Scottish Housing Market Review Q4 2025

Quarterly bulletin collating a range of previously published statistics on the latest trends in the Scottish housing market.

Part of

5. Mortgage Advances, Approvals and LTVs

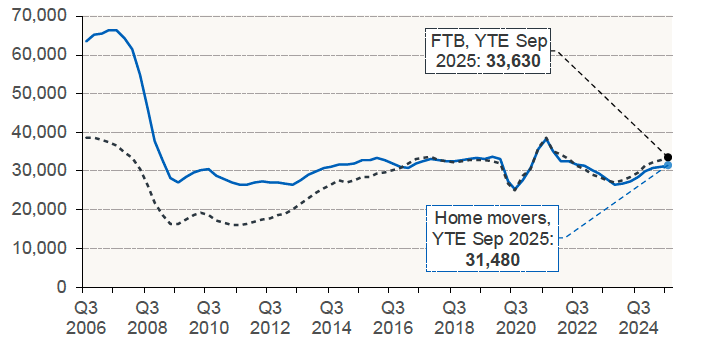

5.1. New Mortgage Advances

There were 9,350 new mortgages advanced to first-time buyers for house purchase in Scotland in Q3 2025, an annual increase of 7.8%. Meanwhile, there were 8,820 new mortgages advanced to home movers, an annual increase of 4.3%. Chart 5.1 shows the trend in new mortgages advanced using a 4-quarter moving total. In the year to end Q3 2025, the 33,630 new mortgages advanced to first-time buyers was the highest since Q1 2022. Over the same period, the 31,480 new mortgages advanced to home movers was the highest since Q3 2022 [Source: UK Finance].

Source: UK Finance

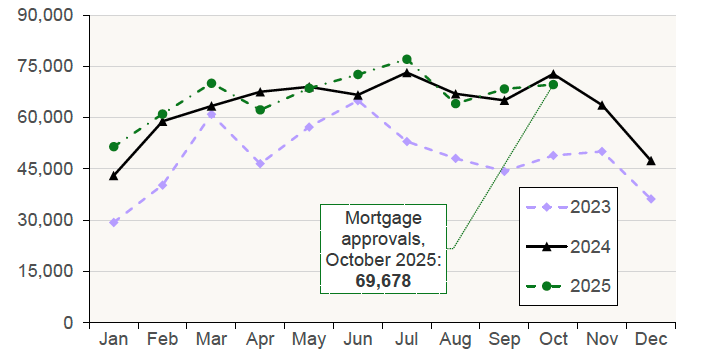

5.2. Mortgage Approvals

Chart 5.2 plots the monthly number of mortgage approvals across the UK for house purchase by individuals. Mortgage approvals for house purchase, which are the firm offers of lenders to advance credit fully secured on dwellings by a first-charge mortgage, are a leading indicator of mortgage sales as they reflect activity early in the buying process.

The number of mortgage approvals in the UK between August 2025 and October 2025 was 202,112, an annual decrease of 1.3%. Focussing on the latest monthly data that is available, the number of mortgage approvals in October 2025 was 69,678, an annual decrease of 4.2%. [Source: Bank of England].

Source: Bank of England

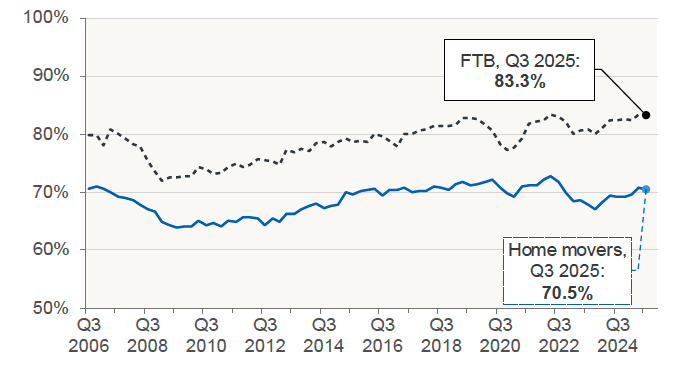

5.3. Loan-to-Value (LTV) Ratios

Chart 5.3 shows that after initially falling following the Covid pandemic, mean LTV ratios on new mortgages advanced to both first-time buyers and home movers in Scotland recovered to their pre-pandemic levels, before declining again as the upward trend in interest rates beginning at the end of 2021 fed through to mortgage lending.

Subsequently, there has been an upward trend in mean LTV ratios for both first-time buyers and home movers in Scotland. However, after reaching a recent peak of 83.4% in Q2 2022, the mean LTV ratio for first-time buyers fell slightly to 83.3% over the following quarter. Similarly, the mean LTV ratio for home movers fell slightly from 70.7% to 70.5%. [Source: UK Finance]

Source: UK Finance

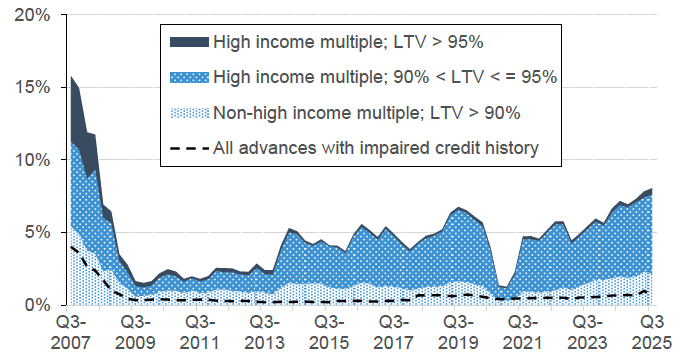

The share of all regulated residential lending across the UK with an LTV greater than 90% increased over the quarter from 7.8% to 8.1% in Q3 2025. The share of all lending with both an LTV greater than 90% and a high income multiple also increased from 5.5% in Q2 2025 to 5.9% in Q3 2025. For both categories, these figures represent the highest levels seen since before the 2008 financial crisis.

Source: FCA. Higher-risk lending is classified by the FCA as an LTV over 90% or an income multiple greater than or equal to 3.5 for single-income purchasers or 2.75 for joint-income purchasers.

The total number of residential mortgage products increased by 136 over the month to stand at 7,054 in early December 2025, which is just below the series peak in September 2025 (7,062). Over the month, product availability increased across all LTV tiers except the 100% bracket. The largest rise occurred in the 90% LTV tier, where the number of mortgages grew by 20, reaching a total of 917. [Source: Moneyfacts UK Mortgage Trends Treasury Report]

There has been a significant increase in the number of buy-to-let (BTL) products, which have risen from 3,231 in December 2024 to 5,237 in December 2025, the highest level since Moneyfacts records for this series began in 2011. [Source: Moneyfacts UK Mortgage Trends Treasury Reports]

Contact

Email: Jake.Forsyth@gov.scot