US Export Plan

The USA Export Plan has been developed to provide targeted, state-level insights that highlights where Scotland’s export strengths most effectively align with specific United States (US) market demands. This is delivered through robust evidence-backed deliverables including sector summaries.

Sector report summaries

Introduction

To build a robust understanding of each sector and its opportunities within the US market, we undertook extensive research, detailed data analysis and wide‑ranging stakeholder consultation. This comprehensive evidence base has enabled us to identify Scotland’s specific sub‑sector strengths and determine how these align with the most promising opportunities across individual US states.

This chapter provides one‑page summaries for each sector, distilling the core findings from our analysis. More detailed sector‑specific reports are also available on request.

Priority states selection process

For each sector, we have identified the top five priority states that present the strongest opportunities for Scottish exporters. These priority states are determined using the core Matrix model, which draws on 106 indicators spanning market potential and competitive dynamics. The results of the model have been further validated through extensive research-based analysis and a series of stakeholder roundtables conducted between January and February 2026.

In addition to the top five priority states, we also highlight a set of other notable opportunity states offering both established and emerging opportunities that have surfaced through research and stakeholder engagement. Although these do not appear in the Matrix top five, they nonetheless offer alternative pathways for Scottish exporters. While the scale of opportunity may be smaller, these markets often present more specialised or differentiated prospects - areas where Scottish companies may hold distinct competitive advantages.

Detailed sector reports

Alongside these summaries, we have provided stand-alone sector reports that provide detailed analysis and commentary for each of the eight priority sectors. Each summary includes an overview of the sector’s economic contribution within Scotland, long-term trends, market competition and the comparative positioning of Scotland’s sectors against international peers. Each report also draws out market trends in the USA; significant issues around regulation, competition, and market entry in that sector; and an identification of at least five US states where opportunities in that sector appear most promising for Scotland.

These detailed sector reports are available on request.

