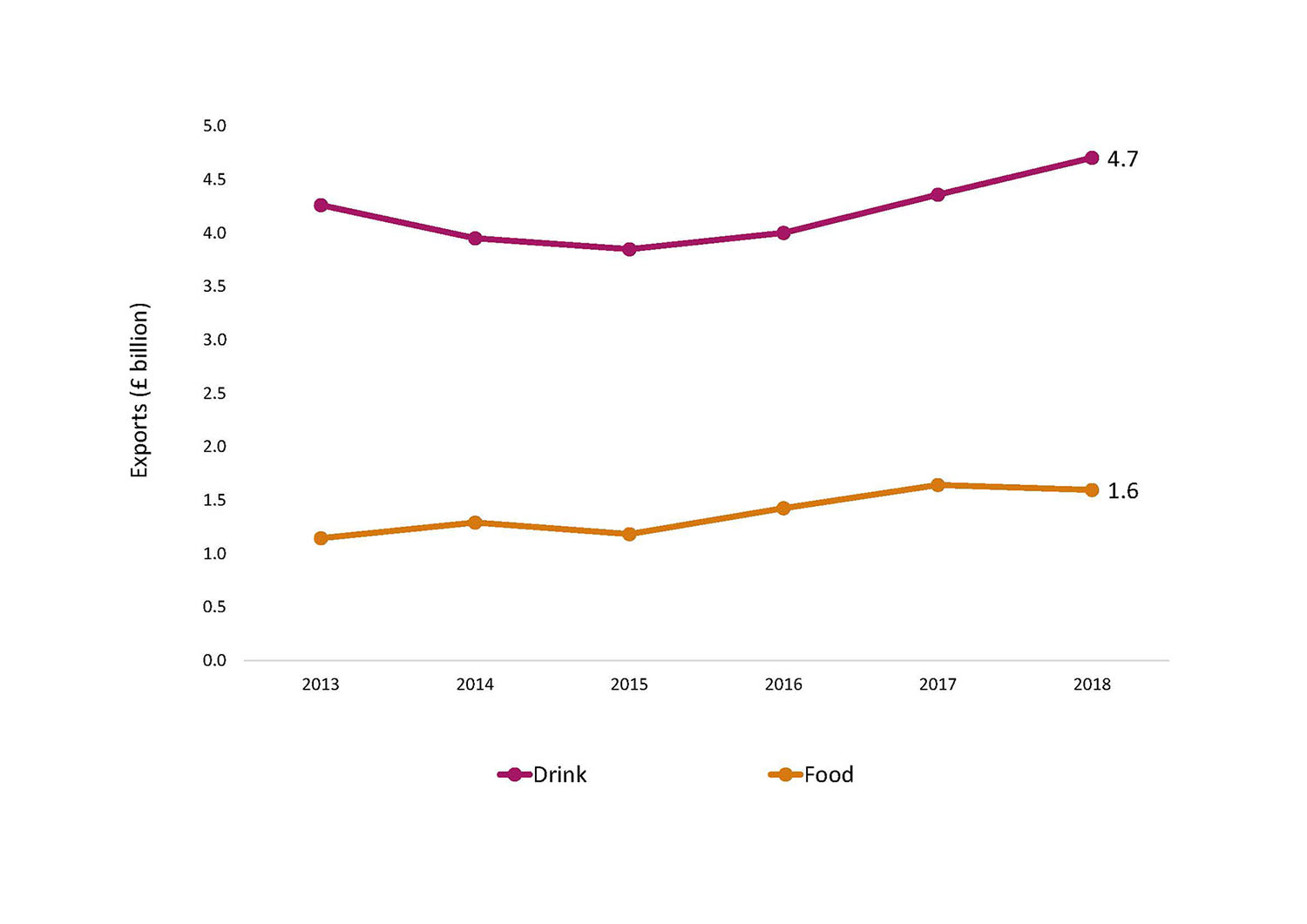

Exports of drink, after a few years of decline, have increased in recent years with overall growth of 10 per cent between 2013 and 2018. International exports of food have generally increased during this period, with overall growth of 40% between 2013 and 2018 (Figure 2).

