Scotland's Fiscal Outlook: The Scottish Government's Medium-Term Financial Strategy

This is the fifth Medium-Term Financial Strategy (MTFS) published by the Scottish Government and provides the context for the Scottish Budget and the Scottish Parliament. This context will also frame the Resource Spending Review.

3. Scotland's Spending Outlook

The purpose of this chapter is to provide an update on the overall spending outlook and its component parts, including:

- The Resource Spending Outlook;

- The Capital Spending Outlook; and,

- Key drivers of spend such as pay and demand-led social security

3.1 Resource Spending Outlook

The MTFS sets out the economic and fiscal outlook for the next five years, providing the necessary context for spending plans. The RSR, published alongside this MTFS, sets out the full detail of our plans and the multi-year portfolio spending envelopes that will enable public bodies and other delivery partners to work with the Scottish Government to plan effectively for the future.

The RSR sets out the high-level parameters for resource spend within future Scottish Budgets up to 2026-27. It offers a strategic funding framework for the Scottish Government and our many partners to plan for the future. It is planned on the basis of the central funding scenario set out in chapter 2; a reasonable estimate of the funding likely to be available over the next five years. The RSR examined all areas of the Scottish Government's spending programmes within the challenging and volatile economic and fiscal context outlined above. The result is a set of multi-year spending envelopes which are set out in Table 10.

| 2022-23 £m | 2023-24 £m | 2024-25 £m | 2025-26 £m | 2026-27 £m | |

|---|---|---|---|---|---|

| Constitution, External Affairs and Culture | 294 | 314 | 294 | 294 | 294 |

| Crown Office and Procurator Fiscal Service | 170 | 170 | 170 | 170 | 170 |

| Deputy First Minister and Covid Recovery | 43 | 43 | 43 | 43 | 73 |

| Education & Skills | 2,927 | 2,943 | 2,943 | 2,963 | 3,472 |

| Finance & Economy | 553 | 556 | 561 | 566 | 629 |

| Health and Social Care | 17,106 | 17,550 | 17,995 | 18,536 | 19,029 |

| Justice and Veterans | 2,839 | 2,839 | 2,839 | 2,954 | 2,969 |

| Net Zero, Energy and Transport | 1,633 | 1,669 | 1,704 | 1,793 | 2,088 |

| Rural Affairs and Islands | 881 | 879 | 879 | 884 | 885 |

| Social Justice, Housing and Local Government | 15,235 | 16,237 | 16,890 | 17,274 | 17,769 |

| Scottish Parliament and Audit Scotland | 122 | 122 | 122 | 122 | 122 |

| Total | 41,802 | 43,322 | 44,440 | 45,599 | 47,500 |

The drivers of public spending identified in section 3.3 illustrate the variable and growing demands on funding over the spending review period. The December 2021 MTFS compared the Scottish Government's central funding scenario with a mid-spending projection. This suggested a growing gap between funding and spending which could reach approximately £3.5 billion in 2026-27. At the extremes, the low funding compared with the high spending trajectory illustrated an estimated gap of approximately £10.3 billion in 2026-27, while a high funding combined with a low spending trajectory gave a £3.7 billion surplus.

The Resource Spending Review responds to this challenge, which has been exacerbated by rising inflation and the cost of living crisis, and sets out the parameters for the Government's spending plans to 2026-27. The RSR shows how the Government will direct spend to its strategic outcomes, supported by a focus on efficiency and reform in public services.

3.2 Capital Spending Outlook

3.2.1 National Infrastructure Mission

The National Infrastructure Mission (NIM), announced as part of the 2018 Programme for Government, is a commitment to increase annual investment by 1% of 2017 Scottish GDP, £1.5 billion, by the end of this Parliament.

The NIM was introduced with an aim of raising Scottish infrastructure investment to internationally competitive levels; boosting broadband, transport, and low-carbon energy; and supporting inclusive economic growth. This level of investment in vital economic and social infrastructure will protect and create jobs in the short term, and support growth and productivity in the long term.

3.2.2 Capital Spending Review

The Scottish Government has published a refresh to the CSR originally published in February 2021, in light of a lower than expected capital settlement from the UK Government curtailing its spending plans, the cost of living crisis and the ongoing pressure facing the construction sector relating to market conditions and the establishment of the new Scottish Government in 2021 with an increased commitment to tackle global climate and nature emergencies.

