Scottish Housing Market Review Q4 2025

Quarterly bulletin collating a range of previously published statistics on the latest trends in the Scottish housing market.

Part of

6. Mortgage Interest Rates

After a tightening cycle which took Bank Rate from 0.1% prior to the December 2021 Monetary Policy Committee (MPC) meeting to 5.25% following the August 2023 meeting, its highest level since 2008, the MPC held Bank Rate steady for the following 12 months. The MPC then cut Bank Rate in regular increments of 0.25% points until it stood at 4% in August 2025. In December 2025 there was a further 0.25% point cut which took it to 3.75%. The next MPC meeting is scheduled for 5 February 2026.

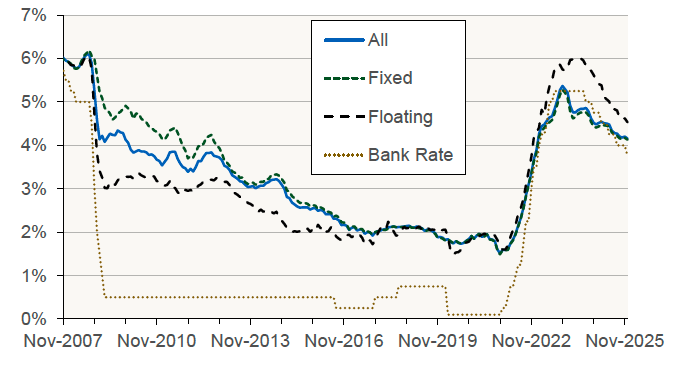

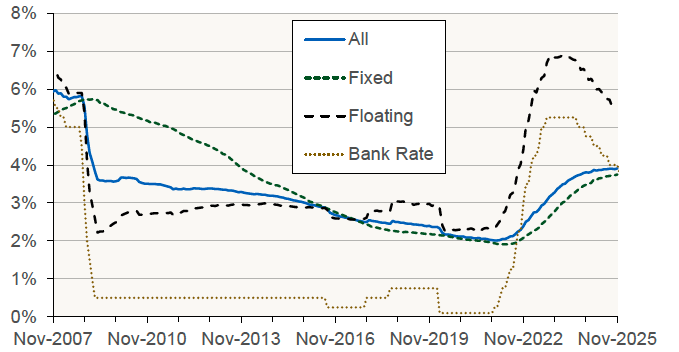

Chart 6.1 and Chart 6.2 shows the effective (or average) interest rates on new mortgage advances and outstanding mortgage balances in the UK. [Source: Bank of England] Reflecting successive cuts in Bank Rate since August 2024, over the 15 months to November 2025, the average interest rate for new floating-rate mortgage advances has fallen by 1.2% points to 4.53%, while for fixed-rate mortgages the average rate has fallen by 0.6% points to 4.13%.

While the average rate on outstanding floating-rate mortgages has also fallen over this period in response to the cuts in Bank Rate (by 1.23% points to 5.48%), the average rate on outstanding fixed-rate mortgages has continued to trend up (from 3.35% in August 2024 to 3.75% in November 2025) as mortgages which reach the end of their fixed period are refinanced at higher rates – this applies particularly to mortgages which had longer-duration fixes.

Effective monthly interest rates on mortgage lending to households: UK (Data as at month-end, to November 2025)

Source: Bank of England

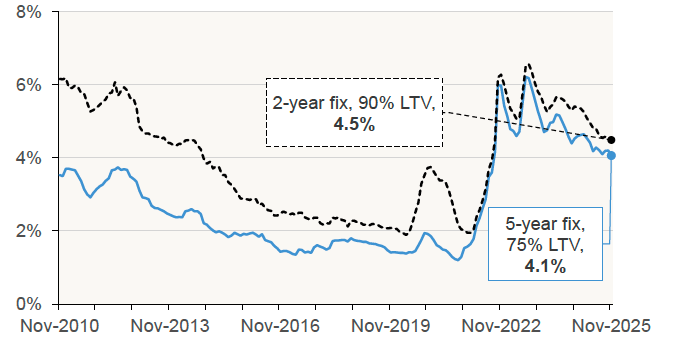

Bank of England data on advertised mortgage rates (as opposed to data in Chart 6.1 which is based on interest actually paid) also shows that advertised mortgage rates are significantly off the peaks reached during the current interest-rate cycle. The average advertised two-year fixed rate for a 75% LTV mortgage has fallen from its post-pandemic peak of 6.22% in July 2023 to 4.06% in November 2025 (down 2.16% points), while the average advertised rate for a 2-year 90% LTV mortgage has fallen from its post-pandemic peak of 6.57% in August 2023 to 4.49% in November 2025 (down 2.08% points).

Source: Bank of England

Data from the Moneyfacts Treasury Report, also relating to advertised rates but averaged across LTVs,[3] shows that the average 2-year fixed-rate mortgage was 4.86% in December 2025, down from 5.52% in December 2024. Over the year, there was also reduction in the average 5-year fixed-rate from 5.28% to 4.91%.

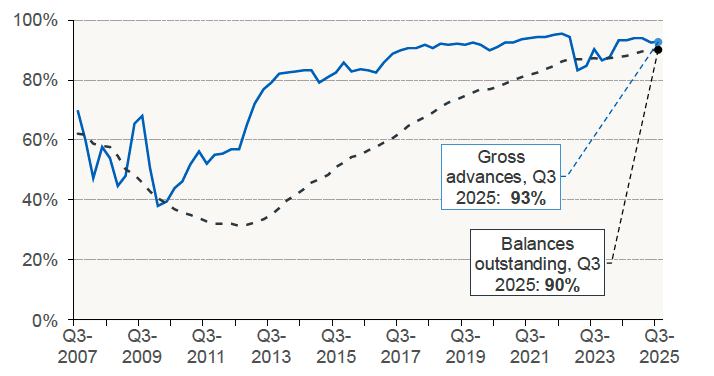

Chart 6.4 shows that the vast majority of regulated[4] mortgages are on fixed rates. The share of gross advances on fixed rates in Q3 2025 was 93%, while the share of outstanding balances on fixed rates in Q3 2025 was 90%. (Source: FCA).

Source: FCA

Contact

Email: Jake.Forsyth@gov.scot