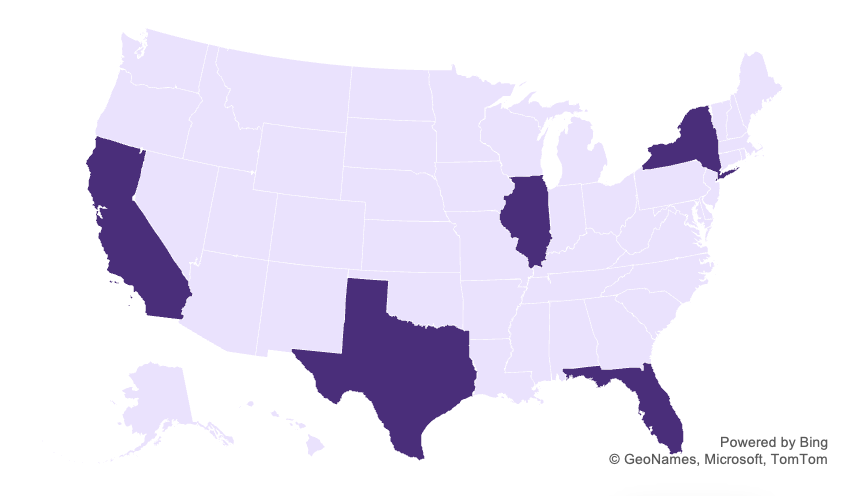

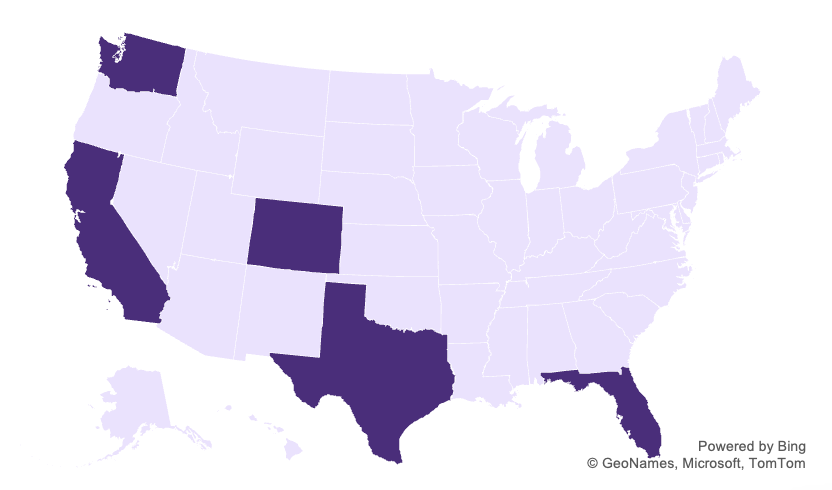

Food and Drink

The Food and Drink sector is one of Scotland’s most valuable and internationally recognised industries. It’s made up of more than 17,000 businesses, directly employs 115,000 people, and contributes £18.9 billion to the Scottish economy annually[10]. The US is a key market for Scottish Food and Drink, with the opportunity strongest for premium products, particularly Scotch whisky and seafood, and a smaller but growing opportunity in health-oriented/functional beverages and dairy products. HMRC goods export data also indicates strong performance in food and drink exports to the United States, reaching £1.2 billion in the year ending June 2025 - a 4.4% increase compared to the same period in 2024.

Opportunities in the US are being shaped by a number of trends including growth in premium and speciality food, diversification of the whisky market, and a rise in health-conscious consumption and sustainability expectations. Given Scotland strengths in premium grocery, the targeting of US states needs to be premium-led rather than volume-led, targeting specialist retail and premium hospitality. However, the US market is complex for this sector, especially for alcohol due to regulation and routes to market differing per state (e.g. open vs control states, plus local jurisdictions). Route to markets for whisky must therefore be cognisant of the open versus control states and local restrictions. Access to the right US importers and distribution networks is also critical, particularly for perishable products such as seafood.

While regulations in this sector are often viewed as complex - particularly around labelling requirements, country-of-origin rules and ongoing uncertainty regarding tariffs - these challenges are not considered overly prohibitive. The more significant barriers tend to be the costs associated with entering the US market and competition from other countries, such as Ireland (Whisky) and Norway (seafood). However, support from SDI In-Market specialists, along with programmes like the US Market Booster, can help exporters navigate these issues effectively and unlock access to this important market.

Top Five Priority States for Scotland in the Sector: California, Florida, New York, Texas, Illinois

