Publication - Research and analysis

Scottish economic bulletin: January 2026

Provides a summary of latest key economic statistics, forecasts and analysis on the Scottish economy.

Business Conditions

Business activity remained subdued in December and cost pressures edged up.

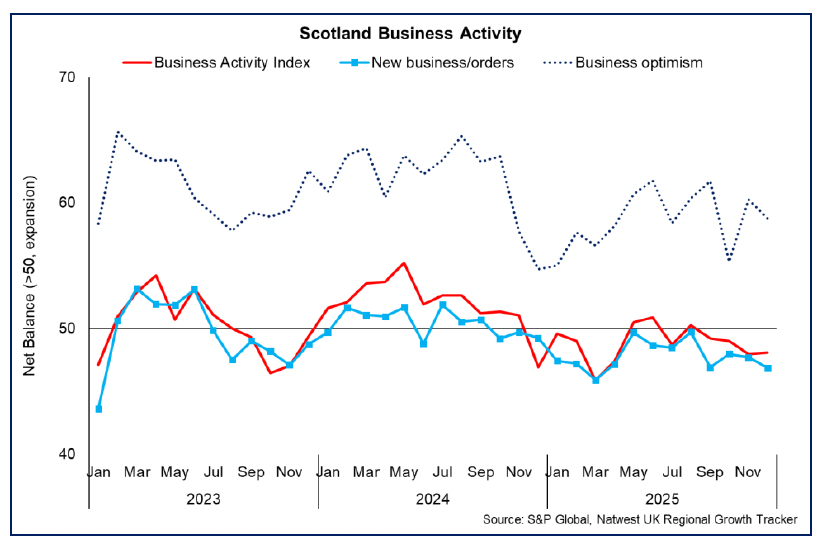

Business Activity

- Business surveys for the final months of 2025 indicate that business activity remained subdued towards the end of the year with businesses continuing to face challenging demand conditions and cost pressures.

- The latest RBS Growth Tracker business survey indicates that business activity contracted for a fourth consecutive month in December, with the index rising marginally to 48.1 (a reading below 50 indicates contracting business activity). The fall in activity was underpinned by ongoing weakness in new business orders, which fell for a fifteenth consecutive month, with businesses citing market uncertainty and tighter client budgets.[6]

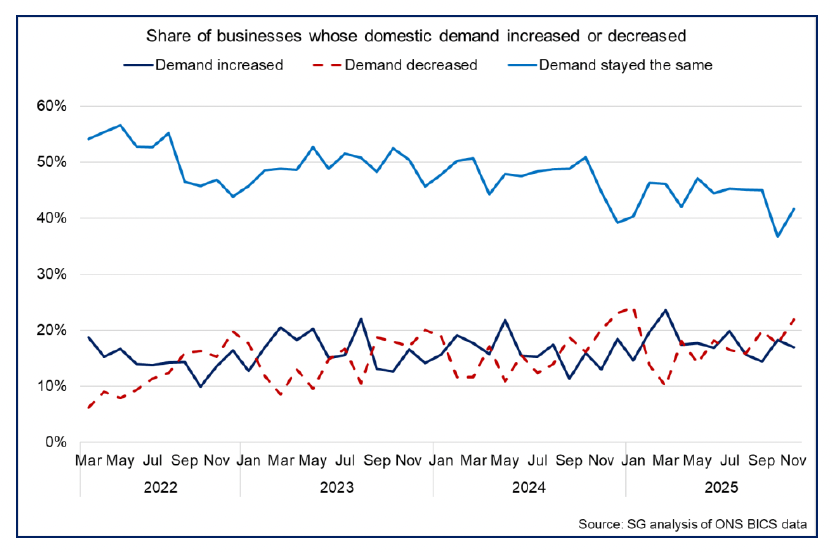

- Data from the latest BICS survey up to November also indicates weakening in demand conditions towards the end of the year with an increasing share of businesses reporting that domestic demand fell from the previous month (21.9%, up from 17.6% in October). The share of businesses reporting that demand increased over the month fell from 18.3% to 17.0%, while the share reporting demand was unchanged rose from 36.6% to 41.6%.[7]

