State of the economy: October 2022

This report summarises recent developments in the global and Scottish economy and provides an analysis of the performance of, and outlook for, the Scottish economy.

Potential Scenarios for the Economy

The level of uncertainty around the economic outlook is exceptionally high, and has been exacerbated further by the UK Government Growth Plan. The degree to which inflation will come down and the extent to which unemployment may be affected are two key factors determining the economic outlook.

Recent developments in international energy markets have highlighted that both the links between gas and electricity pricing, and the potential for constraints in supply at an international level, mean that the outlook for energy supply and consumption are also projected to be a key factor in the economic outlook (see Box A).

The diagram below sets out four alternative potential scenarios for the economy, based on uncertainty over the two dimensions of inflation and unemployment, focusing on energy implications. The top left quadrant 'return to stable growth' is the best case scenario, while the bottom right quadrant 'permanent economic scarring' is the worst case scenario. In the best case scenario, the economy is more energy efficient and energy supply is secure. In the worst case scenario, energy supply becomes constrained and business failure rates are high.

Potential scenarios for the economy: Energy

Return to stable growth (best scenario)

- Inflation returns to target (in part due to energy price guarantee/energy business relief scheme) and economy sees only short interruption to growth.

- Supply chains adapt and commodity prices fall from their peaks, supporting growth.

- Long term electricity contracts provide lower prices and support investment in renewables.

- Economy becomes more energy efficient and energy supply is secure.

Low growth and low investment

- Inflation remains high due to supply chain disruption and high input costs.

- Interest rates continue to rise, increasing the costs of investing in energy efficiency.

- Energy market reform takes time to break link between gas and electricity prices and energy prices remain high.

- Energy intensive businesses struggle.

Recession as demand weakens

- Monetary policy (and energy price guarantee/ energy business relief scheme) reduce inflationary pressure.

- Combination of increased interest rates, supply chain disruption, and a short term fall in real incomes weakens demand in the economy and leads to recession.

- Leads to rising unemployment, business failures, and reduced demand for energy.

Permanent economic scarring (worst scenario)

- Inflation remains high due to supply chain disruption and high input costs.

- Energy price guarantee/energy business relief scheme become unaffordable and is withdrawn, leading to high number of business failures and high unemployment - economic scarring.

- Energy supply becomes constrained, energy rationing in some countries.

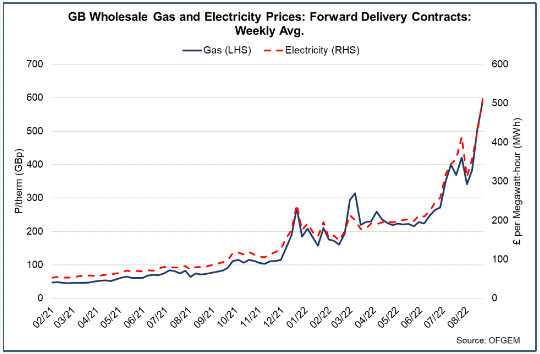

Box A: Energy Demand and Supply

The UK gets around 40% of its electricity demand from gas fired power stations and as such the cost of gas has a strong impact on the cost of electricity.[16] With gas prices at record highs, electricity prices have also risen with little distinction between the cost of electricity produced by gas and electricity produced by other means. In the GB market, the price of electricity is dictated by the costs of the final unit of electricity required to meet demand, which is often gas.

The initial UK Government policy response has been one of price support (energy price guarantee / energy business relief scheme). A market limitation of this is that it weakens price signals and could mean that energy demand could remain too high. So far, energy demand does not appear to have significantly changed as the price cap has changed, and it may not come down further with the introduction of the price guarantee. Therefore, although the energy price guarantee mitigates the price it also distorts the market mechanism in terms of driving change in energy consumption and innovation as you would expect with such a price change. The Energy Price Guarantee will be reviewed in April 2023 and as such there is uncertainty regarding the nature and level of the policy response beyond this.