The refreshed CSR demonstrates that the Scottish Government remains committed to the principles and themes set out in the Infrastructure Investment Plan, enabling the transition to net zero and environmental sustainability, boosting inclusive economic growth, and building resilient and sustainable places, as well as taking forward the recommendations of the Infrastructure Commission for Scotland.

The refresh also provides the opportunity to ensure that Capital and Resource budgets are well aligned behind projects and programmes, enabling successful delivery against the Scottish Government's priorities set out in the RSR.

Table 11 shows high-level funding and financing plans over the CSR period. This demonstrates that the Scottish Government is on target to successfully deliver against the National Infrastructure Mission (NIM), with £34 billion of investment over the 5-year spending review period.

The NIM previously assumed between £250 million and £450 million of capital borrowing would be required annually to ensure sufficient investment to support economic growth. In light of the increasing volatility in the construction sector as well as uncertainty arising from late consequentials we have amended our capital borrowing policy, as set out in section 4.2.3. This will take account of additional consequentials and changes to the phasing of capital programmes as a result of market conditions and supply chain impacts, which are anticipated to continue to impact on the construction industry. The revised policy has allowed additional capital to be allocated across 2023-24 to 2025-26. This will allow extra funding for key commitments which drive forward climate change ambitions, support economic recovery and tackle child poverty.

The refreshed CSR now sets out Financial Transaction (FTs) allocations for both 2023-24 and 2024-25, following confirmation of these allocations in the UK Spending Review in October 2021. Approximately £400m of further FTs is anticipated following an adjustment from prior years, with the profile still to be agreed with HM Treasury.

| 2019-20 NIM Baseline | 2020-211 | 2021-22 | 2022-23 | 2023-24 | 2024-25 | 2025-26 | 5 Year (2021-22 - 2025-26) Total | |

|---|---|---|---|---|---|---|---|---|

| Capital Grant 2 | 4,105 | 4,909 | 5,582 | 5,329 | 5,574 | 5,498 | 5,7183 | 27,701 |

| Capital borrowing 4 / Consequentials | 450 | 200 | 150 | 4505 | 450 | 450 | 450 | 1,950 |

| Financial Transactions 6,7 | 652 | 400 | 552 | 582 | 521 | 513 | 1308 | 2,298 |

| Revenue Finance | 90 | 65 | 55 | 335 | 520 | 690 | 609 | 2,209 |

| Total Investment | 5,297 | 5,574 | 6,339 | 6,696 | 7,065 | 7,151 | 6,907 | 34,158 |

| Audit Scotland modelled NIM trajectory (rounded) | 5,500 | 5,700 | 6,000 | 6,200 | 6,500 | 6,800 | 31,200 |

1 Outturn figures

2 Capital grant figure includes UK Capital Allocation, Additional Whitehall Transfers, Estimated Capital Receipts, Fossil Fuel Levy in 2022-23 only.

3 Modelled figure

4 Capital borrowing policy assumes £450 million of annual funding will be available through borrowing, the Scotland Reserve and Barnett consequentials of which £250 million will initially be assumed to be capital borrowing.

5 Excludes £118 million of carry forward from 2021-22 to avoid overstating as outturn figures for 2021-22 are not available yet.

6 Includes FT Consequentials and FTs Recycled and excludes Reserve drawdown.

7 Includes additional £400m of FTs with 200m in 2023-24 and £200m in 2024-15, with profile to be agreed with HMT.

8 There is currently no UK FT Allocation for 2025-26. Therefore figure is solely FTs recycled

The revenue-financed investment noted in the table above includes Growth Accelerators, Green Growth Accelerators the Learning Estates Investment Programme and the potential deployment of the Mutual Investment Model, which are described in detail in the previous MTFS published in December 2021[19]. In light of the current construction market volatility and the knock on impacts on project timelines, the figures have been revised to reflect the latest estimates. Although there has been a decrease in the forecast deployment of revenue finance over the CSR period, the updated Capital Borrowing policy and the increased deployment of Financial Transactions, at a lower servicing cost than Revenue Finance, ensure the Scottish Government is still on target to successfully deliver against the National Infrastructure Mission.

