Energy

Introduction

The energy sector in Scotland is of huge economic importance. This is recognised in the 2018 Programme for Government which sets out ‘the transition to a low carbon economy’ as a key government priority.

The 2017 Energy Strategy and the 2018 Climate Change plan outline a “2050 vision” for a flourishing, competitive local and national energy sector, whilst setting specific targets for the Scottish energy system to meet by 2030:

- the equivalent of 50 per cent of the energy for Scotland’s heat, transport and electricity consumption to be supplied from renewable sources; and

- an increase by 30 per cent in the productivity of energy use across the Scottish economy.

For the purposes of this analysis, the energy sector is split into two distinct sub sectors, energy support, which is predominately companies providing support to the offshore oil and gas sector, and mining and utilities.Oil and gas exports, as carried out by companies involved in the actual extraction of oil and gas, are excluded from this analysis. Given the diversity across the energy sector, it is also the case that activity within energy will be captured as part of a wider group of sectors within the Scottish economy, for example in engineering and advanced manufacturing.

In 2017, the Energy sector accounted for 0.8 per cent of total registered enterprises in Scotland

(1,435), 3.3 per cent of employment (64,870 employees) and 15.3 per cent of total turnover (£39.9bn) (Table 1).

Table 1: Energy, Number of Enterprises, Employment and Turnover, 2017

| All Private Sector VAT/PAYE Registered Enterprises |

||||||

| Sector/Sub sector |

Enterprises |

Employment |

Turnover (£ million) |

Enterprises (% of total) |

Employment (% of total) |

Turnover (% of total) |

| Energy |

1,435 |

64,870 |

39,921 |

100% |

100% |

100% |

| Energy Support |

130 |

17,860 |

4,479 |

9% |

28% |

11% |

| Mining and Utilities |

1,305 |

47,010 |

35,442 |

91% |

72% |

89% |

Source: Inter-departmental Business Register (IDBR). Proportions may not sum to 100 due to rounding.

As above, activity in the energy sector is likely to be included within a wider group of sector activity. Oil and Gas UK estimate that, including indirect and induced employment, around 110,000 jobs in Scotland were supported by the oil and gas industry at the end of 2018. In addition, figures published by ONS indicate that the Scottish low carbon and renewable energy sector supported over 46,000 jobs in 2017.