Additional opportunity states: Massachusetts, Pennsylvania

Detailed sector report available on request

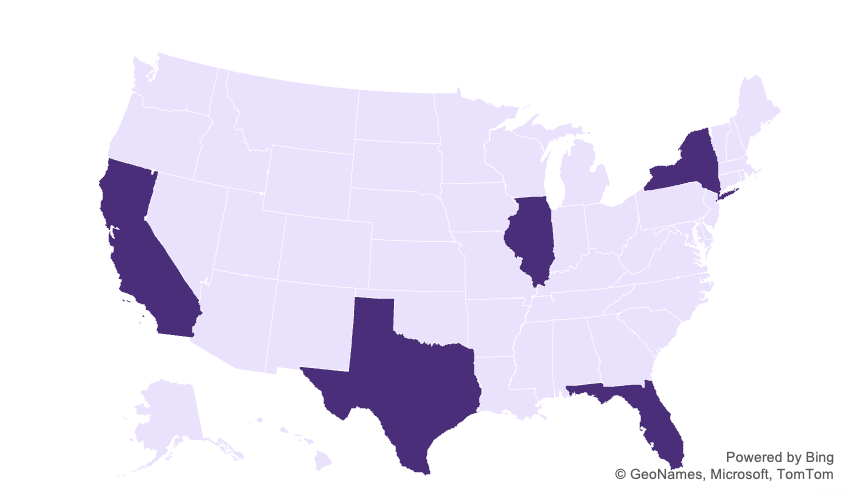

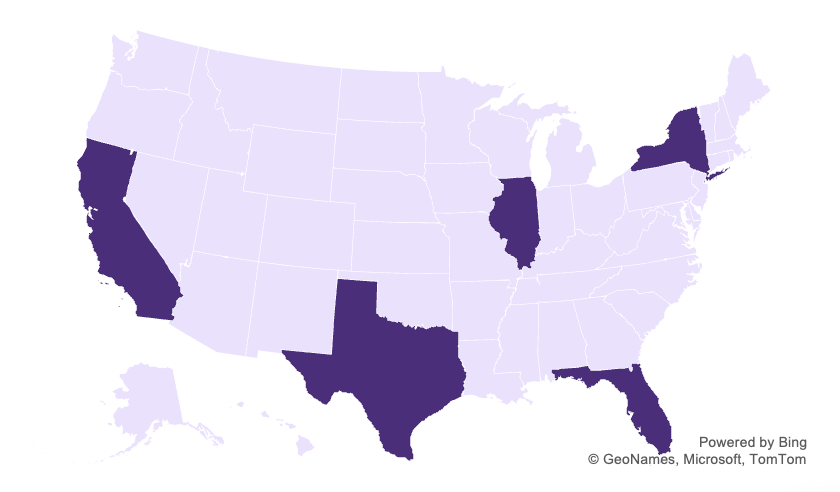

FinTech

Scotland boasts a thriving and internationally competitive FinTech sector, contributing over £14 billion to the national economy. Its significance as a cluster is reinforced by the Kalifa Review, which identifies Scotland as a “large and established cluster” with recognised specialisms in RegTech, Payments, WealthTech, and Open Finance[11]. The FinTech community has expanded to more than 260 companies and now employs over 11,300 people of which 1,700 are employed by FinTechs with international headquarters.

Across the Atlantic, the US FinTech market is one of the most dynamic in the world, with significant investment and innovation occurring across financial services and technology. In recognition of its importance as a key market, in September 2025 Scottish Enterprise and FinTech Scotland launched the Scotland North America Fintech Gateway, a strategic initiative to support export-ready Scottish FinTechs enter the US market, provide market intelligence and attract inward investment.

Furthermore, FinTech Scotland’s analysis shows that 30% of Scottish FinTech firms are actively preparing to export, targeting key markets in North America, Europe and Asia Pacific. Meanwhile, out of the 82 Scotland based FinTech’s which started elsewhere, a third are North American headquartered, proof of the Scottish FinTech cluster’s appeal on the other side of the Atlantic[12].

The priority states identified below are built on a hub strategy – they present major finance and tech centres, plus locations with supportive conditions and strong business networks. Additionally, each State offers strengths in different sub-sectors of FinTech (e.g RegTech, VS Payment, vs Wealthtech) and therefore routes to market will need to be tailored to these strengths, as opposed to a broader ‘FinTech’ single focus. Given the competitive nature of these states, readiness for market entry will be essential. Businesses must have a clear understanding of their product–market fit and ensure they have the resources required to scale rapidly. This is where partnerships with support bodies, such as Scotland–North America FinTech Gateway, can play a critical role.

Top Five Priority States for Scotland in the Sector: Florida, California, New York, Illinois, Texas

Additional opportunity states: Washington (Seattle), North Carolina (Charlotte), Georgia

Detailed sector report available on request

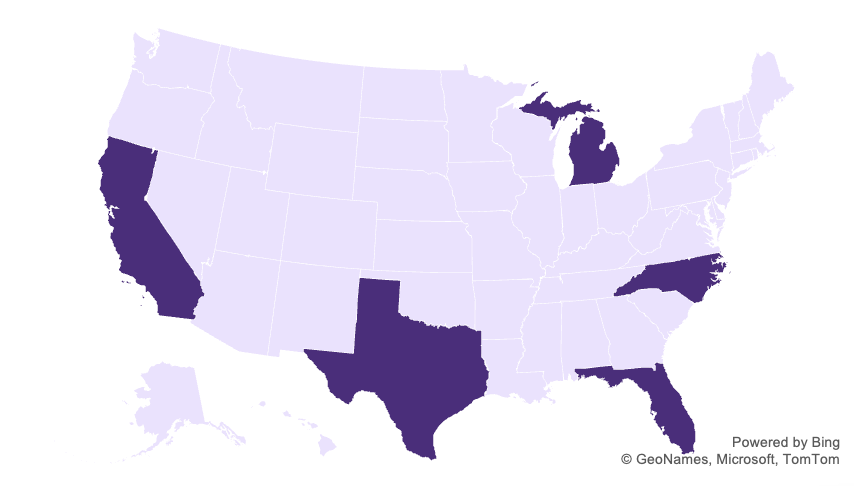

Engineering and Advanced Manufacturing

Engineering and Advanced Manufacturing is a major Scottish strength and a significant part of Scotland’s exports to the US, accounting for £1.2 billion in 2023 and representing 18.4% of total exports[13]. Trends shaping the sector both in Scotland and the US include the growth in Industry 4.0 adoption and Smart Manufacturing (automation, AI and data-driven production). While this sector is not immune to the impact of tariffs on certain materials, there continues to be strong demand from the US, driven by high-growth industries such as aerospace/defence and semiconductors.