The Scottish Government is committed to sustainable deployment of revenue financed investment and capital borrowing to ensure there is no undue financial burden on future policy choices. That is why the Scottish Government has a self-imposed revenue finance investment limit of 5% of the Scottish Government resource budget excluding social security. The latest modelling suggests that over the remaining capital spending review period these costs peak in 2025-26 with planned and committed projects and borrowing costs estimated to be 2.61% of the resource budget excluding social security.

3.3 Risks to the spending outlook

Chapter 4 sets out the range of risks to the spending outlook that we face such as increasing social security expenditure, increased demand on the health service due to an ageing population, public sector pay, and inflationary pressures which would have to be funded entirely from the Scottish Budget envelope. This presents a significant risk given the Scottish Government's limited ability to borrow and transfer resources between years. The section below provides an analysis of the biggest drivers of expenditure to illustrate the pressures on the spending outlook.

3.3.1 Demand-led social security spend volatility

Social Security expenditure is the third biggest spending area in the Scottish Budget, following health and local government. Expenditure on social security benefits is variable, as it is determined by the number of eligible people who apply for support, all of whom must be paid at the rate set in the respective policy. Budget allocations are based on SFC forecasts rather than spending limits, and the Scottish Government will have to meet social security expenditure as it arises, even if it differs from the SFC forecast used to set the initial Budget.

The demand-led nature of payment introduces in-year volatility and uncertainty to the Scottish Budget. The SFC reported a 3% variation from their original forecast for 2020-21[20], which, if replicated in 2022-23, would amount to over £125 million, as the SFC's updated forecasts expect that social security expenditure will be almost £4.2 billion in 2022-23[21]. Social security expenditure is forecast to rise progressively to £6.5 billion by 2026-27.

The Social Security BGAs should also be considered alongside the forecasts of social security expenditure. In 2022-23 approximately 86% of social security benefits expenditure will be funded through BGAs. Social Security expenditure exceeding the BGAs over the RSR period reflects both divergent policy choices of the Scottish and UK governments, as well as economic differences which impact certain benefits. Changes in either UK Government policy relating to benefits, or the OBR's forecasts of benefit demand in the rest of the UK will affect the funding available to the Scottish Government through the Social Security BGAs.

Changes between actual and forecast Scottish expenditure, and the BGA reconciliations, are managed by the Scottish Government's budget management processes, in line with the principles and policies on the use of borrowing and reserve powers as set out in Chapter 4. Further information on the BGAs and reconciliations is set out in Annex B.

The continuing economic and social impacts of COVID-19 recovery and the cost of living crisis adds to the volatility risk associated with benefits expenditure. Disability benefits, which make up the majority of benefits expenditure, have been affected by COVID-19 but are expected to be less impacted by the wider macroeconomic environment except through the uprating of benefit amounts. Any additional expenditure arising as a result of volatility will have to be managed within the limits of the Scottish Government's existing fiscal powers. In Scotland, all benefits expenditure is funded through the overall Resource budget, as opposed to AME (Annually Managed Expenditure), which is the case in England and Wales.

Existing borrowing powers can help manage in-year volatility risk for social security and tax, however these powers have strict annual and overall borrowing limits. As part of the 2021-22 Budget, the Scottish Government had to manage reconciliations which exceeded its borrowing limits, with analysis suggesting that this could happen again. The Scottish Government is committed to building a social security system with dignity, fairness and respect at its heart. Social security is a key part of the Scottish Government's national mission to tackle child poverty and provides vital financial support to households, including those struggling as a result of the cost of living crisis. To support the real terms value of Scottish Benefits, the Scottish Government has uprated eight Scottish benefits by 6% from 1 April 2022 – almost double the September 2021 CPI rate of 3.1%. In addition, to specifically support low-income families with children, the Scottish Child Payment has been doubled from £10 per week per eligible child to £20 – and will further increase to £25 per week when the benefit is rolled out to eligible children under 16 by the end of 2022.

As a result of Scottish Government policy choices, such as delivering the Scottish Child Payment[22]– which is not funded through any additional adjustments from the UK Government – and the launch of new benefits to replace corresponding Department of Work and Pensions (DWP) benefits in Scotland, there is expected to be a growing divergence between the level of funding received from the UK Government (UKG) and the SFC's forecasts of devolved social security expenditure in Scotland. This additional investment will need to be funded entirely from the Scottish Budget envelope.

