State of the economy: October 2022

This report summarises recent developments in the global and Scottish economy and provides an analysis of the performance of, and outlook for, the Scottish economy.

Economic Risks

The risks to the economic outlook and the implications for businesses and consumers, the labour market and more widely are captured in the table below.[1] This sets out a range of indicators through which economic developments and risks are being monitored.[2]

The full scale of the cost crisis and worsening economic outlook are yet to emerge, however economic conditions have progressively weakened over the year so far, and leading indicators are signalling that consumer and business activity have weakened in the third quarter.

The risks are highest around economic output, inflation, exchange rate and UK public finances. Weak consumer sentiment, earnings, and ongoing challenges for businesses around labour shortages are other key risks.

Snapshot of Indicators

| Indicator | Latest Data | Monthly Change | Risk | |

|---|---|---|---|---|

| Monthly Real GDP growth | -0.2% | Jul-22 | down | expected to weaken |

| Business Activity Index (>50 = growth) | 48 | Sep-22 | down | expected to remain fragile with downside risks |

| New Business (>50 = growth) | 46.6 | Sep-22 | down | expected to weaken |

| Indicator | Latest Data | Quarterly Change | Risk | |

|---|---|---|---|---|

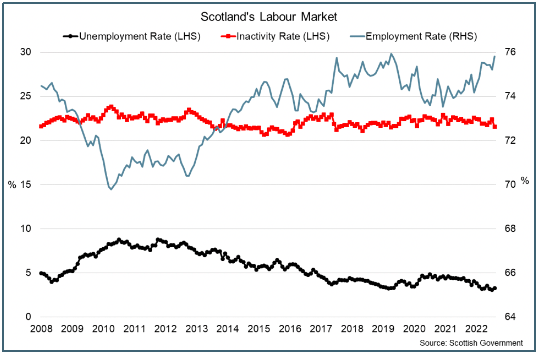

| Unemployment Rate | 3.3% | Jun-Aug 22 | down | expected to remain broadly stable/fine relative to historic trends |

| Employment Rate | 75.8% | up | expected to remain broadly stable/fine relative to historic trends | |

| Inactivity Rate | 21.6% | down | expected to remain fragile with downside risks | |

| Indicator | Latest Data | Monthly Change | Risk | |

|---|---|---|---|---|

| Job Demand Index (>50 = growth) | 63.8 | Sep-22 | down | expected to remain broadly stable/fine relative to historic trends |

| % of firms reporting staff shortages | 41.6% | Sep-22 | down | expected to weaken |

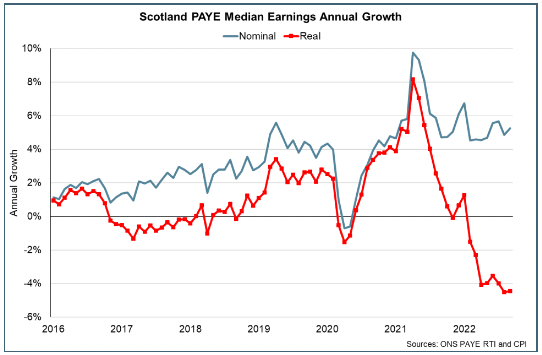

| Nominal median earnings annual growth | 5.3% | Sep-22 | up | expected to remain fragile with downside risks |

| Real median earnings annual growth | -4.4% | Sep-22 | up | expected to weaken |

| Indicator | Latest Data | Monthly Change | Risk | |

|---|---|---|---|---|

| Goods Exports (ex oil and gas) (Nominal growth v same period in 2019) | 12.9% | H1 2022 v H1 2019 | expected to remain broadly stable/fine relative to historic trends | |

| UK Suppliers' Delivery Times (>50 = improving) | 42.1 | Sep-22 | down | expected to remain fragile with downside risks |

| World Geopolitical Risk Index | 129 | Sep-22 | down | expected to remain fragile with downside risks |

| Share of businesses exporting less than a year ago (or unable to export) | 15.8% | Sep-22 | down | expected to remain fragile with downside risks |

| Indicator | Latest Data | Monthly Change | Risk | |

|---|---|---|---|---|

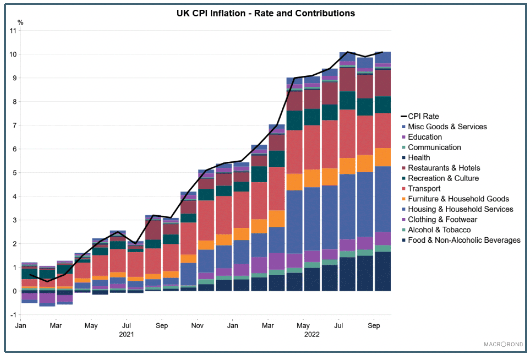

| CPI Inflation Rate (UK) | 10.1% | Sep-22 | up | expected to weaken |

| PPI Input Price Inflation Rate | 20.0% | Sep-22 | down | expected to weaken |

| Oil Brent Crude $/b (monthly average) | $91 | 20-Oct-22 | down | expected to weaken |

| Food Prices Index (F.A.O) | 136.3 | Sep-22 | down | expected to remain fragile with downside risks |

| Exchange Rate (£/$) | 1.12 | 20-Oct-22 | down | expected to weaken |

| Exchange Rate (£/€) | 1.15 | 20-Oct-22 | up | expected to weaken |

| Indicator | Latest Data | Annual Change | Risk | |

|---|---|---|---|---|

| Bond Yields (UK 10 -year) | 3.91 | 20-Oct-22 | up | expected to weaken |

| Public Sector Net Borrowing ex | £20bn | Sep-22 | up | expected to weaken |

| Government Receipts | £71.2bn | Sep-22 | up | expected to remain fragile with downside risks |