Export Performance

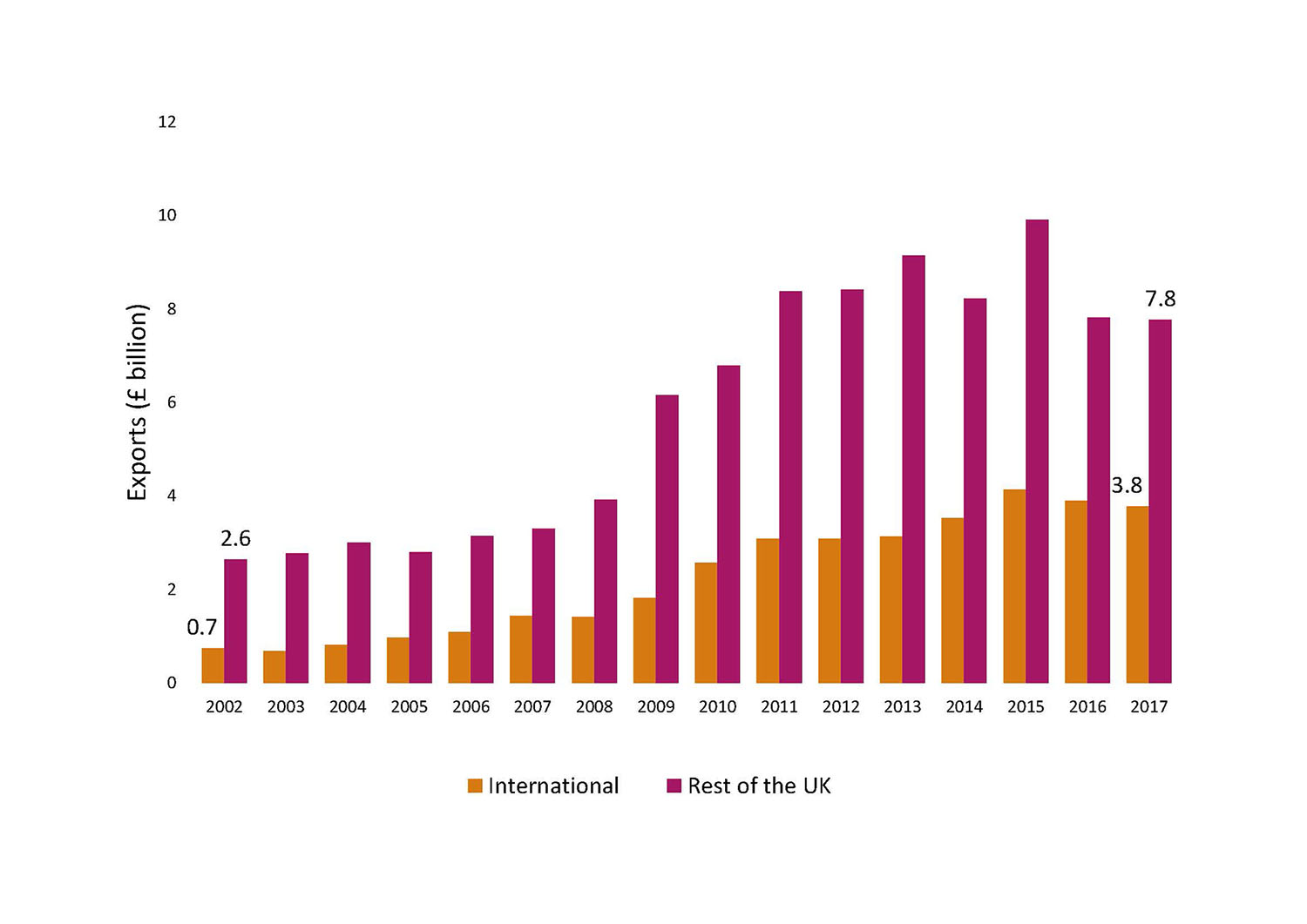

In 2017, the energy sector accounted for 11.7 per cent (£3.8bn) of Scotland’s international exports and 15.9 per cent (£7.8bn) of Scotland’s exports to the rest of the UK. International exports and exports to the rest of the UK have grown significantly since 2002, though growth has weakened in recent years (Figure 1).