3.3.2 Public Sector Pay

Pay accounts for over £22 billion of resource expenditure across the devolved public sector (including Local Government). The Scottish Government pay and reward policies[23] apply directly to 50 public bodies and act as a reference point to other devolved public sector workforces (including Health, Teachers, Police, Fire and Further Education Colleges), albeit they have no formal locus in respect of setting Local Government pay. Over the coming years, certain public services will continue to expand, including new Social Security functions and the response to social care demand. As a result, we anticipate that parts of the public sector in Scotland will continue to grow.

The Scottish Government is committed to exploring with Trade Unions and employers further opportunities for developing non-pay benefits. Work has been ongoing to consider standardising the 35 hour working week across public bodies where the pay policy directly applies, to introduce the right to disconnect and where possible to explore a 4-day working week. In the longer term, this could be an opportunity to limit the cost burden of pay awards to employers, act as a lever to improve productivity, and optimise the role of automation and digitalisation of services, all while creating high value job opportunities and contributing to the wellbeing economy.

In designing pay policy, the Scottish Government must balance economic, fiscal and social factors, including:

- The changes to the cost of living – CPI inflation reached 9% in April 2022, and the Bank of England in its latest Monetary Policy Report estimate it could reach 10% later in 2022;

- The effect of the recent 1.25 percentage points increase to National Insurance Contributions for employees and employers;

- The fact that average pay in the public sector has been higher than in the private sector in recent years, with the ONS estimating that the modelled average public sector earnings premium was 7% in 2019; and,

- The continued improvement in labour market conditions . The number of payrolled employees is now above pre-pandemic levels, having fallen around 3% during 2021.

The affordability of pay uplifts, and recognition of performance across public services, contribute to a fair but fiscally sustainable approach to public sector pay. This is crucial given it is equivalent to half of the Scottish Government resource budget.

The 2022-23 Public Sector Pay Policy continues the progressive principles of recent years. Specifically, it outlined a cash uplift of £775 for public sector workers earning up to £25,000, £700 for workers earning between £25,000 and £40,000, and £500 for those who earn above £40,000 alongside the adoption of a new £10.50 public sector wage floor – building on the impact of the real Living Wage.

In addition to the main single-year pay deal option, the 2022-23 Policy offers the option for public sector bodies to choose a multi-year approach, connected to public service reform and broader changes to terms and conditions.

To illustrate the potential future paybill costs across the devolved public sector, we have modelled three theoretical public sector pay award scenarios – which exclude pension costs (see Table 12)

| Baseline | |||||

|---|---|---|---|---|---|

| (2022-23) | 2023-24 | 2024-25 | 2025-26 | 2026-27 | |

| Illustration of 1% pay award | |||||

| Total | 22.1 | 22.3 | 22.5 | 22.8 | 23.0 |

| Additional cost including Basic Award | 0.2 | 0.2 | 0.2 | 0.2 | |

| Illustration of 2% pay award | |||||

| Total | 22.1 | 22.5 | 23.0 | 23.5 | 23.9 |

| Additional cost including Basic Award | 0.4 | 0.5 | 0.5 | 0.5 | |

| Illustration of 3% pay award | |||||

| Total | 22.1 | 22.8 | 23.4 | 24.1 | 24.9 |

| Additional cost including Basic Award | 0.7 | 0.7 | 0.7 | 0.7 | |

Note: This is the cost of the basic award including employer pension contributions and National Insurance costs. The paybill costs include all bodies within the Scottish Devolved public sector.

3.3.3 Growth in the public sector workforce

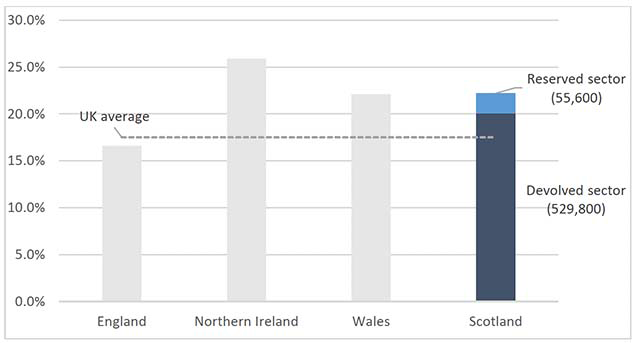

The size and distribution of the workforce in the devolved public sector directly influences the Scottish Budget position. As of 2021 Q3, 585,400 individuals worked in the public sector, representing around 22.2% of all Scottish workers. Around 47% of these public-sector workers are in Local Government and 33% in the NHS. The Scottish public sector is proportionally larger than the UK average of 18% of the total workforce.