| Government Expenditure | £79.3bn | Sep-22 | up | expected to weaken |

| Public Sector Net Debt ex (% of GDP) | 85.1% | Sep-22 | down | expected to weaken |

| Indicator | Latest Data | Monthly Change | Risk | |

|---|---|---|---|---|

| Business Future Expectations (>50 = growth) | 51.5 | Sep-22 | down | expected to remain fragile with downside risks |

| Consumer Sentiment Index (>0 = positive) | -21.1 | Aug-22 | down | expected to weaken |

| Consumer Sentiment Personal Index (>0 = positive) | -26.7 | Aug-22 | down | expected to weaken |

| Consumer Sentiment Economy Index (>0 = positive) | -12.7 | Aug-22 | down | expected to weaken |

| Economic Policy Uncertainty Index (UK) | 226 | Sep-22 | up | expected to remain fragile with downside risks |

The increase in inflationary pressures and the outlook for inflation are very much at the heart of current economic risks. UK inflation rose to 10.1% in September (the same rate as in July) having dipped to 9.9% in August, and is at its joint highest rate since the early 1980s.[3] The rise in inflation has been predominantly driven by increases in the price of electricity, gas and other fuels, up 70.1% over the year to September, driven by the increase in wholesale gas prices, however rising food prices particularly drove the increase in the rate between August and September. Furthermore, inflation has been broad based across goods (13.2%) and services (6.1%) and indicates that domestic inflationary pressures have increased, albeit to a much lesser extent than external drivers.

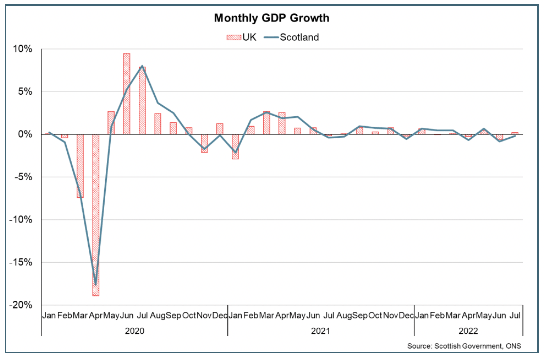

In terms of economic performance, the Scottish economy has been gradually recovering from the pandemic, with GDP 0.1% above its pre-pandemic level. However the pace of growth has been slowing during the year. Latest data for July show Scotland's GDP fell 0.2% over the month, following flat growth (0.0%) over the second quarter. UK GDP as a whole has shown a similar pattern with latest data for August showing a fall of 0.3% over the month and a fall of 0.3% on a 3-month on 3-month basis.[4]

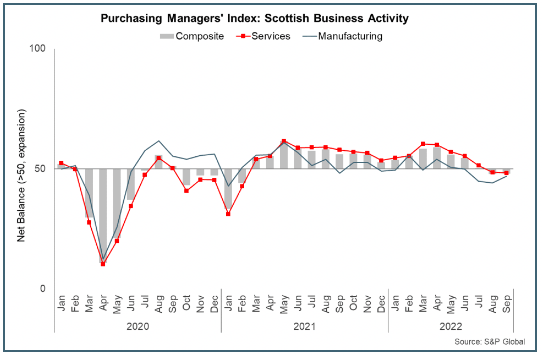

Business survey indicators point to further slowing activity in the third quarter, with the Purchasing Managers' Index (PMI) entering negative territory in August for the first time since February 2021 and remaining negative in September, driven in part by a fall in new business/orders.[5]

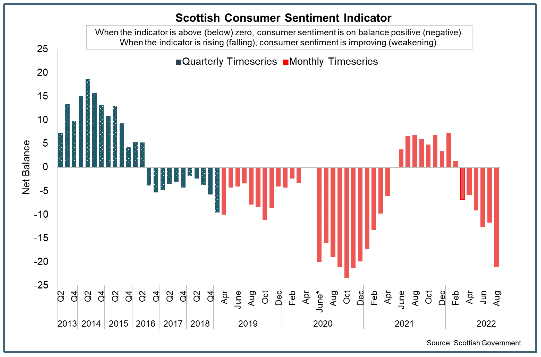

Similarly, there are indications that consumer sentiment and activity is weakening. Consumer sentiment in Scotland has fallen sharply since the start of the year to its lowest level since November 2020 during the pandemic. The survey indicates sharp falls in sentiment regarding the economic outlook, household financial security and how relaxed households feel about spending money.[6]

At a GB level, retail sales volumes fell 1.4% over the month in September and fell 6.9% over the year. However, the value of sales increased by 3.8% over the year, illustrating the impact that rising prices and cost of living issues are having on sales.[7]

The impacts of rising inflation on household budgets is reflected on real earnings. While nominal median PAYE earnings grew 5.3% over the year to September, they fell 4.4% in real terms once adjusted for inflation; the eighth consecutive month of decline.[8]

The growth in nominal earnings partly reflects the ongoing tightness in the labour market. Unemployment in Scotland fell to a record low of 3.1% in the 3-months to July and remains low at 3.3% in the 3-months to August, while vacancy rates remain elevated with 42% of firms reporting a shortage of staff in September, placing upward pressure on pay settlements.[9]

The RBS Jobs Report for September indicates that recruitment activity remains positive, but the levels of demand for staff have eased, indicating that the slowing in business activity and weakening outlook expectations may be starting to feed through to labour market activity.[10] However due to the tightness in the labour market, the Bank of England project that unemployment in the UK is unlikely to rise until mid-2023, despite the economy entering recession.

Contact

Email: OCEABusiness@gov.scot