However, there are limited options to cut demand in the short run and therefore supply side issues become more important. The UK is a net energy importer and recent price changes have contributed to overall changes in the trade balance.

The alternative policy response is to provide income support, that is, transfers to households. The final component of the policy response is to break the link between electricity and gas prices. Decoupling could be done through fundamental change and restructuring of the GB wholesale market. This is the focus of the UK Government's review of electricity market arrangements, with the expectation that such reforms will tackle other structural issues including security of supply, overall system costs and meeting decarbonisation targets over the longer term.

Another uncertainty for the economy is around wages and the extent to which new pay deals will offset a fall in living standards or will lead to a wage price spiral. As noted above, labour shortages are high and real earnings are falling. Nominal wage inflation has continued to increase, averaging around 6%, with a significant proportion indicating that they had given, or were considering giving, interim one-off payments to staff to help offset rising costs.

The diagram below sets out the same alternative scenarios for the economy, based on uncertainty over the two dimensions of inflation and unemployment, but focuses on the implications for wages. In the best case scenario, short term wage increases offset some of the fall in living standards. In the worst case scenario, pressure on wages is untenable for firms and ultimately leads to greater inequality. The scenario that will play out will depend on the extent to which nominal wages rise in response to inflation and the bargaining power of employees to negotiate higher wages. Box B presents modelling of an inflationary impact on the Scottish economy.

Potential scenarios for the economy: Wages

Return to stable growth (best scenario)

- Inflation returns to target (in part due to energy price guarantee/eenergy business relief scheme) and economy sees only short interruption to growth.

- Supply chains adapt and commodity prices fall from their peaks, supporting growth.

- Short term wage increases offset some of fall in living standards, which recover as inflation falls.

- Unemployment remains low.

Low growth and low investment

- Inflation remains high due to supply chain disruption and high input costs.

- Labour market shortages, supply chain disruption, and inflation push wages higher.

- Interest rates remain high in response.

- Unemployment remains low due to labour shortages but there is growing underemployment as businesses reduce worker hours.

- Drives a wage-price spiral.

Recession as demand weakens

- Monetary policy (and energy price guarantee/ energy business relief scheme) reduce inflationary pressure.

- Combination of increased interest rates, supply chain disruption, and a short term fall in real incomes weakens demand in the economy and leads to recession.

- Increased business failures, higher unemployment, continued squeeze in living standards.

Permanent economic scarring (worst scenario)

- Inflation remains high due to supply chain disruption and high input costs.

- Firms seek to cut costs, reducing staff and leading to significant business failures and rising unemployment.

- Pressure to raise wages remains, leading to divide between in-work and out-of-work incomes and greater inequality.

Box B: Modelling an Inflationary Impact on the Scottish Economy

Prices play an important role in the purchasing decisions of consumers and firms by affecting incentives to spend or save; to delay or accelerate future investment plans; and crucially by playing a key role in efficiently allocating scarce resources.

The current increase in inflation is being driven predominantly by the supply side of the economy due to increases in the price of energy and disruption to supply chains. Broadly speaking, these kinds of shocks result in the economy no longer being able to produce the same quantity of goods or services as it used to for the same price. In effect, services and goods become scarcer and hence prices increase to ration out these scarcer resources.

Generally, a small, stable, positive inflation rate is considered to be economically useful. However, periods of high inflation can impair the economy's long-term performance; as well as cause short-term transitory distortions which can often affect certain households disproportionately. For example, food, transport and energy prices are particularly sensitive to commodity price shocks and inflation can be relatively higher for poorer households who tend to spend more of their budgets on this type of expenditure. A recent study by the Institute for Fiscal Studies (IFS)[17] noted that some households with the lowest incomes could experience an inflation rate around seven percentage points higher in October relative to households with the highest incomes.

