Scotland's Fiscal Outlook: The Scottish Government's Medium-Term Financial Strategy

This is the fifth Medium-Term Financial Strategy (MTFS) published by the Scottish Government and provides the context for the Scottish Budget and the Scottish Parliament. This context will also frame the Resource Spending Review.

1. Scotland's Economic Outlook

This chapter provides an update on the latest state of the Scottish economy; a summary of the latest economic forecasts from the SFC and OBR and what these imply for the Scottish Budget; how the Scottish Government is acting to promote economic recovery from the COVID-19 pandemic; supporting households and businesses following the UK's exit from the EU and during the cost of living crisis; all whilst continuing progress towards the delivery of the Scottish Government's National Outcomes[6].

1.1 State of the Economy

The Scottish economy is facing new challenges, with rising inflation placing significant pressure on households, businesses and public services. The economy has shown resilience at the start of 2022 with GDP growing 1.1% and 0.4% in January and February respectively, having rebounded sharply from the fall in output in December at the start of the Omicron wave and is now 1.3% above its pre-pandemic level in February 2020. The removal of remaining COVID-19 restrictions in April marked an important stage in the domestic recovery although risks to the recovery are heightening, with the latest data showing the UK economy shrinking by 0.1% in March as higher prices started to weigh on trade in the wholesale and retail sector.[7]

Scotland's labour market continues to perform strongly with unemployment falling to 3.2% in the period December to February, while the payroll employee level[8] has risen sharply and is now 29,000 above its pre-pandemic level. High vacancy rates and recruitment challenges also continue to persist, creating upward pressure on starting salaries and average earnings growth.

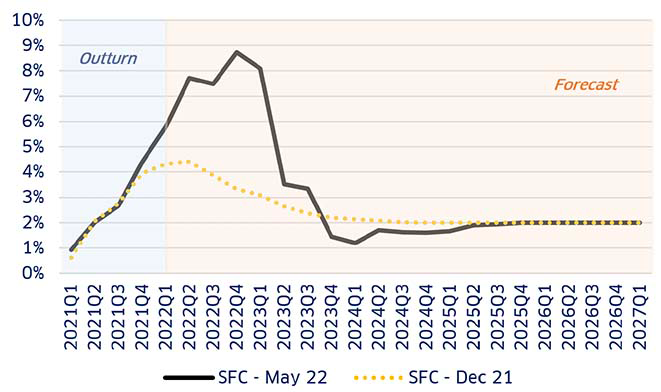

However, over the first quarter of 2022 inflationary pressures that began in 2021 have continued to strengthen with consumer price inflation (CPI) rising to a 40-year high of 9.0% in the 12 months to April and forecast to rise further. These pressures are beginning to be reflected in the latest economic data, such as the Scottish Consumer Indicator[9], which fell sharply across early 2022 due to the weakening sentiment regarding household finances, spending, and the outlook for the economy.

The economic impact of inflation is also disproportionately affecting those on lower incomes who tend to spend more of their income on energy bills where price increases have been particularly intense. The Institute for Fiscal Studies (IFS) estimates that the poorest 10% of households are facing a real inflation rate of just under 11%, relative to a real inflation rate of just under 8% for the richest 10% of households.[10]

Inflationary pressures have been exacerbated by the situation in Ukraine. Scotland's direct trade links with Russia and Ukraine are limited, and as such the direct impacts of the situation are expected to be small. However, the surge and volatility in the price of global commodities such as oil and gas, grains, and metals in which Russia and Ukraine are key global producers, means the indirect impact of higher inflationary pressures will affect all importing economies, including Scotland.

1.1.1 Latest Economic Forecasts of the Scottish and UK Economies

The latest forecasts for the Scottish economy reflect the economic developments that have occurred over the past 6 months. The SFC's forecasts mirror the latest inflation outlook of the OBR which sees the Consumer Price Index (CPI) growing at an average rate of 8% across 2022-23 which is double the rate of inflation forecast at the time of the Scottish Budget in December 2021.