Figure 2: Food and Drink International Exports by Sub-sector, 2013-2018

Source: HMRC 2018

Export Performance by Sub-sector – Rest of the UK

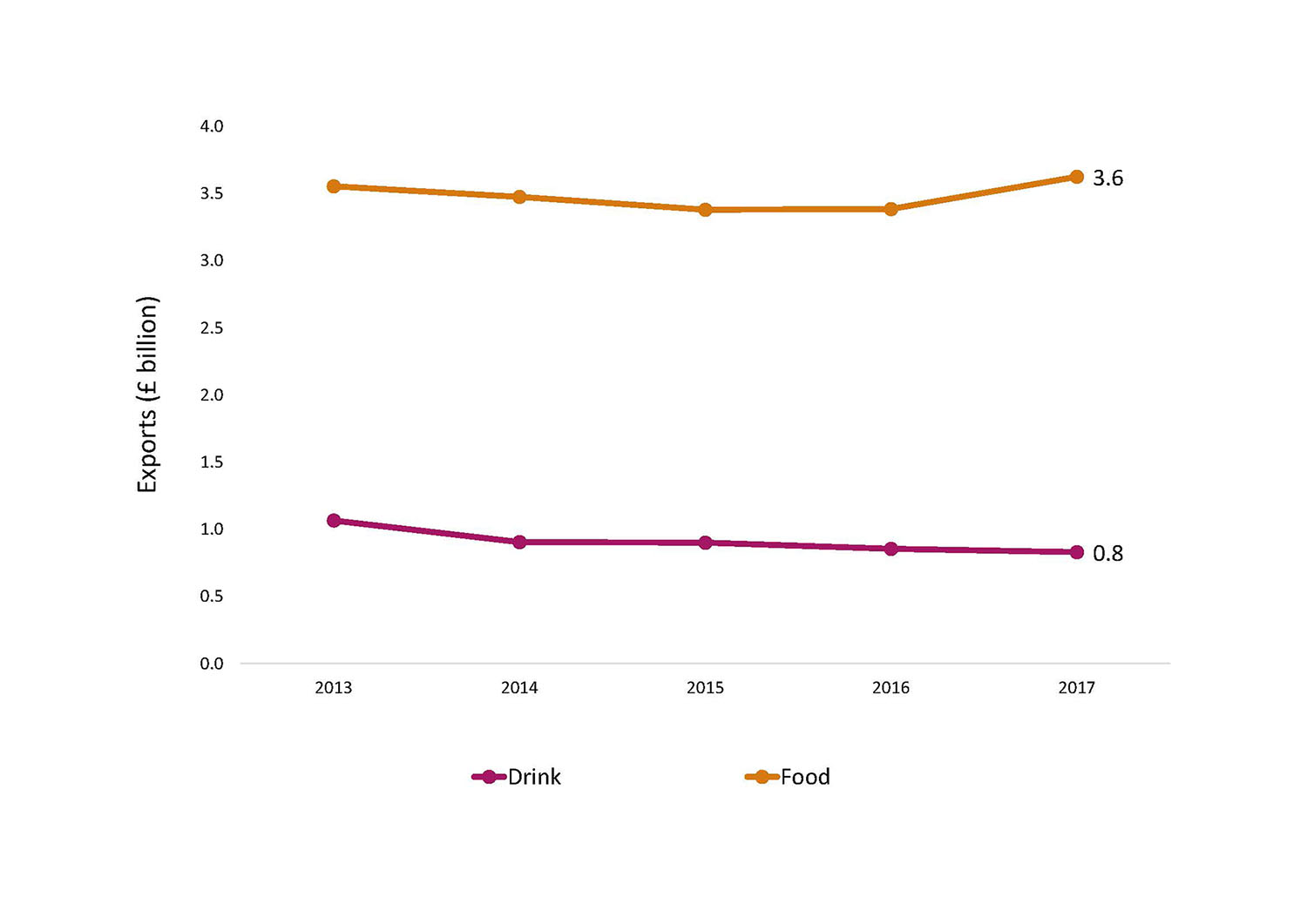

Food and drink exports to the rest of the UK(2) are dominated by exports of food which were worth £3.6bn in 2017. This figure has remained relatively stable since 2013. Drink exports to the rest of the UK, worth £830mn in 2017, have steadily declined since 2013 (Figure 3).

