Publication - Research and analysis

Scottish economic bulletin: July 2026

Provides a summary of latest key economic statistics, forecasts and analysis on the Scottish economy.

Business Conditions

Business activity contracted in May, as demand continued to weaken, although business optimism improved moderately amid easing global energy prices.

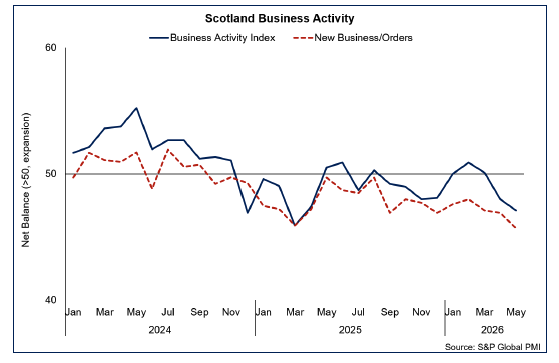

Business Activity

- Business surveys indicate that business activity has been on a downward trend since the start of the conflict in the Middle East, amid increases in global energy prices, following subdued, but positive, business activity at the start of the year.

- The RBS Growth Tracker business survey indicated that the contraction in business activity accelerated in May, with an index reading of 47.1 (a reading below 50 indicates contracting business activity); its lowest since March 2025. Weak underlying demand remains a key driver of this with the index for new business recording a twentieth consecutive month of contraction and falling to its lowest level since January 2023.[11]

- Latest Business Insights and Conditions Survey (BICS) data for May indicates some improvement from April, with businesses more likely to have seen an increase in demand over the month (17.6%, up from 13.3% in April), or stable demand (48.5%, up from 43.5%) than were reporting to have seen a decrease (10.5%, down from 16.7%). This varies by sector, with businesses most likely to report decreased demand being in the Transport and Storage sector (18.8% compared with 16.1% reporting an increase).[12]

Business Concerns

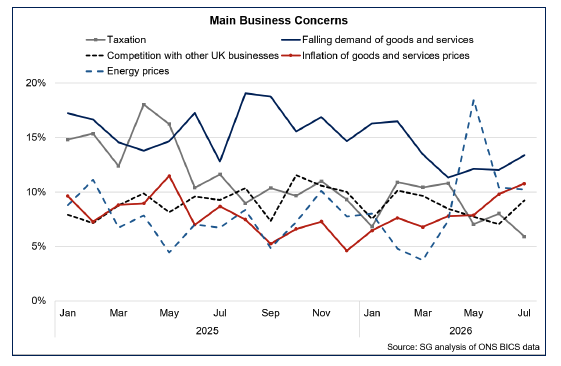

- The latest BICS data from the first half of June shows that falling demand remains the most reported main concern by businesses (13.4%) and has risen since the start of March, albeit the share of businesses reporting it as a main concern is lower than in 2025.

- This is in part due to other concerns being reported more frequently, with an increasing share of businesses reporting to be concerned about inflation of goods and services (10.8%) since the start of the year. Additionally, since March and the escalation of the conflict in the Middle East took effect, there has been an increased share of businesses reporting to be most concerned about energy prices (10.2%), although it has moderated from its spike in April.

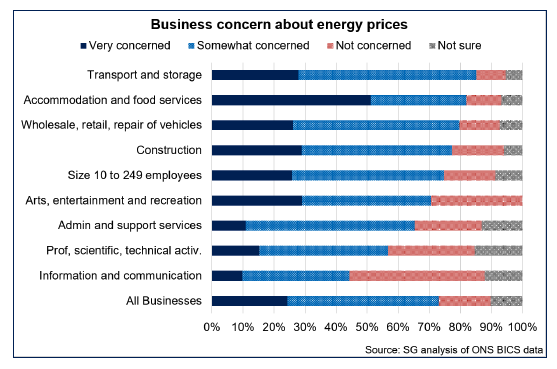

- The increased concern regarding energy prices reflects the increased oil and gas prices arising from the conflict in the Middle East. BICS data from the first half of June (prior to the US–Iran MoU agreement) indicates that 73.1% of businesses in June were very or somewhat concerned about energy prices. This share is moderately smaller than in May (75.8%), with fewer businesses reporting to be ‘very concerned’. However, this concern is relatively broad based across sectors, being most notable in the transport and storage sector (85.1%) and accommodation and food services sector (82.0%).