Figure 1: Energy Exports, International and Rest of UK, 2002-2017

Source: Scotland’s Export Performance Monitor

Source: Scotland’s Export Performance Monitor

Export Performance by Sub-sector – International

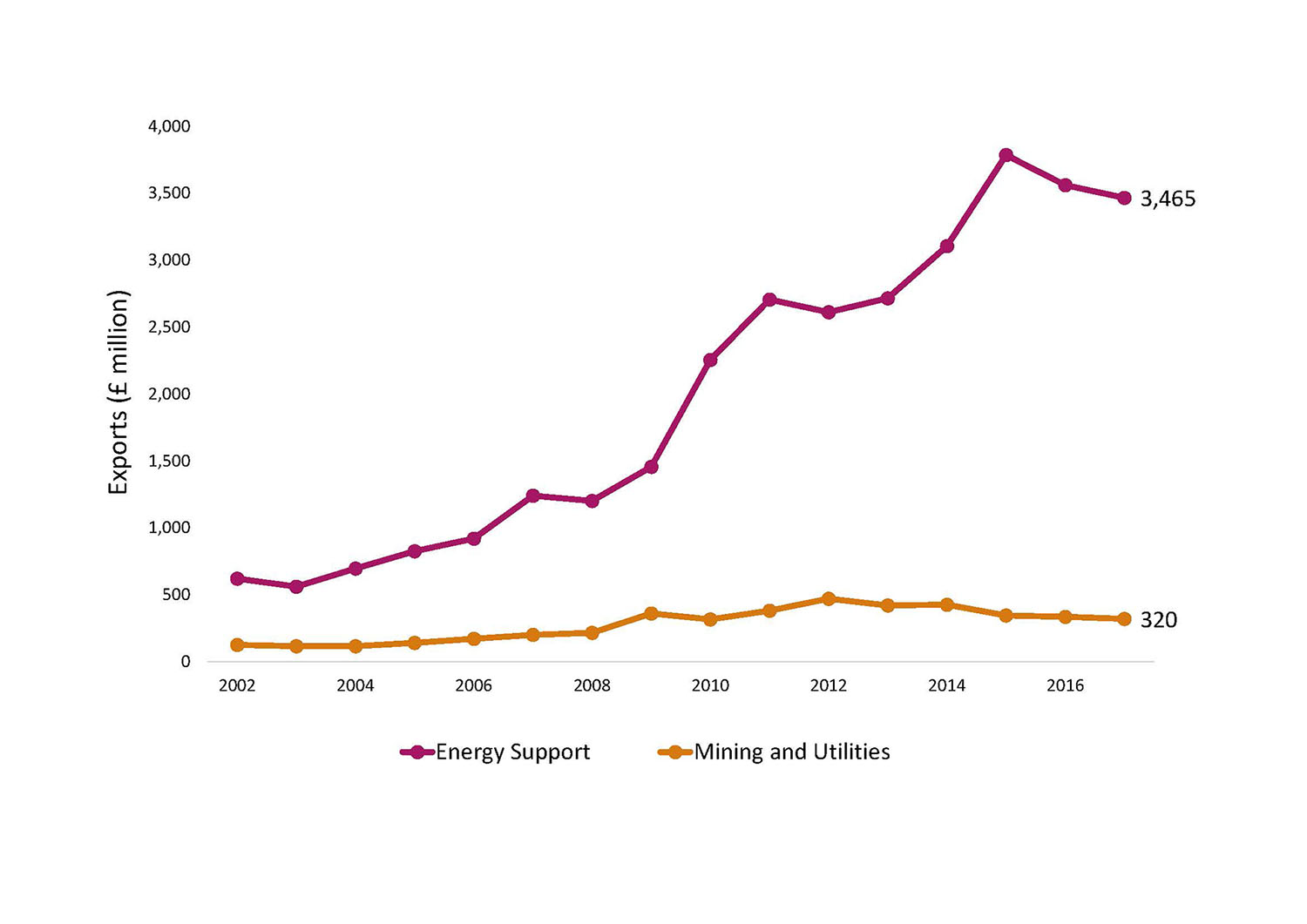

In 2017, the energy support sub-sector accounted for 91.6 per cent (£3.5bn) of international exports from the energy sector. Exports from this sector have increased significantly over time. However, there have been signs of weaker growth in recent years (Figure 2).