Figure 3: Food and Drink Exports to Rest of the UK by Sub-sector, 2013-2017

Source: Scotland’s Export Performance Monitor

Our Strengths

- Scotland’s food and drink products are in high demand from markets across the world.

- Scotland has an established international reputation for quality, provenance and luxury.

- Food and drink are well-connected and take a collaborative industry-led approach through Scotland Food and Drink

- They produce and offer a diverse range of products with broad international appeal.

Our Challenges

- Tariff barriers are one of the key challenges for the drinks industry as well as the variability of retail and distribution models across different markets.

- Capacity will always be a constraint, in particular with the maturation time associated with whisky production. This is part of the reason for seeing diversification into white spirits in the sector.

- Capacity is also an issue in the food sector, particularly in aquaculture and some of the agriculture sectors.

- Brexit and losing single market access would lead to: loss of protected tariffs; increased administrative bureaucracy and costs burdens from non-tariff barriers; restrictions or removal of freedom of movement to an industry reliant on EU labour; reduction or removal of regulations that maintain the value and reputation of Scottish products.

- Structural challenges (e.g. availability of skilled staff and making careers in agriculture and fisheries more attractive) within the sector are being addressed collaboratively by Scotland Food and Drink and partner organisations.

- Making businesses more productive and profitable and mainstreaming innovation. Growing export performance will contribute to delivering these downstream benefits.

- Predominance of 5-6 large retailers dominating routes to market, with a similar situation emerging in food service, has resulted in an industry characterised by very low margins and profitability.

- Dependence on foreign labour in some sub-sectors.

- Limited number of strong brands and a lack of finance available to small businesses to build new brands or to invest in consumer insight.

Our Opportunities

- Middle class consumer markets in developed and developing countries are expanding with Scottish origin branding being significant in positioning and driving market growth.

- White spirits dominate the global spirits market presenting an opportunity for some of the newer gin producers but leaving scope for growth and diversity in the market share for whisky.

- Significant opportunities remain to consolidate and expand on existing markets by focusing on the food sector for international markets through targeted retail and food service.

- Key markets in Scotland Food and Drink’s export plan aligned to Export Growth Plan analysis identify potential export opportunities of around £1 billion (primarily in fish and seafood).

- Capacity constraints are particularly marked in the aquaculture sub-sector. Salmon farming in our biggest competitor Norway has grown in scale in recent years to dwarf that of Scottish producers. This despite Scottish waters offering some of the best conditions for salmon farming anywhere in the world. Adoption of more modern production processes, developing an enabling regulatory framework and addressing fish health challenges, would allow the industry to rapidly expand production sustainably. Given the growth in international demand, in particular for premium Scottish products, additional export sales of several hundred million pounds could be unlocked from this sub-sector alone.