- Oil and gas prices have come down notably and to near pre-conflict levels following the US-Iran MoU agreement in mid-June, albeit there continues to be uncertainty around the pace at which oil and gas supply chains will recover.

Business Costs

- While the Energy Price Cap protects most UK households from immediate changes in energy prices, this does not apply to businesses who have been subjected to increased energy prices depending on existing supplier agreements.

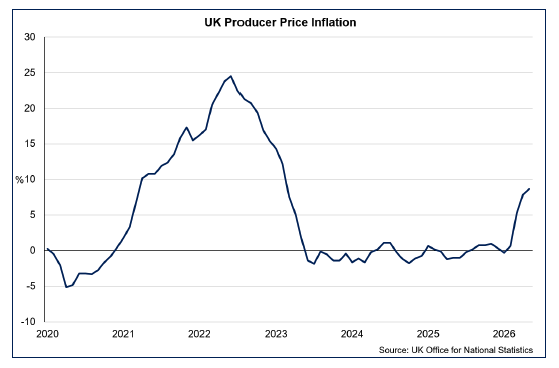

- UK producer input prices rose by 8.7% annually in May, up from 7.9% in April. Crude oil prices remained the main driver of the annual increase in input costs, rising by 71.8% in the year to May, albeit crude oil prices fell 5.9% over the month.[13]

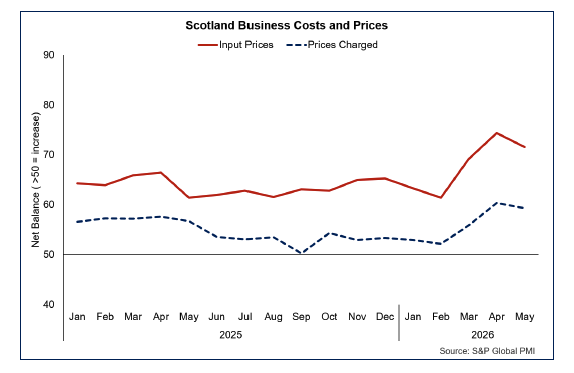

- Similarly, the RBS Growth Tracker business survey also indicated that business input costs continued to rise between April and May, albeit the rate of inflation eased from the previous month. Respondents cited higher energy, raw material and transport costs as the drivers of input price inflation amid the conflict in the Middle East.[14]

- The extent to which businesses have had to, or are able to pass on higher costs to customers depends on various factors, including demand and competition conditions. The prices charged for goods and services by businesses has also increased since the outset of the Middle East conflict but to a lesser extent, indicating that while businesses are passing on part of the increased costs, they are also absorbing some of it. The RBS Growth Tracker data shows that the pace of output price inflation also eased in May, but remains elevated comparing to its pre-conflict level.

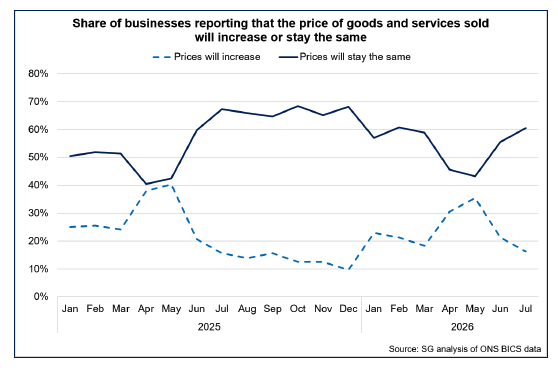

- Furthermore, BICS data from June shows that the share of businesses reporting that they expect to increase prices on goods and services sold, fell from the previous month (16.3%, down from 21.3%), while an increased share of businesses expect prices to remain unchanged in July (60.5%, up from 55.5%).

