Publication - Research and analysis

Scottish economic bulletin: July 2026

Provides a summary of latest key economic statistics, forecasts and analysis on the Scottish economy.

Economic Outlook

The impacts of the energy price shock are expected to continue filtering through the economy in the second half of this year.

- Latest economic forecasts were undertaken before the US - Iran MoU in mid-June to extend the military ceasefire and begin to reopen the Strait of Hormuz. However the ongoing impacts of the conflict in the Middle East are expected to continue to impact through the second half of the year with ongoing uncertainty on disruptions to the agreement and the pace at which global energy supply chains will recover.

- At a global level, the World Bank cut its 2026 global growth forecast to 2.5% in June, with growth projected to slow from 2.9% in 2025 due to higher energy prices and inflation weighing on growth. GDP growth is expected to recover to 2.8% by 2027–28, while global inflation is projected to rise to 4% in 2026 from 3.3% in 2025, even if oil supply stabilises in the near term.[24] Similarly, the OECD has revised down its 2026 global growth forecast to 2.8% before picking up to 3.1% in 2027, assuming a time-limited disruption scenario.[25]

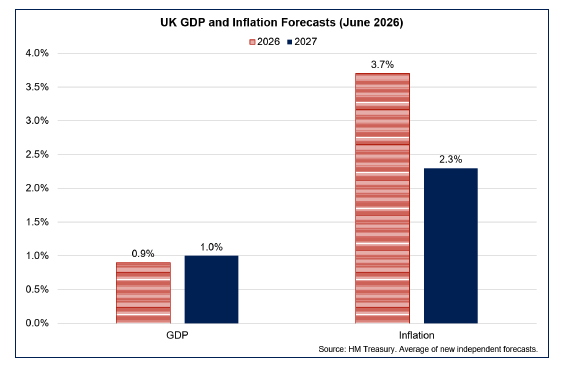

- At a UK level, the latest HMT average of independent forecasts from the first half of June shows UK GDP growth at 0.9% in 2026 (down from 1.1% forecast in February prior to the Middle East conflict), rising to 1.0% in 2027. This remains broadly in line with the Bank of England projections from April.[26],[27]

- The inflation outlook has shifted notably from earlier projections this year, though it remains subject to a high degree of uncertainty. The HMT average of new independent forecasts from the first half of June shows inflation projections have been revised up to 3.7% for 2026, from 2.2% projected in February prior to the conflict.

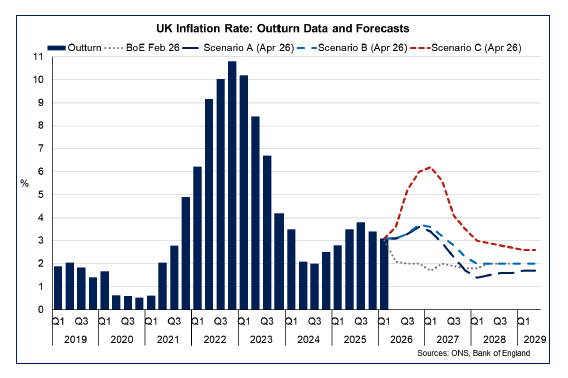

- The Bank of England updated its inflation projections following its June rate decision. In its April Monetary Policy Report, the Bank presented three illustrative scenarios reflecting different paths for energy prices during the Middle East conflict, however, the recent easing in tensions and energy prices has led to a softer central outlook. It now expects inflation to be just under 3% in Q3 2026, rising to slightly above 3.25% in Q4.[28] In the near term, this is slightly lower than the path set out in April in the chart below.

- Longer term however, uncertainty in the inflation outlook remains closely linked to energy supply dynamics, particularly oil and gas flows through the Strait of Hormuz. While the recent US - Iran agreement has eased tensions and helped bring oil prices back to around pre-conflict levels, gas prices remain around 20% higher. Some supply constraints may persist, as oil flows are unlikely to return to pre-conflict levels immediately, suggesting continued pressure on domestic energy costs. The extent to which these pressures feed through to the wider economy remains a key risk and uncertainty to the overall outlook.

Contact

Email: economic.statistics@gov.scot