Figure 2: Energy International Exports by Sub-sector, 2002-2017

Source: Scotland’s Export Performance Monitor

Export Performance by Sub-sector – Rest of the UK

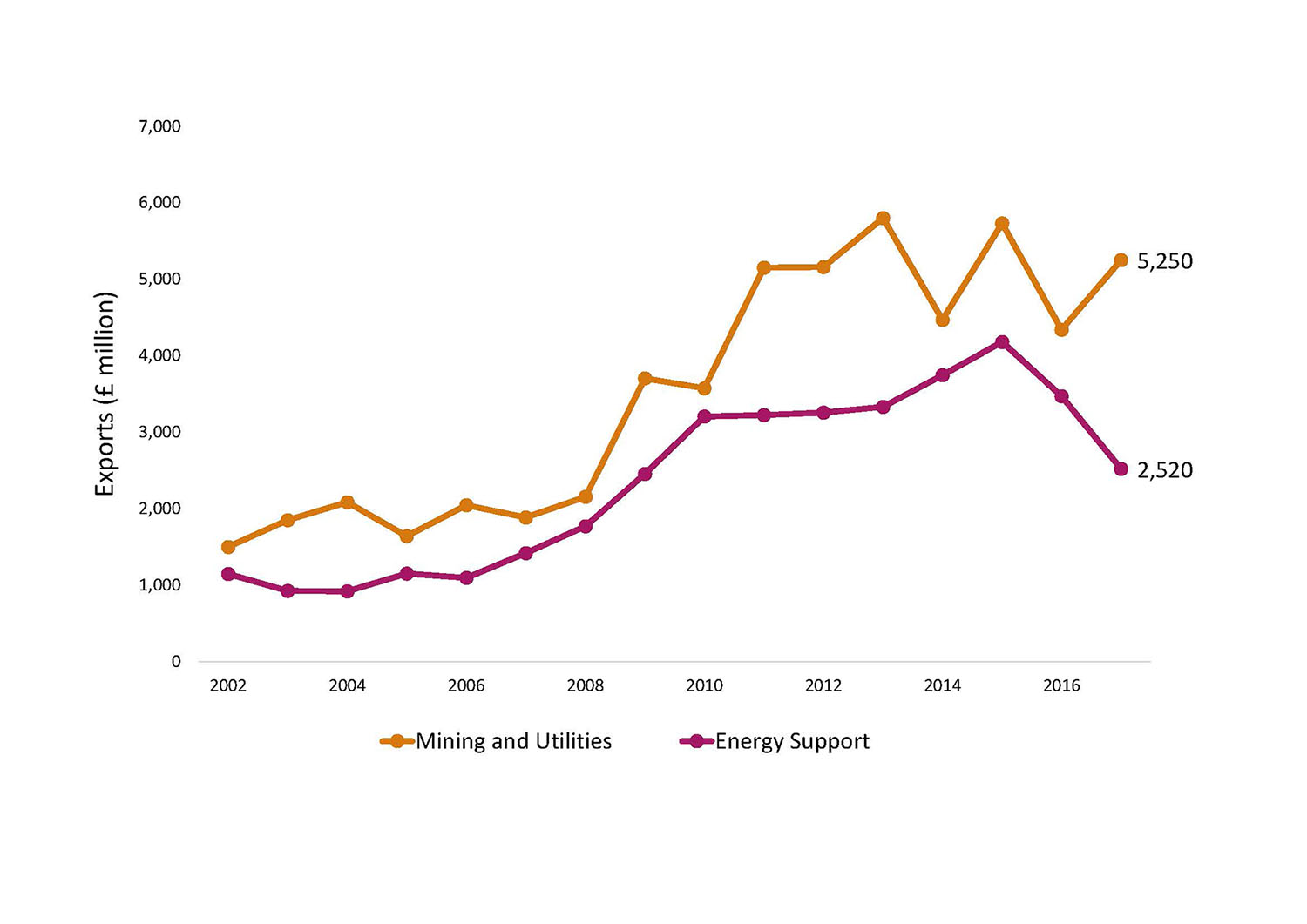

In contrast to international exports, mining and utilities accounted for the largest proportion (67.6 per cent, £5.3bn) of energy exports to the rest of the UK. Exports from this sub-sector have grown significantly over time, despite becoming relatively volatile in recent years (Figure 3). The majority of this sub-sector is from the utilities sector and in particular, relates to Scottish electricity exports to the rest of the UK. Energy support activities were also a large contributor to exports to the rest of the UK, despite a decline in recent years. This is predominately exports of services to the oil and gas sector in the North Sea (which is counted as an export to rest of the UK in the data).

Figure 3: Energy Exports to Rest of the UK by Sub-sector, 2002-2017

Source: Scotland’s Export Performance Monitor

Source: Scotland’s Export Performance Monitor

Our Strengths

- Knowledge and expertise, built on experience of operating in the North Sea, such as vital subsea skills, that can help overcome the engineering and innovation challenges presented by moving to a low carbon future.

- Abundant natural resources, i.e. water, wind, and the renewable sector has effectively harnessed these over the last decade, with over 10 GW of renewable electricity capacity operating in Scotland.

- Long-term vision, through Scotland’s Energy Strategy, providing certainty to businesses investing in renewables and other low carbon technologies.

- Long established oil & gas sector which is a key component of our energy system and economy, contributing to energy security and supporting hundreds of thousands of high-value jobs.

- £90mn commitment over the next decade to support the Oil & Gas Technology Centre as part of the Aberdeen City Region Deal. The Technology Centre and the Oil and Gas Innovation Centre support a sector specific research and innovation ecosystem.

- Global leader in subsea engineering and world-renowned hub with potential for strong growth in international markets.

- Global leader in nuclear decommissioning, in particular in complex sites. There is worldwide interest in this expertise, most notably from Japan.

- UK and Scottish Governments committed to supporting enhanced nuclear. decommissioning capacity & promoting expertise internationally (e.g. via Nuclear Sector Deal and the Higher Activity Waste Policy & Energy skills action plan).

Our Challenges

- Ensuring that the Scottish supply chain captures the economic opportunities from decommissioning, both oil and gas and nuclear. (Oil and gas decommissioning market is forecast to reach £15bn by 2025. Global nuclear decommissioning market, estimated to be worth over £300bn over the next decade).

- Making the right connections and having access to the right information in-market

- Availability of funding for growth (including people resource).

