State of the economy: October 2022

This report summarises recent developments in the global and Scottish economy and provides an analysis of the performance of, and outlook for, the Scottish economy.

Monetary and Fiscal Policy Response

The outturn data illustrates the economic risks which have emerged, however, the level of uncertainty in the economic outlook continues to be extremely elevated, both at a global and domestic level.

In response to rising inflation and slowing growth, in October the IMF forecast global growth to slow to 3.2% in 2022 and to 2.7% in 2023 (revised down 0.2 percentage points from July).[11] In August, the Bank of England revised down its forecast for the UK economy with its central scenario projecting inflation to rise to 13% and pushing the UK economy into recession throughout 2023.[12]

Furthermore, the outlook will be influenced by the monetary and fiscal policy response. Despite the risk of inducing recession, monetary policy is being tightened by central banks as they seek to address underlying inflationary pressures and to reduce the risk that they become embedded more widely in the economy and persist for longer. Higher interest rates will increase the cost of borrowing and debt financing for households and businesses while providing a higher return for savers.

The fiscal expansionary measures announced in the UK Government Growth Plan, many of which have subsequently been reversed, are expected to have material implications for the economic outlook and public finances. It remains unclear how the remaining tax cuts will be funded and the extent to which public expenditure cuts will be forthcoming. The Office for Budget Responsibility will publish its forecasts on 31 October alongside the UK Government's Medium Term Fiscal Plan.

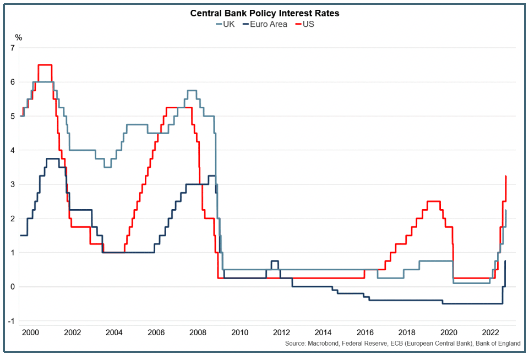

The Bank of England's Monetary Policy Committee has implemented seven consecutive increases in the Bank Rate since December 2021, taking it from 0.1% to 2.25% in September, its highest rate since 2008.[13] The US Federal Reserve announced a fifth successive rate rise in September, increasing its federal funds rate by 0.75 percentage points to a target range of 3% – 3.25%, while the European Central Bank raised interest rates by 0.75 percentage points to 0.75%.

With tightening monetary policy, the scale and duration of the economic downturn in the short term will depend in part on the ability of fiscal policy to support businesses and households through the period of high inflation and low growth while enabling inflation to fall sustainably back to its target rate of 2%.

In response to the significant impact that rising energy prices were projected to have on household and business costs, the UK Government has set out a 6-month package of energy relief for households and businesses to tackle the cost crisis. The Energy Price Guarantee will cap typical household energy bills at £2,500 per year until April 2023, when the policy is scheduled for review. This takes account of the £150 removal of green levies and together with the previously announced £400 energy price rebate means that bills will effectively remain capped at around £2,100 over the winter. Alongside this, businesses (including charities and public sector organisations like schools) will now pay the same energy prices as households for the next six months, with a further review scheduled to consider how to provide ongoing focused support to vulnerable industries, such as Hospitality.

The introduction of the Energy Price Guarantee is expected to reduce the extent to which inflation will rise in the short term, with the Bank of England expecting inflation to now peak at just under 11% in October. However due to the increase in energy prices already embedded, inflation is expected to remain above 10% over the next few months. The extent to which the policy will mitigate energy price inflation in the economy is uncertain beyond April 2023, however the Bank of England will publish their next Monetary Policy Report and forecasts on 3 November.

The larger stock of debt through higher borrowing will also increase the longer term challenges facing sustainability in the public finances, with public sector debt costs in August at a record high.

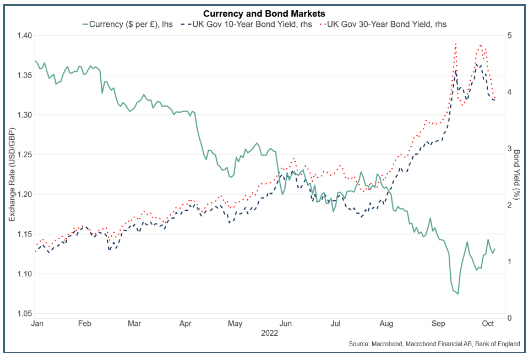

The increasing scale of uncertainty and risk in the economic outlook continues to be reflected in financial market volatility. In the week beginning 24 September, the pound fell to its lowest levels against the dollar since 1985, and bond yields rose to their highest rates in over a decade. Due to the scale of repricing of financial assets, particularly affecting long-dated UK government debt and the exposure of pension schemes, the Bank of England intervened to carry out temporary purchases of long-dated nominal UK government bonds to restore market functioning and reduce risks to UK financial stability.[14] This supported some reversal in the sharp market movements from the previous week, however further subsequent increases in bond yields and the associated risks to UK financial stability resulted in the Bank announcing enhancements to its operations to further support market functioning and an orderly end to the bond purchase scheme.

Following the completion of the Bank's temporary bond-buying scheme and the announced reversal of many of the UK Government Growth Plan measures, Sterling has further recovered from its sharp fall in September, while bond yields have partly reversed from its recent spikes, however remain notably higher than in recent months.

Contact

Email: OCEABusiness@gov.scot