Scottish Housing Market Review Q4 2025

Quarterly bulletin collating a range of previously published statistics on the latest trends in the Scottish housing market.

Part of

7. Mortgage Affordability

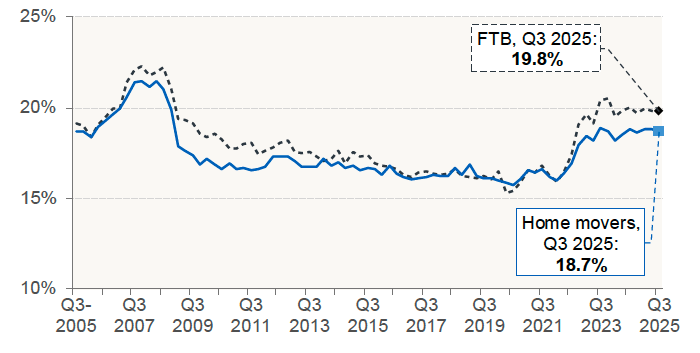

As illustrated by Chart 7.1, the share of borrower income taken up by capital and interest payments for new mortgages peaked at the end of 2023 due to the rise in mortgage interest rates. Subsequently, mortgage interest rates have been falling, which has led to increased affordability. Over the last year, the share of borrower income taken up by mortgage costs has stabilised, although it is still significantly above the post-financial crisis long-run average.

For first-time buyers, who tend to borrow a high proportion of the purchase price and are thus relatively more exposed to interest-rate risk (see Chart 5.3), the share increased from a low of 15.3% in Q2 2020 to 19.8% in Q3 2025, although this is down slightly from 20.0% a year previously. For home movers, the share has increased from a low of 15.7% in Q3 2020 to 18.7% in Q3 2025, which is similar to Q3 2024.

Source: UK Finance

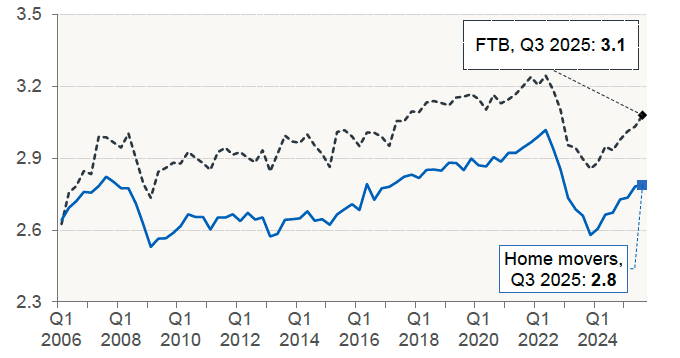

Chart 7.2 shows that the average house-price-to-income ratio for new mortgages in Q3 2025 was 3.1 for first-time buyers and 2.8 for home movers, which for each series is similar to its long-term average since Q2 2005.

Source: UK Finance

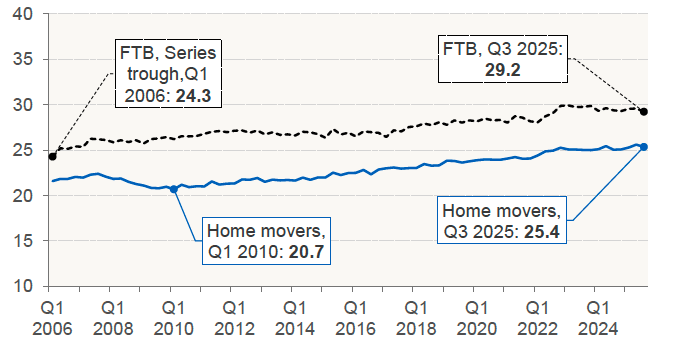

To make their monthly repayments more manageable, an increasing share of borrowers have responded by taking out longer mortgages. Chart 7.3, which relates to Scotland, shows that this is part of a longer-term trend.

Source: UK Finance

Contact

Email: Jake.Forsyth@gov.scot