The Scottish Food Sector

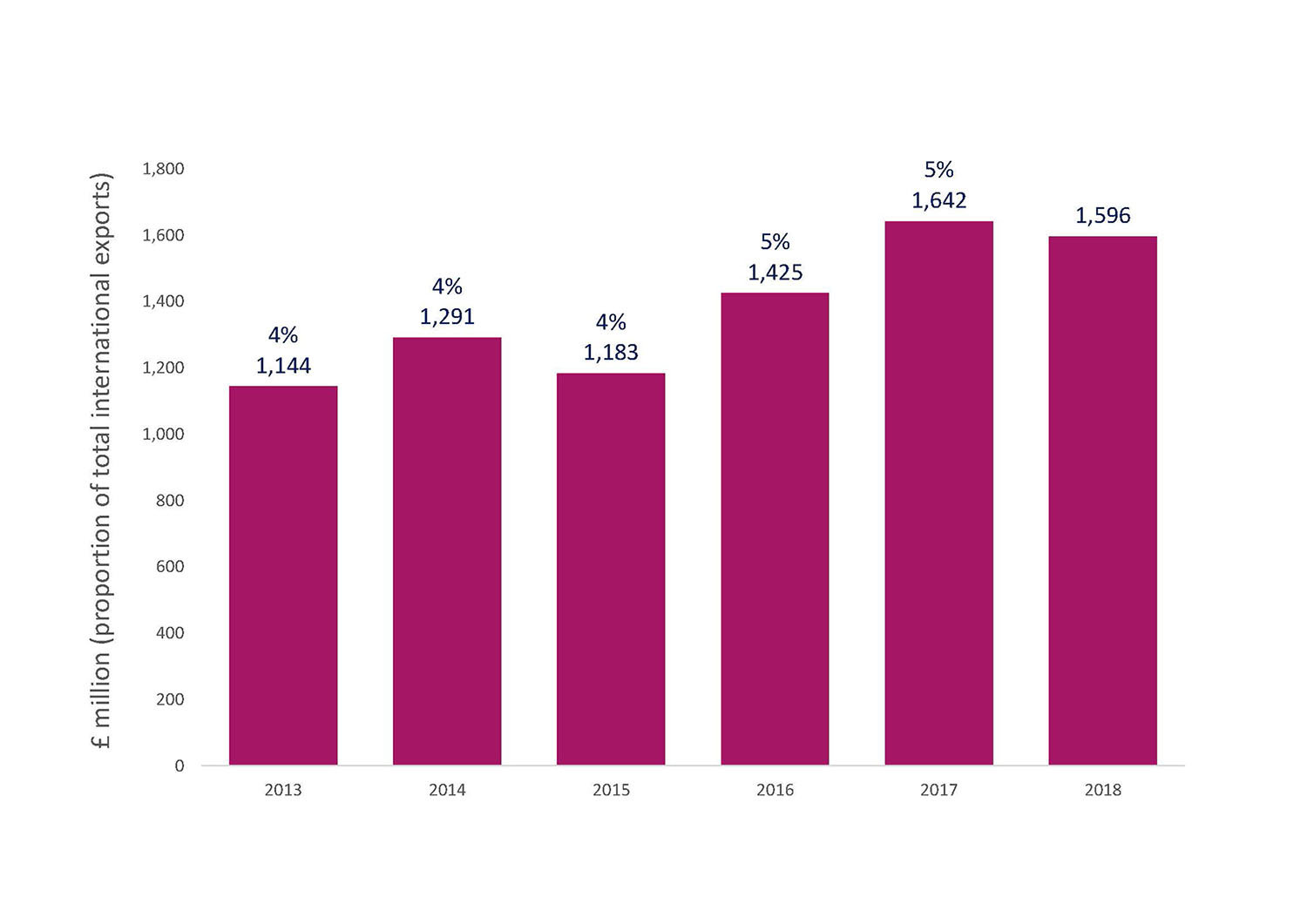

Food accounts for a growing proportion of exports and sales to the rest of the world tend to be focused on the premium end of the market for seafood, red meat and agricultural products (Figure 4).

Figure 4: International Food Exports, 2013-2018

Source: HMRC 2018, Scotland’s Export Performance Monitor (for % of Total)

Source: HMRC 2018, Scotland’s Export Performance Monitor (for % of Total)

Current Export Markets

In 2018, the top five international export destinations for food exports were:

- France – £436 million

- Ireland – £181 million

- USA – £129 million

- Spain – £115 million

- Italy – £77 million

The Scottish Drinks Sector

Scotch Whisky is our leading single product export (mainly produced by a small number of large exporting companies). Gin and craft beer are building on whisky’s success, creating collaborative opportunities and sharing sectoral best practice across the sector.

Figure 5: International Drink Exports, 2013-2017

Source: HMRC 2018, Scotland’s Export Performance Monitor (for % of Total)

Source: HMRC 2018, Scotland’s Export Performance Monitor (for % of Total)

Current Export Markets

In 2017, the top five international export destinations for drink exports were:

- USA – £1,039 million

- France – £442 million

- Singapore – £320 million

- Germany – £174 million

- Spain – £170 million

NB: Singapore serves as an import/export hub for the Asia Pacific region which may artificially inflate its importance as an export destination.