Source: Scottish Fiscal Commission; Office for Budget Responsibility

The SFC continues to forecast a relatively robust labour market, with tight competition for workers keeping unemployment low by historic standards and staying close to 4% across the forecast horizon. However, over the medium term, forecasts of employment in Scotland will begin to decline reflecting the SFC's forecast reduction in the working age population in Scotland.

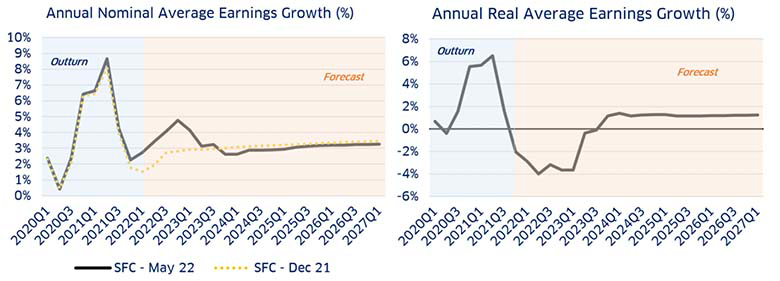

The SFC have also revised up their outlook for average earnings growth in 2022 as a tight labour market and higher levels of inflation increase employee bargaining power for further wage rises. However, the SFC do not expect average earnings growth to match the higher rates of inflation in the economy, resulting in real earnings, or the true purchasing power of earnings, falling sharply by an average of -2.7% across 2022-23.

Source: Scottish Fiscal Commission

As a result of the worsening employment and real earnings outlook, the SFC are now forecasting the largest fall in real household disposable income since records began in Scotland. The SFC have now downgraded their forecast for GDP growth in Scotland over the forecast horizon by an average of around 0.3 percentage points each year relative to their last GDP growth forecast in December 2021.

1.1.2 Fiscal Implications for the Economic Outlook

As set out in further detail in Chapter 2, the Scottish Budget is influenced by the relative performance of devolved tax revenues and social security expenditure. Consequently, differences between the Scottish and UK economic forecasts can have a material impact on the funding outlook for the Scottish Government.

As Table 1 shows, there are some significant differences in the economic outlook forecast by the SFC and OBR. Whilst both institutions have a very similar outlook on unemployment and a relatively similar outlook for earnings, the forecasters have a greater degree of disparity on the outlook for GDP and employment growth at the Scottish and UK level.

| 2022-23 | 2023-24 | 2024-25 | 2025-26 | 2026-27 | ||

|---|---|---|---|---|---|---|

| GDP growth (%) | SFC May-22 | 2.1 | 1.1 | 1.0 | 1.0 | 1.0 |

| OBR Mar-22 | 2.2 | 1.9 | 2.1 | 1.7 | 1.7 | |

| Employment growth (%) | SFC May-22 | 1.5 | -0.2 | -0.2 | -0.2 | -0.3 |

| OBR Mar-22 | 0.8 | 0.6 | 0.5 | 0.4 | 0.4 | |

| Unemployment rate (%) | SFC May-22 | 3.9 | 4.0 | 4.0 | 4.0 | 4.1 |

| OBR Mar-22 | 4.1 | 4.2 | 4.1 | 4.1 | 4.1 | |

| Consumer Price Inflation (%) | SFC May-22 | 8.0 | 2.4 | 1.7 | 2.0 | 2.0 |

| OBR Mar-22 | 8.0 | 2.4 | 1.7 | 2.0 | 2.0 | |

| Nominal average earnings growth (%) | SFC May-22 | 4.1 | 2.9 | 2.9 | 3.1 | 3.2 |

| OBR Mar-22 | 5.1 | 2.4 | 2.7 | 3.0 | 3.3 | |

| Real average earnings growth* (%) | SFC May-22 | -2.7 | 0.4 | 1.2 | 1.1 | 1.2 |

| OBR Mar-22 | -1.1 | -0.1 | 1.0 | 1.0 | 1.2 | |

*Please note that, in a similar methodology as the OBR, the SFC's real earnings forecast is calculated using their forecast of the Consumer Expenditure Deflator (CED) to deflate their nominal earnings forecast. CED is strongly correlated to, but slightly different than, their forecast of Consumer Price Inflation (CPI).