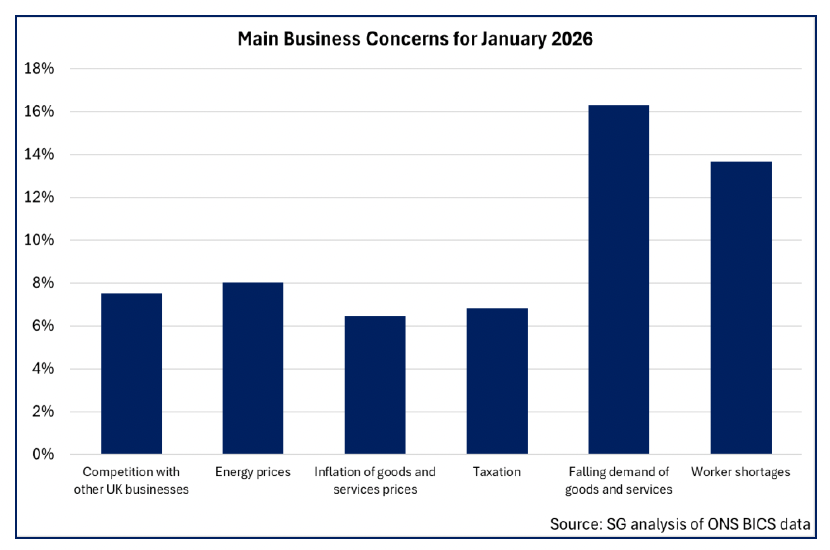

Business Concerns

- Key business concerns over 2025 were falling demand, taxation, and competition with other domestic businesses, with concerns over worker shortages increasing at the end of the year and into January.

- BICS data for January shows that falling demand of goods and services continues to be the most commonly cited concern by businesses in Scotland (16.3% of businesses, up from 14.7% in December) followed by worker shortages (13.6%, up from 10.4% in December).

- Taxation as a reported concern fell for December and January (with 6.8% of businesses reporting it as a main concern for January) after remaining broadly stable around the UK Autumn Budget. The share of businesses reporting competition with other businesses as a main concern also fell for January (7.5%, down from 10.0% for December).

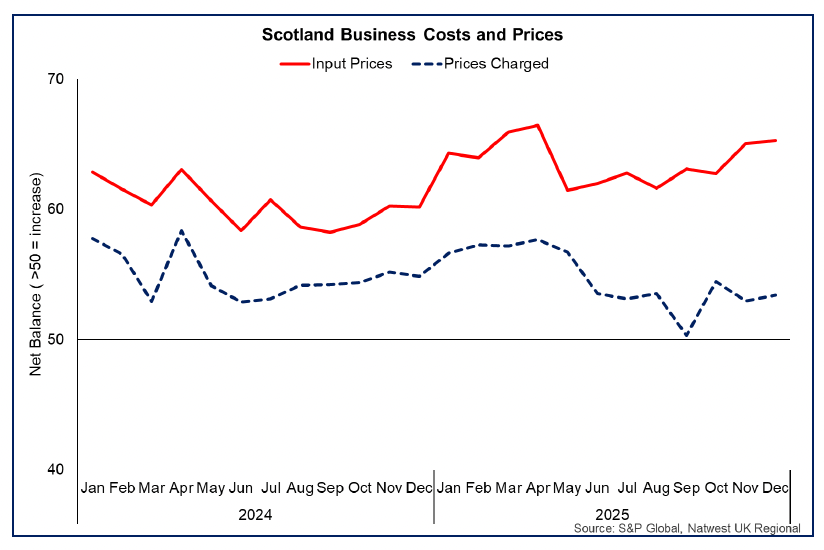

Business Costs

- The latest RBS Growth Tracker business survey indicates that business cost pressures continued to increase in December with the input price inflation indicator rising to its highest level since April 2025. Output prices also continued to rise, with the pace of inflation picking up from that seen in November, suggesting a move by some businesses to protect margins, albeit in the face of subdued demand conditions.[8]

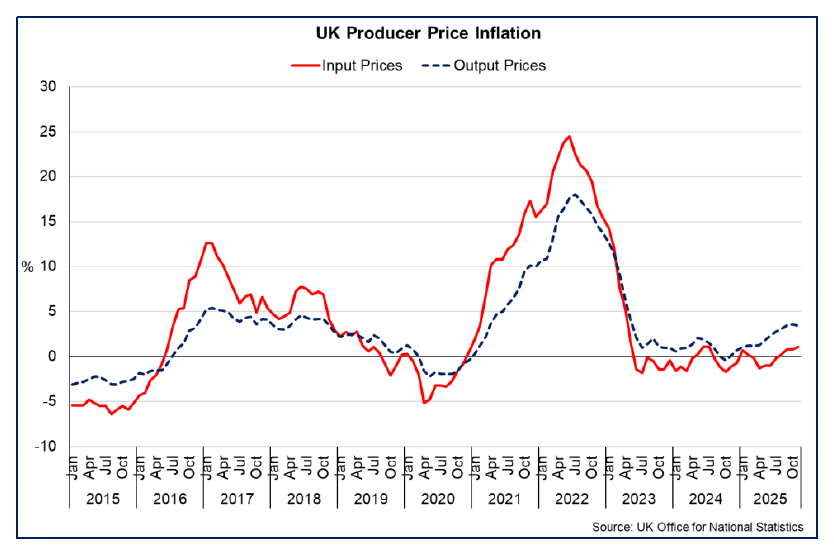

- This challenge is also reflected in latest ONS Producer Price Inflation (PPI) data, which indicates that producer output price inflation eased slightly in November (3.4% from 3.6% in October), while input price inflation picked up to 1.1% (from 0.8% in October). [9]

