Publication - Research and analysis

Scottish economic bulletin: January 2026

Provides a summary of latest key economic statistics, forecasts and analysis on the Scottish economy.

Consumer Activity

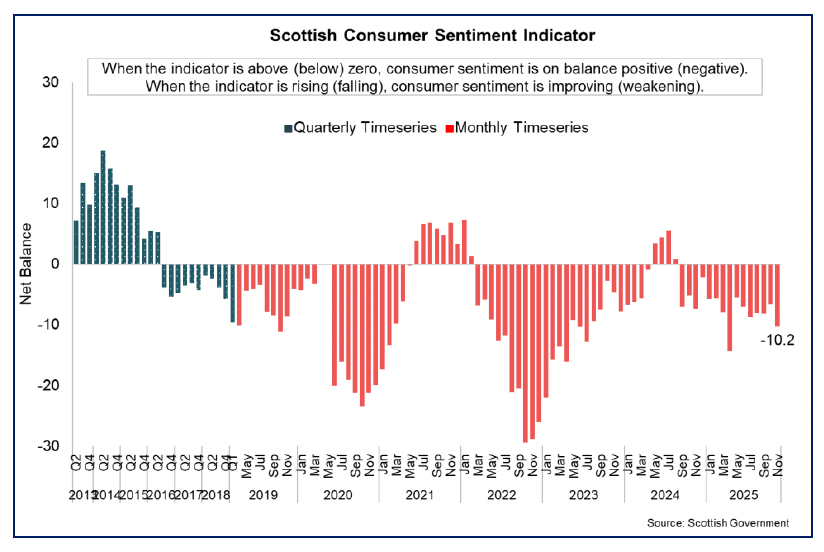

The Scottish Consumer Sentiment Indicator fell by 3.6 points in November to -10.2.

Consumer Sentiment

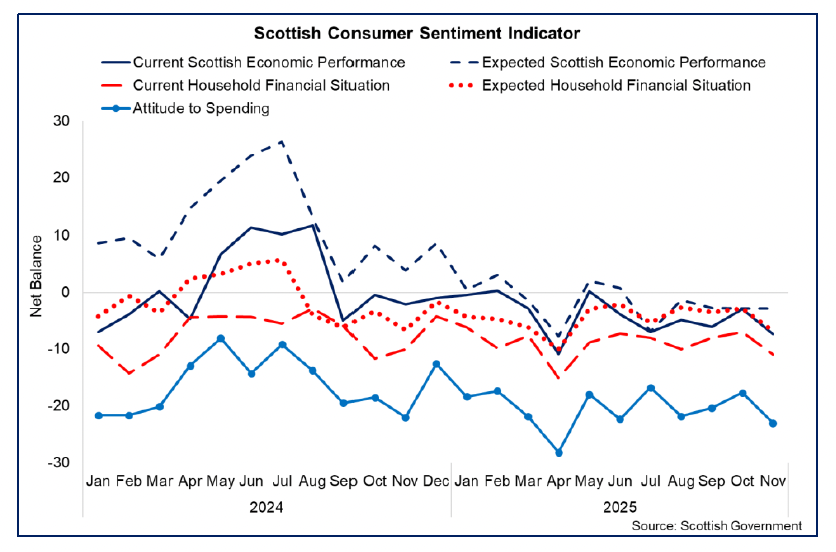

- The Scottish Consumer Sentiment Indicator (SCSI) reflects how people feel the economy is performing, how secure they feel about their household finances and how relaxed they feel about spending money.

- In November, the consumer sentiment net balance fell over the month to -10.2, weakening from -6.6 in October, and is 2.9 points lower than in November 2024. Consumer sentiment is also at its lowest level since April 2025.[21]

- The fall in sentiment over the month was driven by a decline in performance across four of the five sub-indicators, most notably those measuring current economic performance and attitudes to spending, which were down by 4.4 and 5.4 points, respectively. Sub-indicators measuring current and expected security of household finances also softened, both falling by 4 points respectively. All four of these indicators have fallen to their lowest level since April 2025. The remaining sub-indicator, measuring expected economic performance remained unchanged from October.

- More recently at a UK level, the GfK Consumer Confidence Index rose by 2 points in December to -17 with consumers reporting slightly improved confidence around economic and personal financial conditions. That said, the index was unchanged compared to December 2024, similarly indicating that consumer sentiment remains subdued.[22]