- Inconsistent policy priorities leading to patchy government funding for projects in some markets (more of an issue in renewables where projects may not be commercially viable).

- Protectionism in some markets leading to challenging trading conditions in an already highly competitive tendering process.

Our Opportunities

- Global subsea expenditure is forecast to total more than £100bn during the five-year period from 2017-2021 and is forecast to grow to £140bn by 2035.

- Analysis by the International Finance Corporation indicates that the Paris Agreement will help open up $23tn worth of opportunities for climate-smart investments in emerging markets between 2016 and 2030.

- Globally, reactor decommissioning plans will have to be accelerated in line with the plans of countries such as Germany, Switzerland and Belgium that intend to end nuclear generation by 2030.Over 200 nuclear power plants are estimated to close worldwide by 2030. The European commercial reactor decommissioning market is estimated at £53bn (Notably: UK

£12.4bn, France £13.78bn, Russia £8.6bn). The Asian-Pacific region market is estimated at £13bn and North America at £5.2bn

Current Export Markets

In 2017, the top five international markets for the Energy exports overall were: • Brazil

- USA

- Netherlands

- Norway

- Denmark

The top five international export markets vary between the sub-sectors, a more detailed breakdown is provided below (Table 2).

Table 2: Top Five International Destinations for Energy Exports by Sub-sector, 2017 (1)

| Energy Sector |

|

| Energy Support |

Brazil, USA, Netherlands, Norway, Denmark |

Source: Scotland’s Export Performance Monitor

Key Growth Markets

Analysis carried out for the Export Growth Plan identifies 15 priority markets in which there are significant opportunities to increase Scotland’s exports as well as a further 11 where there are more specific sectoral opportunities. Table 3 below breaks down these opportunity markets for energy exports:

Table 3: Potential Opportunity Markets for Scotland’s Energy Exports

Energy:

| Category |

Countries |

| Large and growing demand for imports in this sector |

France, Netherlands, Belgium, Singapore, |

| Scotland currently underperforming similar competitors in this sector |

France, Poland, Sweden, Canada, Australia, India, Singapore, South Korea |

Source: Office of the Chief Economic Adviser calculations

Actions We Will Take

- Support SDI to maximise the energy sector’s economic opportunities on the global low carbon transition market by:

− Helping existing exporters in the sector access new geographical markets to accelerate their export growth.

− Supporting the oil and gas supply chain trend in diversifying internationally to grow their businesses.

− Increase the number of active exporters in the sector in Scotland by stimulating greater ambition to export.

- Work with stakeholders on data challenges by making our data analysis models on the sector available to help to identify the exporting gaps.

- Invest, with SDI and Opportunity North East, in five overseas energy in-market specialist posts. The specialists will take on a proactive trade development roles to identify and highlight new business opportunities for the Scottish energy supply chain through building relationships with customers, government departments, regulators and intermediaries, helping to facilitate improved international links for Scottish oil and gas and energy companies.

- Pursue diplomatic and policy outreach both bilaterally (for example in fulfilling our MoU with New Jersey and California governments) and with international partners such as The Climate Group, in support of trade opportunities as part of a “One Scotland” approach.

- Develop a Scottish nuclear decommissioning capability statement & international mapping & networking exercise.

Stakeholder Consultation

In total, more than 30 organisations have been consulted in the development of this plan. These consultations have helped to shape the plan and have helped us to make links to other relevant work within individual sectors.

While we are not able to reflect all the comments and input we received through these consultations, some pertinent points from key consultees in this sector are captured below.

Key consultees in this sector included Scottish Renewables and the Energy Industries Council. All consultees were supportive of the development of the plan and highlighted the strengths that they see in the sector in Scotland, in particular the skill base, the transferability of experience in the North Sea to other disciplines and the global reputation that Scotland enjoys within the sector. All stakeholders pointed to the global nature of the energy challenge with every country in the world seeking to make the transition to being a low carbon economy and most making commitments to decommission existing nuclear sites. All stakeholders agreed that Scotland is well positioned to respond to these opportunities and highlighted the importance of government-to-government relationships in supporting this.

All stakeholders identified the challenges and limitations of data with the rigid nature of SIC codes not providing the most helpful guide to understand the breadth of activities and subsectors in which a single business may operate.

References:

(1) For some sub-sectors, the values at a destination country level are less robust. Where this is the case they have not been included in this table.