- Nonetheless, the move to protect margins is indicated in latest BICS indicators, which show that the proportion of businesses expecting the prices of their goods and services to rise, rose notably in January to 22.9%, up from 9.7% in December; its highest share since May 2025. However, challenging demand conditions means that not all business are passing through costs. 57.1% of businesses expect the price of their goods and services to stay the same while 1.4% expect their prices to fall.

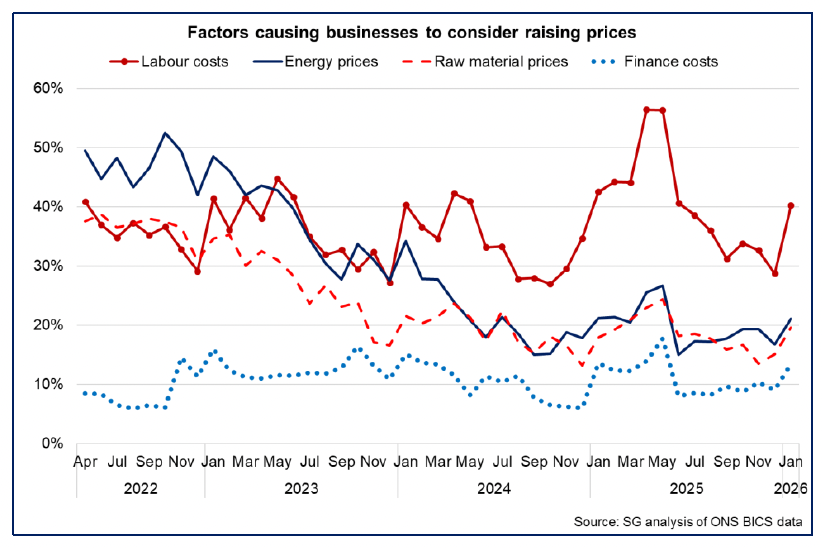

- Labour costs continue to be the main factor causing businesses to consider price increases, and rose from 28.7% in December to 40.2% for January, its highest rate since June 2025. This is followed by energy prices (21.1%, up from 16.8% for December) and raw material prices (19.6%, up from 15.1% for December).

Business Optimism

- Despite current challenges, the RBS Growth Tracker shows that business optimism remained positive in December (58.5) with businesses on balance expecting growth in the year ahead, albeit that this had moderated slightly from November.[10]

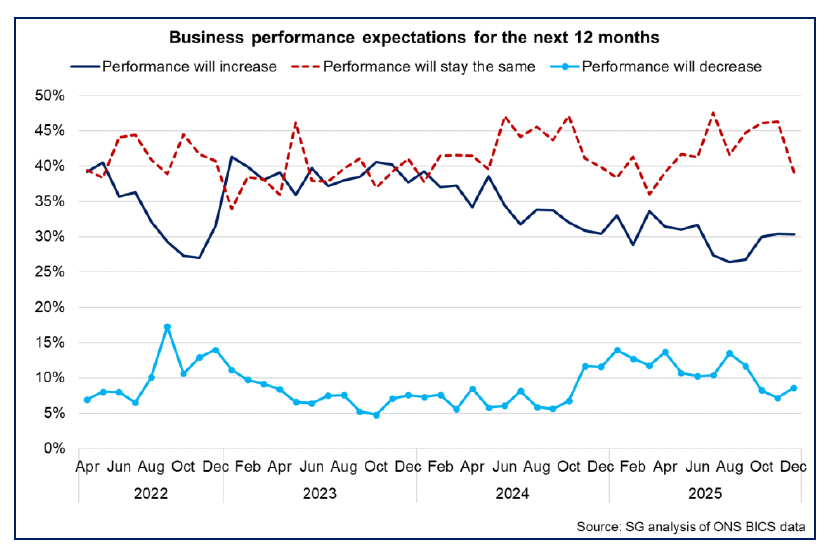

- Latest BICs data also indicates a slight easing in optimism in December with the share of businesses expecting performance to increase over the next year (30.3%) broadly unchanged from November, while the share of businesses expecting performance to decrease rose moderately to 8.7%. However, the largest share of businesses continue to expect performance to remain unchanged (39.1%, down from 46.3% in December).

Contact

Email: economic.statistics@gov.scot