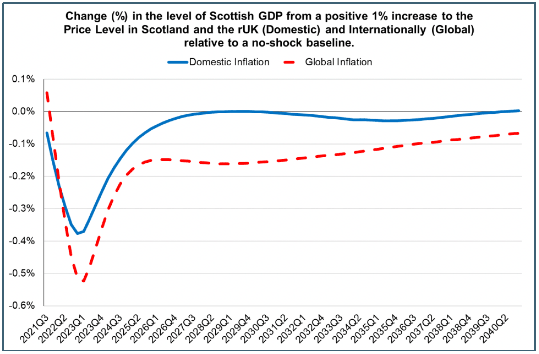

We use the Scottish Government General Equilibrium Model (SGGEM) to analyse the impact of a temporary period of higher inflation on the Scottish economy, focussing on the channels through which inflation affects the economy rather than trying to quantify the impact of the current level of inflation.

In general, the modelling shows that a temporary increase in the price level has a negative impact on the size of the economy. Although nominal wages rise in response to the inflation shock, they do not rise as quickly as prices, reducing real wages and aggregate private sector consumption at the same time as a reduction in private sector investment due to rising interest rates.

The current inflation shock is also being felt by our largest trading partners. Running a scenario where there is a global temporary inflation shock results in a bigger initial impact on the Scottish economy and a slower recovery. This largely reflects the fact that the global economy shrinks which results in lower international investment and trade compounding the negative shock to the domestic economy.

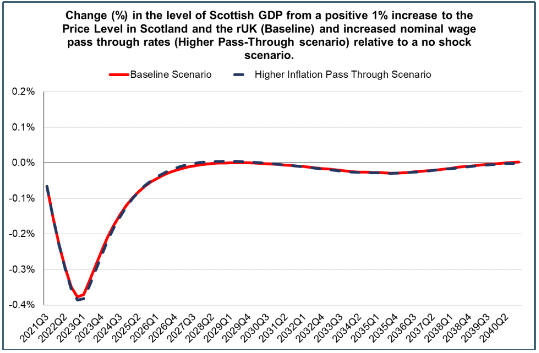

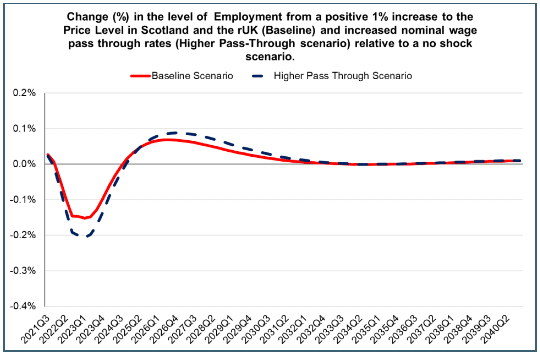

Another characteristic of the current crisis is that the economy currently has a relatively tight labour market, with high vacancies and low unemployment. As a result, most forecasters are not expecting an immediate substantial increase in unemployment in response to the shock. To examine the impact of this, we consider the sensitivity of the results to the degree of 'pass through' from inflation to nominal wage growth, which can be thought of as reflecting the bargaining power of employees to negotiate higher wages. Changing this assumption has a relatively marginal impact on GDP (first chart below) however, it has a more pronounced impact on the labour market (second chart below).

As can be seen, differences in the tightness of the labour market do not appear to have a big effect on how the size of the economy is affected by an inflationary shock. Rather, it has a larger impact on the labour market, through employment and wages. This highlights how the impacts of inflation could be unevenly felt, with those in stable employment and able to secure relatively larger pay increases potentially more resilient to the current inflationary challenges. This highlights the risks set out in the scenarios and in particular the risks to inequality from a worst case scenario of high inflation and high unemployment. A range of policies have already been announced to help households mitigate the impact of higher prices, and there is likely to be a continuing need for such intervention in the short to medium term, as the economy transitions to potentially permanently higher prices for essential commodities.

Contact

Email: OCEABusiness@gov.scot