Publication - Research and analysis

Scottish economic bulletin: July 2026

Provides a summary of latest key economic statistics, forecasts and analysis on the Scottish economy.

Inflation and Cost of Living

The inflation rate remained stable in May, however is expected to rise moderately in the months ahead.

Inflation

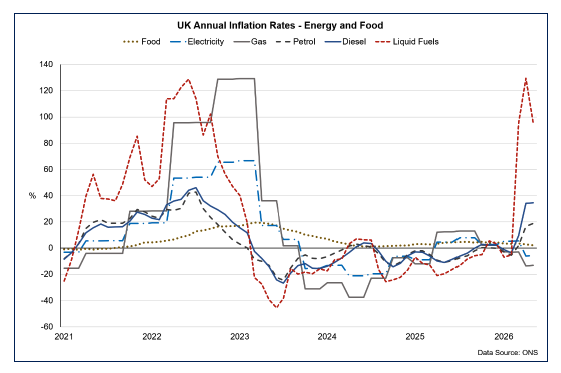

- The UK inflation rate remained at 2.8% in May, unchanged from April and down from 3.3% in March, with part of this fall continuing to reflect the 7% reduction in the Ofgem energy price cap (EPC) that took effect in April.[3]

- Key movements in the annual inflation rate between April and May were in food and non-alcoholic beverages which fell from 3% to 2.2%, its lowest annual rate since December 2024 and partly reflected a marginal fall in the price index over the month. In contrast, annual transport inflation rose from 4.5% to 6.8%, its highest rate since December 2022. The increase in transport price inflation was partly driven by air fares and motor fuels, with annual petrol price inflation at 18.9% and diesel at 34.6%, albeit the diesel index fell 1.5% over the month.

- The greater stability in petrol and diesel prices in May partly reflected that oil prices averaged $104 per barrel over the month, broadly unchanged from an average of $102 in April. Since the announcement of the US–Iran Memorandum of Understanding (MoU) on June 14, oil prices have fallen further to c.$75 and are broadly back to their level before the Middle East conflict escalated at the end of February. As of the final week in June, weekly petrol and diesel prices in the UK are also down c.5% and c.13% from their peaks earlier in the conflict, respectively.[4] However, looking ahead, disruption and risks to the ceasefire continue to present price uncertainty.

- The EPC rose by 13% at the start of July reflecting the increase in wholesale energy prices between March and May.[5] The EPC will next change in October and will partly depend on how energy prices evolve in the coming months.[6]

- Outwith the EPC, households using heating oil continue to experience elevated prices albeit they moderated in May and into June. The household liquid fuels price index fell over the month by 18.7% in May, however remains 95.6% higher compared to May 2025.

- Core inflation, which excludes energy, food, alcohol and tobacco, rose marginally to 2.6% in May, up from 2.5% in April. However it remains lower than 3.1% in March and is lower than headline inflation, indicating that the increase in energy prices are still to fully feed through to wider consumer prices.

Monetary and Credit Conditions

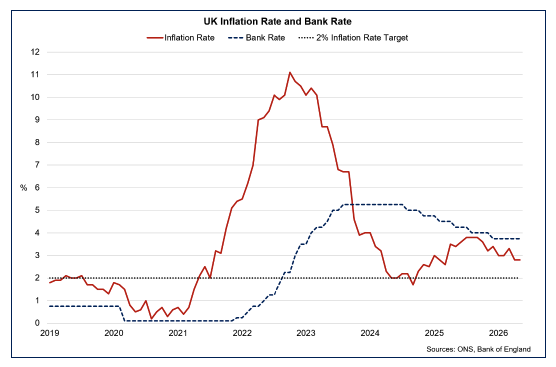

- Looking ahead, inflation is projected to rise during the second half of this year, however developments over the past month have moderated inflationary expectations. The Bank of England revised down its inflation outlook as part of its June rate announcement. Inflation is now expected to be around 3% in Q3 2026 and around 3.25% in Q4 2026, representing a downward revision compared with the projections made in the April Monetary Policy Report but are still notably higher than the 2% which was projected in February, prior to the conflict.[7],[8]

- The Bank’s Monetary Policy Committee (MPC) held the Bank Rate in June at 3.75%. The Committee judged that while energy prices remain elevated relative to pre‑conflict levels, upside risks have eased somewhat in light of recent geopolitical developments. At the same time, financial conditions remain restrictive, with businesses and consumers continuing to face higher interest rates.