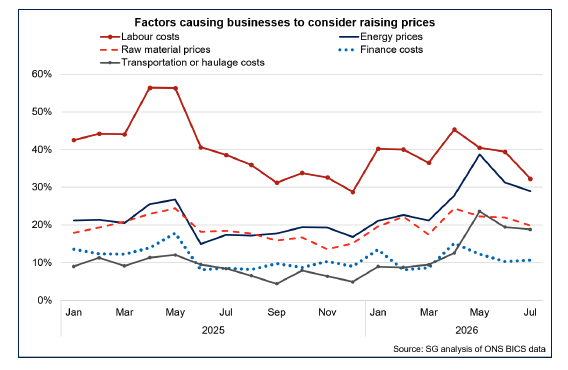

- For businesses expecting to increase prices, labour costs remains the main driver with 32.3% reporting it as a factor. This is however down from its share at the start of the year. Labour costs as a factor is followed by energy prices (29.0%), which has seen an increase in its share in recent months, albeit it has fallen from its recent peak in May. Transportation costs have also been cited by an increasing share of businesses as a factor to consider raising prices amid increases in motor fuel prices. 18.8% of businesses reported this as a factor in June, broadly unchanged over the month.

Business Optimism

- The conflict in the Middle East and increased uncertainty around its risks to inflation and demand has had a notable impact on business sentiment and optimism. The RBS Growth Tracker business survey reported that business optimism improved marginally in May, but remains notably below pre-conflict levels.[15]

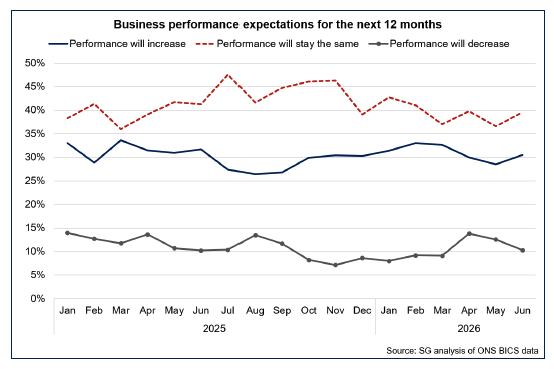

- Similarly, BICS data shows that an increasing share of businesses expect performance to improve (30.5%, up from 28.5% in May) or stay the same (39.5%, up from 36.6% in May) compared to last month. This is mirrored by a smaller share of businesses expecting performance to decrease in the coming year (10.3%, down from 12.6% in May).

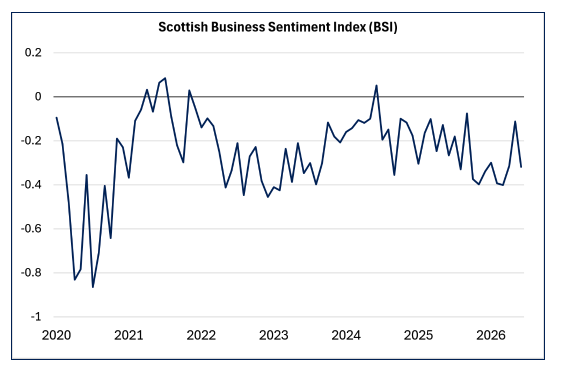

- The Scottish Business Sentiment Index (BSI) provides a real-time measure of business confidence in Scotland by analysing sentiment in news articles related to corporate and industrial developments.[16],[17] Latest data indicates that the BSI fell in June to -0.32 having improved moderately in May and remains below the average for 2025 (-0.24).

Contact

Email: economic.statistics@gov.scot