Scotland’s opportunities in this sector are enabled by some core sub-sector strengths in robotics and automation, advanced materials, subsea and marine engineering, semiconductors (particularly in packaging) and also quantum and photonics (although this is more tech focused). The opportunities in the US are cross-cutting- Scottish firms are not selling into one ‘engineering market’, rather they are selling into multiple industry supply chains including automotive, aerospace/defence, medical devices, semiconductors and energy.

However, accessing the market in this sector can be challenging due to the range of federal and state‑level regulations that companies must navigate. These include rules on origin determinations, state‑specific professional licensing requirements for engineers, and compliance obligations affecting certain industries. Additional hurdles arise from domestic sourcing and procurement conditions attached to some contracts - such as Build America, Buy America provisions - as well as regulatory controls that apply to specific technologies, including defence‑related or other “dual‑use” items. While there is a mixed federal picture on net zero, some states maintain ambitious positions that sustain demand for low-carbon and efficiency-related manufacturing solutions.

The top priority states identified through our Matrix are California, Texas, North Carolina, Michigan, Florida. These are positioned as strong options because of scale, the presence of relevant industrial clusters (e.g., tech-driven manufacturing, automotive, aerospace), and demand for advanced capabilities. Other states offering more specific niche opportunities include Maryland (Quantum and photonics) Pennsylvania (industrial automation), Massachusetts (medical devices/biotech) and Washington (aerospace).

Top Five Priority States for Scotland in the Sector: California, Texas, Michigan, North Carolina, Florida

Additional opportunity states: Pennsylvania, Massachusetts, Washington, Maryland

Detailed sector report available on request

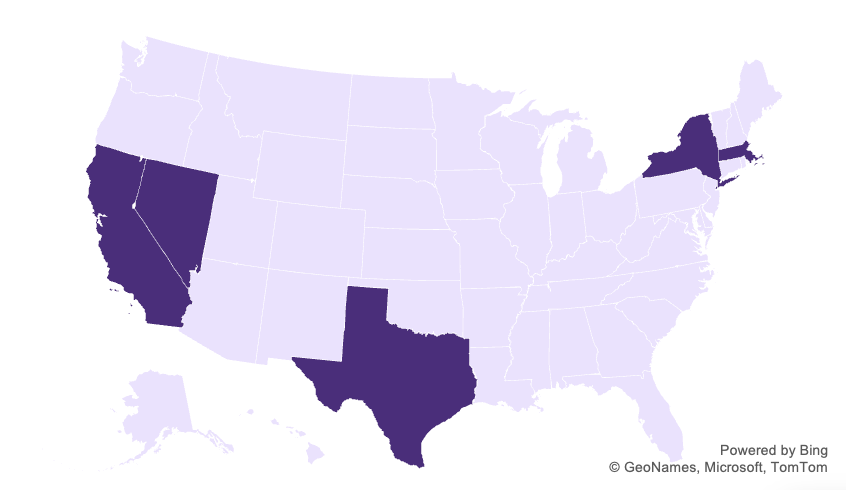

Renewables and Low-carbon Energy

Renewable energy sits at the heart of Scotland’s green economy and international trade ambitions. Scotland is already at the forefront of a range of clean energy innovations, including being home to the world’s first community-owned tidal array and the first floating offshore wind farm. The world’s largest commercial floating wind farm is being developed in Scotland as well[14]. As opportunities in these areas develop overseas, this experience is poised to put Scottish companies in a strong position for exporting relevant goods and services.

However, while the global outlook for renewable energy remains positive, US sentiment toward renewables has cooled under the current administration, with an increased focus on fossil fuels and advanced nuclear over wind and solar. The One Big Beautiful Bill Act (OBBBA), enacted in July 2025, significantly scaled back the Inflation Reduction Act (IRA) by accelerating phase-outs of key tax credits, imposing strict domestic content and foreign entity restrictions, and terminating incentives for EVs and residential solar. These changes have led to cancellations of large-scale clean energy projects.