Public Sector Employment (Office for National Statistics); Public Sector Employment in Scotland (Scottish Government)

Over the last five years the number of workers in the devolved public sector has increased by around 1% per year on average. Over the coming years, we anticipate that parts of the devolved public sector in Scotland will continue to grow, alongside other parts that may shrink. But overall, we expect that without control measures in place, there would be a growing workforce carrying with it an increasing fiscal risk to the Scottish Budget.

To illustrate the potential future costs, based solely on historical trends on growth, we have modelled three scenarios based on assumptions around the pay award and future workforce growth.

| Baseline (2022-23) | 2023-24 | 2024-25 | 2025-26 | 2026-27 | |

|---|---|---|---|---|---|

| Low Scenario - 1% pay award, - 0.5% workforce growth | |||||

| Total | 22.1 | 22.2 | 22.4 | 22.7 | 22.9 |

| Difference from Central Scenario | -0.6 | -0.8 | -1.0 | -1.3 | |

| Central scenario - 2% pay award, 1% workforce growth | |||||

| Total | 22.1 | 22.8 | 23.2 | 23.7 | 24.2 |

| High Scenario - 3% pay award, 2.5% workforce growth | |||||

| Total | 22.1 | 23.1 | 24.0 | 24.8 | 25.5 |

| Difference from Central Scenario | 0.6 | 0.8 | 1.1 | 1.3 | |

Note: This is the cost of the basic award including employer pension contributions and National Insurance costs. The paybill costs include all bodies within the Scottish Devolved public sector. The central scenario of 1% workforce growth is based on the average previous five-year growth of the Scottish Devolved public sector.

In order to mitigate workforce pressures in the current fiscal and economic climate, all public sector employers will need to innovate further and take robust decisions about priorities and service design.

The RSR has introduced measures to reset the pay and workforce expectations, by announcing a broad aim to freeze total paybill costs – as opposed to pay levels - at 2022-23 levels, and a pathway to return the overall size of the public sector workforce to around pre-Covid levels, while supporting expansion in key areas of service delivery.

3.3.4 Public Service Pensions – a mandatory workforce cost

Within the UK, policy is largely reserved to Westminster in respect of public sector pensions and wholly reserved in respect of state pensions, private sector pensions, and pensions taxation policy. Public sector pensions are an important element of current and future obligations for the Scottish Budget. Pension scheme membership is provided as part of public servants' terms and conditions, and the Scottish Government remain committed to public service pensions that are affordable, sustainable and fair to Scotland's public servants and the communities they serve.

Pension scheme expenditure is demand-led and volatile, in that it is more difficult to control than other types of expenditure. For instance if more scheme members retire in a given year than forecasted, the amount of cash flow top-up required can increase, thereby creating an additional budget pressure that needs to be funded. While the cash flow risk for the NHS and Teachers' schemes rests with HM Treasury (scoring as annually managed expenditure in the Scottish Budget), the risk for the Police and Firefighters' schemes rests with the Scottish Government as it is funded through the discretionary Resource budget.

UK Government decisions on overarching policies, such as the discount rate used to value scheme liabilities as part of quadrennial scheme valuations, affect the cost of Scottish public service pension schemes. In the medium term, the upcoming round of public service pension scheme valuations – the 2020 scheme valuations – is the next event that could change pension costs for employers participating in the Scottish NHS, Teachers', Firefighters' and Police pensions schemes, and those in Scotland participating in the reserved Civil Service and Judicial pension schemes.

The employer pension contribution rates set by the 2016 valuations and implemented in 2019-20 will remain in effect for these schemes until new rates are set and implemented from 1 April 2024, providing a level of certainty in the meantime, with costs ultimately being determined by workforce demographics and pay awards. Given the potential for a new discount rate to be used in the 2020 scheme valuations, to be set by HM Treasury in due course, there is a risk that the new contribution rates will be higher than the current rates, with potentially significant budget implications for employers and portfolios that might need to be met without additional funding from the UK Government. Given the contingency of this budget management risk on UK Government decisions, the Scottish Government continues to engage closely with HM Treasury and others to inform our on-going risk management and related planning.

Contact

Email: sophie.osborn@gov.scot