Key Growth Markets

Analysis for A Trading Nation, identifies 15 priority markets in which there are significant opportunities to increase Scotland’s exports as well as a further 11 where there are more specific sectoral opportunities. Table 2 below breaks down these opportunity markets for food and drink exports:

Table 2: Potential Opportunity Markets for Scotland’s Food and Drink Exports

| Category |

Countries |

| Large and growing demand for imports in this sector |

United States, Germany, Netherlands, China, Canada, Spain, Japan |

| Scotland currently underperforming similar competitors in this sector |

Netherlands, Switzerland, Norway, Poland, Belgium, China, Italy, Australia |

Source: Office of the Chief Economic Adviser calculations

Actions We Will Take

As part of the support for the Scotland Food and Drink Export Plan, the Scottish Government, Scottish Enterprise and SDI jointly spent £4.5mn over 2014-2019 to fund a number of in-market specialists in key markets across the world. This funding also included a contribution from industry and is helping Scottish food and drink companies boost their exports in these key markets. We have renewed this support for the next five years where we will:

- Support Scotland Food and Drink’s strategy on premium products for premium markets in retail and food service through an enhanced network of in-market specialists.

- Support mentoring and company matching through the SFD Export Collaboration Charter and the FM Export Challenge programme.

- Support industry by making representations in Scotland’s interests in respect of future trade agreements.

Stakeholder Consultation

In total, more than 30 organisations have been consulted in the development of this plan. These consultations have helped to shape the plan and have helped us to make links to other relevant work within individual sectors.

While we are not able to reflect all the comments and input we received through these consultations, some pertinent points from key consultees in this sector are captured below. Key consultees included the Scotch Whisky Association and Scotland Food and Drink.

The whisky industry is committed to sharing its expertise for the benefit of the wider food and drink sector. The Export Collaboration Charter will see the Scotch Whisky Association and Scotland Food and Drink work in partnership with Scottish Development International to:

- Promote collaboration through the regular exchange of information on export markets and opportunities.

- Share experience on different markets, co-operate on advice and mentoring.

- Facilitate working sessions with export specialists to encourage best practice.

- Create a company match-making service that encourages internationalisation.

- Arrange seminars on market access and protecting intellectual property in export markets.

- Discuss trade policy mechanisms and opportunities to tackle trade barriers.

- Advertise potential export and commercial opportunities to members.

- Partner on a regular basis to support the work of the Scotland Food and Drink network.

- Co-operate, where possible, so that Scottish products are regularly showcased at whisky events in export markets.

- Work together to support a number of Scotland Food and Drink and SDI events in priority markets.

Scotland’s food and drink products are in high demand from premium markets across the world. The Scotland Food and Drink Export Plan is designed to help Scottish suppliers access those market opportunities, overcoming core barriers around lack of information and contacts, and distance from market. The plan brings together the collective resources of SDI, Scotland Food and Drink and key trade associations to help suppliers overcome these barriers and address wider export capability issues. It is based on having a team of in-market specialists in each of the priority markets to open doors for Scottish suppliers, providing market insights and connecting them with new customers and opportunities.

Some common barriers to export have been identified, including:

- Limited operational expertise able to deal with logistical and technical/labelling aspects of exporting. There is a real need to create an “Export Support Hub” to provide practical support in Scotland to develop routes to market and provide regulatory advice.

- There are inconsistencies in the issuing of export licences by local authorities. The inconsistencies relate to varying costs from different councils, interpretation of the rules and timing. The issues in this area were serious enough for at least one company to have stopped exporting live shellfish to the Far East entirely.

- Lack of chilled freight storage facilities at Scottish airports and 24 hour Environmental Health Officer inspection services.

- Lack of overseas flights direct from Scotland that can carry freight (freight carried on passenger aircraft and, as these are generally narrow-bodied, this limits both the volume and the type of packaging that can be used).

- Reliance on Channel Tunnel and sea crossings with tight logistic timings for perishable product (mainly seafood).

- Concerns over the declining number of commercial vets to approve product exports

In addition, there are some sector-specific challenges. In sectors such as seafood, salmon and red meat, there is a limited supply of product, therefore companies need to make very careful market choices. Having direct guidance from the in-market specialists on market opportunities and using the team to make direct connections with potential customers is helping with market selection and entry.

References:

(1) Note, international export data for food is based on HMRC Regional Trade Statistics. Due to a change in their methodology, data is only available from 2013.

(2) Data on food and drink exports to the rest of the UK is sourced from Scotland’s Export Performance Monitor. For consistency with the international exports data, the starting year of 2013 is used.