In the short to medium term, US market dynamics will require many exporters to align with technologies prioritised under current federal policy, such as advanced geothermal, CCS, and grid resilience solutions, while navigating tighter compliance rules, compressed timelines and uncertainty for wind and solar projects. As such, given these current trends, Scottish expertise in some areas, such as floating offshore wind and onshorewind , will be more of a long-term horizon opportunity.

Despite these policy headwinds, demand from US corporations, and particularly from data centres, for clean power remains strong, offering niche opportunities for innovative, cost-competitive solutions that meet domestic sourcing requirements. Furthermore, many US states continue to pursue ambitious clean energy goals. Renewable Portfolio Standards (RPS) and Clean Energy Standards (CES) remain in place across numerous states. Exporters may find strategic opportunities by aligning with states that have the most ambitious clean energy targets, forming partnerships with US utilities, developers, and manufacturers, and leveraging expertise in areas such as offshore wind, CCUS and grid integration.

Top Five Priority States for Scotland in the Sector: California, Texas, New York, Nevada, Massachusetts

Additional opportunity states: Louisiana, Ohio, Illinois

Detailed sector report available on request

Space

Scotland’s space sector is among the fastest‑growing in Europe, contributing around £300 million in GVA and expanding its business base by 65% since 2016. Growth is underpinned by strong academic‑industry collaboration and the development of five planned spaceports.[15] Scotland aims to create 20,000 jobs and capture £4 billion of the global space market by 2030. A Strategy for Space in Scotland, jointly produced by industry, academia and government, highlights a long‑term shift toward “new space,” characterised by smaller, lower‑cost satellites and greater use of accessible space‑derived data.

The sector offers export opportunities across the full value chain—from downstream data services and applications to upstream launch capabilities. It also intersects with several data‑driven industries, including agriculture and climate management. Key subsectors include small‑satellite manufacturing, vertical launch, satellite data analytics, artificial intelligence, and geospatial services.

The US is the largest global player in space data applications, driven by commercial innovation and government investment, with a market valued at $3.2 billion in 2023, projected to reach $11.8 billion by 2032.[16] The Scottish Space Strategy identifies the US as a priority export market, particularly for Earth‑observation and Position, Navigation and Timing (PNT) services. Scottish companies are especially competitive in downstream data, small‑satellite subsystems, and geospatial analytics, while continental Europe and Japan retain stronger advantages in physical components and payloads.

However, accessing large‑scale US programmes can be challenging for smaller Scottish firms, making effective partnerships essential. Companies must also demonstrate that solutions are space‑ready, with Technology Readiness Levels (TRLs) serving as critical evidence for market entry. Key regulatory considerations for operating in the US market include compliance with International Traffic in Arms Regulations (ITAR) and Export Administration Regulations (EAR).

The top priority states identified through our Matrix are California, Texas, Florida, Colorado and Washington. These are positioned as strong options due to the scale of opportunity, the strong history and presence of commercial, military and research-related space activity, from traditional space and national security to ‘new space’ with small sats and geospatial data monitoring. Other states also offering opportunities within the space sector include Washington DC (policy and government decision-makers), Ohio (emerging cluster potential), and Utah (rocket launches and propulsion).

Top Five Priority States for Scotland in the Sector: California, Texas, Florida, Colorado, Washington

Additional opportunity states: Washington DC, Ohio, Utah

Detailed sector report available on request

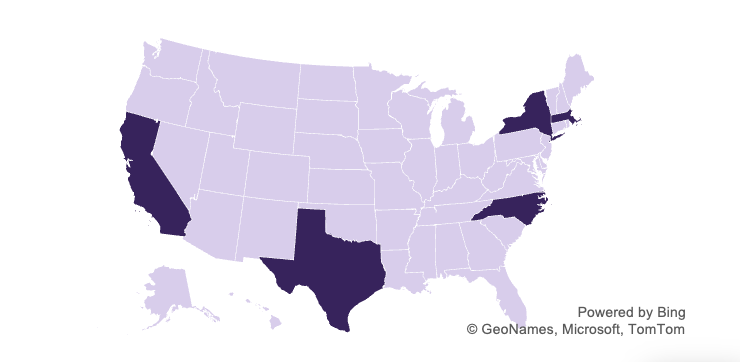

Financial and Business Services

Scotland’s financial & business services sector is a major contributor to the national economy, employing 228,000 people overall, accounting for 8.6% of Scottish employment and £14.5 billion in exports, representing 18.1% of total Scottish exports. Edinburgh and Glasgow are the central hubs, with strong capabilities in banking, asset management, insurance, and professional services, underpinned by a rich heritage and strong academic-industry collaboration.