- The Bank also set out that there was evidence that underlying disinflation had been on track prior to the conflict, while a looser labour market and weak underlying demand continue to dampen second-round effects, reducing the need for further monetary tightening at this stage.

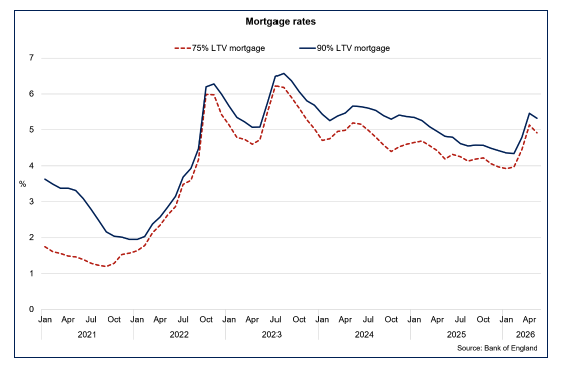

- Increased expectations of higher inflationary pressures and potentially tighter monetary conditions, albeit softening over the month, have fed through to some borrowing costs faced by households. For example, interest rates on two-year 75% and 90% loan‑to‑value (LTV) mortgages eased slightly in May to 4.92% and 5.32%, respectively, down from 5.14% and 5.46% in April. However, rates remain elevated compared with pre‑conflict levels in February, when they stood at 3.97% and 4.34%.[9]

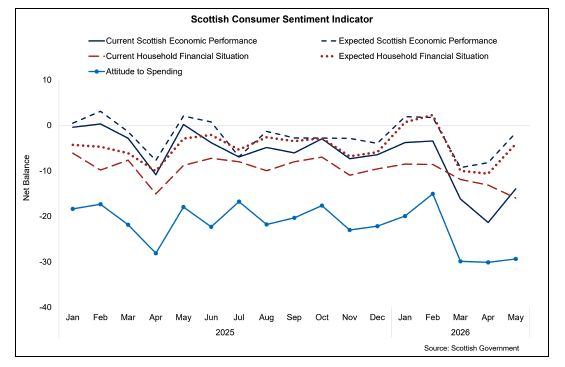

Consumer Sentiment

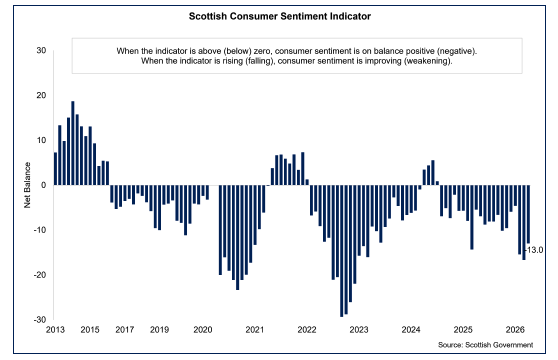

- The Scottish Consumer Sentiment Indicator reflects how people feel the economy is performing, how secure they feel about their household finances and how relaxed they feel about spending money.

- The Scottish Consumer Sentiment Indicator in May improved moderately after two months of weakening, with the indicator rising by 3.7 points to -13.0. The indicator is still notably negative and is 7.5 points lower than the series average.[10]

- All five of the sub-indicators remain in negative territory, however over the month, sentiment improved across four of the five sub-indicators, covering current and expected economic performance, expected household finances and spending attitudes. The remaining sub-indicator, covering current household finances, weakened over the month.

- The largest improvement in May was in the current economic performance sub-indicator (up 7.4 points), while the current indicator for household finances fell 2.9 points. The attitudes to spending and current household finances indicators were the weakest of the five sub-indicators in May, which continues to reflect the challenges facing household budgets.

Contact

Email: economic.statistics@gov.scot