Spending and Cost of Living

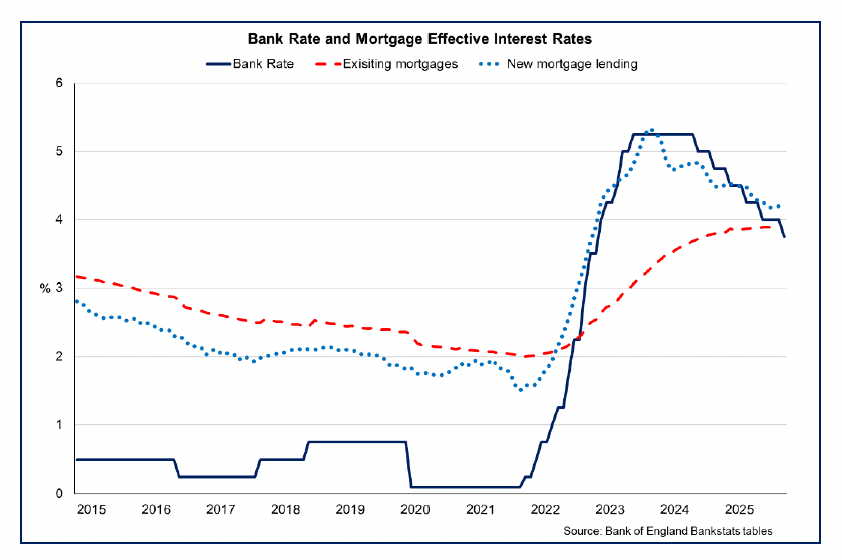

- The slight easing in inflation expectations and the reduction in interest rates are supportive of conditions for stronger consumer and household activity growth, however cost of living challenges and weakness in consumer sentiment are continuing to weigh on activity.

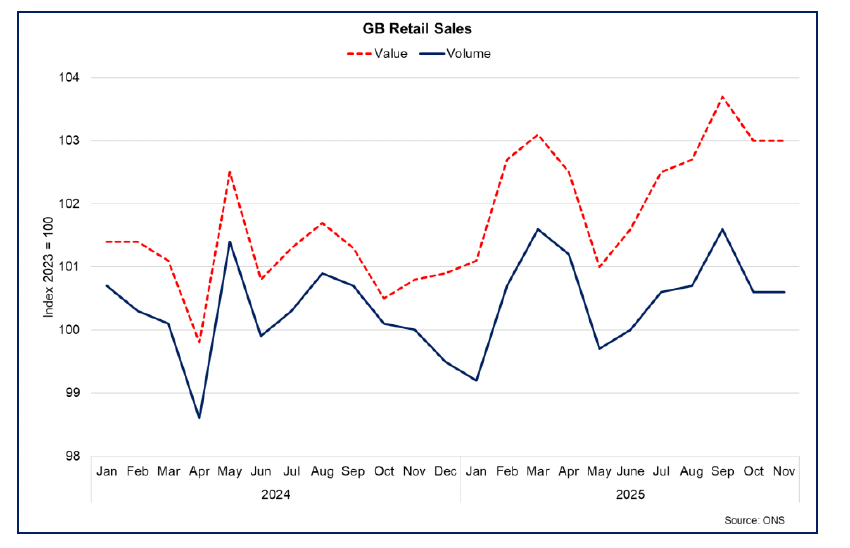

- At a GB level, retail sales growth eased slightly in the 3-months to November to 0.5% in volume terms (0.9% in value terms) though strengthened on an annual basis to 0.7% (2.3% in value terms). [23]

- The gradual loosening in monetary policy over the past year is progressively feeding through the economy. The effective interest rate on new mortgages has been on a downward trend, albeit increased slightly in November to 4.2% (up from 4.17% in October, though down from 4.5% in November 2024) while the effective rate on the stock of existing mortgages picked-up slightly to 3.9%.[24]

- However, while inflation is forecast to come down from its current rate, consumers continue to face cost pressures. The energy price cap increased slightly by 0.2% in January to £1,758 per year for a typical household who use electricity and gas and pay by direct debit, although is expected to fall in April when levies on energy will be met from taxation rather than energy bills.[25]

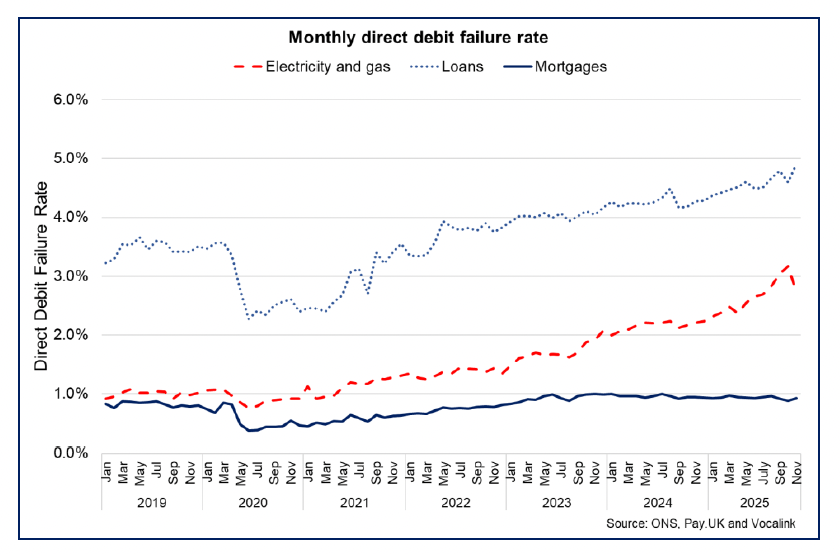

- At a GB level, direct debit failure rates due to insufficient funds data show that the failure rate for electricity and gas payments fell for the first time since April 2025 to 2.73% in November, down from 2.98% in October and its lowest rate since June. However, it remains higher than in November 2024 (2.21%). [26]

- Direct debit failure rates for loans also remain elevated increasing in November to their highest rate in 2025 (4.91%, up from 4.60% in October). Failure rates for mortgage payments remain relatively low, however, the rate rose in November to 0.93%, up from 0.89% in October.

Contact

Email: economic.statistics@gov.scot