Scotland’s sector is expected to grow steadily, driven by technology adoption, AI advancements, and productivity gains. A national sector strategy aims to unlock £7bn in additional GVA by 2028[17], while the asset management subsector targets £1 trillion AUM by 2030[18]. Scotland’s strengths in data, AI, machine learning, and sustainable finance position it well for this transformation, though ensuring talent retention remains a challenge.

The US represents Scotland’s largest F&BS export market in 2023, valued at £1.6 billion.[19] Key US hubs include New York (largest global financial centre), San Francisco, Chicago, Los Angeles, Boston, and Washington DC. Major financial institutions such as BlackRock, JP Morgan, Morgan Stanley, State Street already maintain strong operational presences in Scotland. Prominent subsectors that align Scottish strengths with US demand include asset management, banking, insurance and professional services, although cybersecurity, AI, data, blockchain and FinTech are also notable areas.

The US operates a dual federal–state regulatory system where both federal and state authorities have jurisdiction over financial services, and involves bodies such as the SEC, CFPB and Federal Reserve. Key compliance areas include banking regulations, professional qualification requirements, consumer financial protection laws, anti-money laundering, data privacy, cybersecurity and state licensing requirements. Bilateral mechanisms like the UK‑US Financial Regulatory Working Group help streamline cooperation.

The top priority states identified through our Matrix are California, New York, Florida, Illinois, Texas. These are positioned as some of the world’s leading institutions for financial services, as well as strong lending presence, academic institutions and VC environment. Other states also offering opportunities within the sector include Massachusetts (asset management and mutual funds) and Connecticut (insurance).

Top Five Priority States for Scotland in the Sector:California, New York, Florida, Illinois, Texas

Additional opportunity states: Massachusetts, Connecticut

Detailed sector report available on request

HealthTech and Digital Health

Scotland’s HealthTech and Digital Health sector is a major pillar of its life sciences industry and a recognised source of innovation. The digital health segment generates £1.25 billion in turnover from 131 companies, employing 12,872 people[20], while MedTech, part of the wider HealthTech category, reaches £8.9 billion turnover across 137 companies.[21] Scotland’s strengths span medical devices, diagnostics, imaging, wearables, remote monitoring, self‑care solutions, and core digital infrastructure. Innovation is supported by world‑class academic institutions such as the Digital Health & Care Innovation Centre and ongoing government investment in national digital health strategies.

A defining trend in Scotland and globally is the increasing adoption of AI in healthcare, driven by the country’s ability to leverage high‑quality national data assets for predictive analytics and improved service delivery. The US AI medical diagnostics market is also expanding rapidly, valued at $790m in 2025, rising to $4.29bn by 2034[22], with applications spanning radiology, neurology, oncology, and cardiology. Both Scotland and the US are experiencing a structural shift away from hospital‑centric models, with growth in remote patient monitoring (RPM) and home‑based care.

The US represents the world’s largest healthcare market, with digital health projected to reach $295.4 billion by 2028. HealthTech is identified by Scotland as the largest contributor to life science exports, and the US is regarded as the top priority market. Success in the US often requires local infrastructure such as data centres for HIPAA‑compliant hosting, and on‑the‑ground servicing to support providers and partners. The dynamic US venture landscape recorded nearly 4,000 HealthTech deals in 2024, reinforcing the market’s openness to innovation.

Priority subsectors include MedTech and medical devices, AI diagnostics, and telehealth and virtual care. US regulation is complex, divided between federal and state authority. Key federal bodies include the FDA, HHS and OCR. The FDA oversees medical devices and Software as a Medical Device (SaMD), often taking several years. HIPAA governs protected health information and requires stringent technical and administrative safeguards. Additional oversight comes from the FTC (Health Breach Notification Rule) and USPTO (patents and IP protection). State‑level rules add further variation, particularly in telehealth licensing, reimbursement parity, and privacy laws such as Washington’s My Health My Data Act.