Source: Scottish Fiscal Commission; Office for Budget Responsibility

The SFC are forecasting rising productivity growth in Scotland, which is a key driver of living standards in the economy, citing Scotland as having one of the most educated workforces in the OECD and an internationally competitive level of research and development spend.

However, the SFC are forecasting that longer term demographic trends, for which key levers such as migration policy remain reserved, could dampen growth over the medium term. For example, the SFC forecast that low levels of net international migration will continue to contribute towards a shrinking working age population in Scotland. This falling working age population, combined with falling participation rates, in turn drives most of the gap in their forecasts of both employment and the potential size of the overall economy relative to the OBR's forecasts for the UK.

The SFC also raise the importance of sectoral risks. Since the devolution of significant tax powers to the Scottish Parliament, the Scottish Budget is now affected by the relative growth of tax revenue per person in Scotland and the rest of the UK. This is in turn determined by both economic factors and policy choices in both countries.

Chapter 2 goes into more detail on the latest funding outlook, however, there is some evidence that average earnings growth has been diverging between Scotland and the rest of the UK in recent years, driven in part by strong earnings growth in London. This is discussed in detail in Annex A, but is also a view shared by the SFC. They note that average pay in Scotland has been similar to that of most UK regions since tax devolution occurred but highlighted that London, and its significantly stronger earnings growth performance in sectors such as finance, has been a significant factor in the emerging average earnings gap between Scotland and the UK as a whole.

1.2 Delivering economic prosperity

One of the best ways to protect the Scottish Budget and support living standards across Scotland, is by growing the Scottish economy. The ambition of the Scottish Government's new 10-year National Strategy for Economic Transformation[11] is to build a wellbeing economy – one that is thriving across economic, social and environmental dimensions.

1.2.1 10-Year National Strategy for Economic Transformation (NSET)

The National Strategy for Economic Transformation contains a range of actions – within the powers currently available to the Scottish Government - to deliver economic prosperity for all of Scotland's people and places. It was informed by the Advisory Council for Economic Transformation[12], as well as by wide ranging engagement with businesses, unions and other stakeholders across Scotland.

The strategy offers a route to a stronger economy with good, secure and well-paid jobs and growing businesses; maximising Scotland's strengths and natural assets to increase prosperity, productivity and international competitiveness. It will build on Scotland's strengths in sectors like energy, financial services and life sciences, and carve out new strengths in technology, space and decarbonisation.

Five policy programmes have been chosen, based on rigorous analysis of evidence, to transform our economic model and drive improvement in Scotland's economy:

1. Creating a culture in which entrepreneurship is encouraged in every sector of the economy;

2. Capitalising on new market opportunities, such as the transition to net zero;

3. Improving productivity by boosting traditional and digital infrastructure and targeting regional inequalities;

4. Supporting and incentivising access to lifelong learning and training to ensure Scotland continues to have a skilled, competitive workforce; and,

5. Reducing inequality and poverty, and eradicating structural barriers that prevent participation in the labour market.

Since the launch of NSET in March 2022, we have been laying the foundations for delivering the Economic Transformation Plan as well as addressing some of the most immediate challenges. Successful delivery of the strategy will involve working together with people and organisations from all sectors of the economy. A robust governance structure, co-led by businesses, will hold the public sector and industry to account for delivery, strengthening accountability and transparency and ensuring that the right frameworks are in place to deliver on the actions and to measure success.

Source: Scottish Government - National Strategy for Economic Transformation

The strategy's programmes are interconnected and are a mutually reinforcing cycle, which will ultimately lead to higher living standards and a reduction in poverty. A higher wage, higher participation economy will also generate greater tax revenues, enhancing Scotland's financial sustainability

Overall, the National Strategy for Economic Transformation will help protect the Scottish Budget and improve Scotland's longer term fiscal sustainability by improving economic performance for Scotland. The strategy will help tackle long-term structural challenges and remove barriers to participation in the labour market so that everyone is enabled and empowered to participate in economic success.

Contact

Email: sophie.osborn@gov.scot