The top opportunity states in the sector were identified due to being a centre for global health innovation, having major large-scale hospital systems, world-leading universities and research institutions, deep venture capital and investment networks, as well as being home to major clusters of HealthTech and digital health subsectors.

Top Five Priority States for Scotland in the Sector:California, New York, Texas, North Carolina, Massachusetts

Additional opportunity states: Florida, Minnesota

Detailed sector report available on request

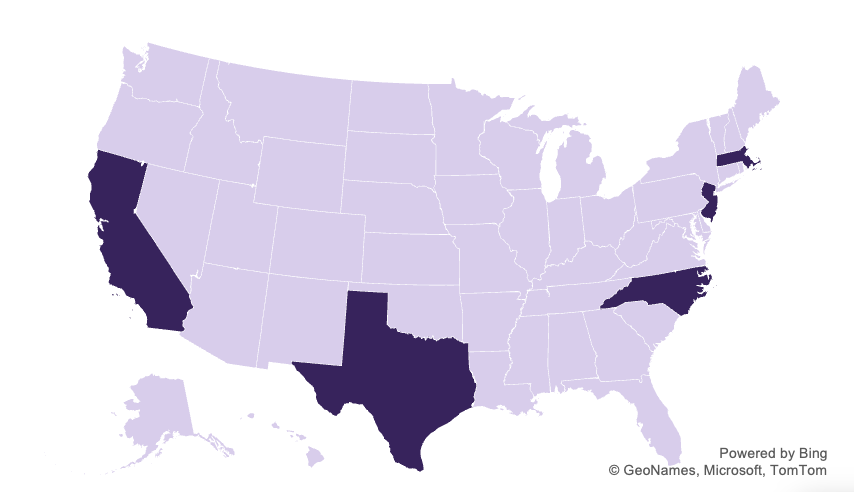

Pharmaceutical Services

Scotland’s pharmaceutical services sector is a major component of its life sciences economy, contributing £1.7 billion GVA and nearly 15,000 jobs in 2023.[23] Pharma services represent 21% of all life sciences exports, with pharmaceuticals adding another 15%, reflecting the sector’s strong international orientation. Scotland’s strengths span early‑stage innovation, clinical research, drug delivery, formulation development, and manufacturing services. Much activity is business‑to‑business, with firms like RoslinCT demonstrating transatlantic success as a leading CDMO specialising in advanced cell and gene therapies.[24]

The US is the world’s largest pharmaceutical market, valued at $639bn in 2024, increasing to nearly $1tn by 2033. 28% of Scotland’s pharmaceutical exports go to the US, much higher than the UK average. This reflects strong opportunities in areas such as biologics manufacturing, sterile fill‑finish, and advanced therapies, especially given the ageing US population and growth in specialty medicines. Global pharma services are shaped by outsourcing growth, with CROs and CDMOs accelerating drug development and reducing costs. In the US, pharmaceutical services outsourcing was valued at $10.3bn in 2023, growing at 5% CAGR to 2030.[25] Strong demand for specialised research, clinical and manufacturing capabilities continues. Another defining trend is AI integration in drug discovery, clinical trials, regulatory submissions, and supply chain management. The US biopharma sector is adopting AI rapidly to improve trial speed, patient stratification, and predictive analytics.

Key subsectors identified include clinical trial activity, drug development, and advanced therapies. US clinical trial activity is robust across major CROs, with growth in decentralised and hybrid trials. Regulations in this sector are primarily on a federal level, covering drug approval pathways, clinical trials, quality systems, serialisation requirements under the Drug Supply Chain Security Act, and HIPAA‑aligned data‑handling rules. The 2025 UK‑US Economic Prosperity Deal provides a time limited commitment by the US to maintain duty-free access for UK-origin pharmaceutical.

The top opportunity states present various strengths across the sector that set them apart, for example California leads activity in genetic engineering, cell therapy and drug discovery, Texas is prominent in oncology and biomedical innovation, Massachusetts is a world-leading biotech and academic centre, New Jersey is home to major pharma HQs and is the largest importer of UK pharmaceuticals, and North Carolina has deep CRO and manufacturing strengths.

Top Five Priority States for Scotland in the Sector:California, Texas, North Carolina, New Jersey, Massachusetts

Additional opportunity states: Connecticut, Washington DC/Maryland/Virginia

Detailed sector report available on request

Contact

Email: William.Gray@gov.scot